Mad Hedge Biotech and Healthcare Letter

March 6, 2025

Fiat Lux

Featured Trade:

(THE DANISH DILEMMA)

(LLY), (NVO)

Mad Hedge Biotech and Healthcare Letter

March 6, 2025

Fiat Lux

Featured Trade:

(THE DANISH DILEMMA)

(LLY), (NVO)

I was having dinner with a group of Mad Hedge Fund Trader readers in Salt Lake City the other week.

One, a successful financial advisor who's been following my market calls for years, posed a question that got the whole table talking: "Between Eli Lilly (LLY) and Novo Nordisk (NVO), which horse should I bet on in this weight loss drug race?"

It's the kind of direct question I appreciate. No beating around the bush, just cut straight to the investment thesis.

And the question couldn't have come at a better time—I'd spent the previous months analyzing the shifting dynamics between these two pharmaceutical powerhouses.

For those who haven't been following the battle between Eli Lilly and Novo Nordisk closely, you've been missing one of the most fascinating corporate duels in recent memory.

The American challenger has been steadily gaining ground against the Danish heavyweight in the GLP-1 market—drugs that were originally developed for diabetes but have become blockbusters for weight loss.

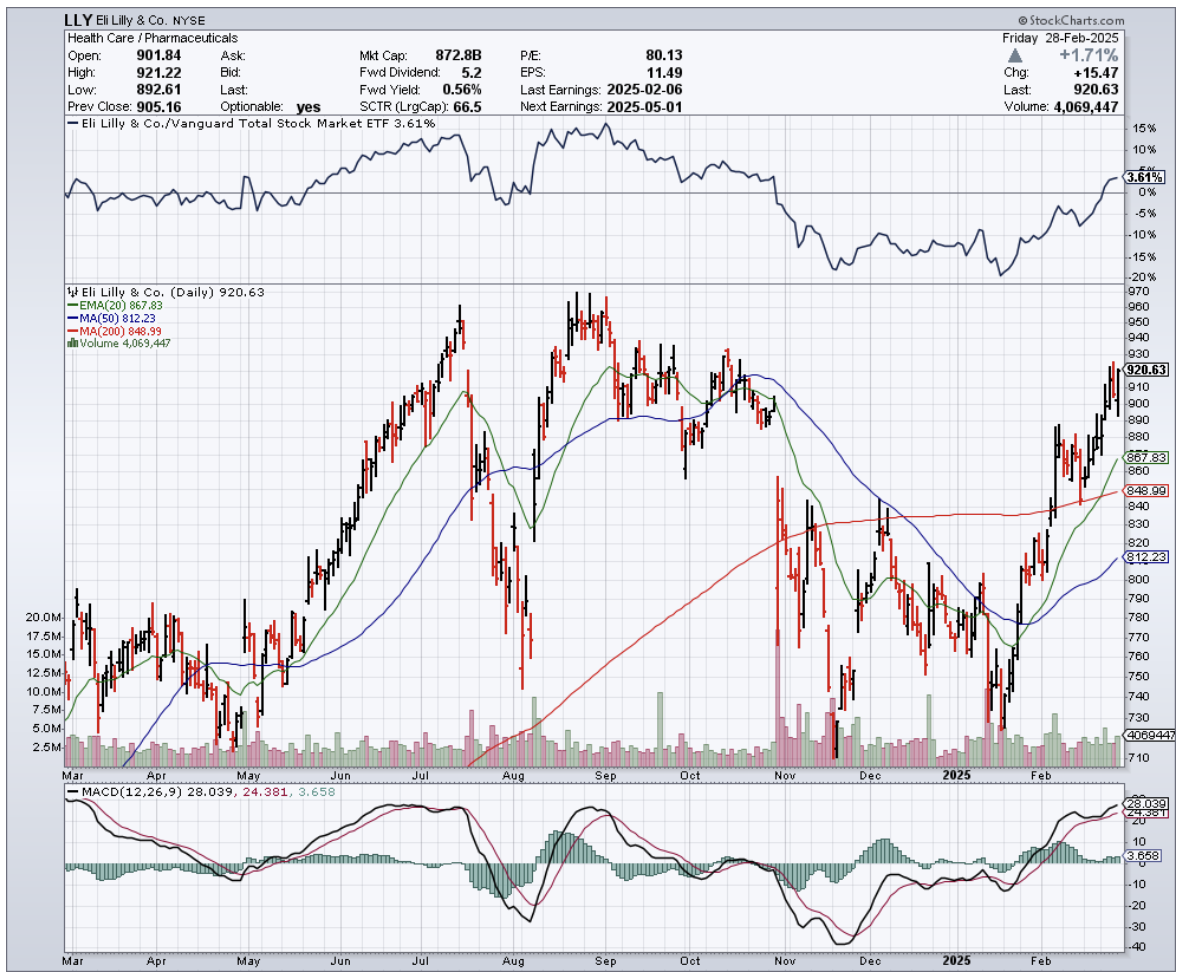

What's particularly interesting is the momentum shift that began in May 2024, with Lilly's upward trajectory continuing through February while Novo Nordisk's stock halted its precipitous decline at a critical juncture.

