Mad Hedge Biotech and Healthcare Letter

May 2, 2024

Fiat Lux

Featured Trade:

(BUT WEIGHT, THERE’S MORE)

(LLY), (NVO)

Mad Hedge Biotech and Healthcare Letter

May 2, 2024

Fiat Lux

Featured Trade:

(BUT WEIGHT, THERE’S MORE)

(LLY), (NVO)

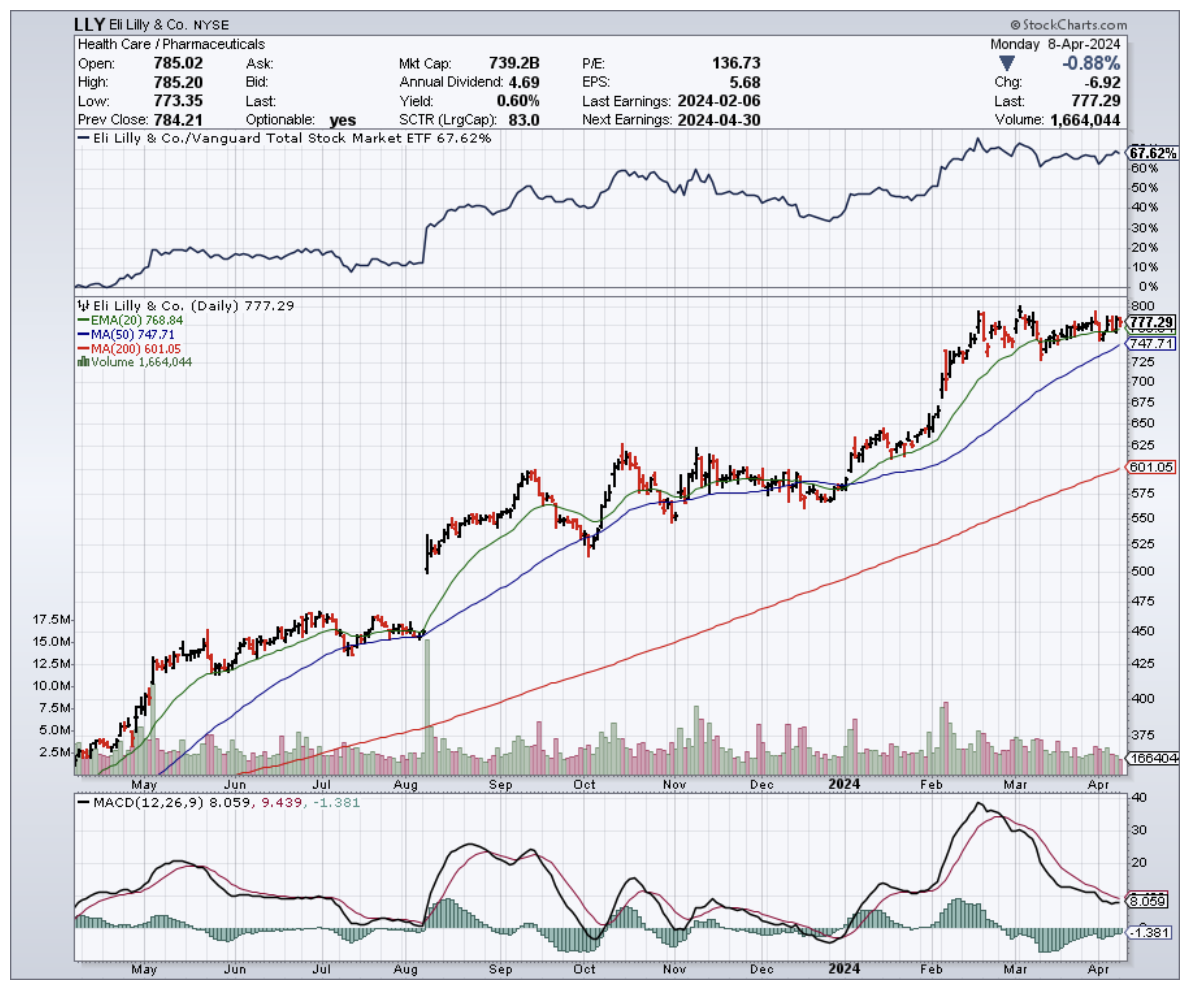

You know that feeling when you find a crumpled $20 bill in an old jacket? That’s a little like what Eli Lilly must be feeling with tirzepatide, only replace that $20 with a cool $34 billion forecast by 2029. Yeah, it’s been that kind of party over at Lilly.

