Mad Hedge Biotech & Healthcare Letter

December 22, 2020

Fiat Lux

FEATURED TRADE:

THE MOST FAMOUS CANCER STOCK YOU’VE NEVER HEARD OF

(TRIL), (NVAX), (PFE), (IMMU), (SHOP), (GILD), (ABBV)

Mad Hedge Biotech & Healthcare Letter

December 22, 2020

Fiat Lux

FEATURED TRADE:

THE MOST FAMOUS CANCER STOCK YOU’VE NEVER HEARD OF

(TRIL), (NVAX), (PFE), (IMMU), (SHOP), (GILD), (ABBV)

Biotechnology stocks have proven time and time again to be excellent growth vehicles for risk-tolerant investors.

Underscoring this claim are companies like COVID-19 vaccine frontrunner Novavax (NVAX), which generated jaw-dropping returns on capital for their investors within an impressively short period.

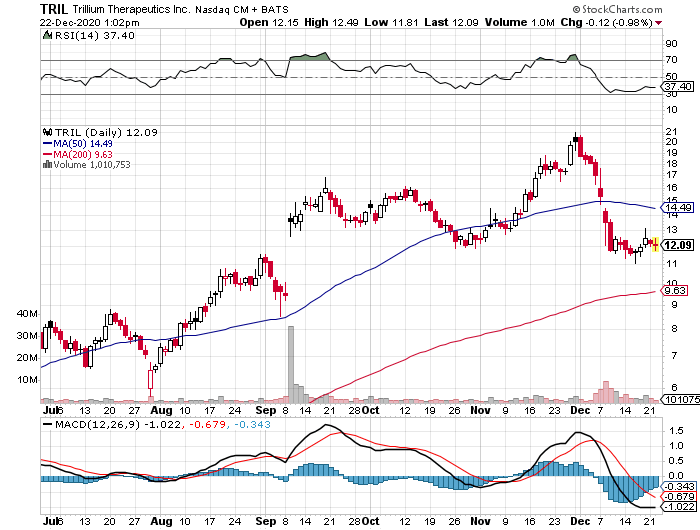

Now, another biotechnology stock is showing telltale signs of following their footsteps: Trillium Therapeutics (TRIL).

Trillium’s story is a familiar one in the biotechnology industry.

Trading only in the penny stock range back in 2019, the company’s share price practically quadrupled since the start of 2020.

Taking into consideration that this meteoric rise actually happened while COVID-19 was blasting the world to smithereens, it’s hardly surprising that this news didn’t receive much media attention.

Trillium’s shares are currently up by an astounding 1,260% -- and the company still has so much room to grow from here.

For context, Trillium had a market capitalization of $7 million in November 2019. This number skyrocketed to $1.3 billion since its shift to cancer technology.

Although a lot of factors came into play, the key turning point for Trillium was when the company decided to go all-in on its cancer programs.

Ultimately, Trillium’s goal is to challenge chemotherapy.

The move to shutter its lead programs on tumor treatments and instead focus on developing cancer-fighting technology was the gamble of a lifetime for the company.

This gutsy move impressed investors, and Trillium was never the same since then.

Today, Trillium is the No. 1 stock on Canada’s S&P/TSX Composite Index, overtaking its previous leader e-commerce giant Shopify (SHOP) by almost 10-fold.

In the US, Trillium shares rank as the No. 4 best-performing company on the Nasdaq Composite Index.

While its epic stock market rally may have some investors feeling left out, all signs point to further gains in the future even for those who missed the initial boom.

Among the major capitalists of this biotechnology company is giant biopharmaceutical company and COVID-19 vaccine leader Pfizer (PFE), which invested $25 million in Trillium’s common stock.

While this equity stake may seem small in relation to Pfizer’s $212.16 billion market capitalization, this initial show of confidence is hailed as a prelude to an even bigger investment in the future.

So far, the most exciting cancer treatments in Trillium’s pipeline are TTI-621 and TTI-622.

These programs are in the same class of emerging cancer technologies, called CD47-based therapies, that prompted Gilead Sciences’ (GILD) $4.9 billion acquisition of Forty Seven, Inc. in April this year.

