I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on February 2, 2021. In fact, not only did we nail the best sectors to go heavily overweight, we also completely dodged the bullets in the worst-performing ones.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing and you don’t want to remain glued to a screen all day, these are the investments you can make. Then don’t touch them until you start drawing down your retirement funds at age 72.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted in red on the spreadsheet.

To download the entire new portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com, log in, go “My Account”, then “Global Trading Dispatch”, the click on the “Long Term Portfolio” button, then “Download.”

Changes

Biotech

Pfizer (PFE) has nearly doubled in six months, while Crisper Therapeutics (CRSP) has almost halved. Since the pandemic, which Pfizer made fortunes on, is peaking and we are still at the dawn of the CRISPR gene editing revolution, the natural switch here is to take profits in (PFE) and double up on (CRSP).

Technology

I am maintaining my 20% in technology which are all close to all-time highs. I believe that Apple (AAPL), (Amazon (AMZN), Google (GOOGL), and Square (SQ) have a double or more over the next three years, so I am keeping all of them.

Banks

I am also keeping my weighting in banks at 20%. Interest rates are imminently going to rise, with a Fed taper just over the horizon, setting up a perfect storm in favor of bank earnings. Loan default rates are falling. Banks are overcapitalized, thanks to Dodd-Frank. And because of the trillions in government stimulus loans they are disbursing, they are now the most subsidized sector of the economy. So, keep Morgan Stanley (MS), Goldman Sachs (GS), JP Morgan (JPM), and Bank of America, which will profit enormously from a continuing bull market in stocks. They are also a key part of my” barbell” portfolio.

International

China has been a disaster this year, with Alibaba (BABA) dropping by half, while emerging markets (EEM) have gone nowhere. I am keeping my positions because it makes no sense to sell down here. There is a limit to how much the Middle Kingdom will destroy its technology crown jewels. Emerging markets are a call option on a global synchronized recovery which will take place next year.

Bonds

Along the same vein, I am keeping 10% of my portfolio in a short position in the United States Treasury Bond Fund (TLT) as I think bonds are about to go to hell in a handbasket. I rant on this sector on an almost daily basis so go read Global Trading Dispatch. Eventually, massive over-issuance of bonds by the US government will destroy this entire sector.

Foreign Exchange

I am also keeping my foreign currency exposure unchanged, maintaining a double long in the Australian dollar (FXA). Eventually, the US dollar will become toast and could be your next decade-long trade. The Aussie will be the best performing currency against the US dollar.

Australia will be a leveraged beneficiary of the synchronized global economic recovery through strong commodity prices which have already started to rise, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

Precious Metals

As for precious metals, I’m keeping my 0% holding in gold (GLD). From here, it is having trouble keeping up with other alternative assets, like Bitcoin, and there are better fish to fry.

I am keeping a 5% weighting in the higher beta and more volatile iShares Silver Trust (SLV), which has far wider industrial uses in solar panels and electric vehicles. The arithmetic is simple. EV production will rocket from 700,000 in 2020 to 25 million in 2030 and each one needs two ounces of silver.

Energy

As for energy, I will keep my weighting at zero. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free. You are looking at the next buggy whip industry.

The Economy

My ten-year assumption for the US and the global economy remains the same. I’m looking at 3%-5% a year growth for the next decade after this year’s superheated 7% performance.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 700% or more from 35,000 to 240,000 in the coming decade. The American coming out the other side of the pandemic will be far more efficient, productive, and profitable than the old.

You won’t believe what’s coming your way!

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again. If I forget, please remind me.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-19 10:02:182021-08-19 12:09:09My Newly Updated Long-Term Portfolio

Below please find subscribers’ Q&A for the August 11Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA.

Q: If we see a correction in stocks, what would you do?

A: Buy more stocks (SPY). All of our positions expire next week, and we go 100% into cash. I’m looking for just a 5% correction and then I’m just going to go piling in 100% invested with a barbell portfolio since everything is working now and some of the best tech stocks like Amazon have already had 10% corrections.

Q: Time for LEAPS again on Amazon (AMZN)?

