Below, please find subscribers’ Q&A for the November 20 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, Nevada.

Q: What are your stock recommendations for the end of the first quarter of 2025?

A: I say run with the winners. Dance with the girl who brought you to the dance. I think portfolio managers are going to be under tremendous pressure to buy winners and sell losers. And, of course, you all know the winners—they’re the stocks I have been recommending all year, like Nvidia (NVDA), Tesla (TSLA), and so on. And they're going to sell losers like energy to create the tax losses to offset their gains in the technology area. That could continue well into next year. Although, we’ve probably never entered a new administration with more uncertainty at any time in history, except maybe during the Civil War. I don’t think it will get as bad as that, but it could be bad.

Q: Is Putin bluffing about nuclear war?

A: Yes. First of all, Russia has 7,000 nuclear weapons, but only maybe 200 of those work. If he does use nuclear weapons, Ukraine will use its nuclear weapons in retaliation. During the Soviet Union, where did the Soviet Union make all their nuclear weapons? In Ukraine. That's where they had the scientists. They certainly have the Uranium—that's the hard part. You could literally put one together in days if you had the right expertise around. This will never go nuclear, and Putin has always been all about bluffing. There's a reason why the world's greatest chess masters are all Russian; it's all about the art of bluffing. So that doesn't worry me at all.

Q: Will Russia sacrifice a higher and higher percentage of its population in the war?

A: Yes, that is the military strategy: keep throwing bodies at your enemy until they run out of bullets.

Q: What is your prediction for 30-year US Treasury yields (TLT)?

A: They go higher. Higher for longer certainly includes the 30-year. The 30-year will be the most sensitive to long-term views of interest rates. If you get a return of inflation, which many people are predicting, the 30-year gets absolutely slaughtered. Adding a potential $10 trillion to the national debt, taking it to $45 trillion, is terrible for debt instruments everywhere.

Q: Should we be exiting the LEAPS that you put out on Occidental Petroleum (OXY) and Schlumberger (SLB)?

A: For Occidental, I would say maybe; it’s already at a low. The outlook for oil prices is poor, with massive new production coming on stream. Regarding Schlumberger, they make their money on the volume of oil production—that probably is going to be a big winner.

Q: What do you think interest rates will do as we go into the end of Powell's term in 18 months?

I have no idea. It just depends on how fast inflation returns. My guess is that we'll get an out-of-the-blue sharp uptick in inflation in the next couple of months, and when that happens, stocks will get slaughtered. People assume that inflation just keeps going up forever after that.

Q: Crude oil (USO) has been choppy at around $70 a barrel. Where do you see it going next year?

A: My immediate target is $60, and possibly lower than that. It just depends on how fast deregulation brings on new oil supplies, especially from the federal lands that have been promised to be opened up. As it turns out, the federal government owns most of the western United States—all the national forests and so on. If you open that up to drilling, it could bring huge supplies onto the market. That would be deflationary. It would be death for oil companies, but it would be a death for OPEC as well. Every cloud has a silver lining. OPEC has been a thorn in my side for the last 60 years.

Q: I'm tempted to buy stocks that are flying up, like Palantir (PLTR) and MicroStrategy (MSTR). What would be an experienced investor trade in these situations?

A: Don't touch them with a 10-foot pole. You buy stocks before they fly up, not afterwards. By the way, if anyone knows of an attorney who is an expert at recovering stolen Crypto, please contact me. I have several clients who've had their crypto accounts cleaned out. Oh, and by the way, the heads of every major crypto exchange have been put in jail in the last three years. Imagine if the heads of Goldman Sachs, Morgan Stanley Fidelity, and Vanguard were all put in jail for fraud and theft? How many stocks would you want to buy after that? Not a lot.

Q: Your recommendations for AI and chips?

A: I think you get a slowdown. In order to buy the new plays in banks, brokers, and money managers, you need to sell the old plays. Those are going to be technology stocks and AI stocks—AI itself will keep winning. They will keep advancing, but the stocks have become extremely expensive. And everyone is waiting to see how anti-technology the new administration will be. Some of the early appointments have been extremely anti-technology, promising to rein in big tech companies. If you rein in big tech companies, you rein in their stock prices, too. I am being very cautious here. The next spike up in Nvidia (NVDA) might be the one you want to sell.

