Mad Hedge Biotech and Healthcare Letter

October 18, 2022

Fiat Lux

Featured Trade:

(JUST WHAT THE DOCTOR ORDERED)

(MRNA), (MRK), (PFE)

Mad Hedge Biotech and Healthcare Letter

October 18, 2022

Fiat Lux

Featured Trade:

(JUST WHAT THE DOCTOR ORDERED)

(MRNA), (MRK), (PFE)

A newly announced collaboration extension with Merck (MRK) might just be what the doctor ordered for Moderna’s stock, which has been experiencing a decline in revenue since the public started resisting boosters.

Moderna stock rose 12% following the news that the FDA approved its collaboration deal with Merck as well as its COVID booster geared towards young kids.

Those positive updates most likely mark the end of a falling knives stage for the company, as it was coming off a 52-week low just days before the announcements.

The deal between Moderna and Merck involves a personalized cancer vaccine, which the two have been working on since 2016. The goal is to use Moderna’s technology as a combo treatment alongside Merck’s mega-blockbuster Keytruda.

The cancer vaccine, currently dubbed mRNA-4157, will be tailored for every patient. It generates a reaction according to the particular mutational signature of an individual’s tumor.

The collaboration is already in its Phase 2 trial for a high-risk melanoma vaccine.

The deal involves Merck shelling out $250 million in cash to exercise its option on this personalized cancer vaccine candidate. Had Moderna not earned copious amounts of cash over its COVID-19 vaccine over the past two years, this money would have seemed like a much bigger deal.

Nevertheless, the agreement is for a 50-50 sharing of costs and, eventually, potential profits. The results of Phase 2 should be disclosed to the public before December 2022.

Regarding how this affects Moderna’s pipeline, the collaboration demonstrates the versatility of the mRNA technology.

The other update that boosted the stock is the emergency use authorization granted to Moderna and fellow COVID-19 vaccine maker Pfizer (PFE), which allowed their boosters to be used on children.

As you know, Moderna markets and sells only a single product: SpikeVax. While this COVID vaccine is, apart from Pfizer’s Comirnaty, the most extensively used worldwide, pushing revenues to $18.5 billion in 2021, and is on track to hit roughly $21 billion in 2022, sales for SpikeVax are expected to decline now that the pandemic has been deemed “over.”

The company’s agreement to 70 million vaccine doses to the US government, on top of the option to purchase up to 230 million, which will be worth about $4.8 billion at $16 per dose, may very well be Moderna’s last to a government.

Currently, the biotech is looking into the private market, in which its vaccine may start costing up to $100.

Reviewing the demand and the current situation, my best estimate is that Moderna would earn roughly $7 billion annually from the private market for its COVID vaccine.

Nevertheless, Moderna’s vaccine has shown proof of concept. This would translate to more confidence in the company’s pipeline. Its expanded collaboration with Merck is a clear indicator of this sentiment.

In terms of the rest of its pipeline, Moderna has several candidates.

The most advanced so far are its Phase 3 programs for a flu vaccine, a respiratory syncytial virus vaccine (RSV), and a cytomegalovirus vaccine (CMV).

Considering the respiratory nature and the resounding success of its mRNA COVID vaccines, it’s reasonable to believe that the Phase 3 trials for these candidates would also be successful.

Hence, Moderna could be looking at substantial revenues once these vaccines enter the market.

While it can be argued that flu vaccines already exist, sometimes being the first to market is insufficient to keep a significant market share.

The current flu market is estimated to be worth $5 billion to $6 billion, and there are definitely a lot of competitors in the sector.

However, Moderna aims to develop a more efficacious vaccine. Needless to say, that could easily command a higher price tag and attract more customers.

Meanwhile, Moderna’s RSV vaccine—if approved—would not have any rivals. This is also another massive segment, with the market for the older adult population alone already worth $10 billion.

Both RSV and flu vaccines are anticipated to be released by late 2024 or early 2025.

When people hear Moderna, they immediately think COVID stock. Then, they immediately begin to wonder about the company’s future. Basically, Moderna has become a victim of its own success.

At the moment, the market is focused on Moderna’s potential revenue loss from its COVID vaccine. That sentiment is clearly weighing on the company’s price, making it undervalued. However, these very same fears make Moderna a steal considering the company’s long-term prospects well beyond its COVID program.

Long-term investors would see this as an opportunity to buy an innovative biotech for a bargain and reap the rewards when Moderna’s other candidates start to gain momentum.