A: Yes, but let Amazon have more time to bottom out. It may just be a “time” correction where it goes sideways for a month or two. The company is still growing at an incredible rate.

Q: What about FedEx (FDX) and Walt Disney (DIS) LEAPS?

A: Those LEAPS I would do, right here, right now. We’ve had our corrections already in those sectors and they’re ready to take off. It’s just a matter of time before these sectors come back into favor. These are both delta peaking plays.

Q: It seems that the US government is taking the stance that they can tax their way out of the fiscal hole; is this true?

A: No, they don’t need to tax their way out of the fiscal hole; deflation will wipe out all US government debt on a 30-year view, and this is what’s happened to not only all the government debt in US history but all government debts all over the world starting with France in the 1600s. By the time the government has to pay back its 30-year bonds, the purchasing power of that dollar will have fallen by 80% or 90%, meaning that essentially the bonds get deflated away to nothing. And this is why we have governments, so they can borrow that money now, spend it now to rescue the economy, and then they never have to pay it back in real dollars. This is why governments borrow. The investors who really have to pick up the bill for this are bond owners, who see the purchasing power of the bonds decline by 2%-3% a year.

Q: When do you see a correction, and what would you do?

A: It’s either going to be in the next couple of weeks or never. If we get one, I would load the boat again with more long positions. Of the five positions out of 100 I’ve lost money this year, four have been short positions, so you can see why we’re really trying to limit the short positions here.

Q: Visa (V) is going ex-dividend tomorrow—is there a risk of early assignment?

A: There is, but if you get an early assignment, just say thank you very much, Mr. Market, call your broker to tell them to exercise your long call position to cover your call short position, and you will get the maximum profit several days earlier than expiration. This happens sometimes as hedge funds try to get the quarterly dividend on the cheap, but you have to act fast, otherwise, you’ll end up with a short position in Visa on your hands, and most likely a margin call. Brokers are not allowed to automatically exercise longs to meet calls anymore. You have to call them and order them to exercise that long. So, pay attention going into quarterly option expirations.

Q: I don’t trust your COVID information any more than I trust the government line.

A: All of my Covid data comes from Johns Hopkins University and is interdependently collated from every country in the United States. If you have any complaints you can go to them. All I can say is there are 620,000 bodies in the country that died of something. Oh, and we had the lowest population growth last month in 50 years. I’ve had family members die from it so I believe that.

Q: If the Republicans win in 2022 and 2024, will the bull market continue?

A: Absolutely not. We get a new recession and another bear market. Everything that’s going well now reverses, the entire environmental infrastructure strategy goes down the toilet, and Covid makes a huge recovery. I would go with what’s working, and 6.5% economic growth now and a market going up 30% a year totally works for me. Of course, I would make another fortune on the short side.

