Mad Hedge Biotech and Healthcare Letter

April 16, 2026

Fiat Lux

Featured Trade:

(THIS BIOTECH MIGHT HAVE CRACKED THE UNDRUGGABLE CODE)

(RVMD), (MRK)

Mad Hedge Biotech and Healthcare Letter

April 16, 2026

Fiat Lux

Featured Trade:

(THIS BIOTECH MIGHT HAVE CRACKED THE UNDRUGGABLE CODE)

(RVMD), (MRK)

My barber Charlie has this uncanny ability to diagnose which of his clients are making money in the market just by watching how they tip.

Last Thursday, while he was working his magic on what's left of my hairline, he mentioned how his pharmaceutical rep clients have been tipping like oil sheiks lately.

"Something big is brewing in biotech," he said. That conversation got me thinking about Incyte Corporation (INCY).

You see, Charlie's pharmaceutical reps understand something most Wall Street analysts miss most of the time, and that’s the difference between flashy breakthrough drugs that grab headlines and the workhorses that generate consistent cash flow quarter after quarter.

Incyte falls squarely into that second category, except their "workhorse" just delivered Q2 2025 numbers that would make a racehorse jealous.

Digging deeper, I found where things get exciting, and why my neighbor's dermatologist probably drives a Porsche.

Incyte's Opzelura cream isn't just another skincare product - it's the first and only FDA-approved treatment for vitiligo in the United States. Think about that for a moment.

When you own the sole solution to a visible medical condition that affects millions, you've essentially discovered a legal monopoly that patients will pay for without batting an eye.

Revenue from this little tube of magic hit $164.5 million in Q2, climbing 38.6% quarter-over-quarter and 35.2% year-over-year.

But the real treasure lies in their emerging drug Niktimvo, which just posted sales of $36.2 million with a staggering 166% quarterly growth.

Meanwhile, the clinical data backing this drug shows 86% of patients with essential thrombocythemia achieving normalized blood counts.

For a condition affecting roughly 60,000 Americans, those efficacy rates suggest Incyte has another blockbuster hiding behind the boring medical terminology.

More impressively, the financial architecture of this company reads like a masterclass in pharmaceutical economics.

Their gross margin expanded to 55.9% while operating income margin hit 25.6%, a three-year high. On top of that, their total debt sits at just $42.4 million against EBITDA of $334.5 million.

That debt-to-EBITDA ratio of 0.04x is like having a mortgage payment of fifty bucks on a million-dollar mansion.

Now here's where Wall Street's myopia creates opportunity.

Everyone obsesses over Jakafi's patent cliff coming in 2028, treating it like some inevitable catastrophe. What they're missing is the patent protection story that extends well beyond that timeline.

Opzelura's patents don't expire until 2040, essentially giving Incyte a guaranteed revenue stream for the next 15 years.

The May settlement with Novartis (NVS) also cut their royalty payments in half, dropping cost of goods sold guidance to just 8-9% of revenues.

Every percentage point of margin expansion in a billion-dollar revenue company translates to serious money hitting shareholders' pockets.

The acquisition angle makes this story even more compelling.

Remember when Sanofi (SNY) swooped in and bought Blueprint Medicines for $9.5 billion in June?

Incyte trades at 13.8x forward earnings, roughly 24% below the sector median, with minimal debt, growing cash flows, and a diversified pipeline that includes povorcitinib and INCB123667.

They're essentially gift-wrapped for a strategic buyer. Those November 2024 rumors about Merck (MRK) sniffing around weren't idle gossip - they were reconnaissance missions.

What really seals this investment thesis is the momentum building behind their numbers.

Non-GAAP earnings per share hit $1.57, beating expectations by a nickel, while management raised Jakafi guidance from $2.95-3 billion to $3-3.05 billion for 2025.

The beauty of Incyte's transformation reminds me of watching a small-town hardware store evolve into a regional empire. They're systematically building a franchise that compounds value over time.

Trading at $84.61 with multiple growth catalysts, patent protection extending into the 2040s, and a strong balance sheet, this represents exactly the kind of overlooked opportunity that creates generational wealth.

My barber may think he's just cutting hair and making conversation, but his pharmaceutical rep theory just validated what decades of investing has taught me: find companies that solve real problems for real people, then hold on tight.

My next visit to Charlie's chair just might coincide with a very good mood and an even better tip.

