Global Market Comments

June 8, 2026

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD or THE TOP IS IN)

(SOXX), (IGV), (XLV), (XLRE), (XLF), (XLK), (TLT),

(USO) (SLV), (UPS), (GLD), (SLV), (MSTR)

Global Market Comments

June 8, 2026

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD or THE TOP IS IN)

(SOXX), (IGV), (XLV), (XLRE), (XLF), (XLK), (TLT),

(USO) (SLV), (UPS), (GLD), (SLV), (MSTR)

Global Market Comments

June 4, 2026

Fiat Lux

Featured Trade:

(LOOKING AT THE LARGE NUMBERS UPDATED)

(TLT), (TBT) (BITCOIN), (MSTR), (BLOK), (HUT)

Global Market Comments

May 11, 2026

Fiat Lux

Featured Trades:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THE FOG OF INVESTMENT),

(META), (NVDA), (AMD), (MU) (AMZN), (GOOGL), (AAPL), (NVDA), (AVGO) (XLF), (XLV), (XLF), (XLV), (OWL), (APO), (MSTR), (C), (MS), (DHI), (XLV), (IBB)

Global Market Comments

March 13, 2026

Fiat Lux

Featured Trade:

(MARCH 11 BIWEEKLY STRATEGY WEBINAR Q&A),

(USO), (UUP), (BITO), (MSTR), (SDS), (PLTR), (VST), (MOS)

