Mad Hedge Biotech & Healthcare Letter

May 26, 2020

Fiat Lux

Featured Trade:

(WHY SORRENTO THERAPEUTICS WENT NUTS)

(SRNE), (REGN), (LLY)

Mad Hedge Biotech & Healthcare Letter

May 26, 2020

Fiat Lux

Featured Trade:

(WHY SORRENTO THERAPEUTICS WENT NUTS)

(SRNE), (REGN), (LLY)

Eyes were popping when Sorrento Therapeutics (SRNE) shares went ballistic in mid-May. The price shot up from $2.62 per share to $9.96 in a single day, a gain of 380%. Unfortunately, Sorrento’s climb was halted just as fast when the stock sank 11.5% two days after.

From the look of it, investors eventually sobered up after the initial excitement and realized that the announcement on Sorrento’s pre-clinical results promised too much too soon for a Covid-19 vaccine.

What does this mean for this company?

This rollercoaster situation is par for the course when it comes to small biotechnology companies such as Sorrento, which has a market capitalization of only $1.15 billion.

Extreme volatility is commonplace, with investors getting all riled up the moment a bit of positive news gets out only to balk the moment they fully digest the nitty-gritty of the announcement.

Get used to it. It is a new factor in the market that is roiling prices daily.

Before I discuss Sorrento’s merits and downsides further, here’s a brief background on the good news that got everyone all excited in May.

As you must have guessed by now, the company’s announcement centered on the coronavirus disease (COVID-19).

According to Sorrento, they have hit upon an “exceptionally potent antibody” for this deadly disease. The experimental “cure” is currently dubbed STI-1499.

The breakthrough hit the airwaves after Sorrento’s CEO contacted a Fox News reporter to discuss their discovery, with the executive saying that they have “a solution that works 100%.”

The company is working with Mount Sinai Health System to assess whether STI-1499 can function as a stand-alone therapy as well as a component of an antibody cocktail designed to fight off the SARS-CoV-2 virus, which causes COVID-19.

STI-1499 works by blocking the virus from attaching itself to the body, thereby effectively protecting the cells from infection.

Needless to say, the success of this antibody means big bucks for Sorrento.

It’s critical to bear in mind that results from tests conducted via test tubes and Petri dishes do not guarantee success when applied to human clinical trials -- and this is exactly the problem with Sorrento’s recent results. Cancer has been cured in rates over 100 times.

The STI-1499 trial results were all collected from lab tests. Sorrento has yet to advance to the early-stage clinical study phase. This means that the experimental vaccine is from a slam dunk at this point.

Simply put, STI-1499 has yet to be tested on living things like a mouse and then of course, on humans.

If history is any indication, then Sorrento should be prepared to handle questions about STI-1499’s efficacy. After all, less than 1 in every 5 experimental drugs designed for infectious diseases actually receives FDA approval.

To make things even more challenging for Sorrento, the company isn’t alone in thinking that an antibody regimen could be used against COVID-19.

Prior to this announcement, news has already broken out that Eli Lilly (LLY) and Regeneron Pharmaceuticals (REGN) are also studying similar kinds of approach for this disease.

Beyond its COVID-19 efforts, Sorrento only has one approved product: topical medication ZTlido. This drug, commercially released in 2018, is used to ease the pain brought about by shingles.

Since its launch, ZTlido hasn’t turned out to be a big moneymaker for Sorrento. In the first quarter, this treatment has raked in only $5.2 million in revenue.

Looking at the company’s recent earnings report, it’s clear that Sorrento has been spending more than it’s making so far.

In the first quarter of 2020 alone, the biotechnology company reported $69.2 million in net loss.

Compounding this situation is Sorrento’s fast-depleting cash to fund its operations, with the drugmaker posting a total of $21.9 million in cash and cash equivalents in the year’s first quarter.

Without coming up with more ways to generate additional capital, Sorrento doesn’t have enough bandwidth to keep the lights on any longer much less fund an aggressive coronavirus program.

As for its pipeline, the biotechnology company has two experimental oncology drugs ready for Phase 2 of their clinical trials. Sorrento also has a number of early-stage studies focusing on cancer and pain.

With all these in mind, the question remains: Is Sorrento stock worth buying today?