The previous month was another difficult time for the markets, with the S&P 500 sliding 9%. Meanwhile, the index has already fallen 24% year to date, dragging several quality businesses along with it.

The silver lining for long-term investors is that many of these beaten-down stocks won’t remain down for long. That means buying flailing quality stocks today, as risky as it may sound, could offer you an opportunity to lock in several high-yielding businesses at cheaper valuations.

In the biotechnology and healthcare world, one of the most promising buys so far is Pfizer (PFE).

This company’s stock price has fallen by 16% in the past six months as Pfizer’s COVID-19 vaccine profits are anticipated to decrease. However, there’s something that investors appear to be overlooking.

The sales of the COVID-19 vaccine, Paxlovid, may gradually decrease, but the fact remains that its bolstering Pfizer’s pipeline. While its bottom line will expectedly show signs of decline as concerns around the coronavirus subside, its revenue won’t disappear completely.

Paxlovid sales are estimated to reach roughly $12 billion in the second half of 2022.

After all, health officials are continuing to administer booster shots, and there’s really no concrete answer if and when that will eventually end.

Moreover, Paxlovid is one of only two preferred antiviral treatments for patients at high risk for severe COVID-19. Based on CDC data, 50% to 60% of the US population aged 12 and above will experience one or more symptoms for progressing to a more severe stage of the disease.

This, along with the additional approvals in other countries, has reaffirmed the $22 billion revenue guidance for Paxlovid this 2022.

Needless to say, injecting this much cash flow into a company—even a large-cap business—would move the needle and put it in a very healthy financial position.

Pfizer’s continued strength amid the chaotic year can be seen in its second-quarter financial report in 2022. In fact, Pfizer reported its highest quarterly sales ever in its history in this quarter.

The company recorded its revenues increased to $28 billion, up by 47% compared to the $19 billion it reported in the same period in 2021. Its net income climbed by an impressive 78% year over year from $5.6 billion in the same period in 2021 to $9.9 billion.

This increase is driven by the substantial contributions of its COVID-19 products, Paxlovid and Comirnaty.

Hence, Pfizer has all but guaranteed that it can stay profitable and deliver outstanding results despite the anticipated decline in Paxlovid sales.

On top of that, the low earnings multiple indicates that a lot of bearishness was already built into the stock. But, the market’s fears seem to do little to slow down Pfizer.

Pfizer has increased its budget for R&D from $2.2 billion in the second quarter of 2021 to $2.8 billion in the same period in 2022.

The company has been aggressive in its decision to acquire several businesses in 2021 and 2022, growing its presence and expanding its portfolio.

More importantly, these new additions have transformed Pfizer into a more diversified company. For example, the company closed on the deal buying ReViral, which is a clinical-stage organization that focuses on treatments for the respiratory syncytial virus (RSV). The addition of ReViral’s resources provides a more solid direction for Pfizer’s ongoing RSV trials.

Aside from that, there are several additional opportunities for this drugmaker.

Pfizer is known to be able to consistently deliver positive free cash flow, which means it's in excellent shape to pursue expansion and growth opportunities while still comfortably paying out a solid dividend. Over the last five years, Pfizer has boosted its dividend by 25%.

So far, the company’s dividend yield is at 3.7%, which is more than twice the S&P 500 average of 1.8%.

Overall, Pfizer is a solid business with an expanding portfolio, a growing pipeline, tons of cash, and an impressive yield. It’s almost impossible to go wrong with this business, particularly at its low valuation these days.

Mad Hedge Biotech and Healthcare Letter

September 27, 2022

Fiat Lux

Featured Trade:

(LAST CHANCE AT SALVATION)

(BIIB), (ESALY), (RHHBY), (LLY), (NVS), (AMGN), (REGN), (BMY), (ABBV), (MRK), (PFE)

Biogen (BIIB) is taking another crack at Alzheimer’s. This is a crucial moment for the biotech following its move to abandon its plans to market Aduhelm, another Alzheimer’s treatment after healthcare insurers refused to pay for it despite gaining FDA approval.

The moment of truth will come this fall when Biogen and Eisai (ESALY) are anticipated to share the results of their massive trial created to determine whether lecanemab, their latest candidate for Alzheimer’s, can deliver its promise to decelerate the progression of the neurodegenerative condition in early-stage patients.

Needless to say, an effective Alzheimer’s drug would not only bring incredible development and hope for patients and their loved ones but also offer a much-needed reprieve for Biogen.