Mad Hedge Biotech and Healthcare Letter

April 17, 2025

Fiat Lux

Featured Trade:

(THIS BIG PHARMA'S GRAND DIVORCE SHOWS PROMISE)

(NVS), (SDZNY), (MRK), (RHHBY)

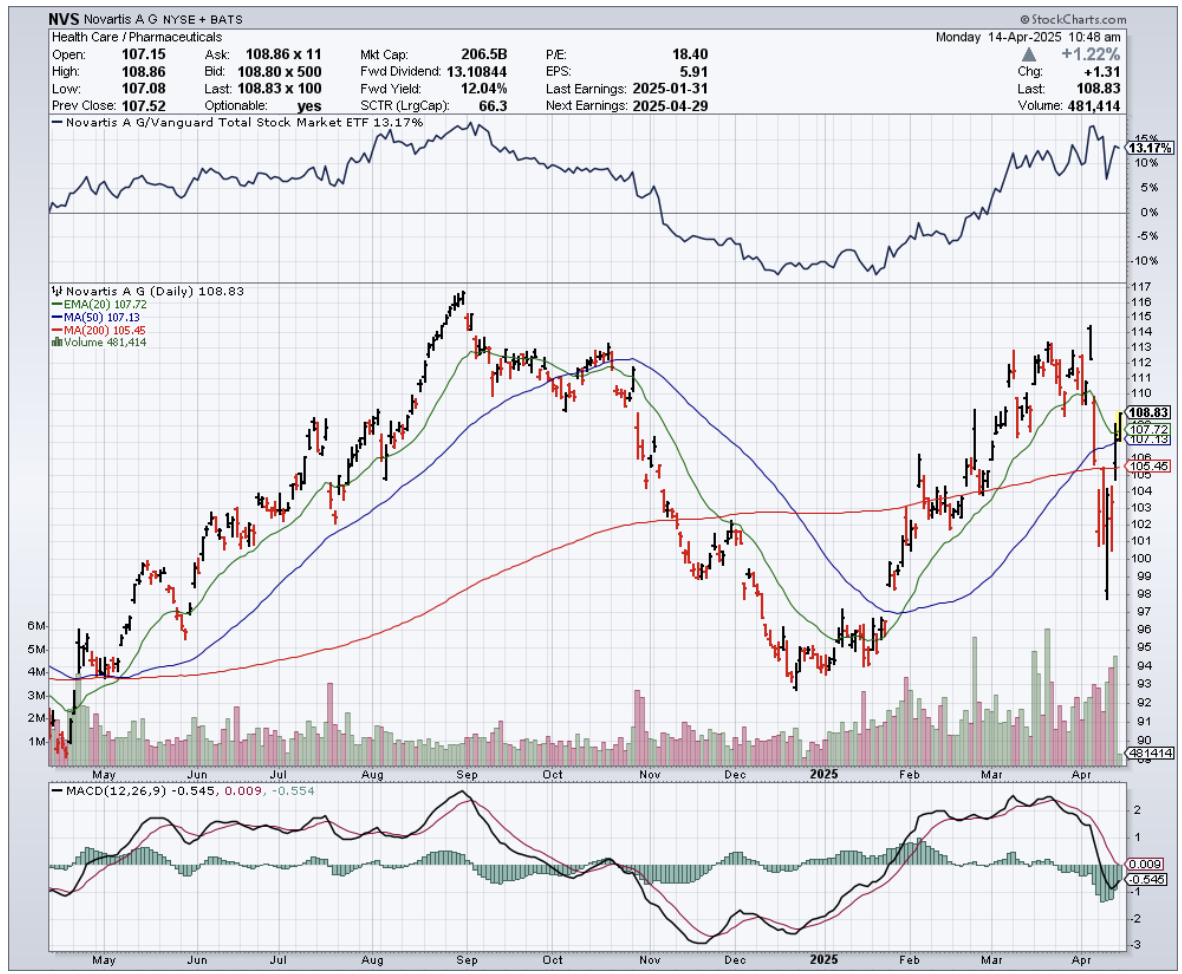

While most corporate breakups end with shareholders reaching for antacids, Novartis (NVS) investors are popping champagne instead.

The Swiss pharmaceutical giant's 2023 divorce from its generics business Sandoz (SDZNY) has transformed the company from a pharmaceutical conglomerate into a focused innovation machine – and the numbers would make even the most jaded among us whistle in appreciation.

I've watched pharmaceutical reorganizations for decades, and most resemble rearranging deck chairs on the Titanic. But Novartis has executed something genuinely transformative.