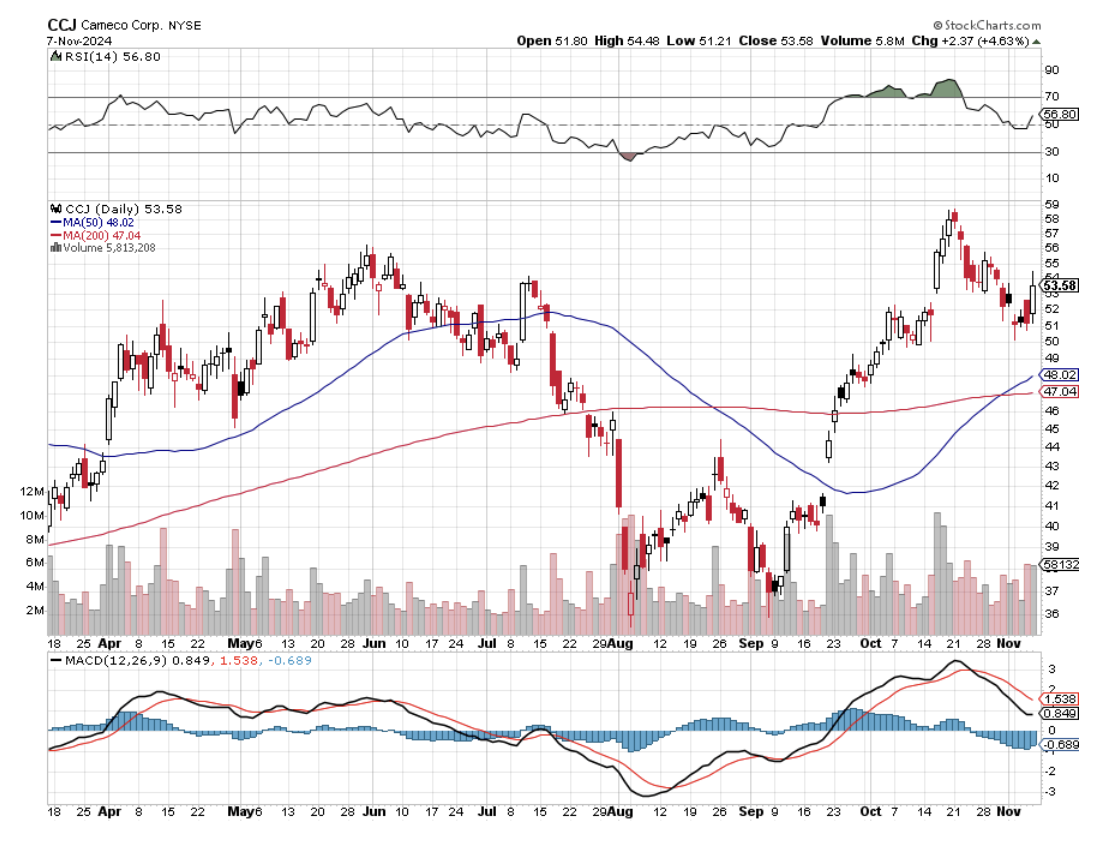

Q: Do you think the uranium play will continue under the new administration?

A: Absolutely, yes. Restrain the Nuclear Regulatory Commission, and costs for the new nuclear starts up like (SMR) go way down.

Q: What do you think of NuScale Power Corp (SMR)?

A: I love it. Again, deregulation is the name of the game—and if you lose a city by accident, tough luck. Let's just hope it happens somewhere else. It's only happened three times before… Three Mile Island, Chernobyl, and Fukushima.

Q: Super Micro Computer (SMCI), what do you think?

A: Don't touch it. There's never just one cockroach. Hiring a new auditor to find out how much money they misrepresented is not a great buy argument to buy the stock. I'm sorry. Very high risk if you get involved.

Q: If Nvidia (NVDA) announces great earnings but sells off anyway, what should I do?

A: Get rid of it and get rid of all your other technology stocks because this is the bellwether for all technology. Tech always comes back over the long term, but short term, they may continue going nowhere as they have done for the last six months, which correctly anticipated a Trump win. Trump is not a technology guy— he hates California. Any California-based company can't expect any favors except for Tesla.

Q: Is there any reason why you prefer in-the-money bull call spreads?

