Mad Hedge Biotech and Healthcare Letter

September 3, 2024

Fiat Lux

Featured Trade:

(ROLLING THE DICE ON BIOTECH)

(RHHBY), (VNDA), (ZVRA), (HALO), (BMY), (GILD)

Mad Hedge Biotech and Healthcare Letter

September 3, 2024

Fiat Lux

Featured Trade:

(ROLLING THE DICE ON BIOTECH)

(RHHBY), (VNDA), (ZVRA), (HALO), (BMY), (GILD)

Remember when you'd jump into a hot tub and the water was just right? That's what the biotech sector feels like right now - it's warming up and ready for a splash.

After years of treading water, biotech stocks are showing signs of life. High interest rates and cash crunches have kept this sector on the sidelines, but the game is changing.

September 2024 is shaping up to be a blockbuster month for the sector, with FDA decisions that could send stocks soaring - or sinking.

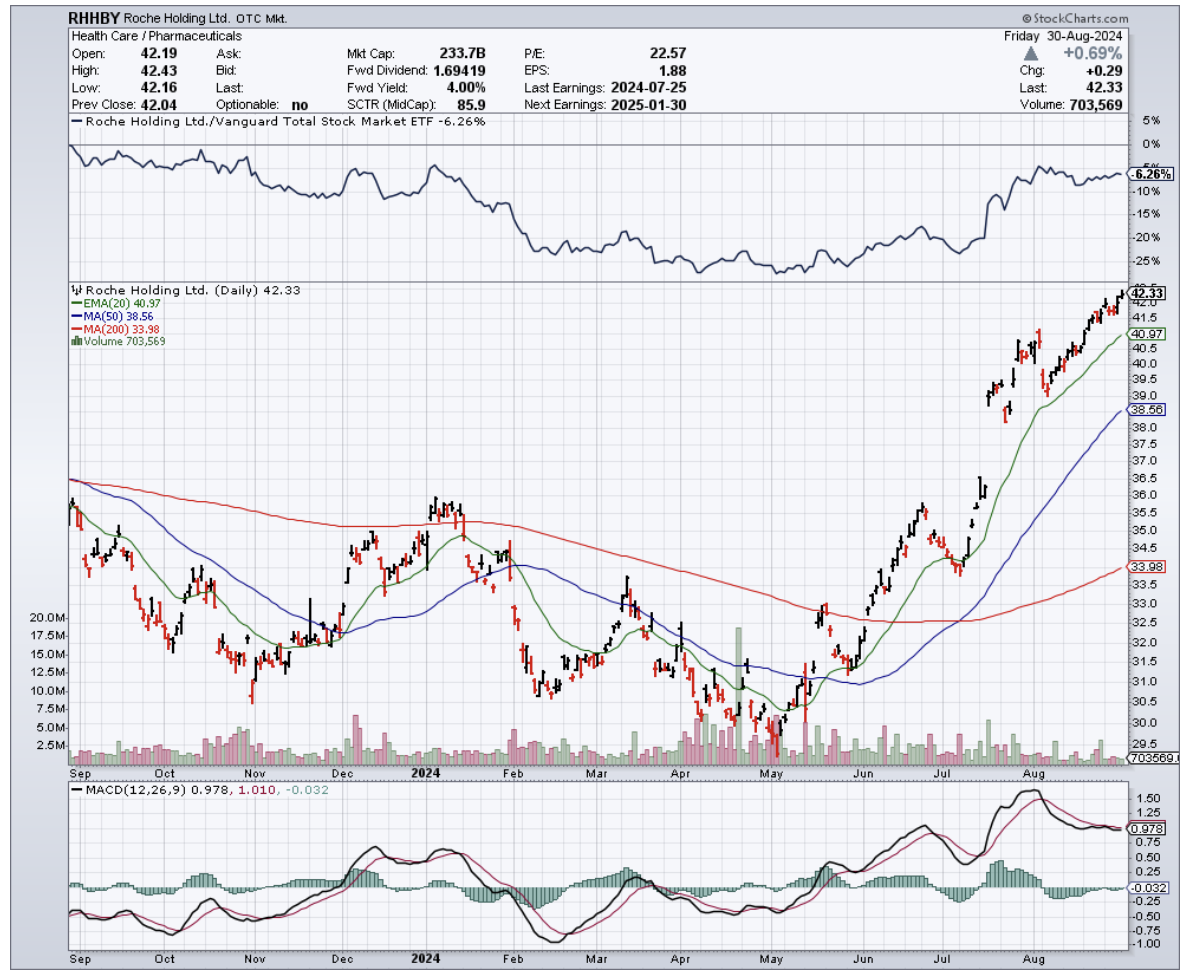

First up, Roche Holding AG (RHHBY) is waiting on pins and needles for the FDA's verdict on Ocrevus SC. This isn't just another drug - it's a new way to deliver their multiple sclerosis cash cow.