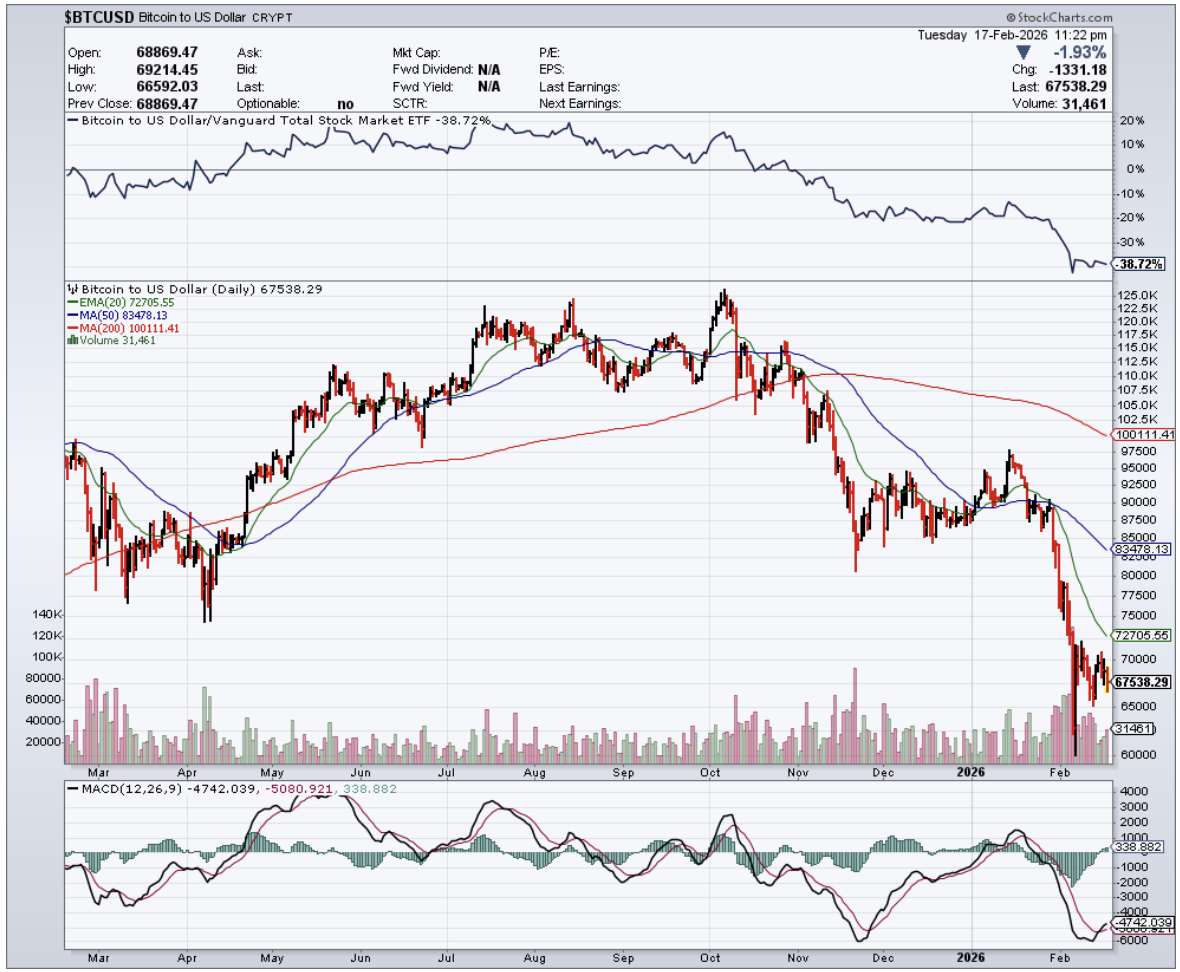

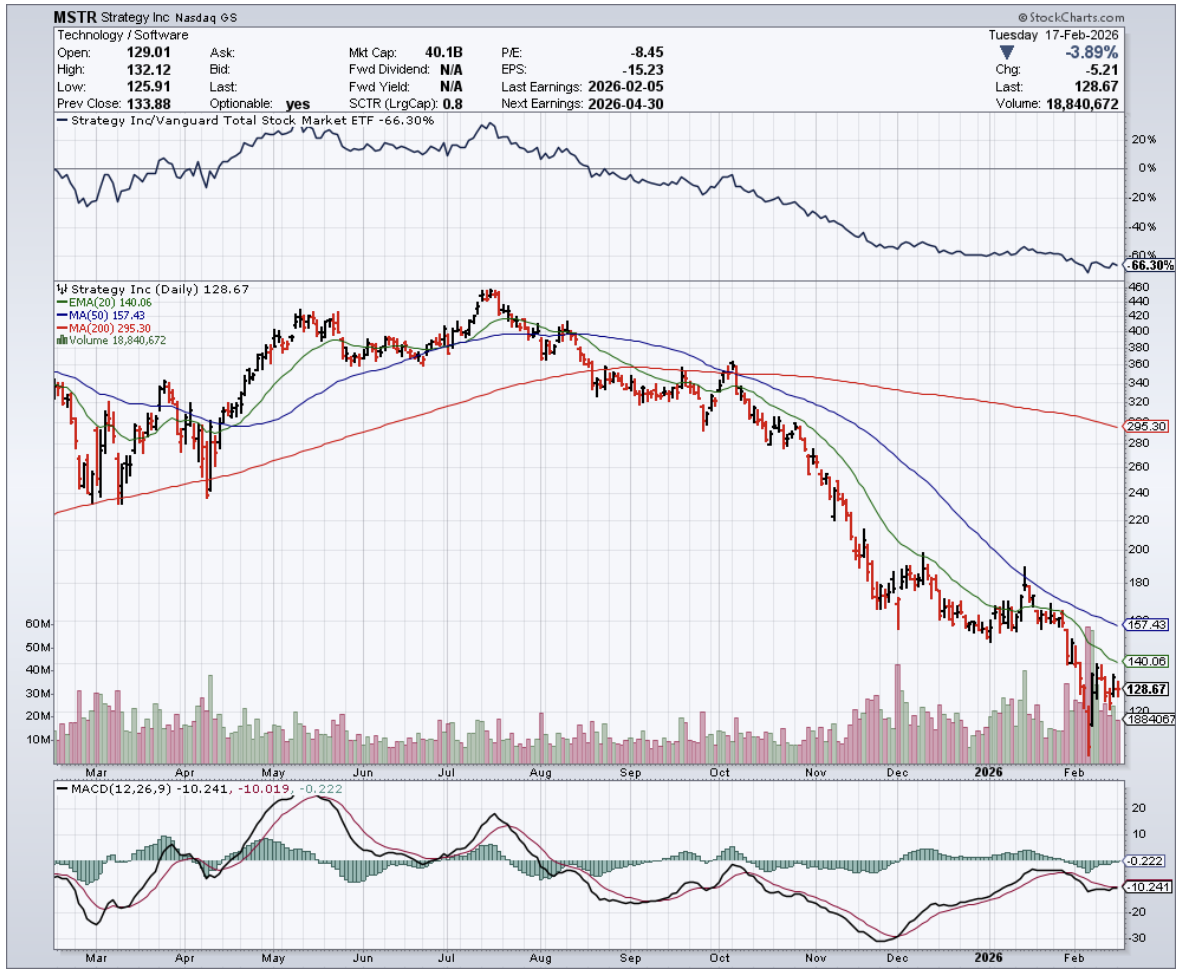

Strategy's (MSTR) carrying $8.2 billion in debt, most of it convertible, with $2.25 billion in cash reserves and over 714,000 Bitcoin (BTC) on the balance sheet.

The CEO says Bitcoin would need to drop to $8,000 and sit there for five years before they'd have a real problem.

The bears say this is a leveraged disaster waiting to implode. The bulls say it's genius financial engineering. I say the numbers tell a more interesting story than either camp wants to admit.

The company started life as a business intelligence software firm. That business still exists, quietly generating revenue in the background, but nobody's pricing MSTR on software fundamentals anymore.

Michael Saylor transformed the company into a publicly traded Bitcoin treasury, and the stock now trades purely on Bitcoin exposure.

When Bitcoin rises, MSTR typically outperforms. When Bitcoin falls, MSTR drops harder. That's the whole trade - leveraged upside and amplified downside.

Three metrics cut through the noise better than any price chart.

Forced liquidations show you when leveraged positions are getting washed out beyond fundamental value.

Long-term holder behavior reveals whether Bitcoin believers are actually holding or quietly heading for exits.

Bitcoin ETF flows tell you when institutional money managers think the worst is over.

I track all three because they separate actual risk from perceived panic.

Forced liquidations matter because MSTR's leverage amplifies Bitcoin moves in both directions. When Bitcoin drops sharply, margin calls force leveraged traders to sell, creating declines beyond fundamentals.