Success would push the biotech to pursue a quick turnabout, with Biogen and Eisai already planning to request an accelerated approval. If the Phase 3 data turns out promising, then the next move would be to clear the way to get Medicare coverage, ensuring that the Aduhelm debacle won’t happen again.

In terms of market opportunity, treatments like lecanemab can rake in over $20 billion in sales in the United States alone.

Still, investors remain cautious. After all, betting on a positive result of an Alzheimer’s trial has proven to be a wrong move in the past—a sentiment that’s apparent in Biogen’s beaten-down price these days.

When Aduhelm gained approval in June 2021, Biogen’s shares climbed almost 40%. Unfortunately, the price steadily fell as the biotech encountered roadblock after roadblock since the drug’s approval and commercialization.

Last year, Biogen shares rose from $270 to hit $400 following Aduhelm’s approval. These days, the biotech has been trading at roughly $205. That’s about 40% below its price in 2018.

By April 2022, Biogen threw in the towel when Medicare flat-out rejected any request to pay for Aduhelm.

More than that, though, Biogen’s results for its lecanemab trial could spell the difference for other Alzheimer’s drugs in late-stage development, including the candidates from Roche (RHHBY) and Eli Lilly (LLY).

What would happen if Biogen fails again?

A failure would make the beginning of a new period for the biotech. Looking at Biogen’s pipeline and portfolio, it’s clear that the next move would either be to sell off pieces of the company or become more aggressive in pursuing mergers.

With the primary business unable to deliver, the expectations shift to the pipeline to pick up some slack. Unfortunately, Biogen’s lineup looks underwhelming. Its disastrous Aduhelm project caused too much damage to the biotech’s finances, restricting its clinical trials.

While Biogen remains the biggest pure neurology biotech thus far, this position is under attack, and its pipeline seems too slow to react in the wake of back-to-back failures.

Reviewing Biogen’s pipeline in Phase 3 trials does not show any candidates that stand out as groundbreaking or transformative. None has the capacity to anchor the company anytime soon.

Apart from that, Biogen is facing fierce competition in its other treatments, including its MS portfolio from the likes of Novartis (NVS), Amgen (AMGN), and Regeneron (REGN).

Meanwhile, more and more pharma names are challenging its neurology drugs like Bristol Myers Squibb (BMY), AbbVie (ABBV), and Merck (MRK). Even Pfizer (PFE) is making a play in this sector with its plan to acquire neurology biotech pure-play Biohaven.

Given Biogen’s track record, the best thing to do right now is to sit and wait until the data are out. If the data turns out positive, then the opportunity would be massive enough for investors to buy in later.

Besides, Eli Lilly and Roche will also release their results in the following months. Those will offer a clearer path and better flesh out the picture of the future of this segment. Most importantly, these will provide investors with safer options to make their bets.

Mad Hedge Biotech and Healthcare Letter

September 22, 2022

Fiat Lux

Featured Trade:

(GOOD THINGS COME TO THOSE WHO WAIT)

(NTLA), (IONS), (TAK), (CRSP), (EDIT), (CRBU), (BEAM), (ALNY), (PFE), (REGN)

CRISPR technology has been receiving so much hype over the past years. However, the promise of this gene editing platform has yet to be realized.

Crispr gene-editing therapies can apply permanent modifications to our DNA by zeroing in on specific genes and then incapacitating them or reworking harmful segments of their genetic instructions.

While this could change in the coming years, investors have become impatient with the progress and lack of any major breakthrough in genomics. Some are losing confidence that this sector could experience explosive growth.