If the FDA gives the green light on September 13, Roche could be looking at a bigger slice of the MS pie. Why? Because this new version doesn't need fancy IV setups, opening doors to treatment centers that were previously off-limits.

But Roche isn't the only one with butterflies in its stomach.

Vanda Pharmaceuticals (VNDA) is hoping to make history on September 18 with Tradipitant. This drug aims to tackle gastroparesis, a condition that's been stuck in treatment limbo for four decades. If Tradipitant gets the nod, Vanda could find itself as the big fish in a very lucrative pond.

And let's not forget about the underdogs.

Zevra Therapeutics (ZVRA) is crossing its fingers for Arimoclomol. This potential game-changer targets Niemann-Pick disease type C, a rare brain disorder that's been waiting for its medical knight in shining armor. September 21 could be that day.

These approvals aren't just good news for the companies involved. They're like a shot of adrenaline for the whole biotech sector. Investors love nothing more than seeing potential turn into profit.

But it's not all about solo acts in biotech. These days, it's all about partnerships.

Take Halozyme Therapeutics (HALO), for instance. They've buddied up with Roche to develop Ocrevus SC, bringing their ENHANZE technology to the party.

These kinds of collaborations are golddust for smaller biotech firms. They get access to resources and markets they could only dream of on their own, making them much more attractive to investors with deep pockets.

Speaking of deep pockets, big pharma companies are on the prowl, and several biotech firms are looking mighty tasty.

Bristol-Myers Squibb (BMY) just showed us how it's done by snatching up Karuna Therapeutics. Why? Two words: KarXT.

This antipsychotic drug is currently under FDA review for schizophrenia, and if approved, it could be another lucrative revenue stream. This kind of deal is a win-win. The big fish gets new toys for its pipeline, and the smaller fish gets a cushy new home.

Now, let's talk about the elephant in the room - interest rates.

Biotech companies and high interest rates go together like oil and water. These firms need cash like plants need water, and high rates make that cash harder to come by.

But here's the thing: the Federal Reserve is hinting at rate cuts.

For biotech, that's like Christmas coming early. Lower rates mean easier borrowing and easier borrowing means more research, more trials, and potentially more breakthroughs.

So if rates drop, don't be surprised to see biotech stocks shoot up faster than a rocket.

But it's not just about drugs in the pipeline. The biotech sector is also home to some serious innovation.

Take gene editing and CRISPR. This isn't your grandpa's genetics - it's like we've found the “track changes” function for DNA.

The market for this molecular magic is set to explode from $4 billion in 2024 to a whopping $17.8 billion by 2034. That's a 16.1% annual growth rate, for those of you keeping score at home.

With this technology, I’m not just talking about curing rare diseases here. I’m talking about the possibility of having your own home testing kits that could make your 23andMe results look like a fortune cookie.

And then there’s personalized medicine, which is turning healthcare into a bespoke tailor shop. Your DNA is becoming the blueprint for your treatments, and the market is following suit.

We're looking at a jump from $300 billion in 2021 to $869.5 billion by 2031. Why the boom? Well, sequencing your DNA used to cost more than a mansion.

Now it's cheaper than a decent night out in New York - from over $1 million in 2007 to about $600 today.

Stem cells and regenerative medicine are also getting investors hot under the collar. We're talking about potentially regrowing organs or giving Parkinson's the boot.

This market is set to grow at a spicy 9.74% annually from 2023 to 2030. Basically, it’s like we're entering the age of biological LEGO.

And let's not forget AI - the new brainiac in the lab. It's turning drug discovery into a high-speed chess game, with the AI market in healthcare expected to hit $95.65 billion by 2028.