Aside from Gilead, AbbVie (ABBV) has also been reported to have invested a huge sum in this technology.

In simplest terms, CD47-based therapies can bypass the “don’t eat me signal” put up by some cancer cells in an effort to evade immune detection.

Thus far, both TTI-621 and TTI-622 have been showing promising results. Trillium recently announced that it will increase the dosage in these programs.

While Trillium leaders have not been specific in terms of being open to an acquisition, their recent statements indicate that they are not completely opposed to one.

It’s either that or a partnership with a company as big or even bigger than Pfizer.

As with all the biotechnology stocks, however, there will always be a risk.

For Trillium, the most evident one is competition.

While it’s true that the company has been recognized as the leader in the CD47 arena, more and more competitors are entering the immuno-oncology space.

Right now, the most obvious rival is Gilead, which added Immunomedics (IMMU) to its arsenal via a $21 billion acquisition deal.

Given the sheer amount of money that Gilead has been spending to practically corner the immuno-oncology market, it’s to be expected that more biopharmaceutical titans will enter the fray.

This is one of the reasons Trillium has been tagged as a prime candidate for a massive acquisition deal soon. So far, Pfizer is considered the most probable suitor.

Despite its astonishing performance this year, Trillium’s market capitalization still remains within the small-cap territory. That’s to be expected since its lead assets are still undergoing trials.

Considering that it is an early-stage biotechnology stock, Trillium does not have much in terms of income.

However, the company does have enough cash to last for a while. At the moment, it has $130 million cash.

With its total expenses of $38.8 million in 2019, I say this could offer the company more than three years of breathing room financially.

But it would be shocking if Trillium’s value won’t enter the large-cap territory (higher than $10 billion) if and when the company’s high-value assets reach the late-stage studies.

The fact that it’s also an attractive acquisition candidate offers incredible incentive to its investors.

Simply put, Trillium’s stock could get as much as 1,000% gain over the coming two to three years, making it an ideal investment for risk-tolerant investors.

Mad Hedge Biotech & Healthcare Letter

December 17, 2020

Fiat Lux

FEATURED TRADE:

(ALL HAIL THE DIVIDEND KING)

(JNJ), (PFE), (GSK), (SNY), (MRK), (MRNA)

Major problems have the tendency to attract major problem solvers.

That’s why it came as no surprise when the biggest pharmaceutical companies, like Pfizer (PFE), GlaxoSmithKline (GSK), Sanofi (SNY), and Merck (MRK), jumped in to work a solution the moment a global pandemic threatened the planet.

Now, another big name in the healthcare industry is set to release its own solution.

As Johnson & Johnson (JNJ) releases more positive data from its COVID-19 vaccine program, it becomes more obvious that the company won’t simply be one of the businesses benefiting from the world turning the corner on the pandemic—it will be one of the companies making that happen.

While companies like Pfizer have already gained approval and are out in the market today, JNJ’s day in the sun could be happening sooner than anticipated as well.

What we know so far is that JNJ would be able to manufacture at least 1 billion doses of its COVID-19 vaccine, JNJ-78436735, by early 2021. Given the company’s massive production capacity, catching up with the global demand won’t be an issue either.

More importantly, JNJ’s vaccine offers more convenience in terms of storage compared to current leaders Pfizer and Moderna (MRNA) since JNJ-78436735 does not need ultra-special requirements.

Unlike the other vaccines, JNJ’s candidate can be stored at refrigerator temperature for up to three months.

Plus, JNJ-78436735 is formulated to be a one-dose vaccine, which means it would be easier to administer than the two-shot candidates from Pfizer and Moderna.

While this is great news, the company already announced that it would be selling JNJ-78436735 at cost during the pandemic.

That doesn’t necessarily mean that JNJ is doing all these for purely altruistic reasons though. Even when the pandemic is over, there will still be a demand for the COVID-19 vaccine.

The market for this is estimated to be worth roughly $100 billion in sales and over $40 billion in profits.

If approved, then JNJ can comfortably share this opportunity with competitors.

Given the pricing and the target market, JNJ is projected to earn at least $3 billion in sales for JNJ-78436735 in 2021 alone.