Tirzepatide, the magic ingredient in both Zepbound for weight loss and Mounjaro for diabetes, is turning heads—and not just because it’s raking in the cash. This drug is proving to be a one-stop-shop for boosting Lilly’s bottom line and shaking up the market.

Since Zepbound’s launch in November 2022, Lilly’s stock has been on a tear, skyrocketing from $349.95 to a whopping $733.51.

That’s a gain of over 109%. It’s like Eli Lilly has turned into the Usain Bolt of the biotech and pharma sector, sprinting past the S&P 500 and its pharma peers without breaking a sweat.

Actually, Lilly's got a double-whammy against the competition. Not only does Tirzepatide keep raking in successful studies, but it's also got a sweet price point.

We're talking about Zepbound being a good 20% cheaper than Novo Nordisk's (NVO) big hitter, semaglutide.

Essentially, patients get the same results, but a lot less strain on their wallet. This combination easily gives Lilly a serious edge in the diabetes and obesity drug battle.

But wait, there’s a hiccup. Despite the blockbuster status of Zepbound, there’s a bit of a snag recently with this drug—supply can’t keep up with demand.

It makes you wonder whether this is a classic case of "too much of a good thing," right?

This shortage has even made the US Food and Drug Administration limited availability list. But fear not, Lilly’s got plans to boost production with a new facility in Concord, North Carolina by year-end.

Still, this supply problem didn’t stop Lilly from coming up with tirzepatide’s latest party trick: tackling obstructive sleep apnea (OSA).

Basically, OSA disrupts your sleep by making your throat muscles a bit too enthusiastic at night. They tighten up and block your airway, leaving you gasping for air (not exactly the recipe for restful sleep). Untreated OSA can be a serious health hazard, linked to heart problems down the line.

And here's a scary statistic: 80 million adults in the US have sleep apnea, but a whopping 85% of those cases go undiagnosed. That's right, millions are unknowingly battling a condition that disrupts sleep, increases the risk of heart problems, and leaves you feeling like a zombie all day.

Given these figures, it’s not surprising that Lilly’s looking to turn this challenge into the next big opportunity.

In fact, recent studies have shown tirzepatide could reduce those pesky episodes of stopped breathing during sleep by about 30 times an hour compared to a placebo. Talk about a breath of fresh air.

So, how much money will tirzepatide rake in at its peak? Well, it's already approved for diabetes AND obesity, but there's room for even more growth.

To date, Lilly is projected to rake in $25 billion in peak sales for this drug, but with recent developments, even that seems low.

Think about this: Tirzepatide made over $5 billion last year – its first full year on the market.

Then, it snagged the obesity indication in November 2023, now pharmacies can't keep it on the shelves, showing demand is off the charts.

Now, I know you’re wondering if you’ve missed the boat with Lilly’s stock price more than doubling in a blink.

But here’s the kicker: there’s potentially a lot more upside. Beyond tirzepatide, Lilly’s got a full deck with new drugs and a solid dividend that’s been fattening wallets at a rapid clip—up 101.6% in the last five years alone.

So, what’s the bottom line? If you’re looking to park some cash in a stock that has a track record of turning medical breakthroughs into gold, you might want to give Eli Lilly a closer look.

After all, betting on a company that’s leading the charge in medical innovation can sometimes feel like finding that $20 bill—only a lot, lot bigger.

Mad Hedge Biotech and Healthcare Letter

April 30, 2024

Fiat Lux

Featured Trade:

(HITTING CTRL+ALT+DELETE ON DRUG R&D)

(DNA), (GOOGL), (JNJ), (ILMN), (JNJ), (ALTO), (GROIV)

Mad Hedge Biotech and Healthcare Letter

April 25, 2024

Fiat Lux

Featured Trade:

(RACING TO SWAP A GOLDEN GOOSE FOR A NEW FLOCK)

(MRK), (NVO), (LLY), (JNJ), (ABBV), (PFE)

Big pharma usually makes investors smile - fat profits, juicy dividends, and stocks that crush the market.

