I've been around the block a few times when it comes to investing, and let me tell you, I know a thing or two about spotting a winner. And right now, there's one name in the biotechnology and healthcare world that's caught my eye like a shiny new penny: Eli Lilly (LLY).

First off, let's talk about Lilly's recent partnership with Amazon Pharmacy (AMZN). This pair is bringing the future to us, offering direct home delivery of Lilly's medications, including the much-talked-about weight-loss drug Zepbound.

You heard that right. Thanks to this partnership, you can now get your hands on Lilly's weight-loss wonder drug, Zepbound, without ever leaving your couch.

Approved last year for obesity treatment, Zepbound is shaping up to be a blockbuster. And let's not forget about LillyDirect, the platform making all this possible, blending healthcare provision with top-notch delivery service.

Since launching in 2020, Amazon Pharmacy has been on a mission to simplify how we get our prescriptions, and teaming up with Eli Lilly only turbocharges this mission.

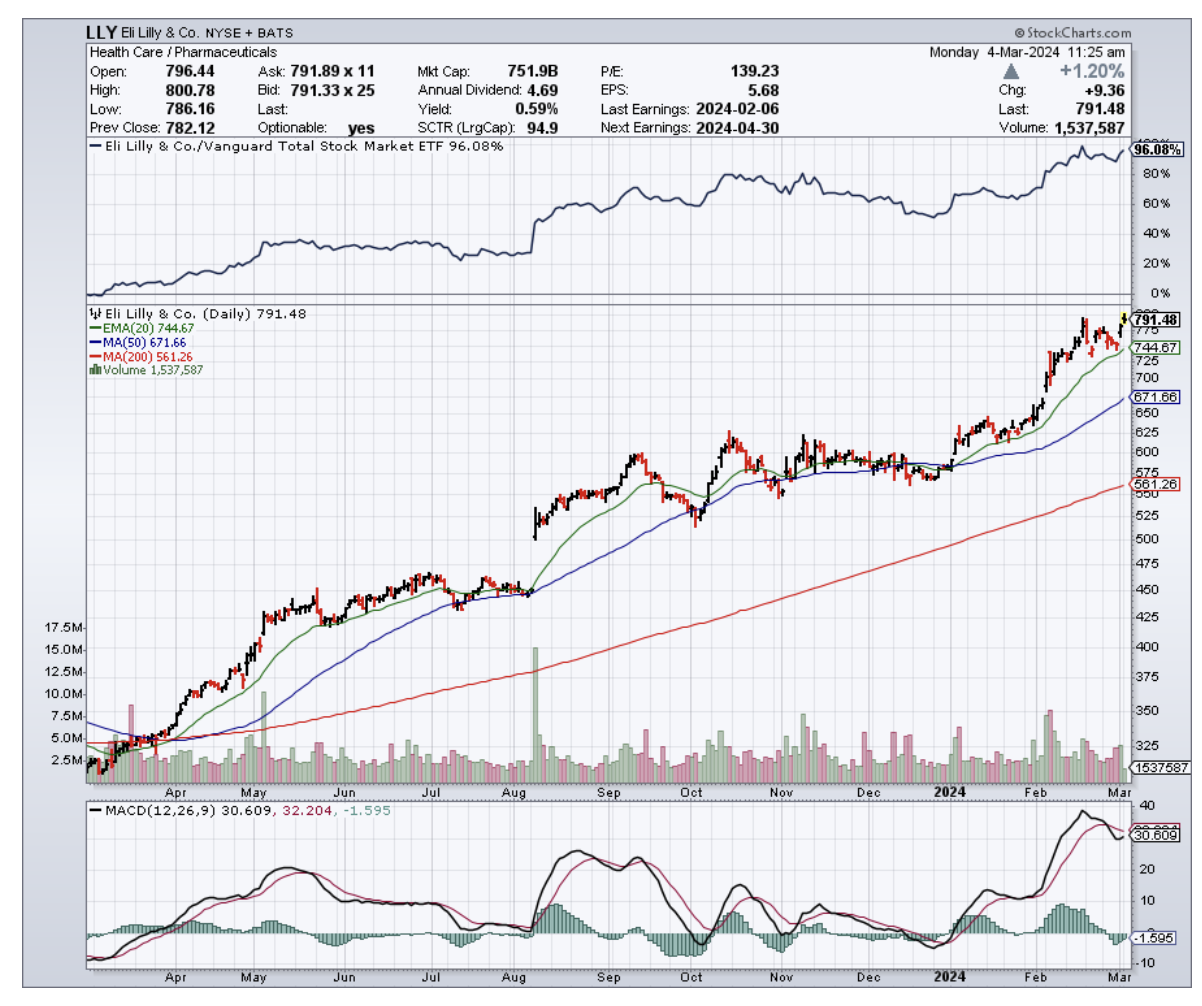

Now, let's talk about Lilly’s financials. This biotech’s market cap has ballooned to an eye-watering $700 billion, thanks to a 130% surge over the past year.

The buzz around Zepbound, showing potential for a 27% reduction in body weight, has investors sitting up and taking notice.

But I hear you ask, "Have I missed the boat on Eli Lilly?" My take? Not at all.

In fact, I think this stock could easily double in value and even surpass the trillion-dollar mark within the next five years. It's a bold prediction, but I've been around long enough to know a sure thing when I see it.

With obesity rates tripling since 1975 and more than half of the global population predicted to become obese or overweight by 2035, the demand for effective treatments like these is going to skyrocket.

Actually, the market for weight loss treatments is projected to reach $100 billion by 2030. And Lilly? They're ready to ride that wave all the way to the bank.

To date, Lilly only has one strong competitor in this space: Novo Nordisk (NVO). While other pharma giants, like Pfizer (PFE) and Amgen (AMGN), are trying their best to gain traction, these two are leaps and bounds ahead.

Now, I know what you might be thinking. "Isn't it expensive to develop these cutting-edge treatments?" You bet your bottom dollar it is.

Lilly isn't afraid to put its money where its mouth is. They're investing heavily in manufacturing capacity to keep up with the inevitable surge in demand. It's a bold move, but that's what separates the winners from the also-rans in the biotech race.

That’s not where it ends though. Lilly has another ace up its sleeve: donanemab, their early Alzheimer's treatment. This could also be a potential competitor of Biogen (BIIB) and Tokyo’s Eisai’s (ESALY) lecanemab, currently marketed as Leqembi.

Sure, the FDA might have put a temporary hold on Lilly’s candidate’s approval, but I've seen this rodeo before. It's just a minor bump in the road for this potentially game-changing drug.

If donanemab gets the green light, it could add billions more to Lilly's already impressive revenue streams. For perspective, the market for Alzheimer’s treatments is predicted to reach $6 billion to $8 billion by 2025 and record $15.5 billion by 2031.

Of course, no investment is without risk. But when I look at Eli Lilly, I see a company that's firing on all cylinders.

They're making strategic partnerships, investing boldly in their future, and have a track record of success that's the envy of the industry.

With a pipeline full of promising treatments, I believe Lilly is poised to gallop its way to even greater heights in the years to come.

So if you're looking for a biotech thoroughbred with a pedigree of success and a bright future ahead, I'd say Lilly is a horse worth betting on.