However, the appeal of JNJ stock does not lie in its COVID-19 vaccine candidate.

Pretty much like industry stalwarts such as Walmart (WMT), JNJ is one of the safest blue-chip stocks.

Founded in 1886, it has shown its capacity to weather practically all types of market crashes thanks to its consumer defensive strategy.

While JNJ is not immune to setbacks, as it faced patent expirations for its best-selling drugs and even lawsuits for products like Tylenol and the infamous Baby Powder legal battle, the company managed to repeatedly bounce back primarily because of its well-diversified business segments.

Simply put, its strong products easily offset the weaknesses.

JNJ manufactures and markets basic items like bandages, baby formula, and even skincare products—all of which are goods that customers continue to buy regardless of what is happening to the economy.

Specifically, JNJ owns a number of multibillion-dollar brands like Band-Aid, Listerine, and Nicorette. However, it doesn’t heavily rely on already established names.

For instance, its consumer health sector—the smallest segment in the company—raked in $13.9 billion in sales in 2019.

Meanwhile, its medical devices division generated $26 billion in the same year.

Its pharmaceuticals sector, which covers drugs and treatments for infectious diseases, oncology, and cardiovascular, brought in a whopping $42.2 billion.

A more recent demonstration of JNJ’s ability to weather market downturns is the company’s third-quarter earnings report, which showed a 3.8% jump in its EPS to hit $2.2 and a 1.7% increase in its sales to reach $21.1 billion.

By 2021, JNJ is projected to report a 9% increase in its revenue and a 12% earnings growth following the easing of the pandemic woes and the increasing sales of its top cancer treatments Darzalex and Imbruvica.

Over the past five years, JNJ’s stock has rallied by over 40% and generated a total return of 65%.

To date, this stock trades at merely 17 times forward earnings and pays a respectable forward yield at 2.7%, making it a good investment at a decent price.

As in the past, it’s easy to bet on JNJ’s dividend growth in the next years and even decades for three main reasons—an extremely diversified portfolio that already has an established solid footing across global markets, a rock-solid balance sheet, and a hyper-focus on development and growth.

JNJ’s solid foothold in the worldwide healthcare market along with its innovative R&D spending serves as key drivers for its impressive cash flow and consistent dividends.

Most investors are familiar with companies tagged as Dividend Aristocrats. These stocks are part of the S&P 500 group that managed to increase their dividends for at least 25 years in a row.

However, there’s an even more elite group of dividend stocks that do not get as much fanfare: the Dividend Kings.

To be categorized as a Dividend King, the company must be able to grow its dividend for at least 50 consecutive years.

Since it went public 76 years ago, JNJ has been able to boost its annual dividend for 58 straight years---making this company one of the globally recognized Dividend Kings of the S&P 500.

Mad Hedge Biotech & Healthcare Letter

December 15, 2020

Fiat Lux

FEATURED TRADE:

(DON’T BUY ASTRAZENECA FOR ITS COVID-19 VACCINE)

(AZN), (PFE), (MRNA), (ALXN)

AstraZeneca (AZN) is one of the leaders in the COVID-19 vaccine race, but you wouldn’t have guessed it by observing the stock price in the past months.

The indifference might be rooted from the company’s recent issues with its vaccine candidate, AZD1222, which includes dosing errors and lack of transparency on their trial data.

In comparison, frontrunners like Pfizer (PFE) and Moderna (MRNA) have been gaining back to back approval from the FDA and even from investors.

Let me tell you why this doesn’t really matter for AstraZeneca anyway.

For one, AstraZeneca won’t even make a profit from its COVID-19 vaccine candidate. In fact, the British drugmaker pledged earlier this year that it will sell AZD1222 at no profit.

So, what is the financial benefit of AstraZeneca’s vaccine?

The potential big win from this COVID-19 program is not from AZD1222 itself, but from AstraZeneca’s long-acting antibody cocktail.

This treatment could be the solution needed to prevent the progression of diseases among patients who are already infected with the virus. It can also be used as a preventive measure, which can last up to 12 months, for those who cannot take a vaccine.

If AZD1222 gains approval, then this COVID-19 vaccine is projected to add $3 billion—an impressive 30%—to AstraZeneca’s 2021 profits.