Lately, though, some of these giants are looking more like grumpy old men. Sure, there are exceptions like Novo Nordisk (NVO) and Eli Lilly (LLY) printing money with their obesity blockbusters.

But what about the rest? Even with Washington breathing down their necks, patent cliffs, and a shaky economy, you'd think these drug titans wouldn't be lagging the market, right? Wrong.

Check out the "Big Eight" top dogs - Johnson & Johnson (JNJ), Merck (MRK), AbbVie (ABBV), Pfizer (PFE), and the rest. Only a few have really delivered the goods in the past five years. AbbVie and Merck have been alright, but the others? They make me want to take a nap.

Now, I'm not saying give up on pharma entirely - there's still money to be made. But you've got to do your homework. Today, let's take a look at Merck.

They raked in $60.1 billion in 2023, making them a heavy hitter. But without their COVID cash machine Lagevrio, growth is...less impressive. Still up, but not setting the world on fire.

The real story is spending - Merck went on a spree, burning through cash on R&D. Why? Their golden goose Keytruda, that $25 billion cancer blockbuster, is facing generic competition soon.

Merck isn't just sitting around waiting for the Keytruda patent cliff either. They're furiously throwing money at new drugs, acquisitions, cancer, heart disease, immune disorders - hoping to find the next Keytruda before the current one fades away. It's like an aging rockstar desperately trying to write another big hit.

But let's be real, finding billion-dollar breakthroughs is a gamble, even for giants like Merck. They've got potential in the pipeline for sure, but it's a long road from the lab to pharmacy shelves. Plenty of drugs flame out along the way.

Looking back, 2023 wasn't a victory parade for Merck. It was more like a mad dash to spend their way out of the looming Keytruda patent cliff. But hey, sometimes you've gotta break a few eggs to make an omelet, right?

Speaking of potential winners, let's talk about those newly approved lung drugs – sotatercept could be a major player.

Merck's vaccine department is looking strong too, with potential blockbusters targeting lung infections and RSV in the pipeline.

Of course, it hasn't all been smooth sailing. That new cough drug, gefapixant, getting rejected by the FDA again? Merck took a hit on that. Still, this biotech’s not giving up. This is a company buying time to build up a whole new arsenal, and the Keytruda cliff might hurt, but they'll come out swinging.

So, let’s forget about that 2023 earnings dip. Merck's forecasting a serious jump in 2024 profits as they dial back the crazy spending. Yes, their balance sheet took a hit, but look at what they're building. They're hunting big deals to bolster that pipeline, and that's a good thing in my book.

Speaking of big moves, Merck's been on a shopping spree. Wall Street might get nervous if they drop another bombshell, but I trust their judgment. These aren't just random buys; this is how they protect their future cash flows. Besides, any short-term drama from a big deal could be a sweet buying opportunity.

And while Merck’s still figuring out which one could be the next big thing, the true star of the show, until that patent cliff arrives, is still Keytruda.

That beast is still growing and could keep going strong for years, especially in early-stage treatments. Plus, that new subcutaneous version of this blockbuster treatment? Talk about extending the gravy train well past the generic competition.

Let's also check out the other horses in this race: sotatercept's early sales numbers, a potential FDA approval for that HER2 drug, the saga of gefapixant's third shot (or not), and the cash potential of V116 and Welireg. Not to mention, juicy updates on that Moderna (MRNA) partnership…Merck’s next months could be packed with surprises.

As for this company’s dividend? Decent track record, but don't expect fireworks after the recent hike. As for buybacks, Merck seems to have...other priorities right now. Those profits are pouring straight into the growth pipeline.

The bottom line: While some of Big Pharma looks pale lately, Merck is still bringing it, share price gains and all. Sure, that gefapixant rejection stings. But Keytruda keeps roaring, and Merck's pipeline is buzzing with potential. I'm not sweating earnings.

Merck's got contingencies lined up for the Keytruda patent apocalypse - new drugs, deals, maybe even extending Keytruda itself. They're playing for the long game here. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

April 18, 2024

Fiat Lux

Featured Trade:

(A RARE OPPORTUNITY OR A PROBLEMATIC DEBT-ACLE?)