While bargain hunters are picking through NVO's wreckage, I'm skeptical we'll see a mass migration back to the Danish giant. Here's why.

First, there's the Trump factor. Our newly reinstalled president hasn't been subtle about demanding pharma companies shift production capacity back to American soil or face potential tariffs.

This presents a much bigger problem for Novo Nordisk than for Lilly.

The Indiana-based Lilly has a well-diversified manufacturing footprint, including substantial domestic capacity, while NVO relies heavily on non-U.S. production.

Years spent covering the White House taught me one thing: when a president threatens tariffs, smart investors listen—even if those threats haven't materialized yet.

Trump's policy shifts can come suddenly and dramatically. I've seen enough administration policy pivots over decades to know that being caught flat-footed when the music stops is a recipe for portfolio pain.

Beyond geopolitical considerations, Lilly's Zepbound (their branded weight loss medication) has been steadily gaining share in new prescriptions, showing more robust efficacy than Novo's offerings, and—in a savvy competitive move—is priced at a relative discount. It's a triple threat that's steadily eroding Novo's first-mover advantage.

But what's really impressive about Lilly's position is that they aren't putting all their eggs in the weight loss basket.

They've made solid advances in immunology and oncology, with a diverse pipeline that doesn't rely solely on incretin-based growth drivers.

This brings to mind a conversation I had with a pharmaceutical executive while flying my Ercoupe to an industry conference last weekend.

"The companies that survive long-term in this industry," he told me, "never let themselves become dependent on a single breakthrough, no matter how big."

Meanwhile, Wall Street has been revising upward its estimates for the total addressable market for weight loss drugs, anticipating expanded indications, sustained consumer adoption, and penetration into markets outside the U.S.

This strengthens the bull case for Lilly while simultaneously raising concerns about Novo Nordisk's ability to maintain its market leadership.

Speaking of market leadership, Lilly's oral GLP-1 receptor agonist Orforglipron could be submitted for regulatory approval in late 2025, potentially beating Novo's next-generation product to market.

If commercialized in 2026 as anticipated, it could further disrupt Wegovy's (Novo's weight loss drug) market position.

Some might argue that Lilly's outperformance against Novo since mid-2024 has already priced in these advantages.

But a closer look at Lilly's valuation suggests the market still isn't fully convinced of the company's growth potential.

Is this caution warranted? Perhaps. Wall Street doesn't expect Lilly's current surge in revenue growth to continue through 2027.

Lilly's management has indicated pricing will likely remain stable, but the broader expectation is that medium-term pricing may remain muted or even decline, especially as Novo's products face pricing negotiations by 2027.

This could pressure Lilly's market position, particularly given the relatively high prices in U.S. markets.

We should anticipate a more competitive landscape after 2027 as other competitors enter the weight loss drug market, though market share dynamics should remain relatively stable through 2030.

Let's talk valuation. Lilly is trading at a forward non-GAAP P/E of 37.8x, almost double its sector peers. That sounds expensive until you realize it's more than 10% below its five-year average.

More tellingly, when accounting for earnings growth prospects, Lilly's PEG ratio of 1.13 is almost 40% below the sector median.

Translation? The market hasn't gone full FOMO on Lilly yet, despite its recent outperformance of the S&P 500. In fact, price action suggests growing conviction that the stock is poised to retest its all-time highs.

Lilly weathered two setbacks in 2024 as the market questioned whether it could credibly challenge Novo's dominance.

Yet the stock found firm support above the $700 level in August, November, and again in January, confirming my belief that this support zone is rock-solid, attracting value-conscious buyers who recognize Lilly's growth potential relative to its valuation.

The breakout above the $840 zone (December highs) marks a decisive move that validates the bull case.

And while the outlook beyond 2027 remains murky, the market's restraint in valuing Lilly gives investors who've been watching from the sidelines another opportunity to board this train before it leaves the station.

"So what's your call?" pressed the advisor, who like many in his field has been forced to dump expensive research analysts while still needing solid investment ideas for his growing client base.

The rest of the table, a mix of successful entrepreneurs and self-taught traders, leaned in to hear my response.

"If you're picking between the two for a long position, Lilly is the clear choice," I replied. "They've got the edge on domestic production, they're better insulated from potential tariffs, they have a more diverse pipeline, and the market momentum is clearly in their favor."