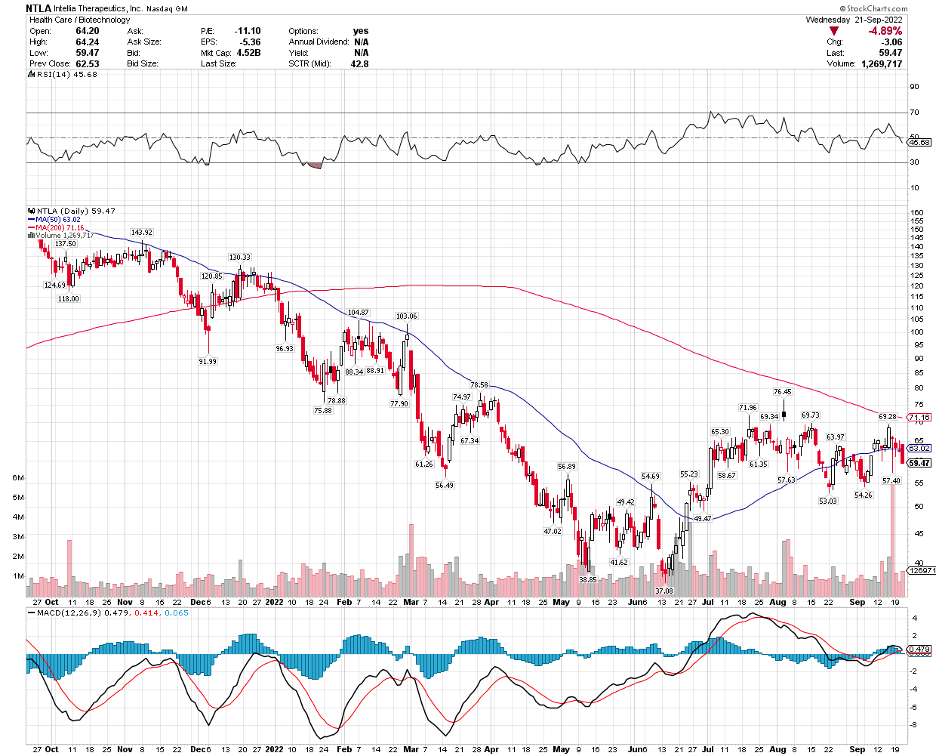

This is what happened with Intellia Therapeutics (NTLA).

Earlier this week, the company showed data that patients who received a one-time gene-editing infusion exhibited sustained improvement in a genetic condition that can result in fatal swelling when left untreated.

To be more specific, Intellia’s update means it could deliver a potentially permanent solution for hereditary angioedema. In this condition, a patient has a miswritten gene in their liver cells that produces a specific protein that triggers a dangerous swelling throughout the body.

Applying the treatment to 6 patients, Intellia’s one-time treatment lowered blood levels of the harmful proteins by more than 90% and decreased the swelling.

This is a more notable effect than the results from existing drugs like Takhzyro from Ionis Pharmaceuticals (IONS) and Takeda Pharmaceutical (TAK).

Despite the encouraging update, Wall Street still spurned the stock, and its price fell.

It looks like investors have lost patience with the slow progress of clinical studies in genetic treatments, pushing some to take advantage of the positive news from Intellia to abandon their positions.

Actually, it’s not only Intellia that suffered from this mistreatment by the market. Investors have also been dumping other stocks utilizing the Nobel-prize-winning technology, Crispr-Cas9, including CRISPR Therapeutics (CRSP), Editas Medicine (EDIT), Caribou Biosciences (CRBU), and Beam Therapeutics (BEAM).

Intellia was hailed the top CRISPR stock in 2021 when the company and its co-collaborator, Regeneron (REGN), shared their promising interim results from a Phase 1 study assessing NTLA-2001, a treatment for a rare genetic disease called transthyretin (ATTR) amyloidosis.

This Crispr infusion candidate managed to knock out rogue genes in the liver cells of 12 patients, halting ATTR’s poisonous effects on their hearts or nerves. Based on clinical data, Intellia’s therapy caused an over 90% drop in the fatal protein triggered by the genetic condition.

If successful, this one-and-done ATTR treatment from Intellia would go head-to-head against other chronic drug therapies like Onpattro by Alnylam Pharmaceuticals (ALNY) or Pfizer’s (PFE) Vyndagel, which generates $2 billion in sales every year.

Many companies use Crispr technology to edit human genomes in an effort to treat and possibly even cure rare genetic diseases. Their treatments typically utilize either an ex vivo or an in vivo approach. With ex vivo therapies, the genes are altered outside the patient’s body.

However, Crispr’s use is not only limited to targeting genetic conditions. There are also gene-editing companies that are working on leveraging the technology to come up with treatments for various kinds of cancer.

In particular, Crispr technology has been a biotech favorite in the development of chimeric antigen receptor T-cell or CAR-T therapies. There are used to genetically engineer immune cells to target specific tumors.

Apart from these, some biotech companies are using Crispr technology to conduct screening. This is different from genetic testing, though.

When using Crispr for screening, the genes are modified in a manner that makes them nonfunctional or inoperative. Crispr screening allows biotechs to explore which genes take on particular functions, which can be critical in the development of drugs and treatments.

Intellia’s recent updates are clear indications that Crispr technology works. Since this will be applied to humans, we should expect the timeline and adaptation to take longer.

I have become more and more thrilled with developments in the gene editing space. Moreover, I believe it’s no longer about “if” but when it will happen.