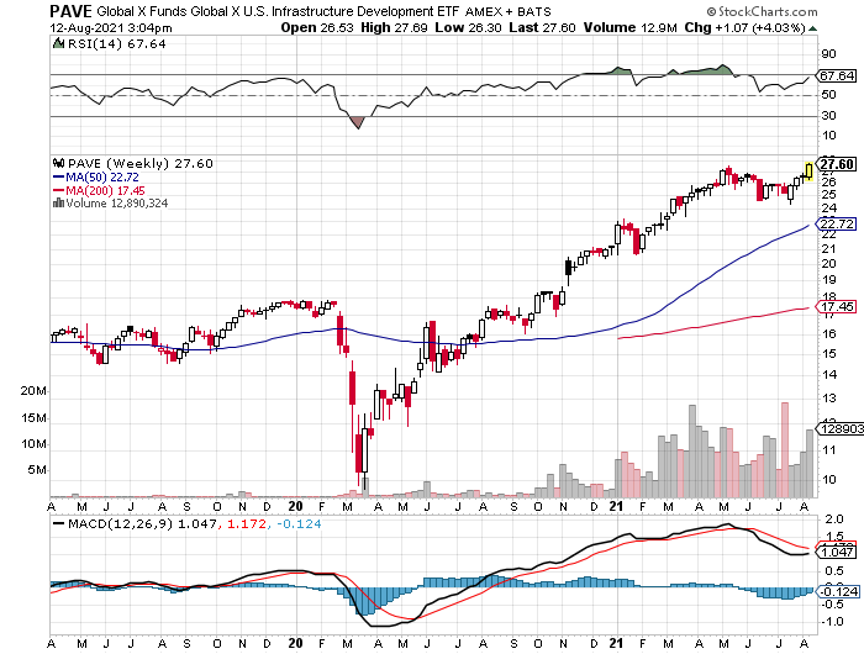

Q: How should you play infrastructure?

A: There is an infrastructure ETF called the Global X Funds Infrastructure ETF (PAVE) that has already had a big move, up 176% in 17 months. Other than that you can just play your basic commodity stocks like US Steel (X), Nucor (NUE), and Freeport McMoRan (FCX).

Q: How long will the hot housing market continue?

A: Ten more years. That's how long it will take to digest the current 85 million strong millennial generation who are now buying first-time homes or upgrading what they’ve got. And remember, we’re still operating with half of the new home construction capacity that we had 15 years ago before the last financial crisis.

Q: What's your prognosis for semiconductors?

A: They just had a super-heated spike; I expect them to take a break. That's why I took profits on Advanced Micro Devices (AMD). We’ll find a new bottom, and then I want to buy back into it. It’s taking a break with the rest of technology right now, which is perfectly normal.

Q: Would you take this dip to add to mRNA and BioNTech?

A: I would say yes. This is an industry that’s on the eve of a biotech revolution—the cure of all human diseases. And these two companies with their mRNA technologies are in the best place to take advantage of that.

Q: Will there be a big spike down in August?

A: It looks like it’s not happening. Like I said, if it doesn’t happen in the next few weeks, it’s not going to happen. Excess liquidity is just driving all investment decisions. If it doesn’t go down now, what’s the reason for it to go down in October? I just see no negatives at all on the horizon except for another out-of-the-blue variant like a Lambda or an Epsilon variant.

Q: Does slow population growth include illegal immigration?

A: It does, immigration both legal and illegal has been constant for decades and decades, it’s about a million people a year. But Americans are not reproducing like they used to, the birth rate hit a 50-year low last year because women did not want to go to the hospitals which were full of COVID patients. A lower population growth over the long term is very bad for economic growth. That is why Japan has essentially been in a nonstop recession for the last 32 years, because of their baby bust.

Q: Do you have political debt ceiling concerns?

A: No, these are always last-minute before midnight deals. I don't see this being any different, never underestimate the ability of Congress to spend more money, no matter who is in power.

Q: What do you think of oil in the short run?

A: Short term it may go sideways, we may even have a rally to new highs, but the long-term trade for oil is that it’s going out of business. EVs, mean you lose 50% of demand for oil in the next 10 years, and they will start discounting that now in the price of oil.

Q: Why is silver down so much?

A: It’s being dragged down by Gold (GLD), and silver (SLV) always moves twice as fast as gold.

Q: How are muni bonds going forward?

A: I don’t see them going much further. They had a massive rally, discounting an increase in taxes which hasn’t happened. So even if they do raise taxes which may be next year’s business, that is fully discounted in the Muni market already.

Q: What am I missing? You’ve been saying for months not to get involved with Bitcoin but then I heard you say you bought LEAPS.

A: No, I didn’t buy the LEAPS. I tried to buy the LEAPS but missed them and it ran away and they ended up tripling in two weeks. It’s just not like buying a normal stock. Once these things turn, they just start going up every day for weeks with no pullbacks whatsoever. This is valuation-free security with no dividend, interest, or earnings. It’s driven by pure supply and demand.