The approval of this technology would also fall nicely in place with the rest of AstraZeneca’s plans.

Since the start of 2020, AstraZeneca has made it clear that it would start pivoting to focus on rare diseases.

Its latest plan towards developing this expertise is the $39 billion acquisition of biotechnology company Alexion Pharmaceuticals (ALXN).

Here’s the nitty-gritty of this massive merger.

The $39 billion price tag comes in the form of cash and stock, putting each share at $175. Alexion shareholders will get $60 in cash on top of 2.1 AstraZeneca shares for every share they own. Aside from that, Alexion will own 15% of the newly formed company.

If everything goes according to plan, then the deal will be completed by the third quarter of 2021.

This acquisition will significantly expand the R&D programs of AstraZeneca, especially its highly specialized and rare diseases sectors.

This combined company is estimated to rake in double-digit growth in its revenue through 2025, with the company potentially gaining significant synergies of roughly $500 million annually – a fair price that could easily justify the premium price AstraZeneca paid for the merger.

AstraZeneca should also be able to expect double-digit increases in its core EPS accretion for the first three years, with the company realistically anticipating a strong FCF with a strong investment-grade rating.

Now, let’s take a look at what Alexion brings to the table.

Alexion is one of the most promising biotechnology companies to date, which managed to achieve significant growth since its IPO. From 2017 to 2020, the company managed to boost its annualized revenue by 20%, growing from $3.5 billion to $6 billion.

With a market capitalization of $34.21 billion, it has invested a significant part of its budget to the development of rare disease drugs.

The most popular products in Alexion’s portfolio are chemotherapy drugs Ultomiris and Soliris, which generated $4.3 billion in combined sales in 2019 alone.

For 2020, sales of these two treatments are expected to rise by 17% to reach $5 billion.

Prior to this deal with AstraZeneca, Alexion has been engaged in an acquisition spree since 2018.

It managed to snap up four smaller biotechnology companies for $4 billion in total, with its $1.4 billion purchase of Portola Pharmaceuticals as its most recent deal.

Truth be told, the performance of Alexion’s rare disease treatments in the market didn’t skip a beat despite the pandemic in 2020.

In fact, these products have been substantially outperforming expectations that the company itself presented in January.

With this merger, AstraZeneca will gain access to Soliris and its widely successful follow-on medication Ultomiris.

Apart from these mega-blockbuster drugs, AstraZeneca will also get its hands on a handful of treatments for rare metabolic diseases, making the company on pace to rake in roughly $840 million in revenue for this year alone.

With all these plans in place, it’s clear that the strongest reason to buy AstraZeneca is not its COVID-19 program.

Buy this stock for the promising long-term prospects not only for rare diseases, but also for its treatments in cancer, cardiovascular diseases, and even diabetes. Buy it as well for its consistent growth, with the company braving the pandemic headwinds and achieving 10% revenue growth and a 16% jump in core EPS to date.

Global Market Comments

December 14, 2020

Fiat Lux

FEATURED TRADE:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GREAT ASSET SHORTAGE),

(INDU), (PFE), (MRNA), (PTON), (DOCU), (ETSY), (CAT), (JPM), (BABA), (TSLA), (TLT), (ABNB), (DIS)

Markets are wonderful arbiters of the laws of supply and demand.

When there is a shortage of a particular security, Wall Street has a magical ability to manufacture more by running the printing presses to meet supply, or in the modern incarnation, open the spreadsheets.

Except for this time.

The amount of new cash created by global quantitative easing and the prolific saving habits of locked up Americans are creating more demand than even this efficient highly process can accommodate.

Which means that prices can only go up.

How long and how far is anyone’s guess. My target for the Dow Average is 120,000 in ten years, but even I don’t expect that to take place in a straight line. So, we are all sitting on our hands waiting for the next pullback to buy into, which may….or may not ever happen.

A lot of Dotcom Bubble memories are rising up from the dead. Analysts in 1999 made outlandish forecasts of stocks rising 50% in a year, which then took place in four days. That happened to Tesla (TSLA) last month and Airbnb (ABNB) last week.