By jettisoning vaccines, ophthalmology, and generics, they've engineered a corporate metamorphosis that delivered 10% revenue growth to $51.7 billion in 2024.

Novartis now operates with laser focus on four therapeutic areas. Entresto, their heart failure medication, generated $7.8 billion in 2024 – up 31% year-over-year. That's roughly the GDP of Montenegro flowing from a single pill.

Cosentyx pulled in $6.1 billion (up 25%), while Kisqali and Kesimpta both jumped nearly 50%. These aren't merely drugs; they're annuities with patent protection.

The scale defies easy comprehension: nearly 300 million patients worldwide received Novartis medications in 2024. That's treating almost every American, then adding Japan for good measure. When pharma executives dream of market penetration, this is what they see before their alarm clocks rudely interrupt.

What separates Novartis from the pack is their capital allocation strategy. They're investing $9 billion annually in R&D – not throwing darts at a scientific board but methodically advancing a pipeline designed to replace blockbusters as patents expire.

Their 2024 acquisition of Chinook Therapeutics exemplifies this approach: precise, strategic, and focused on enhancing their nephrology portfolio rather than empire-building.

The geographic distribution of Novartis's revenue reveals similar strategic clarity. While 43% comes from the United States, their China strategy deserves special attention. Sales there surged over 20% in local currency during 2024.

Having tracked emerging markets throughout my career, I recognize the pattern – Novartis is positioning itself at the confluence of demographic shifts, increasing chronic disease prevalence, and expanding healthcare access.

For those who prefer hard numbers to market philosophy, Novartis delivered EBIT growth of 29% to $16.3 billion, with operating margins expanding to 31.55%. Net profit jumped to $11.9 billion, with margins at 23% – among the industry's highest.

Despite returning $15.9 billion to shareholders through dividends and buybacks, their balance sheet remains fortress-like.

Net debt stands at just $18 billion, with a Net Debt/EBITDA ratio below 1x – meaning they could extinguish their entire debt in less than a year with current cash flows.

Unlike pharmaceutical giants that bet everything on a single therapeutic area, Novartis has positioned itself as a formidable player across multiple high-value niches.

In oncology, rather than challenging Merck (MRK) or Roche (RHHBY) directly, they've developed unique assets like Pluvicto and Kisqali that face minimal head-on competition.

For cardiology, while Entresto faces patent expiration in 2025, they're already advancing next-generation therapies like Leqvio.

Meanwhile, the global prescription drug market exceeded $1.7 trillion in 2024 and should grow at 7.7% annually through 2030. Novartis has strategically positioned itself precisely where that growth curve steepens most dramatically.

No investment thesis is complete without acknowledging risks, and Novartis faces several significant challenges.

Entresto's patent cliff in 2025 creates a $7.8 billion revenue gap that needs filling. Cosentyx follows in 2027-2028.

Without Sandoz, they can't offset these losses with their own generics. Pricing pressure from Medicare and competition from other pharmaceutical giants present additional headwinds.

And pharmaceutical innovation remains inherently unpredictable – even with billions in R&D, clinical trials fail with alarming regularity.

Despite these concerns, Novartis shares still appear undervalued after rising nearly 19% over the past year.

The company trades at a P/E of 18.69x – substantially below the industry average of 55.91x. Its EV/EBITDA ratio of 10.97x represents a significant discount to peers.

Throughout my market-watching career, I've developed healthy skepticism toward corporate transformations. They typically generate more PowerPoint slides than actual results.

But Novartis has delivered tangible financial improvements that flow directly to shareholders. For those seeking healthcare exposure without betting on clinical-stage biotechs with binary outcomes, Novartis offers a compelling package of growth, income, and relative stability wrapped in Swiss precision. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

April 10, 2025

Fiat Lux

Featured Trade:

(THE $5 BILLION SECRET I SPOTTED IN MY DOCTOR'S WAITING ROOM)

(AMGN), (NVO), (LLY), (MRK), (REGN)

Last Tuesday, my orthopedist kept me waiting 40 minutes past my appointment time – just long enough for me to witness what Wall Street's finest analysts have somehow managed to miss.

As I sat thumbing through a dog-eared copy of Golf Digest from 2018, I counted eight different patients called in for Prolia injections.

By the sixth one, I'd put down the magazine and started taking notes on my phone. By the eighth, I was already mentally calculating position sizes for my portfolio.

"You know what you just saw?" my doctor asked when he finally saw me. "That's Amgen's cash cow – $5.4 billion in sales last year for a twice-yearly injection. And guess what? Half these patients will be on it for life."