With the innovations from this tech, scientists could have supercomputers as their lab partners – ones that never need coffee breaks and can crunch data faster than you can say "blockbuster drug."

Given all these possibilities, I think it’s a good time to talk about strategy. After all, investing in biotech isn't one-size-fits-all. It's more like a buffet - you pick what suits your taste and risk appetite.

For the adrenaline junkies who like to walk the tightrope without a net, there's the high-risk, growth investor approach. These brave souls get their kicks from cutting-edge stuff like gene editing and personalized medicine, often diving into early-stage biotech firms working on the next big breakthrough.

It's not for the faint of heart - these stocks can swing wilder than a monkey on espresso. But when they hit, oh boy, do they hit.

Just look at the personalized medicine market - it's set to explode from $300 billion in 2021 to a mind-boggling $869.5 billion by 2031. That's the kind of growth that could make your portfolio do backflips, assuming you can stomach the ride.

On the other side of the petri dish, we've got the value and low-risk investors. These are the steady hands who prefer their biotech stocks aged like fine wine and served with a side of sleep-easy. They're eyeing established companies with robust pipelines, diverse portfolios of approved drugs, and ongoing trials.

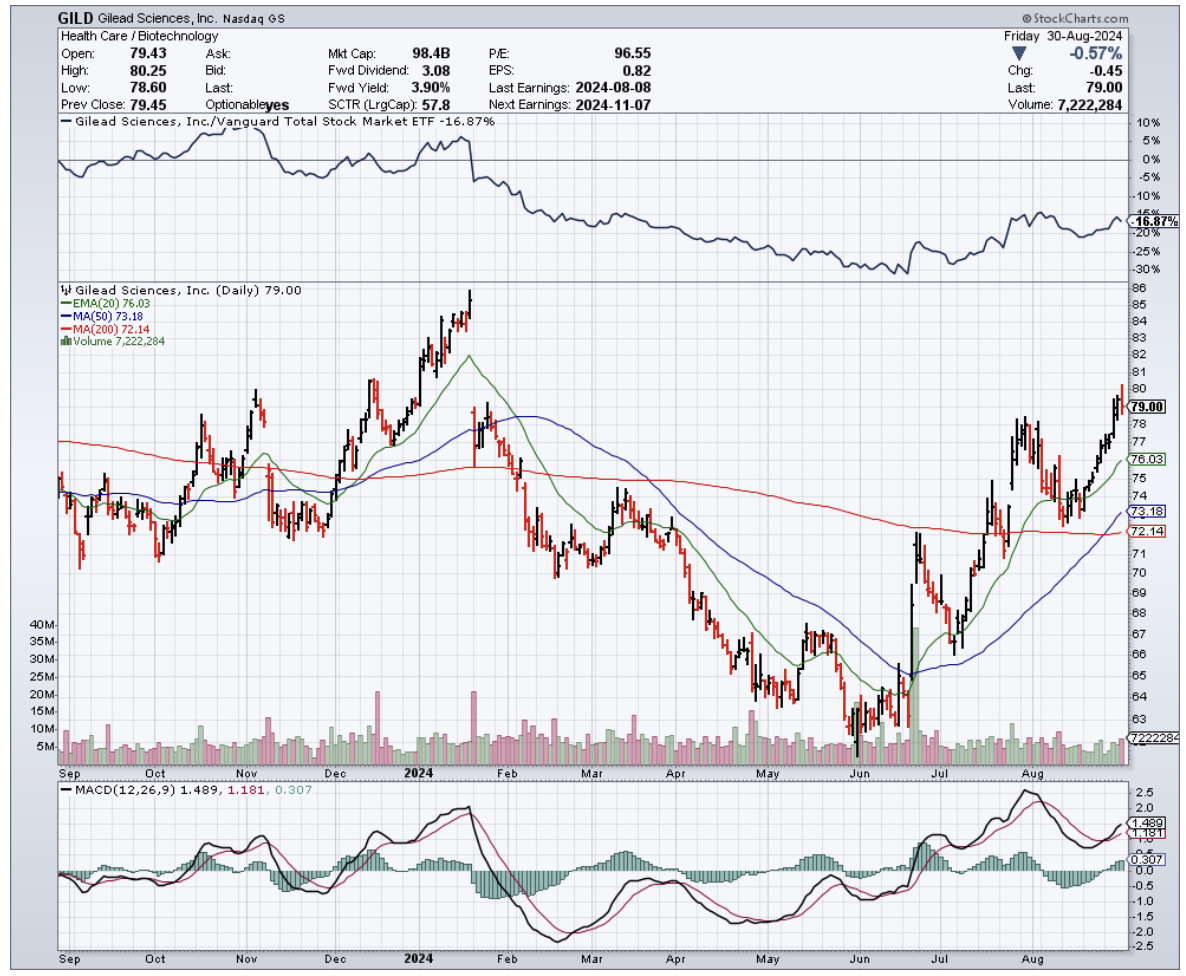

Think Roche with its Ocrevus SC, or old guards like Gilead Sciences (GILD) that have weathered more storms than a lighthouse.

These investors are the tortoises in the biotech race - slow and steady, but with a knack for crossing the finish line, often with a healthy dividend check in hand. They might not make headlines, but they're more likely to let you sleep soundly while your portfolio does the heavy lifting.

No matter which style you choose, one thing is undeniable: the biotech sector is like a sleeping giant, and it's starting to stir. The question is, will you heed the wake-up call or sleep through the alarm?

Mad Hedge Biotech and Healthcare Letter

August 29, 2024

Fiat Lux

Featured Trade:

(ONE TEST TO RULE THEM ALL)

(ILMN), (BAYRY), (LLY), (MRK), (BMY), (AZN), (RHHBY), (NVS), (GH), (TEM), (TMO)

“One test to rule them all, one test to find them, one test to bring them all, and in the lab bind them,” the scientists at Illumina (ILMN) whispered – probably.

Their latest creation just got the FDA nod, and it's set to turn the world of cancer diagnostics on its head. It's as if Gandalf himself handed oncologists a palantír that reveals tumors' deepest secrets.

For those less versed in Middle-earth lore, this is like inventing a universal remote for tumor profiling, and oncologists can't wait to start channel surfing.