In the meantime, the smartest traders, call them the oldest traders, are taking profits on the best years of their careers.

Of course, the short-term direction of the market will be determined by the January 5 Georgia Senate election, where the polls are in a dead heat. The last time this happened, during the presidential election, the Democrats won by a microscopic 15,000 vote margin.

If history repeats itself, the Biden administration will get an extra $6 trillion to play with to restore the shattered US economy. Think $2 trillion for infrastructure spending in all 50 states, $2 trillion for the rescue of bankrupt states and municipalities, $1 trillion for alternative energy and EV subsidies, and another $1 trillion in odds and ends. Needless to say, much of this will end up in the stock market.

I am getting a lot of questions these days regarding what will end this once-in-a-generation runaway bull market. The pandemic created this bull market by accelerating technology, business evolution, and corporate profitability by ten years. I bet a year ago, you weren’t spending your day on Zoom meetings, as I was.

The great irony is that the Pfizer (PFE) and Moderna (MRNA) vaccines may not only kill Covid-19 but the bull market as well. That’s because money will then come out of stocks and go back to the real economy.

That makes pandemic darlings like Peloton (PTON), DocuSign (DOCU), and Etsy (ETSY) especially risky. But then 6% growing GDPs were never what stock market crashes were made of, so any declines will be modest.

As for my own positions, I have a rare 100% long portfolio, mostly Tesla, but also the (TLT), (CAT), (JPM), and (BABA), 80% of which expires with the option expiration on Friday, December 18.

After that, I’ll take it easy with 10% short (TLT) and 10% long (TSLA) and wait for the market, or Georgians to tell me what to do.

A flood of money is to hit the stock market, says hedge fund legend Ray Dalio. The US is facing a perfect storm in favor of all risk assets. There is no reason why price earnings multiples for American stocks can’t reach 50X, double the current 25X. Buy what the central banks are buying. The funny thing is that I agree with Ray on everything. Buy risk on dips.

Stocks will keep soaring into 2021, says JP Morgan strategist Marko Kolanovik. The more risk the better. The Fed will keep interest rates low for at least another year, and ultra-low rates will force big institutions out of bonds and into stocks. Volatility (VIX) will decline. It all sounds like a great long stock/short bond trade to me. Hmmmmm.

Tesla completed a $5 Billion share issue, after a move to $650, up $142 from my November Mad Hedge BUY recommendation. The stock seems hell-bent on testing the Goldman Sachs $780 price recommendation before the December 18 S&P 500 entry. Elon Musk’s creation is now worth a staggering $608 billion. It’s the best recommendation in the 13-year history of the Mad Hedge Fund Trader.

San Francisco rents dive 35%, as tech workers flee to the suburbs. A lot of remote work is now permanent. Studio apartments are now a mere $2,100, and a one-bedroom can be had for $2,716. For a two-bedroom if you have to ask, you don’t need to know. Shocking!

Sales of million-dollar homes are soaring, as ultra-low interest rates persist and people spend much more time at home. So, bigger for your pod is better. Mortgages over $766,000 are up 57% YOY.

Jamie Diamond says he wouldn’t touch bonds with a ten-foot pole, and nor would I. A 91-basis point yield just doesn’t do it for the chairman of JP Morgan Chase (JPM), one of my recurring longs. Stocks are a much better choice, even if there is a bubble in progress. Keep selling every rally in fixed income, especially the (TLT).

Weekly Jobless Claims soar to 853,000, up a massive 153,000 from the previous week. To see this happen during the Christmas hiring season is heartbreaking. With 200,000 a day falling to Covid-19, I’m surprised it's not higher, which means it will be. This is what peaks look like. Washington has totally given up.

An $800 billion payday for the bay area. That is the amount of wealth created by just two companies, Tesla (TSLA) and Airbnb (ABNB), since March. And the great majority of shareholders live in the San Francisco Bay Area, including its venture capital and pension funds. No wonder home prices in the suburbs are up 20% YOY. The great irony is that (ABNB) received a massive government bailout only in March. I hope they repay the loans early.