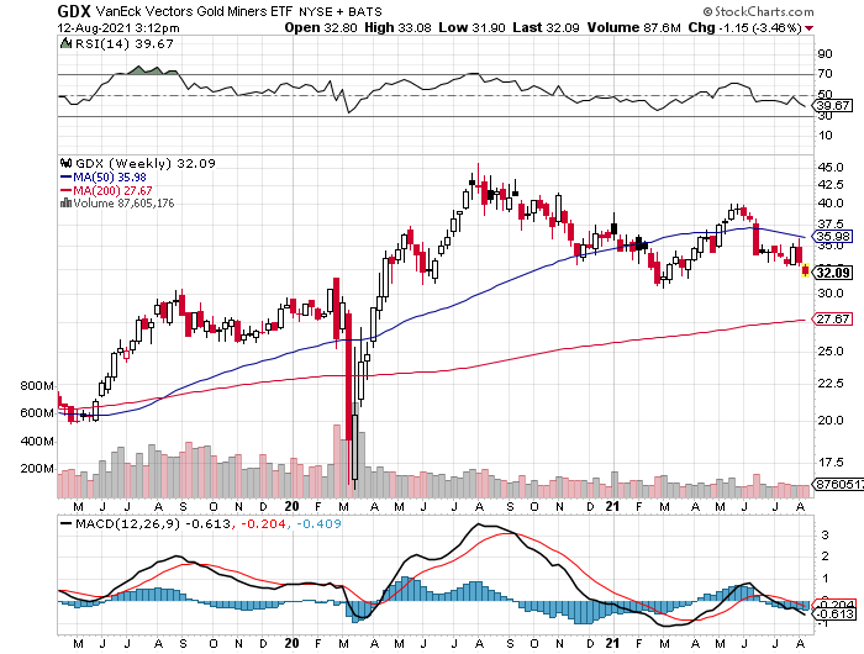

Q: What do you think of the precious metal miners like the Van Eck Vectors Gold Miners ETF (GDX)?

A: Let the current meltdown burn out and then go into long term LEAPS.

Q: What’s the best way to buy silver?

A: The best way is doing 2-year LEAPS on Wheaton Precious Metals (WPM) at current levels.

Q: What do you think about Coinbase (COIN)?

A: It’s definitely a candidate, but you want to get it on a down day. Coinbase is in the “selling shovels to the gold miners” business which is always a fantastic business model and we here in California know all about it. It’s just a question of when and where to get involved. It’s been gyrating this week because of their new burden of doing the tax reporting on all crypto buyers among their customers. That will definitely be a drag on the business.

Q: What's your short-term view on the big commodity plays like Freeport McMoRan (FCX), Alcoa Aluminum (AA), and US Steel (X)?

A: I would say they’re all going up. Maybe half the infrastructure bill has been discounted into the metals prices, but not all of it, therefore they have more to go to the upside.

Q: What are the best real estate buys?

A: There are none anywhere; maybe somewhere in eastern Europe, but still unlikely. It’s the best time ever now to rent. Buying here would be madness. And by the way, I predicted this property boom 10 years ago, if you go back in my research because 2021 was when the millennials would show up as massive buyers in the housing market, right when there was going to be a demographic shortage. That’s why I think the real estate boom goes on for another 10 years. But you won't see the gains that we’ve seen this year. You will maybe see 5% or 10% gains a year, definitely not 50% or 100% gains that we’ve just seen.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in here, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-thomas-wine.png538374Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-13 09:02:332021-08-13 10:17:50August 11 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the March 31 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Would you buy Facebook (FB) or Zoom (ZM) right here?

A: Well, Zoom was kind of a one-hit wonder; it went up 12 times on the pandemic as we moved to a Zoom economy, and while Zoom will permanently remain a part of our life, you’re not going to get that kind of growth in stock prices in the future. Facebook on the other hand is going to new highs, they just announced they’re laying a new fiber optic cable to Asia to handle a 70% increase in traffic there. So, for the longer term and buying here, I think you get a new high on Facebook soon; there's maybe another 20-30% move in Facebook this year.

Q: I can’t really chase these trades here, right?

A: Correct; if you wait any more than a day or 2 on executing a trade alert, you’re missing out on all of the market timing value we bring to the game. So that's why I include an entry price and the “don’t pay more than” price. And we never like to chase, except last year, when we did it almost all the time. But last year was a chase market, this year not so much.