Now, you might be thinking, "What's the big deal?" Well, let me break it down for you.

This test, called TruSight Oncology Comprehensive (TSO for short), is the first FDA-approved genomic in vitro diagnostic kit that can make pan-cancer companion diagnostic claims.

In plain English, that means it's a single test that can be used across multiple cancer types. We're talking about a game-changer in precision oncology here.

Let's get into the nitty-gritty. This TSO test is a beast. It screens for a whopping 517 genes and provides comprehensive information on tumor mutational burden (TMB) and microsatellite instability (MSI).

These are crucial biomarkers that help determine how a patient might respond to immunotherapies. The breadth of data this single FDA-approved test can collect is unprecedented.

Now, you might be wondering, "Haven't we had companion diagnostics before?" Sure, but they've typically been limited to specific drugs or cancer types.

This pan-cancer test from Illumina is different. It can be applied to a wider range of solid tumors, and let me tell you, oncologists are loving it.

In fact, about 39% of U.S. oncologists have already said they strongly prefer using multi-gene panels over single-gene tests for guiding treatment decisions. That's a clear signal that there's demand for comprehensive diagnostic solutions like TSO.

Illumina's been busy across the pond, too. A version of this test has been available in Europe since 2022. But the U.S. version's got some new tricks up its sleeve.

It can help identify patients who might benefit from specific immunotherapies, including Bayer's (BAYRY) Vitrakvi and Eli Lilly's (LLY) Retevmo. The latter is a new addition compared to the EU version of the test.

Let's talk about these therapies for a second. Vitrakvi is used for adult and pediatric patients with certain NTRK mutations, regardless of their type of cancer. That's pretty cool, right?

But here's the kicker - these NTRK gene fusions are only found in about 0.1% to 0.3% of solid tumors, and they're tough to detect.

TSO's ability to scan both RNA and DNA means it can find multiple forms of this biomarker. That's a big deal for companies like Bayer, who've sometimes struggled to find eligible patients for this targeted therapy.

But Illumina's not resting on its laurels. They've got a growing pipeline of companion diagnostic claims in development, working hand in hand with drugmakers. They're planning to seek these in future regulatory submissions.

You see, Illumina's been playing the long game, forging partnerships with big pharma to co-develop companion diagnostics that align with targeted therapies.

Take their 2019 partnership with Merck (MRK), for instance. They teamed up to develop and commercialize a companion diagnostic using Illumina's TruSight Oncology 500 assay.