Is Cuba the next big play? A Biden détente could lead to the emerging market investment opportunity of the decade with the $43 million Herzfeld Caribbean Basin Fund (CUBA). It just had its best month in 11 years (like many of us). With Fidel Castro long dead, what’s the point in continuing a 60-year-old cold war. A big market for American products and services beckons, not to mention the tourism and cruise opportunities. But can Biden afford to lose the Florida Cuban vote in the next election?

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

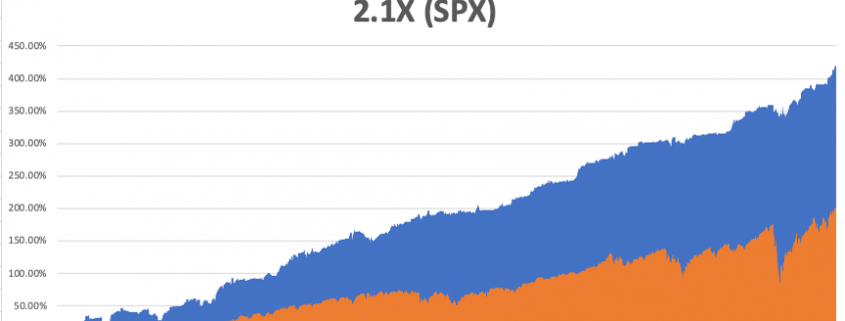

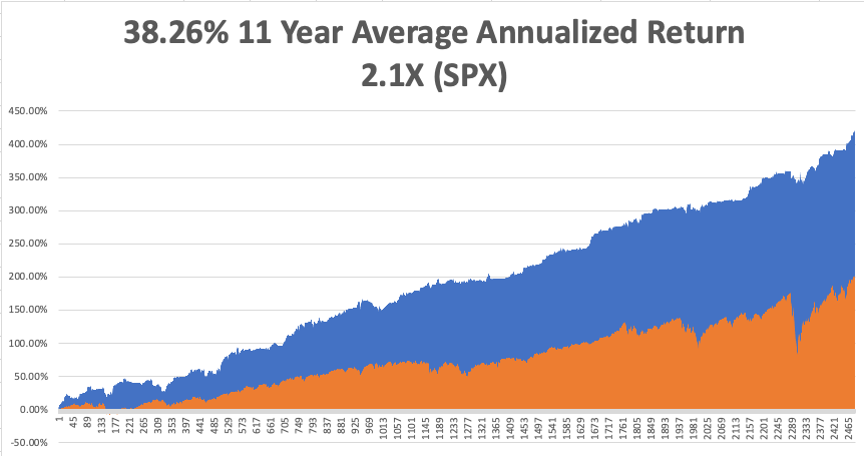

My Global Trading Dispatch catapulted to another new all-time high. December is up 8.55%, taking my 2020 year-to-date up to a new high of 64.99%.

That brings my eleven-year total return to 420.90% or more than double the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.26%. My trailing one-year return exploded to 66.30%, the highest in the 13-year history of the Mad Hedge Fund Trader.

The coming week will be a slow one on the data front. We also need to keep an eye on the number of US Coronavirus cases at 16 million and deaths 300,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, December 14 at 12:00 PM EST, US Consumer Inflation Expectations for November are released.

On Tuesday, December 15 at 11:00 AM, the New York Empire State Manufacturing Index for December are published.

On Wednesday, December 16 at 8:00 AM, US Retail Sales for November are printed.

On Thursday, December 17 at 8:30 AM, the Weekly Jobless Claims are published. We also get November Housing Starts.

On Friday, December 18, at 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I was stunned to learn that 84 million people are watching The Mandalorian, the latest Star Wars installment Disney (DIS) launched in its hugely successful streaming service a year ago.

It reminds me of when I first saw Star Wars in 1977. I was changing planes in Vancouver, Canada on the way to Tokyo and used a long layover to take a taxi to the nearest theater to catch a film I’d heard so much about.

I was amazed when I realized that the guy sitting in the next seat had memorized the entire script and was mouthing all the words. The only other time I have ever seen this happen was sitting on the benches at Shakespeare’s Globe Theater in London. At least then, they were reciting Romeo and Juliet.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

December 10, 2020

Fiat Lux

FEATURED TRADE:

(A STOCK TO SWEETEN YOUR YEAR)

(NVO), (LLY), (MRK), (PFE)

Diabetes is one of the major health issues plaguing the United States, with the CDC reporting that over 34 million people are suffering from this disease – and 20% of them are not even aware of their condition.