Although it can be tempting, exhilarating even, to run after a high-flying biotechnology stock plastered all over the news, the wise move would arguably be to restrain yourself and stay on the sidelines -- for now.

If STI-1499 fails in the clinical trials, then all of Sorrento’s gains would be wiped out instantaneously.

What I know so far in terms of the company’s plans to raise more funds is that a public offering might happen soon. If that happens, then the value of the existing Sorrento shares will be diluted.

So if you’re confident to take this gamble of either losing half your money or making it multiple times your initial investment, then this might just be your cup of tea.

However, I can see too many unknown variables for Sorrento to be a compelling stock to buy at the moment.

While Sorrento looks to be offering promising products and is on its way to fueling growth through capital fundraising methods, I have doubts on its ability to cash in big on COVID-19.

One reason is that I find the company’s timing a bit off. On top of that, I’m also not convinced on their capacity to execute particularly in terms of manufacturing.

Most importantly, Sorrento’s is not even considered as the frontrunner in the COVID-19 vaccine race.

I would prefer to wait and see how STI-1499 performs in at least two more stages of clinical trials.

At the very least, these studies would be able to give us a hint at how safe and effective the experimental vaccine is. Right now, I think there are a number of other biotechnology stocks that can provide more reasonable and even attractive risk-reward propositions.

Mad Hedge Biotech & Healthcare Letter

April 28, 2020

Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE)

(GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

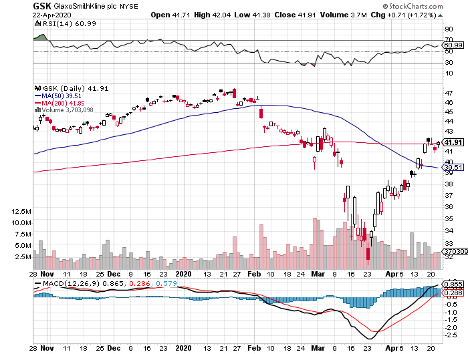

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but take advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.

Mad Hedge Biotech & Healthcare Letter

April 28, 2020

Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE)

(GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but takes advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.

Mad Hedge Biotech & Healthcare Letter

April 23, 2020

Fiat Lux

Featured Trade:

(POST-PANDEMIC STOCKS TO DIVERSIFY YOUR PORTFOLIO)

(BPMC), (NVTA)

Mad Hedge Biotech & Healthcare Letter

April 21, 2020

Fiat Lux

Featured Trade:

(GETTING YOU BANG PER BUCK WITH ALEXION PHARMACEUTICALS)

(ALXN), (GILD), (RHHBY), (REGN), (SNY)

Since nobody can actually control when to get sick or what type of disease to acquire, it makes absolute sense that biotech stocks remain one of the wisest bets if you want to put your hard-earned cash to work.

The question, therefore, is what are the best biotech stocks to buy now?

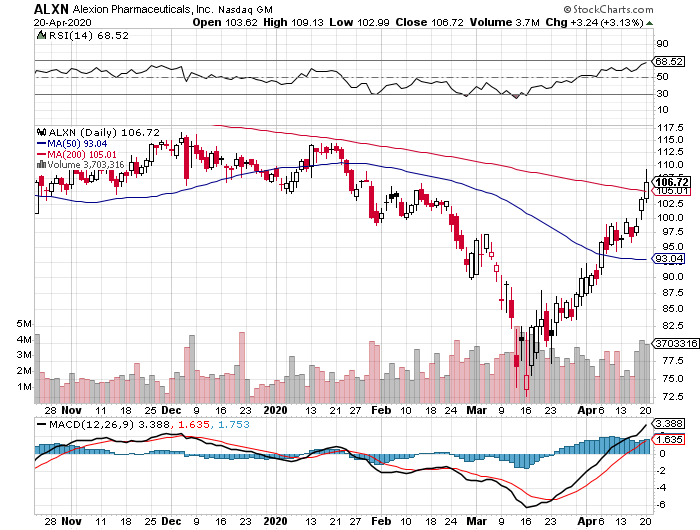

Looking at the biotechnology stock prices today, I can say that Alexion Pharmaceuticals (ALXN) will give you the most bang for your buck.