(AMGN), (LLY), (NVO)

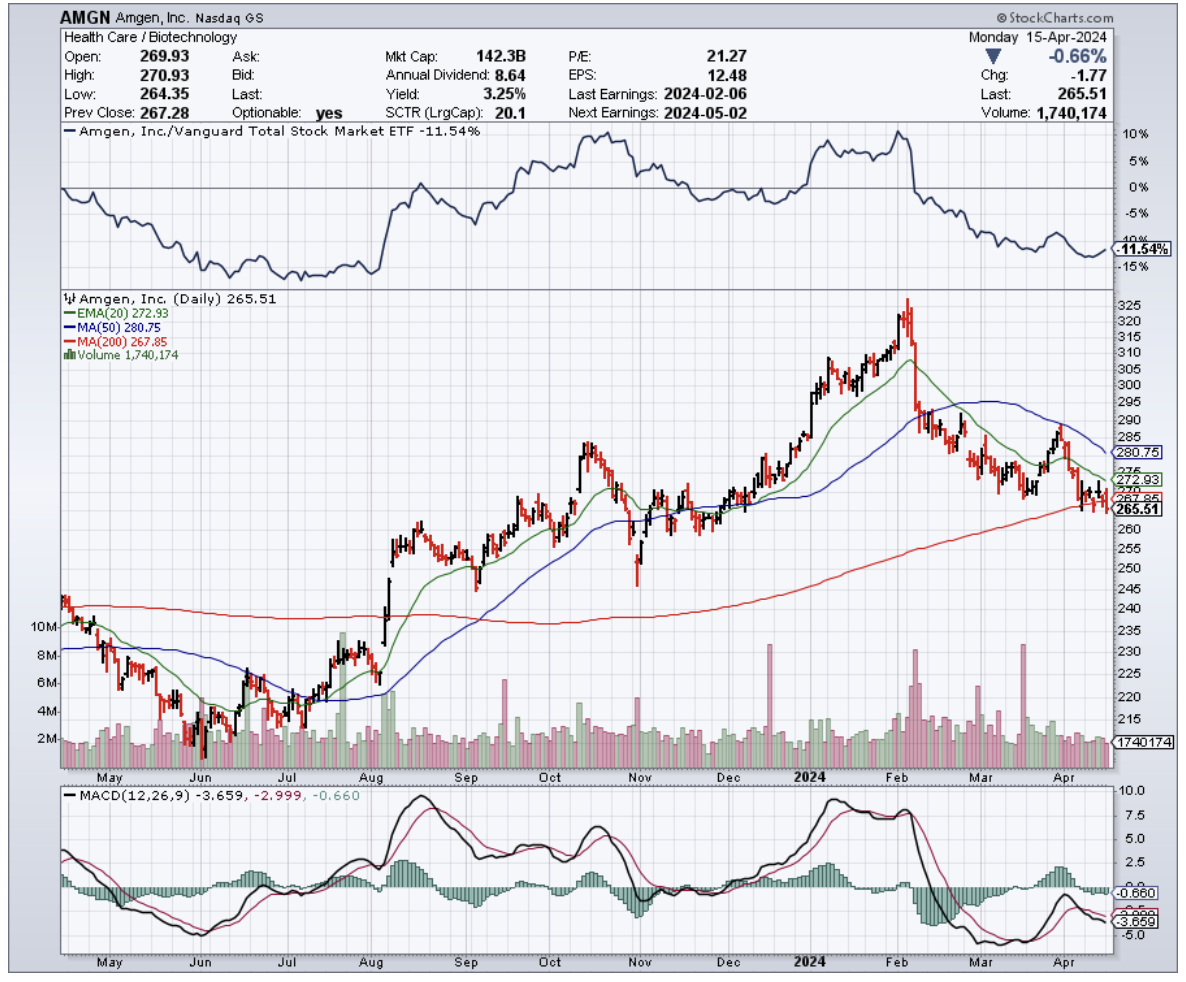

Remember Gordon Binder and his "Science Lessons?" Well, Amgen (AMGN) seems to be re-reading a few chapters from the book by its legendary former CEO.

Their nearly $28 billion buyout of Horizon Therapeutics (HZNP) screams blockbuster ambition, but it also means they loaded up on debt like it's going out of style. This HAD better work.