When I pressed him on competing drugs, he just laughed. "Their sales reps bring the best lunches. But seriously, it works, patients tolerate it, and insurance covers it. In medicine, that's the holy trinity."

While half of Wall Street hyperventilates about which pharmaceutical giant will dominate the weight loss market, and the other half chases whatever shiny tech story came out this morning, they're all missing Amgen (AMGN) – a money-printing machine trading at just 14.9 times earnings with a 3.1% dividend that grows like clockwork.

I've been investing in pharmaceutical companies since I covered Merck's (MRK) explosive growth for The Economist in the late 1970s, and one lesson has remained constant: the market consistently underestimates companies with proven track records during transitions.

Amgen, trading at $307, is a textbook example of this phenomenon right now.

The headline numbers don't initially spark excitement – management is guiding for modest 5% revenue growth and 4% EPS growth this year. But having analyzed hundreds of pharma companies over five decades, I know these conservative guidance figures are often the prelude to significant outperformance.

What matters more is their $5.9 billion R&D investment last year (up 25% from 2023) and the underappreciated potential of their pipeline.

Look beyond the surface, and you'll find Amgen has quietly built something remarkable. While everyone's fixated on Novo Nordisk’s (NVO) Ozempic and Wegovy, few have noticed that Amgen's existing product portfolio is delivering solid results.

Inflammation drug TEZSPIRE grew 71% year-over-year and is approaching the $1 billion annual sales milestone. Oncology drug BLINCYTO jumped 41%, and their cholesterol drug Repatha, combined with bone health treatment EVENITY, delivered $1 billion in year-over-year growth.

The real hidden value lies in Amgen's obesity program. The anti-obesity market that barely existed a few years ago has exploded to $2.2 billion and is projected to grow at 30% annually through 2030.

Eli Lilly (LLY) and Novo Nordisk have seen their market caps soar into the stratosphere on the strength of their GLP-1 drugs, but Amgen's market valuation doesn't reflect any meaningful potential from MariTide, their Phase 3 obesity candidate.

This reminds me of 2012 when I began accumulating Regeneron (REGN) while the market was completely missing the potential of Eylea. That position delivered a 580% return over the following three years.

What's particularly attractive about Amgen is the margin of safety it offers. With a 3.1% dividend yield (backed by a manageable 45% payout ratio and 13 consecutive years of growth), a forward P/E of just 14.9, and a fortress-like 46.3% operating margin, you're being paid to wait for the pipeline to deliver.

The company has been aggressively paying down the debt from its Horizon Therapeutics acquisition, reducing long-term obligations by $6.6 billion last year alone.

Their financial discipline stands in stark contrast to many of the speculative biotech plays I've been pitched recently. At a dinner with venture capitalists in Boston last week, I listened to presentation after presentation about pre-clinical assets with billion-dollar valuations and no revenue in sight.

Meanwhile, Amgen generated $33.4 billion in sales last year with industry-leading EBITDA margins of 45%.

Of course, there are risks. The upcoming patent expiration of osteoporosis drug Prolia this year creates a revenue gap that needs filling.

The Trump administration's Department of Government Efficiency (DOGE) initiative could potentially impact FDA testing labs, slowing approval timelines. But these concerns are already priced into the stock, while the potential upside from MariTide and other late-stage candidates is not.

Having navigated multiple market cycles since the 1970s, I've learned that the best investments often come when solid companies are temporarily overlooked during market rotations. Amgen remains a proven pharmaceutical innovator with strong cash flows, growing dividends, and a promising pipeline that offers compelling value.

I started building a substantial position in Amgen at around $260 during the post-election pharmaceutical sell-off and have continued to accumulate shares on weakness.

With a reasonable valuation, strong pipeline optionality, and dividend income that beats 10-year Treasury yields, Amgen represents the kind of steady compounder that has consistently outperformed over full market cycles.

In my decades of investing, I've found that buying excellent businesses during periods of unwarranted pessimism is the closest thing to a guaranteed winning formula.

With Amgen, you're essentially being paid a 3.1% annual dividend to own a company that could deliver a major surprise in the obesity market – the same market that transformed Novo Nordisk and Eli Lilly into two of the world's most valuable companies.

Sometimes the smartest investments are like colonoscopies – nobody's excited to talk about them at parties, but they'll save your financial health in the long run.