For over a decade, this ultra-rare-disease biotechnology company had been regularly valued at roughly 22 to 67 times its cash flow and frequently well above 30 times forward EPS.

Now, you can buy this top biotech stock for less than eight times its Wall Street profit consensus in 2021 and 10 times its cash flow for next year as well. It definitely doesn’t hurt that its PEG ratio is less than 1, categorizing it as an “undervalued” stock today.

However, its attractive pricing isn’t the only thing that’s putting Alexion in the news these days as this biotech company has been active in the race to find a coronavirus cure since early February.

When news about the pandemic broke, Alexion decided to repurpose its rare chronic blood disease bestseller Soliris as a potential COVID-19 treatment since the drug showed promising results on patients with severe pneumonia or acute respiratory distress syndrome.

Alexion’s efforts have been quite promising so far, with the biotech company targeting to commence a Phase 2 study of Soliris within the month. What we know so far is that this experiment will involve 10 patients as part of the proof-of-concept trial.

Apart from Alexion, other top biotech companies repurposing old drugs in search of a COVID-19 cure are Gilead Sciences (GILD) with Remdesivir, Roche (RHHBY) with Actemra, and Regeneron (REGN) and Sanofi (SNY) with Kevzara.

Outside its coronavirus treatment efforts, Alexion actually prides itself on a promising pipeline. To date, three treatments are projected to turn into blockbusters soon.

The first is Strensiq, which is formulated to treat a rare disease commonly known as hypophosphatasia. Patients with this disorder have an enzyme deficiency, making them unable to properly process calcium and phosphorus. As a result, they end up with malformed bones and teeth.

The second treatment is Kanuma, which is for patients suffering from lysosomal acid lipase (LAP) deficiency. People with this condition lack a key enzyme, preventing them from effectively breaking down fats.

Both conditions are extremely rare. Hypophosphatasia affects only 1 in 100,000 people while LAP is suffered by 1 in 40,000 individuals.

The third treatment is Ultomiris, which is widely regarded as Soliris’ successor.

For years, Soliris has been Alexion’s major moneymaker. However, uncertainties on the company’s hold on its patent exclusivity have started to shake investors’ faith in this stock. With one of Soliris’ key patents set to expire in 2021, the biotech company has to brace itself for the onslaught of generic competition.

This is where Ultomiris comes in.

Alexion has been busy migrating its customers to opt for Ultomiris before Soliris’ key patent expires.

To make this offer enticing, the biotech company has priced the newer drug to be slightly cheaper than the old blockbuster. Ultomiris costs $458,000 while Soliris is priced at $500,000.

To sweeten the deal further, the newer treatment is only required once every eight weeks. In comparison, Soliris’ treatment schedule is bi-monthly.

Basically, it’s as if Alexion has effectively restarted the clock in its patent exclusivity on this ultra-rare disease indication. The company aims to convert at least 70% of its users by mid-2020.

From a financial point of view, Alexion is performing quite well. Its fourth-quarter report showed that the company earned $1.4 billion in revenues, demonstrating a 23% increase from the same quarter in 2018.

Meanwhile, it raked in $5 billion in full-year sales for 2019. This indicated a 21% jump from its relatively paltry sales of $4.1 billion.

Looking at the metrics, Alexion is one of the surprisingly cheap stocks considering its growth. It also has the added bonus of dominating its chosen ultra-rare disease space.

This is typically a good strategy to avoid competition while also being able to seek high price points for its innovative treatments. The fact that insurers generally cover these treatments all but guarantees that Alexion is secure in terms of cash flow predictability.

Despite the panic induced by the coronavirus market, investing opportunities are everywhere --- if you know where to look.

Alexion is a solid company with strong growth prospects and is selling at a reasonable price. Any opportunistic investor worth his salt would know that this is the ideal time to strike.

Naturally, many people are wondering about which stocks to own in light of the coronavirus. The latest development on the race to find a coronavirus cure is a joint effort involving two giant names from the biotechnology industry: Regeneron Pharmaceuticals (REGN) and Sanofi (SNY).

Taking a page off Gilead Sciences’ (GILD) move to recycle HIV drug Remdisivir and Roche Holding’s (ROG) decision to utilize rheumatoid arthritis Actemra, Sanofi and Regeneron are looking into an existing drug’s ability to offer refuge for patients suffering from COVID-19.