The goal? To identify genetic mutations in cancer patients that would respond to Merck's cancer drugs like Keytruda. This partnership boosted the adoption of Illumina's NGS platform in clinical oncology settings, contributing to both companies' growth.

The market liked what it saw at the time. Illumina's stock got a nice bump following the partnership announcement. And why wouldn't it?

The deal strengthened Illumina's position in the oncology diagnostics market, which is projected to grow at a CAGR of 12.4% from 2023 to 2030.

But Merck's not the only dance partner Illumina's got. They've also teamed up with Bristol-Myers Squibb (BMY) to use their TSO 500 assay as a companion diagnostic for immuno-oncology therapies.

This collaboration expanded Illumina's reach into new oncology applications, allowing BMY to use the TSO platform to identify patients most likely to benefit from its immune checkpoint inhibitors.

And there's more - Illumina's also forged partnerships with AstraZeneca (AZN), Roche (RHHBY), and Novartis (NVS) to develop companion diagnostic tests.

Next, let's talk numbers. Each new FDA-approved indication could potentially add $100 million to $200 million annually to Illumina's revenue. That's no chump change.

Unsurprisingly, Illumina's not the only player in this game.

Companies like Foundation Medicine (a Roche subsidiary), Guardant Health (GH), Tempus (TEM), Caris Life Sciences, Thermo Fisher Scientific (TMO), and GRAIL (another Illumina subsidiary) are all working towards pan-cancer or multi-cancer diagnostics.

Still, Illumina's TSO test is the first to secure FDA approval for pan-cancer companion diagnostic claims. This lead could translate into a significant market advantage.

Actually, Illumina already holds more than 70% market share in the global NGS market as of 2022. This means it’s well-positioned to benefit from this growth, and this latest FDA approval could further consolidate its market dominance.

Speaking of the FDA, they’ve been busy too. They've ramped up their support for precision medicine in recent years, approving a growing number of companion diagnostics and genomic tests.

From 2017 to 2021, they approved over 25 new companion diagnostics, a significant increase from the 5-10 approvals per year in the early 2010s. And a substantial portion of these approvals has been for oncology-related tests.

In 2021 alone, 68% of the FDA's new drug approvals were for cancer treatments.

Now, let's zoom out and look at the bigger picture. According to the World Health Organization, there were an estimated 19.3 million new cancer cases and 10 million cancer deaths worldwide in 2020.

The global cancer burden is expected to rise to 28.4 million cases by 2040, a 47% increase from 2020.

In the U.S., about 1.9 million new cancer cases are expected to be diagnosed in 2023.

The economic impact is also staggering. The economic burden of cancer in the U.S. was estimated at $157 billion in 2020, and it's projected to increase to over $246 billion by 2030.

These numbers stress the growing need for early detection and personalized treatment solutions.

But, unlike other companies, here's where advanced diagnostics like Illumina's TSO can make a difference. By ensuring patients receive the most effective treatments based on their genetic profiles, these tests can reduce unnecessary treatments and improve outcomes.

Studies have shown that using precision diagnostics can lower overall healthcare costs by 15% to 20% by avoiding ineffective therapies and hospitalizations.

Essentially, what we're seeing here is more than just a new test. It's a glimpse into the future of cancer treatment - more precise, more personalized, and potentially more effective.

For patients, it could mean better outcomes. For healthcare systems, it could mean more efficient use of resources. And for us? Well, it could mean significant opportunities in a rapidly growing market.

As Gandalf might say, "All we have to decide is what to do with the time that is given us." Illumina's chosen to use their time crafting this powerful new tool.

The quest to conquer cancer continues, and Illumina’s TSO might just be the ring-bearer we've been waiting for.

Keep your eyes peeled, fellow adventurers. The journey into precision oncology is only just beginning, and it promises to be an epic saga indeed.

Mad Hedge Biotech and Healthcare Letter

August 22, 2024

Fiat Lux

Featured Trade:

(BITING OFF MORE THAN THEY CAN CHEW)

(LLY), (NVO), (CTLT), (ZLDPF), (RHHBY), (AMGN), (PFE), (LZAGY), (TMO)

"If you build it, they will come." But what happens when they come before you've finished building?

That's the billion-dollar question facing the makers of GLP-1 weight loss drugs.