A: Well, there are lots of reasons. Number 1, it's a short volatility play. Number 2 it's a time decay play, which is why I only do front months because that's when the time decay is accelerated. Thirdly, it allows you to increase your exposure to the stock by tenfold, which brings in a much bigger profit when you're right. If you look at our trade alerts, we make 15% to 20% on every trade, and 200 trades a year adds up to a lot of money. You can see that with our 75% return for this year. And it's a great risk management tool; the day-to-day volatility of call spreads is low because you're long one call option short the other. So, the usual day-to-day implied volatility on the combination is only about 8% or 9%. The biggest problem with retail investors is the volatility scares them out of the market at market lows and scares them back in at market highs. So, call spread reduces the volatility and keeps people from doing that. The risk-reward is overwhelmingly in your favor if you have somebody like me with an 80% or 90% success rate making the calls on the stocks. And, of course, having done this for almost 60 years, nothing new ever happens in the stock market—you're just getting repetitions of old stuff. All I have to do is figure out is this the 1970s story, the 1980s story, the 1990s, the 2000s, 2010s story? I have to figure out which pattern is being repeated. People who have been in the market for one year, or even 10 years, don't have that luxury.

Q: I’m having trouble getting filled on your orders.

A: You put out a spread of orders. So if I put in an order to buy at $9.00, split your order up into five pieces: at $9.00, $9.10, $9.20, $9.30, $9.40; and one or all of those orders will get filled. Another hint is that algorithms often take my trade alerts to the maximum price. Don't pay more than that price immediately, but they have to be out by the end of the day, so if you just enter good-till-cancel orders, you have an excellent chance of getting filled by the end of the day or at the opening tomorrow.

Q: Should I purchase SPDR S&P Regional Banking ETF (KRE)?

A: I'd say yes. That probably is a good buy with deregulation, making all of these small banks takeover targets.

Q: What should we be looking for in the fear and greed index?

A: When we get to the high end, like in the 70s, start taking profits. When we get to the low end, like the 20s, start buying and adding LEAPS and more long-term leverage option plays.

Q: What are we looking for to go short?

A: Much higher highs and a bunch of other monetary and technical indicators flashing warning signals, which are too many to go into here. Suffice to say, we did make good money on the short side this year, a couple of times on Tesla (TSLA), including a pre-election short that we covered in Tesla, and we were short a whole bunch of technology stocks going into the July meltdown. So, you know, we do both the long side and the short side, but it's been a long play—11 months this year and a short play for a month.

Q: Is the euro going back up eventually, or does the dollar (UUP) rule?

A: Sorry, but as long as the US dollar has the highest interest rates in the developing world and the prospect of even higher rates in the future, it's going to be a dollar game for the next couple of years.

Q: Will a ceasefire in the Middle East affect the markets?

A: No. The U.S. interest in geopolitical data ends at the shores—all three of them. So if the war of the last couple of years doesn't change the market—and it's been an absolutely horrific war with enormous civilian casualties—why should the end of it affect markets?

Q: What stock market returns do you see for the next four years?

A: About half of what they were for the last four years, which will be about 90% by the time Biden leaves office. You're going to have much higher interest rates and much higher inflation, and while the new administration is very friendly for some industries, it is very hostile for others, and the net could be zero. So, enjoy the euphoria rally while it lasts.

Q: What about crypto?

A: Well, I did buy some crypto for myself at $6,000, and I'm now thinking of selling it at $96,000. Would I recommend it to a customer? Not on pain of death—not at this level. You missed the move. Wait for the next 95% decline, which is a certainty in the future. And, by the way, absolutely nobody in the industry can tell you when that is.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Below, please find subscribers’ Q&A for the November 6 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, Nevada.

Q: What do we do in the market now in view of the Trump Victory?

The driving theme of the market has completely changed overnight. Falling interest rate plays are dead. The new theme is deregulation. The good news is that there are a lot of cheap deregulation plays out there, especially in financials. Deregulation is also a factor with (NVDA), where the government was lining up for an antitrust suit. New nuclear stocks like (CCJ) and (VST) also do well with a lighter regulatory touch.

Q: How will the defense industry perform under Trump?

A: Poorly. If we cease supplying Ukraine with weapons and withdraw from our international commitments, there’s no need for weapons at all. We’ll just have to be happy with the 50-year-old weapons that we have right now. And, of course, that's one of the reasons why Putin was such a big supporter of Trump. Avoid (LMT) and (RTX). Other stocks were already selling off as Trump rose in the polls.

Q: Will housing be a loser with the housing shortage?

A: Yes, it will, because you won’t find home buyers if they don’t have any money—if interest rates and mortgage payments are too high, those buyers are absent from the market. They can’t afford to step up to the current price levels and mortgage levels.

Q: Do you really think the Fed may not cut interest rates?