According to a recent announcement, the two companies are looking to test rheumatoid arthritis medication Kevzara on COVID-19 patients.

This drug was initially approved in 2017 and while it failed to reach blockbuster status at the time, Sanofi and Regeneron are preparing to transform it into the next leader in this pandemic race.

It should be noted though that Kevzara is not a coronavirus cure. Rather, the companies are hoping to use this drug to combat the symptoms related to COVID-19.

This is why it’s promising.

When a person gets infected by the novel coronavirus, the immune system is activated and starts attacking the virus to protect the body. As time passes, the immune system goes into overdrive and ends up overreacting, causing additional damage.

Gradually, the immune system starts attacking even the healthy tissue and organs as with the case for some COVID-19 patients.

This means that the coronavirus is causing an accelerated response from the immune system resulting in the patients’ damaged organs starting with the lungs.

This is where Kevzara comes in.

The drug functions as an inhibitor of the protein that triggers the patient’s immune and inflammatory response.

That is, Kevzara can stop the body from attacking itself despite the triggers caused by the coronavirus.

In terms of the specifics of this joint effort, Regeneron will take the lead for the US trials while Sanofi will be in charge of international efforts.

Aside from Kevzara, both Regeneron and Sanofi have been pursuing separate leads on how to deal with the pandemic.

Sanofi has been working in tandem with the US Department of Health and Human Services (HHS), specifically with the Biomedical Advanced Research and Development Authority (BARDA), to come up with a coronavirus vaccine.

However, it’s the coronavirus efforts of Regeneron that gained much attention in the past weeks.

In February, Regeneron and the HHS expanded their partnership to come up with potential COVID-19 treatments. So far, the biotechnology giant has decided to work on monoclonal antibodies via its VelocImmune platform.

This avenue is particularly promising since Regeneron has already come up with an antiviral drug to combat Ebola. Its collaboration with HHS has also already resulted in plans to develop a MERS treatment, which is also a type of coronavirus.

According to Regeneron executives, the company will have a coronavirus treatment ready for human testing by August. If all goes well, then it aims to produce 200K prophylactic doses.

Although its innovative coronavirus proposals are exciting, Regeneron remains focused on its older and more dependable money makers particularly the eye drug Eylea.

This strength is in display in Regeneron’s fourth quarter results, which showed better than expected numbers.

For Eylea alone, the company generated an 11% year-over-year growth in sales.

Despite the emergence of new competitors like Novartis’ (NOVN) Beovu, Regeneron’s eye drug remains the leading product in this sector. In fact, Eylea managed to cross $2 billion in global sales just for the year 2019.

As for inflammation-reducer Dupixent, the treatment’s global sales climbed 136% in 2019.

Meanwhile, revenue from its cancer immunotherapy Libtayo soared to over quintuple from the previous period.

Building from the strength of Eylea, Regeneron also announced its successful late-stage clinical study that aimed to expand the indication of the drug to moderately severe to severe non-proliferative diabetic retinopathy (NPDR).

If this Eylea expansion pushes through, then Regeneron has yet another blockbuster drug in its hands.

In the past five years, Regeneron has demonstrated a strong EPS growth, growing by 23.74% annually. Given its recent performance and based on forward-looking statements, the company can be expected to report an average of 17.4% growth on its EPS in the next two years.

Amid the panic and confusion caused by the coronavirus pandemic, it’s crucial to remain objective, especially with the stock market.

Before making a decision, ask yourself this question: “Will this current situation change the 10-year or even the 20-year outlook for the financial sector?”

Despite the paranoia proliferating in the market in the past months, I believe the answer to this question is still a resounding “no.”

For now, it would be wise to treat owning stocks like how to own businesses. It's important to think about which stocks to own during the coronavirus, but don’t do it just to make a quick buck. Rather, take a look at lasting and stable companies with the capacity to not only grow over the years but also to compound their returns.

Mad Hedge Biotech & Healthcare Letter

December 12, 2019

Fiat Lux

Featured Trade:

(THE STAMPEDE INTO BIOSIMILAR DRUGS),

(BIIB), (NOVN), (REGN), (ALXN), (NITE), (PFE), (AMGN), (MRK)