Why the gamble? Horizon brings heavyweight rare disease drugs like Tepezza to the table. Sales have been flatlining near $2 billion, but Amgen smells potential. With the indication just expanded and a measly few percent of patients treated, there's room to run...if they can find those patients. That's the tricky part with rare diseases.

Other gems like Uplizna round out the deal. Now, it's all about whether Amgen can make this expensive new portfolio pay.

Let’s take a look at Amgen’s 2024 pipeline. The biotech’s goals this year center on a few key drugs – some acquired, some homegrown.

Tepezza and Uplizna are all about finding those elusive rare disease patients and expanding market access. We're not just talking sales growth here... it's about proving their ability to dominate this niche.

In their "General Medicine" department, there's Olpasiran in Phase 3. A stellar Phase 2 could mean over a BILLION in sales if it gets the green light. But Phase 3, as we know, is where the tough questions get asked.

Over in Oncology, I’m keeping an eye on Tarlatamab, Lumakras, Blincyto, and Nplate. They're the revenue drivers of the future, with Tarlatamab aiming for billions by the 2030s.

Lumakras was supposed to be a star, but it's a bit slow out of the gate. Then there's Blincyto – already raking in the big bucks with nearly 50% year-on-year growth. This one's HOT.

Nplate's a blockbuster with almost $2 billion in sales, but US government orders make it a tad volatile. Tezspire is another potential star, flirting with the billion-dollar mark.

Bottom line? Amgen is hustling to build a diverse portfolio for the long haul.

Crunching the numbers, Amgen's 2024 guidance looks strong, boosted by that Horizon acquisition.

They're projecting about $33 billion in revenue and decent EPS. Tax breaks and low capital expenditures are sweet bonuses.

But...remember that debt. It's over $60 billion on the long-term books. Luckily, Amgen locked in good rates on those bonds, but that interest bill? It's a beast they'll have to tame eventually.

Amgen’s shareholder returns are mostly a chunky 3%+ dividend, not much to write home about. The real magic depends on those high-powered sales teams turning the rare disease business into a cash machine and seeing those other drugs deliver. If it happens, cash flow will surge, and everyone will get fatter payouts.

As for the biggest threat to Amgen’s future? The ever-changing, cash-hungry beast that is the biotech industry.

Amgen's constantly fighting patent expirations, forcing them to pump cash into R&D just to stay ahead. You hit some home runs, like the crazy new weight loss drugs driving skyrocketing revenues as seen in the success of Eli Lilly (LLY) and Novo Nordisk (NVO), but more often, you strike out. This is why long-term investors in Amgen should strap in for a bumpy ride.

Overall, Amgen's got a unique mix of assets. And that Horizon Therapeutics move? Bold but calculated. It gives them a boatload of rare-disease drugs and pairs them with top-notch sales teams.

Plus, there's a bunch of promising candidates in their pipeline. The biotech world is an industry where success is never guaranteed, BUT Amgen's got the potential to keep knocking it out of the park. If they do, those shareholder returns should get a whole lot sweeter. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

April 11, 2024

Fiat Lux

Featured Trade:

(BELLY BUSTERS)

(NVO), (LLY), (JNJ), (AMGN), (RHHBY), (GSK), (VKTX)

Did you know that more Americans are now trying to lose weight than trying to quit smoking? That's a staggering shift, and it has a lot to do with the buzz around those new obesity drugs.

Novo Nordisk (NVO) got the ball rolling in 2021 when they received the green light to market their diabetes drug, Ozempic, as a weight loss miracle called Wegovy.

Not to be outdone, Eli Lilly (LLY) swooped in the fall of 2023 with Mounjaro – also a diabetes drug, sold as Zepbound – that got the FDA nod for weight loss, too.

Then, the whole pharma world, it seems, has started to go all-out on obesity, flooding the market with a whole new generation of weight loss drugs.

To date, there are 124 obesity meds in the works – a mix of 61 Phase 1 hopefuls, 47 in Phase 2, eight in Phase 3, and eight already greeting patients.

Remember that whole fen-phen disaster back in the 90s? That left a bad taste in everyone's mouth when it comes to weight loss drugs.

But things are different this time. These new obesity meds, especially those from Novo Nordisk and Lilly, are a game-changer. They're blowing those old weight loss pills out of the water.