As the waiter cleared our plates, one of the younger traders at the table asked about price targets. I tapped my wineglass thoughtfully with my pen—a habit that drives my wife crazy.

"The breakout above $840 was significant," I said. "If the fundamentals hold, which I believe they will, we could see a return to all-time highs before the bears even realize what hit them."

This led to a spirited debate about pharmaceutical valuations that lasted well past dessert.

It's these impromptu investment summits that remind me why I still travel the country meeting readers, despite having technically "retired" years ago.

The collective wisdom and diverse perspectives always sharpen my own thinking.

When the check arrived, someone joked that talking about weight loss drugs had made them lose their appetite.

“Not Lilly,” I quipped. “They're happily eating Novo's lunch”

Mad Hedge Biotech and Healthcare Letter

January 14, 2025

Fiat Lux

Featured Trade:

(THE HEAVIEST HITTERS)

(NVO), (LLY)

During my morning coffee run yesterday, I couldn't help but notice the transformation of my local café's menu. Where once stood a simple array of pastries, now sits a fortress of "keto-friendly" and "low-carb" options.

The barista told me they could barely keep them in stock. Times are changing, but not fast enough to stem the tide of what's become a global health crisis.

Here's a sobering statistic that explains why two pharmaceutical giants are about to have their best decades ever: In 1975, only 3 out of 100 men were obese. By 2022, that number exploded to 14. Women haven't fared much better, jumping from 6.6 to 18.5 out of 100.

But here's the real kicker – childhood obesity has multiplied TENFOLD since 1975.

Enter Novo Nordisk (NVO) and Eli Lilly (LLY), two companies that have discovered what might be the holy grail of modern medicine: drugs that can shrink waistlines almost as effectively as a year of dedicated dieting, but with considerably less willpower required.

I've been tracking both companies closely, and the numbers are staggering. Eli Lilly's tirzepatide (marketed as Mounjaro for diabetes and Zepbound for weight loss) has achieved what most thought impossible – a 20.80% average weight loss over 72 weeks. That's the kind of number that makes both bathroom scales and Wall Street analysts take notice.

Morgan Stanley certainly has. They're projecting the market for these weight-loss wonder drugs to explode from $6 billion in 2023 to an eye-popping $105 billion by 2030. And here's why I think even that might be conservative.

Last week, I caught up with an old friend who heads one of the largest healthcare investment funds in Boston. He shared an interesting insight: "The biggest problem these companies have isn't competition – it's keeping up with demand." Both Novo Nordisk and Eli Lilly are investing billions just to scale up production. It's like trying to drink from a firehose of opportunity.

Let's break down why these stocks are so compelling:

The market for diabetes medications is exploding. We're looking at 537 million adults with diabetes today, growing to 783 million by 2045. These aren't speculative numbers – they're based on current trends that show no signs of reversing.