GLP-1 drugs, the newest darlings of the pharmaceutical world, are selling like hotcakes. Eli Lilly (LLY) and Novo Nordisk (NVO), the current heavyweights in this arena, raked in a whopping $10.4 billion and $6.85 billion respectively last year.

Basically, the demand is there, but the supply? Well, that's another story.

So far, Lilly and Novo have been throwing money at the problem like it's going out of style. We're talking billions here. Novo's earmarked $6.5 billion for production this year alone, while Lilly's already shelled out $5.3 billion to beef up its manufacturing muscle. They're expanding facilities faster than you can say "miracle weight loss drug."

But even that's not enough. Lilly admits the industry needs at least 10 to 15 dedicated sites to even come close to meeting demand.

It's like trying to serve a five-course meal to a packed restaurant with just one chef and a microwave.

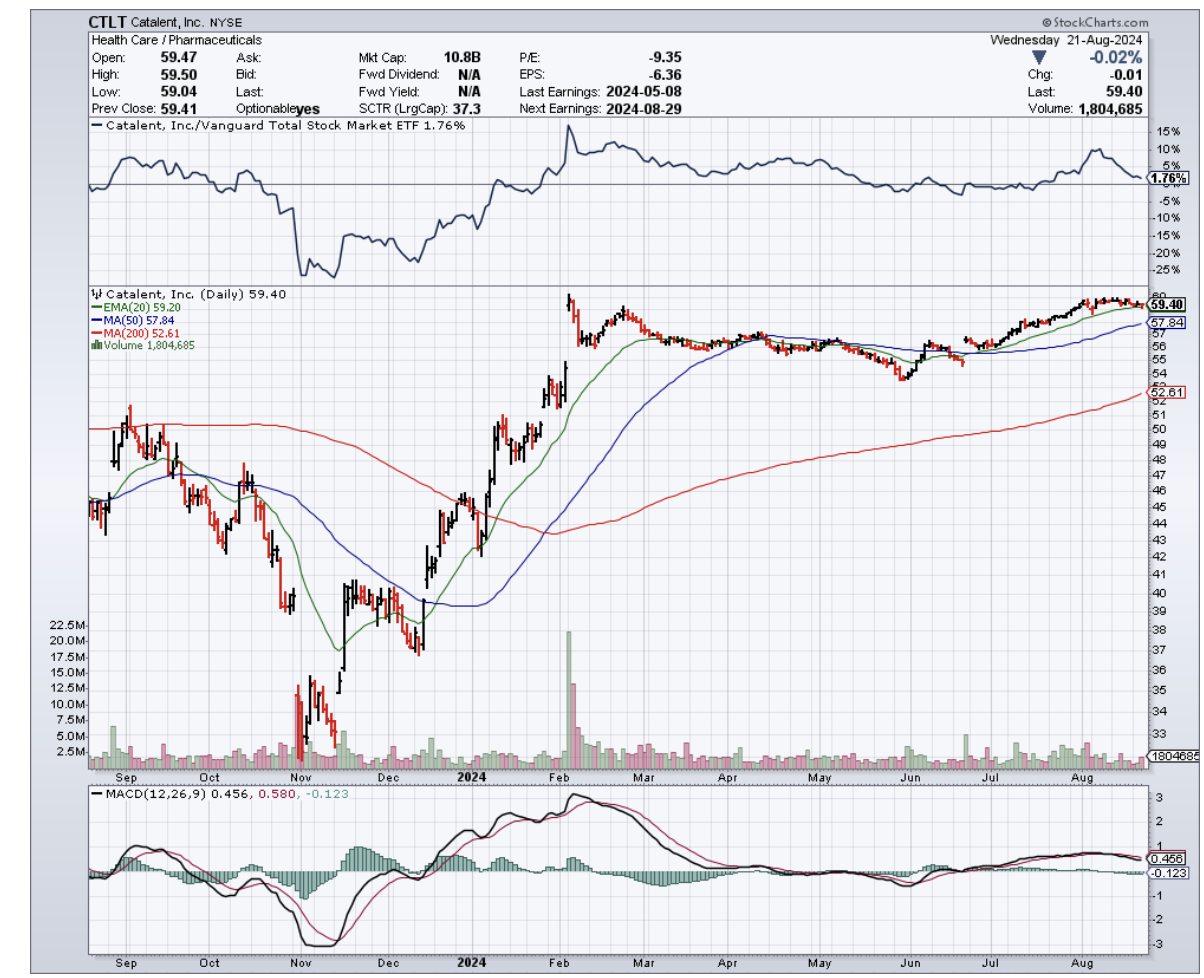

And let's not forget about the price tag on these manufacturing sites. Novo just dropped $11 billion to buy three fill-finish sites from Catalent (CTLT). Talk about paying a premium for prime real estate.