It's not about fitting into those skinny jeans anymore (though that's a nice bonus). The focus is on health.

And while Novo Nordisk and Eli Lilly might be the big names in the obesity drug game, they've got competition. There's a whole crew of pharma companies jumping on the bandwagon, like Currax Pharmaceuticals, Roche (RHHBY), GlaxoSmithKline (GSK) – you get the picture.

But here's the really wild part about these drugs like Mounjaro and Wegovy, which use GLP-1 (Glucagon-like peptide-1) compounds to treat diabetes: They kinda stumbled onto their weight loss powers by accident.

Turns out, while they were busy helping diabetes patients, boom, patients started shedding pounds. Talk about a happy side effect.

As expected, this has created excitement in the market. Now, usually in the drug world, it's baby steps forward. A little better here, a bit less nausea there... yawn.

But with eight of these drugs already in the late stages of development (Phase 3), expect even more surprises as potential breakthroughs could bypass traditional drug trial phases for a faster route to market.

Frankly, I'm shocked at the number of new mystery drugs suddenly popping up in early testing. Even those old-school Big Pharma players are jumping in: AstraZeneca (AZN), Novartis (NVS), Amgen (AMGN), and, heck, even Johnson & Johnson (JNJ) – everyone wants a slice of the obesity pie.

Now, this whole obesity meds craze reminds me of what happened with those PD-1 drugs in cancer treatment.

One good result, and suddenly everyone was scrambling to get their version to market. But like in a reality TV show, not everyone makes it to the finale.

But what's the endgame in this obesity market expansion? Not 124 contenders, that's for sure.

Even right now, with everything in its early stages, you can already see which candidates have the potential. The competition's going to get fierce, and only the strongest drugs will survive.

Viking Therapeutics (VKTX), for example, has a dual GLP-1 and GIP agonist showing serious promise. After just 13 weeks, patients lost an average of 14.7% of their weight.

This data, released in February, proves Viking’s not just chasing the big pharma players; they're running right alongside them.

Now, over at Novo and Lilly, the pace hasn’t slowed down one bit either. Wegovy, which is Novo's contender in the ring, just got a nod in March for something a bit bigger than weight loss.

It’s been approved to tackle some serious heavyweights — cardiovascular deaths, heart attacks, and strokes in adults dealing with obesity or who are overweight. It's like getting a one-two punch for health.

As for Eli Lilly? They’ve been making some noise with tirzepatide, especially around metabolic dysfunction-associated steatohepatitis, or MASH for short.

They’ve got results showing that 74% of adults who were either overweight or obese managed to kick MASH to the curb without any increase in liver scarring after sticking with the treatment for 52 weeks.

Sadly, the biggest roadblock isn't the science, it's the money. It’s not just about making these drugs. It’s about getting them into the hands of those who need them most.

The current scene? A bit of a heartbreaker.

Most US insurance companies are drawing the line at covering Wegovy or Zepbound for obesity. This leaves a hefty bill on the table, putting these potentially life-altering treatments out of reach for many.

Think about it – the people who could benefit the most, maybe those on Medicaid or living paycheck to paycheck, are staring at a closed door. And let’s not even get started on Medicare, which, as of now, can’t even touch these drugs.

It’s a strange paradox, isn’t it? The very treatments that could lift the weight of obesity off society’s shoulders are dangling just out of reach for many.

So, now, the burning question isn’t so much about whether these treatments can make shareholders and companies do a happy dance. It’s more about where we’re heading.

Think about cancer treatment – the sickest patients get the cutting-edge drugs first. What would that even look like in obesity?

Will all these 124 experimental options help level the playing field, finally forcing insurers to step up? Only time will tell.

As of now, the obesity treatment field is going through a revolution. While the market faces challenges like accessibility, I suggest you closely monitor the progress of key players like Novo Nordisk and Eli Lilly.

Consider smaller, innovative companies, such as Viking Therapeutics, for potential high-risk, high-reward investments as well.

Mad Hedge Biotech and Healthcare Letter

March 19, 2024

Fiat Lux

Featured Trade:

(NOT JUST A ONE-TRICK PONY, BUT A BIOTECH THOROUGHBRED)

(LLY), (NVO), (PFE), (AMGN)