Mad Hedge Biotech and Healthcare Letter

March 27, 2025

Fiat Lux

Featured Trade:

(NO SHERPA REQUIRED)

(MRK), (BMY)

Perched high above the timberline on Colorado's Mt. Elbert last weekend, I found myself short on oxygen and long on questions—namely, which pharmaceutical heavyweight deserves a spot in my portfolio: Merck (MRK) or Bristol-Myers Squibb (BMY)?

At 14,438 feet, the air thins out fast, but the thinking gets clearer. Clarity tends to arrive when your brain’s running at 60% capacity.

I’d stuffed my pack with company reports, earnings transcripts, and a few too many granola bars—one of which was being stalked by a very persistent marmot as I paused to catch my breath. I must’ve looked like an underprepared Everest hopeful, hunched over charts and trying to find altitude-adjusted alpha.

On paper, both firms dominate the oncology space and have made a career out of telling cancer where to shove it. But markets don’t care about reputations—they care about margins, pipelines, and who's going to make it through the next patent cliff without blowing out their kneecaps.

Let’s start with the money.

Merck posted Q4 2024 revenue of $17.76 billion, up 6.77% year-on-year. Its price-to-sales ratio sits at 3.74x—above the sector median, but still 14.7% cheaper than its own five-year average. It’s also beaten revenue expectations for 12 straight quarters. That’s not a hot streak. That’s clinical precision.

Bristol-Myers pulled in $12.34 billion last quarter with 7.5% YoY growth, but it trades at a much lower 2.51x P/S. That’s a discount—16.5% under the sector median. Ten out of twelve quarters beating the Street is nothing to sneeze at either. You get the sense both firms have their accounting departments on creatine.

Debt? Merck sits on $24.6 billion in net debt, but with a net debt/EBITDA ratio of 0.84x, it's practically sipping debt through a paper straw. Bristol-Myers, on the other hand, carries $40.1 billion with a 2.07x ratio. Still manageable, but not the kind of leverage that makes you sleep like a baby—unless you're the baby in question.

Dividends? Bristol-Myers pays more—4.14% vs. Merck’s 3.42%. That might earn it a second glance from income hawks, but when you zoom out, Merck still wears the financial crown.

Now here’s where things get messier.

Merck has a bit of a single-product addiction problem. Keytruda brought in $7.83 billion last quarter, making up a jaw-dropping 50.2% of total revenue. It's a blockbuster, yes, but when one drug makes up half your business, you start looking like a biotech version of Jenga. Merck’s top five products represent 75.7% of sales.

Bristol-Myers shows better balance. Eliquis is its biggest hitter, pulling in 25.9%, while its top five products account for 71.6% overall. Not exactly ironclad diversification, but a more even spread than Merck’s lineup.

Still, Keytruda is a monster. It outsold Bristol’s Opdivo by a whopping $5.4 billion in Q4 alone. That’s not a competition—that’s a beatdown. But both companies are running out the clock on their oncology flagships. Keytruda loses U.S. patent protection in 2028. Merck’s answer is a subcutaneous version—MK-3475A—patent-protected until 2039. Bristol’s already fired back with Opdivo Qvantig, a smart preemptive strike that could buy them time and market share.

Pipelines? Merck leads here too. BMY has 74 active R&D projects, 11 in Phase 3. Merck? Over 90 clinical-stage assets, 31 of them in Phase 3, and five are already under regulatory review. They’re not just defending Keytruda—they’re building the next dynasty.

Meanwhile, Bristol-Myers’ stock is flashing overbought signals like a Christmas tree. Merck, by contrast, trades below its VWAP, and Wall Street sees an 18.3% upside from here. Bristol-Myers? A yawn-worthy 1.36%. That's a rounding error, not an investment thesis.

Fast forward to 2029. I expect Merck to print a non-GAAP EPS of $11, led by Keytruda, Welireg, and a few wild cards currently in late-stage trials. Bristol-Myers might reach $6.80 EPS on $44 billion in revenue. Not bad, just... not Merck.

After sorting through this on the summit—between water breaks, altitude headaches, and one increasingly assertive marmot—the picture came into focus. Merck is the better long-term pick. They’ve got the product, the pipeline, the margin, and the momentum.

As I packed up and started the long descent, I dropped my guard for half a second and the marmot made his move—snatched my energy bar right off my pack. Bold little bastard. But honestly, he earned it.

Sometimes, the one who climbs higher sees further and waits patiently gets the prize. Merck just did all three.