While Lilly and Novo scramble to ramp up production, their manufacturing woes have created a window of opportunity for competitors eyeing a slice of the GLP-1 pie.

Boehringer Ingelheim and Zealand Pharma (ZLDPF) are closest to market with their Phase 3 drug survodutide.

Meanwhile, Roche (RHHBY) and Amgen (AMGN) aren't far behind in Phase 2. Even Pfizer's (PFE) dipping its toes in the water with an early-stage drug.

But here's where it gets interesting for us who want a piece of the action. These newcomers are facing a manufacturing dilemma of their own.

Do they build their own facilities and risk being late to the party? Or do they outsource and potentially lose control over production?

Some, like Boehringer and Roche, are already talking about using third-party manufacturers. It's like hiring a catering company instead of building your own restaurant – less upfront cost, but you're at the mercy of someone else's kitchen.

Enter the contract manufacturing organizations (CMOs), the unsung heroes of the pharmaceutical world who might just hold the key to unlocking the full potential of the GLP-1 market.

Let’s take a look at the big players in this space.

Lonza Group (LZAGY), with its $6.6 billion in annual revenue and 10% market share in biologics contract manufacturing, is a force to be reckoned with. They're not just sitting on their laurels either – they're pumping $850 million into a new biologics facility in Switzerland.

Then there's Thermo Fisher Scientific (TMO), the 800-pound gorilla of the industry. With a cool $44.9 billion in revenue last year and an 8% to 10% market share in contract manufacturing, they're a go-to partner for big pharma.

They've been on a shopping spree too, scooping up Pharmaceutical Product Development (PPD) for $17.4 billion to boost their manufacturing capabilities.

And, of course, let's not forget about Catalent. They might have sold some facilities to Novo, but they're still a major player with $4.8 billion in revenue last year. They're betting big on biologics, with plans to increase capacity by 40% by 2025.

As for those looking for growth potential, keep an eye on Samsung Biologics. They're the new kid on the block, with a 30% compound annual growth rate over the past five years and the world's largest single-site biologics manufacturing facility.

So, there you have it. The obesity epidemic is a tragedy, but it's also a trillion-dollar opportunity.

With half the population projected to be obese by 2030, this isn't just a health crisis—it's a financial frontier.

The GLP-1 market is poised to balloon to $130 billion, creating a feeding frenzy for those ready to capitalize on the supply squeeze.

But here's the real meat of the matter: in this gold rush, it's not just the drug developers who are striking it rich. The real winners are the manufacturers—those with the capacity to meet the insatiable demand. They're the ones handing out the "shovels" in this weight loss bonanza.

So while everyone else is focused on the flashy GLP-1 drugs, I suggest you also keep a watchful eye on these behind-the-scenes players.

Now, if you'll excuse me, I'm off to patent my groundbreaking idea: GLP-1-infused kale chips. Who says you can't have your cake and eat it too?

Mad Hedge Biotech and Healthcare Letter

August 15, 2024

Fiat Lux

Featured Trade:

(THE INCREDIBLE BULK)

(LLY), (NVO), (RHHBY), (AMGN), (PFE), (VKTX)

Mad Hedge Biotech and Healthcare Letter

July 25, 2024

Fiat Lux

Featured Trade:

(REVERSING THE FOG)

(SAVA), (ESALF), (BIIB), (LLY), (RHHBY), (ACIU), (AVXL), (ATHA)

Close your eyes and think back to your favorite childhood memory. Maybe it's the smell of your grandma's apple pie wafting through the kitchen, or the sound of your grandpa's belly laugh as he tickled you mercilessly.

Now imagine those memories being ripped away, one by one, until all that's left is a hollow shell of the person you once knew and loved.

That's the heartbreaking reality of Alzheimer's disease, and it's a fate that Rick Barry, the newly minted executive chairman of Cassava Sciences (SAVA), is determined to change.