November 2025 and mid-January through early February 2026 saw forced liquidations soar, bringing steep dives exceeding normal corrections. MSTR's share price reflects these exaggerated moves.

Long-term holder data provides the second metric. As of February 10, holders with Bitcoin for over ten years control 17.2% of the supply. Combined holders from 1 to 10 years account for another 30.8%.

Nearly half the Bitcoin supply is held by people who've demonstrated multi-year conviction. These holders don't contribute to volatility - newer entrants trading Bitcoin as one asset class among many create the price swings.

Bitcoin ETF flows round out the picture. From January 16 through early February, outflows far surpassed inflows. Since February 6, inflows have consistently exceeded outflows. If that continues, it signals fund managers believe the worst may be over.

The debt structure deserves a closer look. Most of the $8.2 billion is convertible notes with no collateral requirements and no forced liquidation risk.

The company holds $2.25 billion in cash, providing roughly 2.5 years of dividend coverage for preferred shares.

CEO Phong Le said Bitcoin would need to stay at $8,000 through 2032 before debt coverage becomes a problem. Saylor said if issues arise, they'd refinance.

Whether that's possible in a distressed scenario is unknowable, but it's at least 6 years away under pessimistic assumptions.

The preferred stock structure adds complexity. MSTR issued multiple classes paying 8% to 11.25% dividends.