Overall, the gene editing sector is not for fast-paced investors. This is for those willing to wait for a very long time, particularly for stocks like Intellia Therapeutics.

Mad Hedge Biotech and Healthcare Letter

September 6, 2022

Fiat Lux

Featured Trade:

(ONLY FOOLS RUSH IN)

(APDN), (RVPH), (NERV), (JNJ), (BMY), (AZN), (LLY), (PFE)

Following a promising first half of 2022, it looks like the markets are taking an about turn as more and more investors start dumping their stocks.

The seemingly recovering Nasdaq Composite showed a 4.3% decline last month despite reporting its best record since 2020 just last July.

Nevertheless, several biotech names appear to have avoided the crash thanks to some exciting company-specific updates.

The top gainers so far include Apple DNA Sciences (APDN), which skyrocketed 340% by the end of August. Among the projects in its pipeline, the most promising to date is its monkeypox virus test.

Another name on the list is Reviva Pharmaceuticals Holdings (RVPH). This clinical-stage biopharmaceutical firm reported a whopping 244% gain during its second-quarter earnings report.

However, the top gainer that has been on the news lately is Minerva Neurosciences (NERV). This budding biopharmaceutical company gained 321%, according to its report last month.

Minerva Neurosciences isn’t a name I have kept track of nor even heard of until these past months when its wild upswing started to make me curious.

The company started attracting attention when billionaire Steve Cohen of Point72 Asset Management fame invested in it. This move saw Minerva Neurosciences’ shares soar to more than 70% at that time.

Just before August wrapped up, the company filed for its long-delayed schizophrenia treatment, Roluperidone.

Entering the neuroscience industry is a clever move, especially with the potential of this segment. In 2021, this market was estimated to be worth $32.22 billion. By 2027, the neuroscience segment is projected to reach $41.24 billion.

As for schizophrenia, roughly 1% of the entire population is affected by this disease. Based on recent WHO reports, more than 24 million individuals are suffering from schizophrenia annually.

In 2021, the global schizophrenia drug market was reported to cost $8.02 billion. Taking into consideration the changes in the environment and living conditions, the number is expected to go higher as the years pass. With these in mind, the estimated worth of this market is expected to reach $10.15 billion by 2027.

Minerva Neurosciences wouldn’t be the first to take interest in the schizophrenia segment. Prior to this biopharma’s entry, there have already been a handful of key players attempting to be hailed as the leader of this sector.

The names include Johnson & Johnson (JNJ), Bristol-Myers Squibb (BMY), AstraZeneca (AZN), Eli Lilly (LLY), and Pfizer (PFE).

However, only Minerva Neurosciences specifically targets the negative symptoms of schizophrenia. That makes the company stand out in this steadily growing segment.

Given that Minerva Neurosciences is cheaper than these stocks, would it then be wise to buy shares from the smaller company to gain entry into the neuroscience market?

At this point, Minerva Neurosciences has yet to prove that it’s more than just a one-trick pony. In fact, the company has not even sufficiently shown that it has mastered its single trick.

When looking at the potential of any biotechnology and healthcare company, I generally begin by checking out its pipeline.

For Minerva Neurosciences, the list does not look sustainable.

The company’s MIN-301 for Parkinson’s Disease remains inconsequential since it’s still in the preclinical trial stage.

Prior to this, Minerva Neurosciences worked with JNJ to develop treatments for insomnia and major depressive disorder. However, those have yet to yield tangible results that can move the needle for the company’s share price.

That means Minerva Neurosciences is all about Roluperidone. While the company is moving as fast as it could to launch the product to market, more questions remain than answers.

Actually, the company seems to have eliminated earnings conference calls. These could have been useful in offering a more accurate picture of its future, but it looks like investors will need to make do with whatever information is published.

Admittedly, exciting times could very well be waiting for Minerva Neurosciences’ shareholders. The recent progress with Roluperidone most likely offered them some relief.

No doubt that the optimistic investors are hoping that the 321% gain would signify another incredible run in the following weeks. However, this might not be likely. In fact, a pullback seems to be more in the horizon.

Considering its sparse pipeline and the lingering uncertainty over Roluperidone’s performance, this might not be the best time to buy Minerva Neurosciences’ shares.

Mad Hedge Biotech and Healthcare Letter

August 30, 2022

Fiat Lux

Featured Trade:

(THE TIMES ARE A-CHANGING)

(NVS), (LLY), (ALC), (GSK), (PFE), (JNJ), (BMY)