You see, Barry isn't just some suit looking to make a quick buck. No, sir. This man's got skin in the game, and a personal connection to the fight against Alzheimer's that'll tug at your heartstrings.

His decision to join Cassava's board back in June 2021 was driven by a gut-wrenching story about his buddy's father, Buddy. This once-vibrant Navy fighter pilot and commercial airline captain was reduced to a shell of his former self by the cruel hand of Alzheimer's.

And folks, this ain't an isolated case. We're talking about 6.9 million Americans aged 65 and older living with this wretched disease in 2024, with that number set to double in the next 30 years.

Globally, over 55 million people are grappling with dementia, and Alzheimer's is the big, bad culprit in 60-70% of those cases.

While the situation is admittedly grim, Cassava Sciences offers a glimmer of hope: simufilam.

This experimental drug is Cassava's secret weapon, designed to whip a rogue protein called filamin A back into shape.

When filamin A goes off the rails in Alzheimer's patients, it wreaks havoc on brain function. But simufilam, like a disciplined drill sergeant, could get this unruly protein back in line, normalize cellular processes, reduce inflammation, and give synaptic function a much-needed boost.

Now, I know you're probably skeptical, but the Phase 2 trial results were nothing to sneeze at. A whopping 47% of patients saw their cognitive function improve, and the biomarkers of neurodegeneration and inflammation took a nosedive.

But the real moment of truth lies ahead in the Phase 3 trials, RETHINK-ALZ and REFOCUS-ALZ. These trials are the big leagues, with nearly 2,000 participants and top-line results expected by the end of 2024.

If simufilam can prove its mettle, it could be a game-changer for millions of Alzheimer's patients who are desperate for a breakthrough.

Of course, Cassava Sciences isn't the only horse in this race. The heavyweight contenders like Eisai (ESALF), Biogen (BIIB), Eli Lilly (LLY), Roche (RHHBY), and AbbVie (ABBV) are all jockeying for position, while smaller outfits like AC Immune (ACIU), Anavex (AVXL), and Athira Pharma (ATHA) are making some intriguing moves of their own.

But what really sets Cassava apart is the fire in their belly. When Barry says, "If you create great benefit for your patients, you'll create great value for your shareholders," you can tell he means business. This isn't just about lining pockets – it's about making a real difference in people's lives.

And let me tell you, the impact of Alzheimer's is staggering. Over 11 million Americans are providing unpaid care for their loved ones with Alzheimer's or other forms of dementia.

In 2023 alone, these unsung heroes clocked in a mind-boggling 18.4 billion hours of care, valued at a cool $350 billion.

And to make things worse, 70% of these caregivers are stressed to the max trying to coordinate care, while 66% are struggling to find resources and support. On top of that, 74% are also worried sick about their own health.

Financially, Alzheimer's is a beast that just keeps growing. In 2023, it drained $345 billion from the nation's coffers.

Fast forward to 2024, and that price tag is expected to hit $360 billion. And brace yourselves, because by 2050, we could be staring down the barrel of a $1 trillion problem.

So, is Cassava Sciences stock a slam-dunk investment? Well, that depends on your appetite for risk.

In the biotech world, the stakes are high, and the outcomes are never guaranteed. Simufilam's fate rests squarely on the results of those pivotal Phase 3 trials.

But one thing I can say with certainty is that Cassava Sciences has got guts. They're the underdog taking on Alzheimer's, armed with a potentially groundbreaking treatment and a whole lot of heart.

In a world where roughly 1 in 9 people over 65 are living with Alzheimer's, the impact of a successful therapy would be nothing short of seismic.

As investors, it's easy to get caught up in the cold, hard numbers. But sometimes, it pays to step back and consider the human element.

Behind every stock symbol, there are countless families praying for a miracle, tireless researchers burning the midnight oil, and brave souls like Rick Barry putting their money where their mouth is.

So, while I can't tell you to go all-in on Cassava Sciences just yet, I can tell you this: they're fighting the good fight. And in a world that often seems like it's gone completely off the rails, that's something worth getting behind. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

July 2, 2024

Fiat Lux

Featured Trade:

(TWO-STEPPING TO A CANCER CURE)

(GILD), (AZN), (RHHBY), (PFE), (MRK)