As the company pays these, the $2.25 billion cash reserve depletes. When that happens, they'll likely issue more common shares, creating predictable dilution that investors can model.

Between 2023 and early 2024, you could write "AI" in a presentation and ride the thematic wave.

Bitcoin-exposed stocks traded with roughly 80% correlation - buy any name, and you get the same trade. That correlation dropped to approximately 20%.

The market stopped treating Bitcoin plays as a basket and started differentiating between companies that can actually monetize exposure versus companies just burning cash.

MSTR's getting repriced as investors figure out whether leveraged Bitcoin accumulation with convertible debt makes sense.

I'm bullish on both Bitcoin and MSTR.

The leveraged structure means MSTR outperforms Bitcoin on the upside. The debt structure is more defensible than bears claim, and the runway extends further than most investors realize.

MSTR trades as a binary bet.

You either believe Bitcoin appreciates over time despite volatility, or you think the growth trajectory is unsustainable, and this is capital looking for a place to die.

There's no middle ground.

The emotional intensity around both Bitcoin and MSTR tells me most investors are making decisions based on where they bought rather than what the balance sheet shows.

The framework for navigating this is pretty straightforward.

Track forced liquidations to identify when price moves exceed fundamentals. Watch long-term holder behavior to gauge conviction among true believers.

Monitor ETF flows for signs that institutional money thinks we've seen the worst. Free cash flow, leverage structure, and whether the company's actually accumulating Bitcoin per share (not just in absolute terms) round out the analysis.

Companies selling stock during panic create some of the best buying opportunities of the decade, provided the balance sheet can survive to benefit.

MSTR's balance sheet suggests more runway than the disaster scenarios imply. Whether Bitcoin hits $8,000 and sits there for five years remains to be seen.

But if you're waiting for that scenario to invest, you've already made your bet.

Global Market Comments

February 9, 2026

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ICEBERGS AHEAD)

($VIX), ($SPX), (AMZN), (KRE), (XLP), (XLI), (IAT), (TAN), (XLK), (HOOD), (MSTR), (COIN), (SLV), (LLY), (SMCI), (UUP), (MSFT), (MSTR)

Global Market Comments

January 30, 2026

Fiat Lux

Featured Trade:

(JANUARY 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(MUB), (UUP), (USO), (HAL), (SLB), (CCJ), (CBOE), (GLD), (TLT), (META), (MSTR), (HOOD),

(COIN), (NVDA), (SLV), (GME), (AAPL)

Global Market Comments

January 16, 2026

Fiat Lux

Featured Trade:

(JANUARY 14 BIWEEKLY STRATEGY WEBINAR Q&A),

(CSCO), (GLD), (MSTR), (JPM), (FXA),

(BTC), (SOFI), (HOOD), (UUP)