Q: How are LEAP purchase notifications transmitted?

A: Those go out in the daily newsletter Global Trading Dispatch when I see a rare entry point for a LEAP, then we’ll send out a piece and notify everybody. But it’s very unusual to get those. Of course, a year ago we were sending out lists of LEAPS ten at a time when the Dow Average ($INDU) is at 18,000. But that is not now, you only wait for those once or twice a year. On huge selloffs to get into two-year-long options trades, and that is definitely not now. The only other place I've been looking out for LEAPS right now are really bombed out technology stocks begging for a rotation. Concierge members get more input on LEAPS and that is a $10,000 a year upgrade.

Q: What are your thoughts on silver (SLV) and long-term gold (GLD)?

A: I see silver going to $50 and eventually $100 in this economic cycle, but it's out of favor right now because of rising interest rates. So, once we hit 2.00% in the ten years, it’s not only off to the races for tech but also gold and silver. Watch that carefully because your entry point may be on the horizon. That makes Wheaton Precious Metals (WPM) a very attractive “BUY” right now.

Q: Are you going to trade the (TLT)?

A: Absolutely yes, but I’m kind of getting picky now that I’m up 42% on the year; and I only like to sell 5-point rallies, which we got for about 15 minutes last week. And I also only like to buy 5- or 10-point dips. Keep your trading discipline and you’ll make a ton of money in this market. Last year we made about 30% trading bonds on about 30 round trips.

Q: How much further upside is there for US Steel (X) and Nucor Corp. (NUE)?

A: More. There's no way you do infrastructure without using millions of tons of steel. And I kind of missed the bottom on US Steel because it had been a short for so long that it kind of dropped off the radar for me. I think we have gone from $4 to 27 since last year, but I think it goes higher. It turns out the US has been shutting down steel production for decades because it couldn't compete with China or Japan, and now all of a sudden, we need steel, and we don’t even make the right kind of steel to build bridges or subways anymore—that has to be imported. So, most of the steel industry here now is working for the car industry, which produces cold-rolled steel for the car body panels. Even that disappears fairly soon as that gets taken over by carbon fiber. So enough about steel, buy the dips on (X) and (NUE).

Q: What stocks should I consider for the infrastructure project?

A: Well, US Steel (X) and Nucor Corp (NUE) would be good choices; but really you can buy anything because the infrastructure package, the way it’s been designed, is to benefit the entire economy, not just the bridge and freeway part of it. Some of it is for charging stations and electric car subsidies. Other parts are for rural broadband, which is great for chip stocks. There is even money to cap abandoned oil wells to rope in Texas supporters. All of this is going to require a massive upgrade of the power grid, which will generate lots of blue-collar jobs. Really everybody benefits, which is how they get it through Congress. No Congressperson will want to vote against a new bridge or freeway for their district. That’s always the case in Washington, which is why it will take several months to get this through congress because so many thousands of deals need to be cut. I’ve been in Washington when they’ve done these things, and the amount of horse-trading that goes on is incredible.

Q: Is it a good thing that I’ve had the United States Treasury Bond Fund (TLT) LEAPS $125 puts for a long time.

A: Yes. Good for you, you read my research. Remember, the (TLT) low in this economic cycle is probably around $80, so you probably want to keep rolling forward your position….and double up on any ten-point rally.

Q: Do you think we get a pop back up?

A: We do but from a lower level. I think any rallies in the bond market are going to be extremely limited until we hit the 2.00%, and then you’re going to get an absolute rip-your-face-off rally to clean out all the short term shorts. If you're running put LEAPS on the (TLT) I would hang on, it’s going to pay off big time eventually.