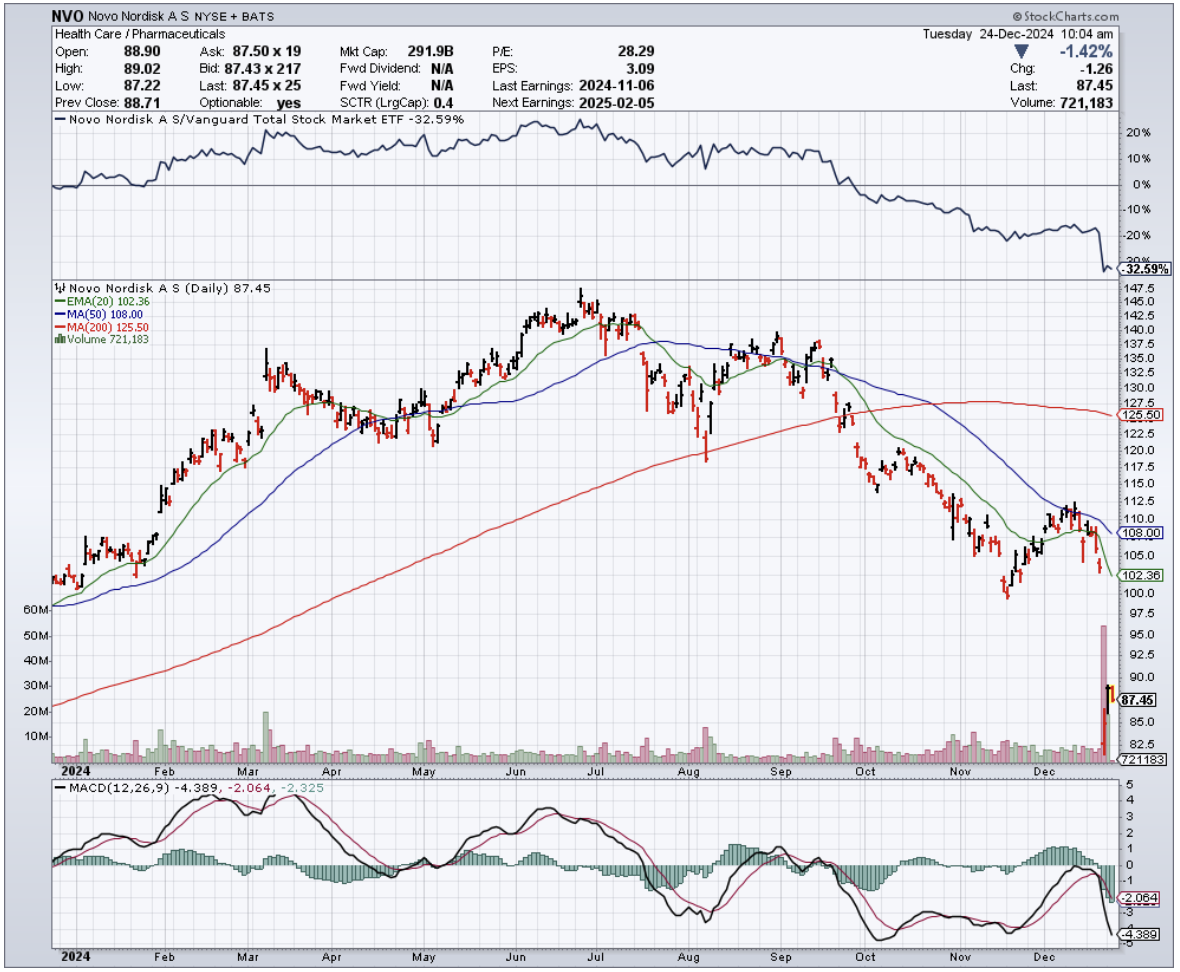

Novo Nordisk currently dominates the GLP-1 market with a 66.80% share internationally, while Eli Lilly's tirzepatide holds 17.60%.

In the insulin market, Novo Nordisk's supremacy is even more pronounced, controlling 44.50% of the global market share compared to Eli Lilly's estimated 20-25%.

This is where it gets pretty interesting. Despite Novo Nordisk's market dominance, Wall Street has developed a crush on Eli Lilly.