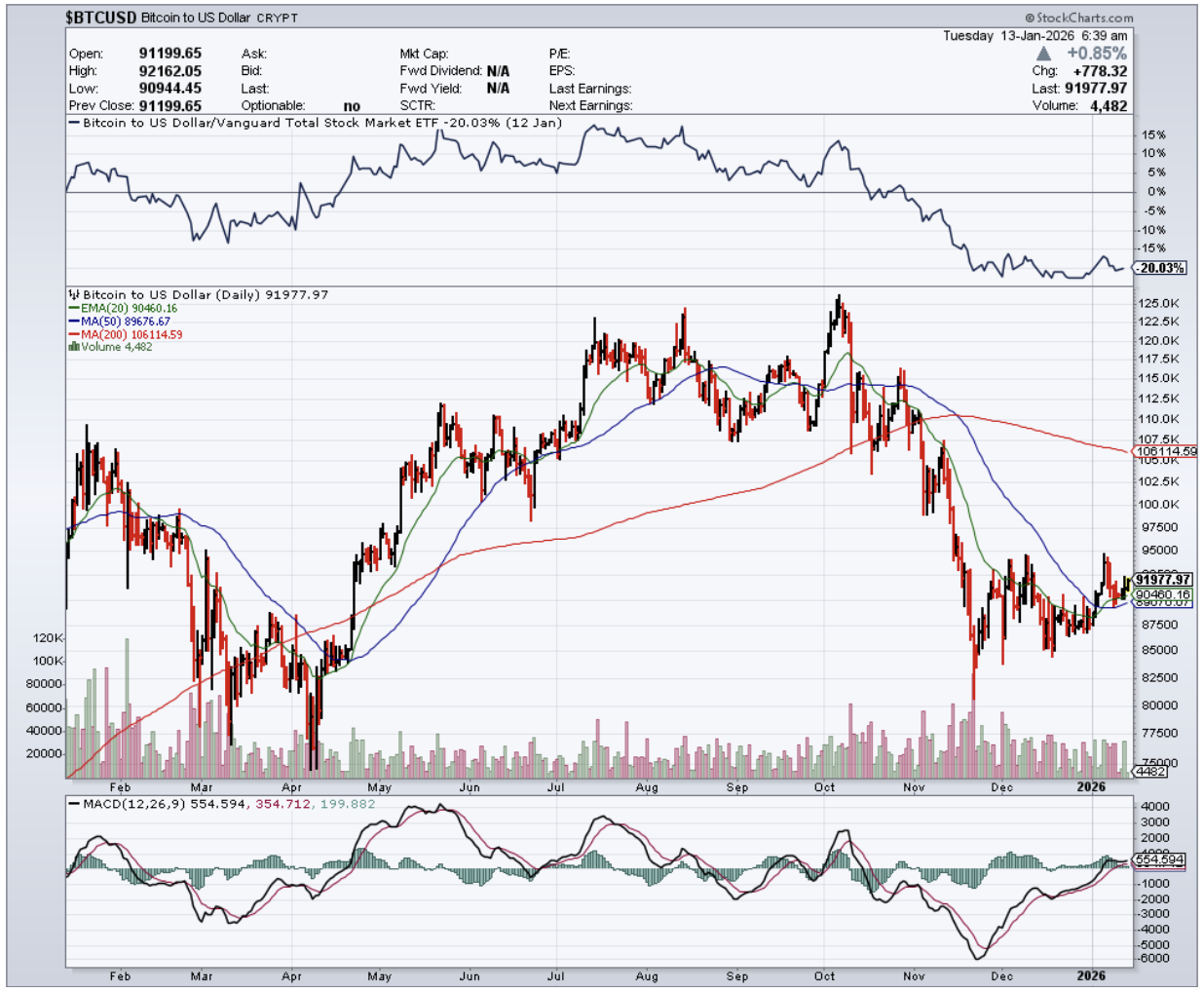

One might postulate that the price of Bitcoin and Chinese housing have no relevant correlation with each other.

Think again!

Granted, Chinese citizens aren’t denominating their mortgages in Bitcoin to snap up their ritzy Shanghai townhouses overlooking the Bund.

I don’t mean that.

But Bitcoin is an asset just like stocks, bonds, and commodities, and is exposed to one-off events that shake out the financial system.

What’s brewing in the Middle Kingdom?

China’s biggest property builder, Evergrande, has since collapsed into one of the largest restructurings in global property history.

Add it up, Chinese bank deposits are estimated at over $45 trillion, more than 2x the US.

Would any Chinese financial crisis lead to an epic flight to fiat alternatives?

Does nobody recognize that this is a planned liquidity drain of the property market in China by the CCP?

All escape "exits" have already been shut. You can't even buy paper gold in China either. Forget Bitcoin!

So I don’t believe that the potential disorderly selling of Chinese flats or the bust of a major property developer would end up boosting the price of Bitcoin because the Chinese government has made it abundantly clear that Bitcoin remains a hard prohibition for its citizens, with enforcement expanded through 2024.