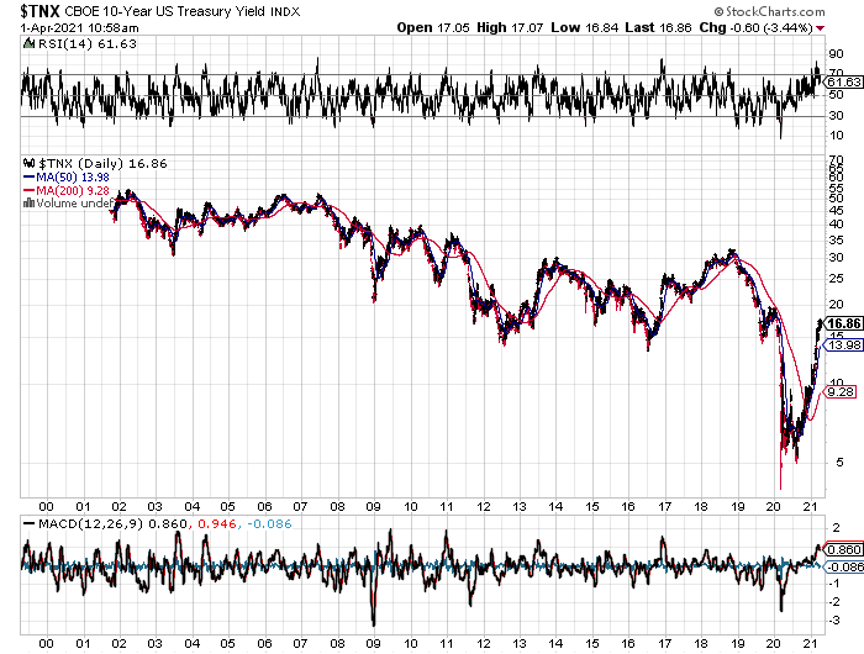

Q: If we see 3.00% on the 10-year this year, do you see the stock market crashing?

A: I don’t think we’ll hit 3.00% until well into next year, but when we do, that will be time for a good 10% stock market correction. Then everyone will look around again and say, “wow nothing happened,” and that will take the market to new highs again; that's usually the way it plays out. Remember, then year yields topped all the way up at 5.00% when the Dotcom Bubble topped in April 2020.

Q: Has the airline hospitality industry already priced in the reopening of travel?

A: No, I think they priced in the hope of a reopening, but that hasn’t actually happened yet, and on these giant recovery plays there are two legs: the “hope for it” leg, which has already happened, and then the actual “happening” leg which is still ahead of us. There you can get another double in these stocks. When they actually reopen international travel to Europe and Asia, which may not happen this year, the only reopening we’re going to see in the airline business is in North America. That means there is more to go in the stock price. Also coming back from the brink of death on their financial reports will be an additional positive.

Q: Do you think a corporate tax increase will drive companies out of the US again and raise the unemployment rate?

A: Absolutely not. First of all, more than half of the S&P 500 don’t even pay taxes, so they’re not going anywhere. Second, I think they will make these offshoring moves to tax-free domiciles like Ireland illegal and bring a lot of tax revenues back to the US. And third, all Biden is doing is returning the tax rate to where it was in 2017; and while the corporate tax rate was 35%, the stock market went up 400% during the Obama administration, if you recall. So stocks aren't really that sensitive to their tax rates, at least not in the last 50 years that I’ve been watching. I'm not worried at all. And Biden was up on the polls a year ago talking about a 28% tax rate; and since then, the stock market has nearly doubled. The word has been out for a year and priced in for a year, and I don't think anybody cares.

Q: What about quantum computers?

A: I’m following this very closely, it’s the next major generation for technology. Quantum computers will allow a trillion-fold improvement in computing power at zero cost. And when there's a stock play, I will do it; but unfortunately, it’s not (IBM), because we’re not at the money-making stage on these yet. We are still at the deep research stage. The big beneficiaries now are Alphabet (GOOGL), Microsoft (MSFT), and Amazon (AMZN).

Q: Is it time to buy Chinese stocks?

A: I would say yes. I would start dipping in here, especially on the quality names like Tencent (TME), Baidu (BIDU), and Alibaba (BABA), because they’ve just been trashed. A lot of the selloff was hedge fund-driven which has now gone bust, and I think relations with China improve under Biden.

Q: Your timing on Tesla (TSLA) has been impeccable; what do you look for in times of pivots?