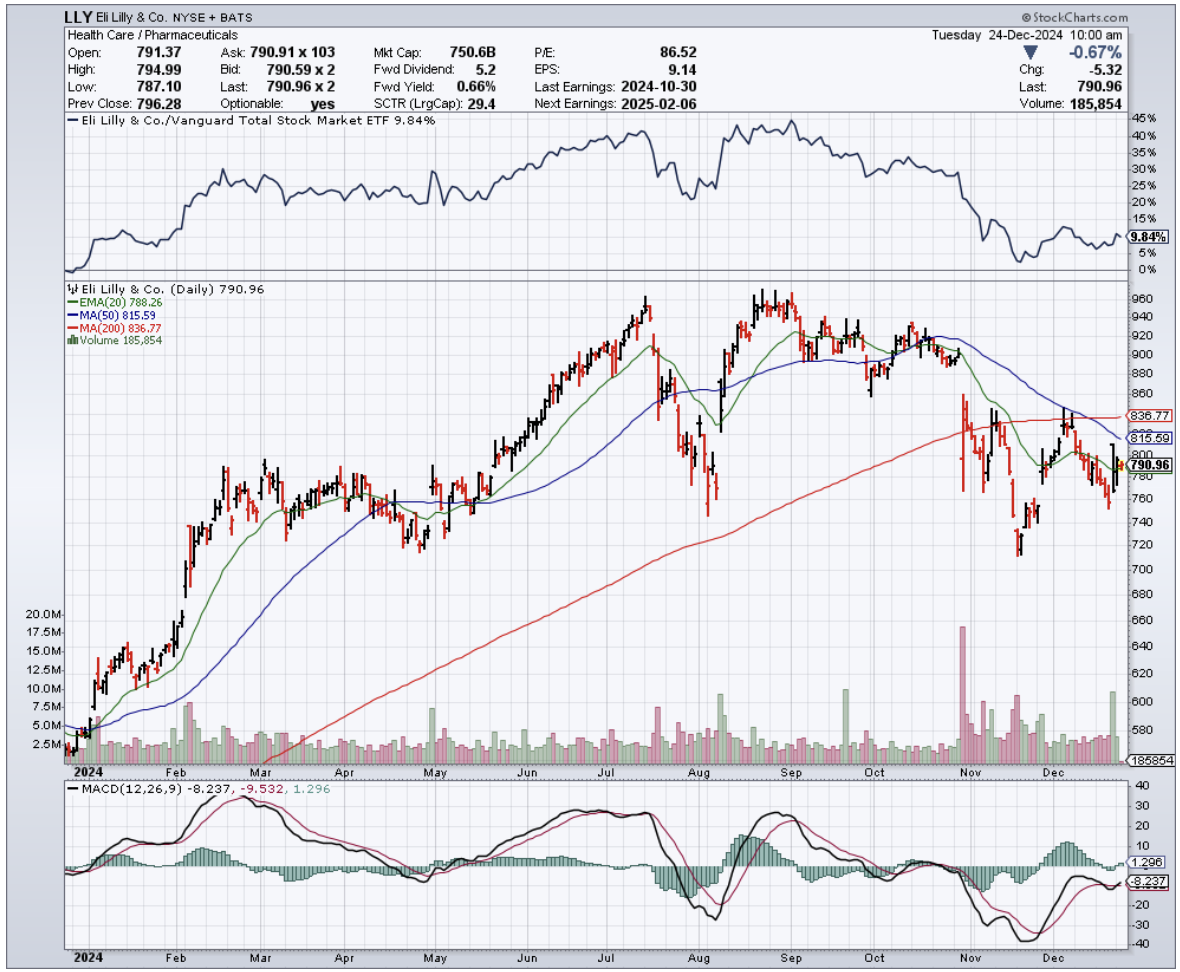

Looking at the Price/CFO ratio, Novo Nordisk is trading BELOW its 10-year average, while Eli Lilly's valuation has soared to levels that would make a tech startup blush.

For 2025, Novo Nordisk's EPS is expected to hit $3.88. With a reasonable PE ratio of 25x, that suggests a fair value of $97.20 by the end of 2025 – an 11% upside potential.

Meanwhile, Eli Lilly, with an expected EPS of $21.57 and a justified PE ratio of 30x, points to a fair value of $647.10, suggesting it might be overvalued by about 17%.

The biggest risk? A global shift toward healthier lifestyles. But having just driven past my local McDonald's with a line wrapped around the building at 10 PM, I'm not losing sleep over that scenario.

My call? I'm long Novo Nordisk. While both companies are excellent, I prefer buying the market leader at a discount rather than the challenger at a premium. It's like buying beachfront property in Miami – the price might seem high today, but just wait until next year.

So, I'm maintaining a core position in Novo Nordisk with plans to add on any significant dips. The obesity epidemic isn't going away anytime soon, and neither is the demand for these medications.

For those looking to play both sides of this market transformation, a smaller position in Eli Lilly isn't crazy – just be prepared for some volatility given the current valuation.

And, yes, I'm aware there’s plenty of hand-wringing over these stocks' valuations. But the next time someone tells you the market's getting too heavy, just remember - in this case, that's exactly the point.

Mad Hedge Biotech and Healthcare Letter

December 26, 2024

Fiat Lux

Featured Trade:

(PHASE 2 OR NOT PHASE 2: THAT'S NOT EVEN A QUESTION IN 2025)

(LLY), (NVO)

I had dinner with a veteran biotech investor at San Francisco's Waterbar earlier this month, watching the Bay Bridge lights while discussing what's coming for biotech in 2025.

"The game is changing," he said, picking at his salmon. "It's not about platform promises anymore. Show me the Phase 2 data, or don't show up at all."

He's nailed what I've been seeing in my recent travels through the biotech corridors of Boston, San Diego, and Basel. The days of throwing money at shiny new platforms are ending.

That means that by 2025, we'll see venture capital concentrate in fewer but larger deals, especially in companies with solid Phase 2 data.

Let me break down what this means for our portfolio next year. First, North America will dominate in advanced biologics and AI-driven drug discovery. I've toured enough labs recently to see that our capabilities in these areas are leaving others in the dust.

Europe's doubling down on sustainable manufacturing and rare diseases - smart move given their regulatory environment. Asia? They're positioning to own generics and biologics manufacturing, with India making particularly interesting moves in antibody-drug conjugates.

The money's following these regional specialties. If you're investing in biotech companies that don't align with their region's strengths, you might find yourself waiting longer for returns than a Red Sox fan waiting for another World Series.

My contacts in several major VC firms confirm they're already adjusting their 2025 strategies around these regional strengths.

Here's what's really interesting: obesity and GLP-1 drugs are the exception to every rule. After watching Eli Lilly (LLY) and Novo Nordisk's (NVO) recent success, everyone wants a piece of this action.

Even early-stage obesity plays are attracting serious capital, bucking the trend toward late-stage investments.

But remember this about 2025 - being picky about Phase 2 data isn't just smart, it's survival. We're heading into a market where strong clinical validation will matter more than ever.