A: All of the announced Trump policies are highly inflationary, and one of the Fed’s primary missions is to control inflation. But, it comes down to: is the Fed going to look forward or look back? Historically, it is very much a “look back” organization, so they will probably wait on their higher interest rates. And that is what uncertainty is all about; all of a sudden, you go from very firm convictions of what’s going to happen next—what stocks to buy, what sectors to play—to “I don’t know!”. With a Harris win, at least you had some certainly. With Trump, we don’t know what he really wants to do, can do, or be allowed by the courts. It will take time to figure all this out.

Q: Why did none of these issues occur during Trump’s first term?

A: Well, virtually all of Trump’s first term, interest rates were at zero because the Fed was still doing quantitative easing, trying to recover from the ‘08 financial crisis, but also recovering from the pandemic. The amazing thing about the Biden administration is that the stock market did so well during the 5% interest rates that prevailed practically for his entire term.

Q: Do you have a “BUY” target for iShares 20+ Year Treasury Bond ETF (TLT) on the downside after the Trump win?

A: The answer is we are going to retest the low of the year, which is $82 in the TLT, and last time I checked, we were at $89.78—so down seven points. But again, we now have a lame-duck government, so no dramatic action with a split Congress. We basically have until January 20th, when the new government comes in, to find out what they will actually try to do. I think you'll find that the “campaign Trump” and the “in-office Trump” are two totally different people.

Q: Okay, what about the iShares 20+ Year Treasury Bond ETF (TLT) LEAPS position you put out two weeks ago? Should we sell or hold?

A: Well, if you want to be cautious, go cash—sell. But this is a LEAPS that has another 15 months to expiration, and there's a pretty decent chance we'll be going into recession sometime next year, especially if interest rates and inflation take off. That could make your LEAPS trade very attractive—it could drive interest rates down to 3.5%, which is virtually where they were in September. Since September, bonds have basically given up their entire rally for the year on the possibility of a Trump win. So, you know, would I put on that trade today? No. Will I put it on at $82, I probably will. We'll just have to see what the new world looks like.

Q: What's the direction for gold (GLD) and silver (SLV)?

A: Down. Those two plays were dependent on falling interest rates, which are now gone. Now that they're going back up again, it kind of trashes the entire gold-silver trade. So, at some point, gold will drop to a point where the flight to safety bid offsets the fear of rising interest rates. You still have a lot of Chinese savings in gold going on and central bank buying. That's where you get back in. Where that is is anybody's guess.

Q: Any thoughts on Crown Castle International (CCI)?

A: It is an interest-rate play. We did really well with CCI from April to September, when the 10-year treasury went from 4.5% to 3.5%. Run that movie in reverse, and it doesn't do very well. We've had a big sell-off on (CCI) this morning. So it's getting killed on the prospect of rising rates and inflation.

Q: Do smaller stocks do better under Trump?

A: No. Smaller stocks are much more dependent on interest rates than large stocks because they're very heavy borrowers at high rates. So, any rally there should be sold into.

Q: Should I bet the ranch on crypto here?

A: Absolutely not. $6,000 is where you should have bet the ranch on crypto, not at $75,000. Crypto is barely moving today, despite promises by Trump to completely deregulate the sector. So, no, I am definitely not a buyer of crypto here.

Q: What about the gold trade alert that I sent out yesterday?

A: That was on the assumption that Harris would win, and she didn't. If you want to be conservative, get out of the position now. We have five weeks to expiration on that position, so it really depends on where gold finds its bottom—it could hold up here or a little bit lower, and we'll still be at the max profit. If we go into free fall, I'm going to just stop out of the position and write that one off as me being too aggressive before the election when I had the perfect positions going into it, being long JP Morgan (JPM) and Nvidia (NVDA).

Q: Is the Occidental Petroleum (OXY) spread okay?

A: For energy, I would say yes, probably. But we'll have to see how sustainable this current rally is.

Q: So, wait on the currency plays, like (FXA), (FXE), (FXB), and (FXC)?

A: Absolutely, yes. It's another wait for the dust to settle trade.

Q: What will the price of crude oil do from here?

A: Probably go down more with large new supplies coming out of the U.S.

Q: Why are financial stocks up huge?

A: Deregulation. Financials are among the most regulated industries in the world. If you don't believe me, try running a hedge fund someday, where they're breathing down your neck every five seconds for audits, reports, and so on. They also win on the revenue side with restrictions coming off mergers and acquisitions with the end of antitrust enforcement.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.