If there is a 20% dip in Chinese property prices, the Chinese would believe that’s a once-in-a-century buy-the-dip type of event, which ultimately became a multi-year decline exceeding 30% in many tier-2 and tier-3 cities.

That doesn’t mean that some won’t try to sell on the down low and get their money out of China through hell or high water.

Some certainly will. China made it clear they didn’t want their citizens investing in overseas assets. I know of the odd millionaire spinning out a random credit card to put a down payment on a house in Vancouver.

What this does scream is policy error big time, an overtightening that could result in a hard landing that is ruinous for global growth.

That would be the worst-case scenario, and I would put that at 10%, which in hindsight proved directionally correct, though slower and more structural than abrupt.

Evergrande was once China’s darling real estate developer. Now, it has defaulted, been restructured, and effectively dismantled.

It was founded in 1997 by Xu Jiayin. It has completed around 1,300 commercial, residential, and infrastructure projects, and at its peak, employed over 200,000 people directly, with millions indirectly exposed.

The company’s success came because it was aligned perfectly with the parabolic boom in real estate that has been driven by the last two decades of staggering Chinese growth, growth for a country that is unparalleled in all of modern human history.

The tragedy in all this is that over 1.6 million Chinese put deposits down on homes that hadn’t been built, and this was more often than not their entire life savings.

Most likely, it is they who held the bag, many of whom faced long delays, partial recoveries, or state-mediated completions.

Better them than me.

For a soft landing to happen, the Chinese government has selectively intervened while still allowing developers to fail.

Even though I categorize this as a quasi-gray swan, opposed to a solid black swan, it is highly likely that it did not spill over into the broader global market, and when large bitcoin dips occurred, bitcoin buyers were ultimately gifted lower prices to enter.

These opportunities were few and far between in that cycle, and I can guarantee that MicroStrategy CEO Michael Saylor went on to repeatedly execute additional bitcoin purchases, often financed with corporate paper.

Limiting the fallout proved more complex than initially assumed, with piecemeal liquidity support and moral-hazard constraints shaping policy responses, plugging holes before they became unpluggable, not unlike our own debt ceiling mess.

The larger issue remains to ponder. Was this the tip of the iceberg?

The silence and lack of major actions from policymakers made everyone nervous at the time, but most likely, they were managing it quietly through state banks and local governments.

The response was largely driven by the People’s Bank of China, which initiated targeted liquidity operations that became a multi-year pattern rather than a single rescue event.

Evergrande was ultimately confirmed to have over $300 billion in liabilities, more than any other property developer in the world. At its peak, it was a beast in China’s high-yield dollar bond market.

A lackluster response to an already expensive market proved costly, with real estate still estimated to account for roughly 35 to 40% of household assets in China despite price declines. At the time, home sales by value showed their sharpest drop since the onset of the coronavirus.

Isolating Evergrande became a point of emphasis for the Chinese Communist Party, using the firm as a scapegoat for sky-high property prices.

They were the fall guy.

This was more of a political show than anything else, a show of power, letting the world know that this economic pain was nothing to even bat an eyelid about.

Bitcoin, perceived as a riskier asset along the risk curve, was not immune from sell-offs, and risk-off sentiment contributed to episodic drawdowns during the 2021 to 2022 cycle.

I had faith in the Chinese government’s authority to contain systemic fallout, and while $40,000 proved only a temporary reference point for Bitcoin, the asset ultimately moved through a full cycle drawdown before reaching new highs in subsequent years.

Short-term relief rallies did occur as headlines improved, though always within a broader macro tightening cycle.

This episode should be understood as part of a standard risk reset, where a 5% equity drawdown translated into roughly double that in crypto volatility.

Booking some of those gaudy profits earlier in the cycle to lower cost basis while deploying capital at lower levels ultimately proved to be the correct play.

Global Market Comments

January 12, 2026

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or RISK IS RISING),

(MSFT), (ABBV), ($VIX), (SPY), (AAPL), (CRWD), (GLD), (SLV), (TSLA), (MSTR), (NVDA)