I've seen enough biotech cycles to know that when the market gets selective, you want to be where the data is solid.

The numbers back this up. Looking at the trends, Phase 2 companies have consistently captured the highest deal sizes, except for that brief period in 2023 when obesity deals sent Phase 1 valuations through the roof.

By 2025, expect this preference for Phase 2 assets to become even more pronounced. Phase 3 investments have been declining - dropping from $4.2 billion in 2021 to $1.7 billion in 2024 - partly because companies with strong Phase 2 data are getting snatched up through partnerships or acquisitions before they even get to Phase 3.

Speaking of partnerships, watch Big Pharma's moves carefully in 2025. They're increasingly hungry for de-risked assets, and strong Phase 2 data is their favorite meal.

I had lunch with a Big Pharma exec last week who told me they've completely restructured their BD team to focus on Phase 2 assets in their regional sweet spots.

As for AI platforms? They'll still get funded - companies like Xaira and Generate:Biomedicines are proving that. But by 2025, they'll need to show more than just fancy algorithms. The market's going to demand real clinical validation.

I recently visited an AI-driven drug discovery company where the CEO proudly showed me their latest neural network. "That's great," I told him, "but show me your clinical data." The silence was deafening.

So, what’s the play here? Well, I'm keeping my own biotech portfolio focused on companies with strong Phase 2 assets heading into 2025, especially in regional sweet spots.

And yes, I've got a position in the obesity space - sometimes a trend is too strong to ignore, even for an old contrarian like me.

One final thought: keep an eye on those time gaps between funding rounds. They're getting longer, and by 2025, companies that don't fit neatly into regional specialties or lack solid clinical data might find themselves in the financial equivalent of a Phase 2 trial that never ends.

Now, if you'll excuse me, I've got a call with a German biotech CEO about their sustainable manufacturing process. These regional specialties aren't going to research themselves.

Mad Hedge Biotech and Healthcare Letter

December 24, 2024

Fiat Lux

Featured Trade:

(THE LAB RESULTS ARE IN)

(GILD), (TSLA), (WVE), (EDIT), (CRSP), (LLY), (NVO), (WMT), (CVS), (CCCC), (RHHBY)