More alarmingly, there are at least 88 million individuals that are already in the prediabetic stage.

Since the number of people with diabetes has multiplied in the past 20 years, it presents a massive market for a lot of biotechnology and healthcare companies.

In 2019, the diabetes treatment and drug sector in the US alone recorded a landmark valuation of more than $15 billion and the CDC expects this number to reach $16 billion by 2025.

That’s why it comes as no surprise that more and more companies are attempting to corner the diabetes market.

Since it was founded back in 1876, Eli Lilly (LLY) has been known as the king of the diabetes industry.

However, one competitor has been aggressively working to dethrone Eli Lilly: Novo Nordisk (NVO).

In 2019, NVO’s share in the global diabetes market reached an impressive 29%.

Now, the company aims to boost its share to reach more than 33% by 2025.

Looking at its track record, NVO’s goal of becoming one of the most dominant forces in the diabetes sector is very close to reality.

The company recorded consecutive revenue and net income increases for the past three years.

According to its second quarter report for 2020, NVO reported $4.8 million in revenue. Meanwhile, its net income reached $1.7 billion, representing an 11% boost compared to its performance in the same period last year.

NVO has also seen a promising growth from its newly launched Type 2 diabetes treatments, Ozempic and Rybelsus.

Ozempic alone has been phenomenal, with the drug already reporting $1.1 billion in sales for the first half of 2020 in the US.

This shows off an impressive 156% increase from its record during the same period in 2019 – and the drug has yet to reach its peak.

To put things in perspective, Ozempic recorded $1.7 billion in annual sales last year, a substantial jump from the $264 million it earned when it was launched in 2018.

Rybelsus is another drug expected to take in huge numbers for NVO. The drug has already brought in $64.5 million in revenue in the first six months since its launch in the fourth quarter of 2019.

While all these sound promising, NVO actually has another trick up its sleeve.

The company is planning to sustain its growth by catering to large and well-defined but underserved sectors.

Interestingly, this is similar to the strategy used by Merck (MRK) and Pfizer (PFE) from 1982 to 2000.

At the time, the two healthcare titans decided to cater to the then under-penetrated market of cardiovascular disease.

Initially, the goal was to provide treatments that can abate the risk factors of a heart disease called atherosclerosis. Merck and Pfizer isolated two issues they wanted to address: hypertension and high cholesterol.

Apart from eventually creating drugs specializing in these health issues, Pfizer went on to discover that an ingredient of its products has the sought-after side effect of letting men feel “young” and active once again.

Thus, the best selling Viagra was born.

From the way NVO has been handling its pipeline candidates, a similar result might be well on its way.

For instance, its moneymaker Ozempic is now considered a promising candidate for another underserved market: the progressive liver disease NASH.

Other than that, NVO is also working on listing obesity as a chronic disease. That way, insurers will be required to cover treatment for the condition.

To date, there are 650 million people categorized as obese and only 2% of them are seeking treatment.

Once again, Ozempic will be a stepping stone in this plan.

NVO has been testing the drug’s efficacy on diminishing the patient’s appetite, calling the experimental Ozempic application AM833.

This can gradually transform into a solid revenue source as there are roughly 460 million people suffering from diabetes worldwide, and only 6% of them are in control of their condition.

Basically, NVO is aiming to prevent complications derived from obesity and diabetes.

With such a distinct approach to the growing opportunities, NVO is undoubtedly on its way to building a mega-franchise.

Despite the COVID-19 pandemic wreaking havoc across the globe, NVO is one of the handful of companies with rising earnings expectations this year.

From the previous guidance of $2.72 earnings per share, the company increased it to $2.86 for the rest of the year. Even its 2021 forecast climbed from $3.05 EPS to $3.14.

Overall, this company offers a solid and sustainable revenue stream along with a promising pipeline of candidates with the potential to become mega-blockbusters well beyond the diabetes sector.