After all, in investing—as in mountain climbing—peaks and profits favour those who don’t lose their breath or their nerve.

Mad Hedge Biotech and Healthcare Letter

March 20, 2025

Fiat Lux

Featured Trade:

(EVEN A PIG COULD MAKE MONEY HERE)

(OGN), (MRK), (RHHBY), (BAYRY), (PFE), (AZN)

I was camped out in Kyiv the other month when news of Organon's (OGN) earnings hit my phone.

While Russian drones buzzed overhead, I was studying pharmaceutical balance sheets—talk about surreal. Did I mention I've led a strange life?

In mid-February, Organon pleasantly surprised me with Q4 2024 results. Hadlima, their biosimilar to Humira, rocketed to $44 million in quarterly sales, up 83.3% year-on-year.

Meanwhile, Organon's dividend yield sits at a whopping 7.32%, blowing away the healthcare sector average.

Let me be blunt: this is an income investor's dream hiding in plain sight.

Organon emerged in 2021 when Merck (MRK) spun off its women's health, biosimilars, and off-patent drugs businesses. This allowed Merck to focus on its immunology and oncology pipeline while Organon became a pure-play commercial entity.

These spinoffs often create enormous value that the market misses in the early years.

Organon's share price has been trading sideways since early 2025 despite several wins: commercializing Hadlima, acquiring Dermavant, and maintaining a 23% operating margin even as some medications face generic competition.

The market clearly isn't paying attention. When stocks with this kind of dividend yield maintain solid margins, my antennae start twitching.

Their recent Phase 3 ADORING 3 study showed that even 79.8 days after stopping Vtama treatment, atopic dermatitis remained mild. That's patient retention gold, folks.

When patients can stop medication and still see benefits almost three months later, that's the kind of sticky customer base pharmaceutical execs dream about.

Revenue hit $1.59 billion in Q4 2024, down just 0.63% year-over-year but up 0.63% quarter-over-quarter.

Renflexis sales reached $64 million, down 16.9% due to competition from other Remicade biosimilars and superior new medications like AbbVie's (ABBV) Skyrizi.

But here's where things get interesting—this sales decline was expected and already priced in. Organon isn't being valued in Renflexis's future.

The real stars? Nexplanon and Vtama. Nexplanon sales reached $258 million in Q4, up 11.7% year-on-year.

Even better, its patent protection runs until August 2030. CEO Kevin Ali expects it to "comfortably get beyond $1 billion in 2025."

When a CEO uses words like "comfortably" about billion-dollar projections, I tend to listen.

Vtama, acquired in the $1.2 billion Dermavant purchase, brought in $12 million in partial Q4 sales.

The FDA expanded its label in December 2024 to include atopic dermatitis in patients over age 2—a condition affecting 31.6 million Americans. This approval significantly expands its market potential.

Remember, blockbuster drugs don't announce themselves with trumpets—they sneak up on you through expanded indications and growing prescriber bases.

Now, many folks will point to Organon's debt—$8.36 billion at 2024's end. But that's lazy analysis.

Look deeper and you'll see its net debt/EBITDA ratio improved from 5.01x to 4.74x over 12 months. They're steadily strengthening their financial position.

I've watched this happen before with pharma spin-offs—initial debt concerns gradually fade as strong cash flows tackle the balance sheet.

Management knows what they're doing. For 2025, they forecast a slight revenue dip but improved EBITDA margins of 31-32%, outperforming competitors like Perrigo, Alvotech, and Amneal.

In the broader pharmaceutical landscape, Organon competes with heavyweights like Roche (RHHBY), Ferring Pharmaceuticals, Bayer (BAYRY), Pfizer (PFE), and AstraZeneca (AZN)—but with a more specialized focus that gives them maneuverability these giants lack.

Wall Street's average price target is $20.50, suggesting a 33.9% upside. When was the last time you saw a 7.32% dividend yield with 33.9% upside potential?

I project non-GAAP EPS to reach $4.52 by 2029, slightly above analyst estimates, driven by Hadlima, Nexplanon, and Vtama growth, plus upcoming biosimilars HLX14 and HLX11. My friends at major healthcare funds are starting to take notice, but the broader market hasn't caught on yet.

At $15.31 per share, Organon trades at a non-GAAP P/E of 3.39x—80.8% below the sector median and 25.7% below its 5-year average. That's not just cheap—that's backing up the truck cheap.

You know what they say about bears and bulls making money, while pigs get slaughtered? Well, at these valuations, even a pig could make money on Organon.