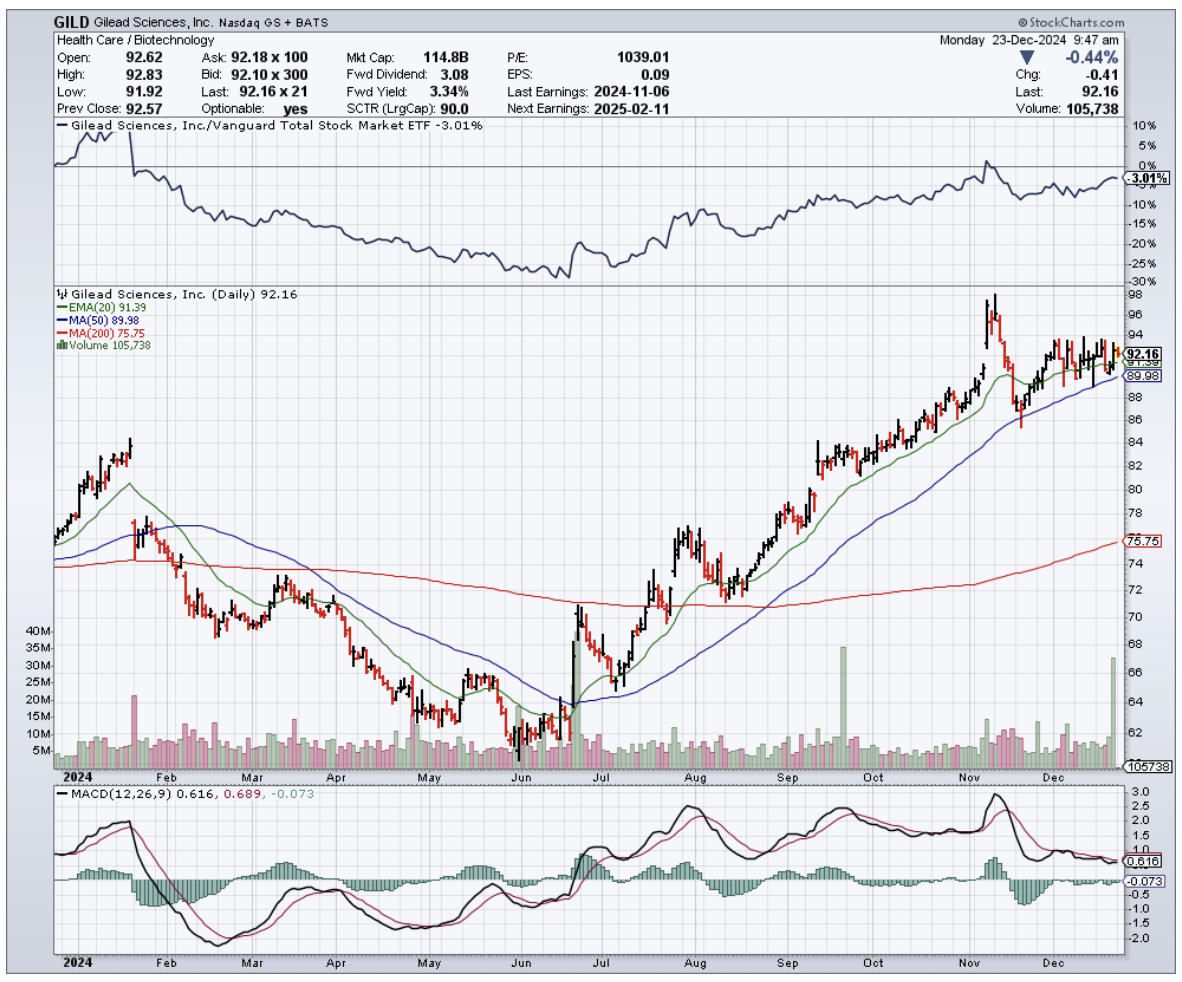

I found myself gridlocked in Bay Area traffic a few days ago, inching past Gilead's (GILD) sprawling Foster City headquarters, when my phone lit up with a call from an old friend at Goldman.

“Alright, tell me—what’s the real story with biotech this year?” she asked, her tone hovering somewhere between curiosity and exasperation. “Half my portfolio feels like a masterstroke, the other half... well, let’s just say it’s testing my patience.”

As I watched a Tesla (TSLA) weave through traffic like it was auditioning for a Fast & Furious reboot, I smiled.

Biotech has always been a bit of a high-stakes chess game—brilliance in one corner, chaos in another, and always a few surprises lurking behind the next move.

“Let me break it down for you,” I said, steering the conversation as carefully as I did my car through the bumper-to-bumper maze.

First, the winners are crushing it, and I mean crushing it. Gilead (GILD) finally cracked the code on HIV treatment, developing what's essentially a vaccine that doesn't require popping pills like they're Tic Tacs.

My contacts in clinical development tell me the Phase 3 data in cisgender women is nothing short of spectacular. With a $6 billion annual market potential by 2028, this isn't just another incremental advance - it's the kind of breakthrough that makes everyone in biotech salivate.

Then there's Wave Life Sciences (WVE) and their RNA editing technology. Remember when we thought CRISPR was the only game in town? Well, Wave just showed us there's more than one way to edit a gene.

Their liver-targeting therapy is the first successful RNA editing in humans - think of it as spell-check for your DNA, but reversible. The market's currently at $1.1 billion, but with 35% CAGR through 2030, this train is just leaving the station.

Speaking of trains leaving stations, molecular glue developers like C4 Therapeutics (CCCC) are watching Big Pharma back up the Brink's truck.

We're talking $8 billion in licensing deals this year alone. After all, when Roche (RHHBY) drops $300 million upfront - not milestone payments, mind you, but cold hard cash - you know they've seen something special in the data room.

But here's where it gets interesting, and I had to pull over at this point in the conversation because my friend wasn't going to like what came next.

CRISPR stocks? Down 20%. Editas (EDIT) and CRISPR Therapeutics (CRSP) are learning that revolutionary science doesn't always translate to revolutionary returns.

My friend Janet at the Fed might be talking about higher rates, but these companies are bleeding cash faster than a Silicon Valley startup's WeWork budget.

The obesity market? Unless your name is Eli Lilly (LLY) or Novo Nordisk (NVO), you're probably not having a great time.

Only three startups cleared $100 million in funding this year. In biotech terms, that's like trying to build a house with pocket change.

The global market's sitting at $4.1 billion, but it's more crowded than a San Francisco coffee shop during a tech conference.

And don't get me started on Walmart (WMT) and CVS (CVS) trying to play doctor. They thought they could disrupt traditional healthcare with their “get your physical next to the garden tools” model.

The result? A combined loss of $250 million and a wave of clinic closures.

The lesson here is clear: just because you can sell lightbulbs and Band-Aids in the same aisle doesn’t mean you should try to diagnose strep throat next to the automotive department.

A kid in a modded Subaru WRX cut me off as I wrapped up the call, but I left my friend with this: In biotech, timing is everything.

Gilead and Wave are showing us that patience pays off when the science is solid. Meanwhile, CRISPR stocks remind us that even the most promising technology needs good timing and deep pockets.

So, watch those clinical trial results like a hawk, and keep an eye on where the venture money's flowing.

But most importantly, remember what my old mentor used to say: "In biotech, you're not just betting on the science - you're betting on the scientist, the CFO, and sometimes, just sometimes, on whether people are ready to get their flu shot next to the garden center."

Now, where's that highway patrol when you need them?

If I had a nickel for every time someone said pharmaceutical manufacturing was boring, I could’ve started bidding against Novo Holdings for Catalent (CTLT) myself.

Sure, I’d still be $16.5 billion short, but you get the point—this deal is huge, and it’s about to make some smart money look even smarter.

Here’s the deal: Novo Holdings is shelling out $16.5 billion to snap up Catalent, a contract development and manufacturing organization (CDMO).

If that acronym sounds like alphabet soup, let me translate: CDMOs are where the real action happens.

These are the guys behind the curtain making sure your miracle drugs and life-saving treatments aren’t just ideas—they’re products hitting the market at scale.

The numbers don’t lie. The CDMO market sits at $146 billion right now.

Fast-forward to next year, and that balloons to $243.3 billion. By 2029, it’s cruising toward a cool $332 billion.

And if you think that’s impressive, just wait: the broader pharmaceutical outsourcing trend is nowhere near slowing down.

In 2014, Big Pharma still clung to in-house production for 66.3% of its output.

Today? That figure’s down to 51%, and dropping fast. Why? Because outsourcing lets the specialists handle the hard stuff—faster, cheaper, and more efficiently.

For investors, Catalent’s immediate upside is a no-brainer. The acquisition premium is pure gravy, but that’s not the whole story.

Rivals like Lonza Group (SWX: LONN) and Samsung Biologics are already feeling the heat.

The biologics CDMO market alone is expected to expand by $10.63 billion between 2024 and 2028, and you better believe those two are scrambling to stay ahead.

If you own shares, keep your seatbelt fastened. If you don’t, well… you might want to rethink that.

And here’s where it gets really interesting: Novo Holdings may be private, but its publicly traded golden child, Novo Nordisk (NVO), is set to ride this wave like a pro surfer.

They’re already a global powerhouse in biologics, and Catalent’s souped-up manufacturing capabilities are going to help them scale production with military-grade efficiency.

Lower costs, tighter operations, bigger margins—it’s like handing a Formula 1 car to an already championship-winning team.

So if you’re not watching Novo Nordisk stock, you’re doing it wrong.

Of course, it’s not just the big CDMO players who stand to win here. Companies like Danaher (DHR), Repligen (RGEN), and Avantor (AVTR) are quietly cashing in on this gold rush.

These firms supply the picks, shovels, and critical bioprocessing tools that CDMOs need to keep production humming.

As Catalent scales under Novo Holdings, demand for these essentials will go through the roof.

Zooming out, the pharma manufacturing landscape is evolving at a breakneck pace.

The CDMO market is expected to hit $530.3 billion by 2033, growing at a steady 7.7% CAGR.

That’s not speculative growth—it’s a structural shift, backed by demand for biologics, gene therapies, and personalized medicine.

In short, we’re entering an era where outsourcing is king, and companies with the infrastructure to capitalize on it are poised to dominate.

Don’t forget about the big dogs in Big Pharma, either.

Pfizer (PFE), Eli Lilly (LLY), and Merck (MRK) aren’t just spectators in this game. They’re snapping up CDMO capacity, investing in biologics, and doubling down on therapies with blockbuster potential.

The Catalent deal is just the latest chess move in a game where the stakes keep getting higher.

So what does this mean for you? If you’re holding Catalent, congratulations—your portfolio is about to get a nice bump.

But the real play here isn’t Catalent alone. It’s understanding that CDMOs, suppliers, and adjacent players are the unsung heroes of this industry transformation.

You want exposure to the companies enabling the next wave of medical innovation? This is where you look.

Novo Holdings just threw down the gauntlet, and the smart money is already moving. The pharmaceutical manufacturing sector isn’t boring—it’s booming.

So, while everyone’s chasing flashy biotech startups and blockbuster drugs, the real smart money is quietly following the companies that make those breakthroughs possible.

Catalent isn’t just a $16.5 billion deal—it’s proof that outsourcing is the new backbone of pharma’s future. Call it “The Big Batch Theory:” scale up, outsource smart, and watch the returns multiply.

Ignore this shift, and you’re leaving money on the table.

Now, if you’ll excuse me, I need to check my CDMO positions. Just like a perfectly run batch, they’re growing fast—and that’s exactly how I like it."

Mad Hedge Biotech and Healthcare Letter

November 26, 2024

Fiat Lux

Featured Trade:

(NO MORE EATING AT YOU)

(PFE), (LLY), (NVO), (AMGN), (RYTM), (ALT)