A: Tesla trades like no other stock, I have actually lost money on a couple of Tesla trades. You have to wait for things to go to extremes, and then wait two more days. That seems to be the magic formula. On the first big selloff go take a long nap and when you wake up, the temptation to buy it will have gone away. It always goes up higher than you expect, and down lower than you expect. But because the implied volatilities go anywhere from 70% to 100%, you can go like 200 points out of the money on a 3-week view and still make good money every month. And that’s exactly what we’re going to do for the rest of the year, as long as the trading’s down here in the $500-$600 range.

Q: Is Editas Medicine (EDIT), a DNA editing stock, still good?

A: Buy both (EDIT) and Crisper (CRSP); they both look great down here with an easy double ahead. This is a great long-term investment play with gene editing about to dominate the medical field. If you want to learn more about (EDIT) and (CRSP) and many others like them, subscribe to the Mad Hedge Fund Biotech & HealthcareLetter because we cover this stuff multiple times a week (click here).

Q: Is the XME Metals ETF a buy?

A: I would say yes, but I'd wait for a bigger dip. It’s already gone up like 10X in a year, but the outlook for the economy looks fantastic. (XME) has to double from here just to get to the old 2008 high and we have A LOT more stimulus this time around.

Q: What about hydrogen?

A: Sorry, I am just not a believer in hydrogen. You have to find someone else to be bullish on hydrogen because it’s not me. I've been following the technology for 50 years and all I can say is: go do an image Google for the name “Hindenburg” and tell me if you want to buy hydrogen. Electricity is exponentially scalable, but Hydrogen is analog and has to be moved around in trucks that can tip over and blow up at any time. Hydrogen batteries are nowhere near economic. We are now on the eve of solid-state lithium-ion batteries which improve battery densities 20X, dropping Tesla battery weights from 1,200 points to 60 pounds. So “NO” on hydrogen. Am I clear?

Q: Why do you do deep-in-the-money call and put spreads?

A: We do these because they make money whether the stock goes up down or sideways, we can do them on a monthly basis, we can do them on volatility spikes, and make double the money you normally do. The day-to-day volatility on these positions is very low, so people following a newsletter don’t get these huge selloffs and sell at bottoms, which is the number one source of retail investor losses. After 13 years of trade alerts, I have delivered a 40.30% average annualized return with a quarter of the market volatility. Most people will take that.

Q: Is ProShares Ultra Short 20 Year Plus Treasury ETF(TBT) still a play for the intermediate term?

A: I would say yes. If ten-year US Treasury bonds Yields soar from 1.75% to 5.00% the (TBT) should rise from $21 to $100 because it is a 2X short on bonds. That sounds like a win for me, as long as you can take short term pain.

Q: What is the timing to buy TLT LEAPS?

A: The answer was in January when we were in the $155-162 range for the (TLT). Down here I would be reluctant to do LEAPS on the TLT because we’ve already had a $25 point drop this year, and a drop of $48 from $180 high in a year. So LEAP territory was a year ago but now I wouldn’t be going for giant leveraged trades. That train has left the station. That ship has sailed. And I can’t think of a third Metaphone for being too late.

Q: Would you buy Kinder Morgan (KMI) here?

A: That’s an oil exploration infrastructure company. No, all the oil plays were a year ago, and even six months ago you could have bought them. But remember, in oil you’re assuming you can get in and out before it crashes again, it’s just a matter of time before it does. I can do that but most of you probably can’t, unless you sit in front of your screens all day. You’re betting against the long-term trend. It works if you’re a hedge fund trader, not so much if you are a long-term investor. Never bet against the long-term trend and you always have a tailwind behind you. All surprises work to your benefit.

Q: If you get a head and shoulders top on bitcoin, how far does it fall?

A: How about zero? 80% is the traditional selloff amount for Bitcoin. So, the thing is: if bitcoin falls you have to worry about all other investments that have attracted speculative interest, which is essentially everything these days. You also have to worry about Square (SQ), PayPal (PYPL), and Tesla (TSLA), which have started processing Bitcoin transactions. Bitcoin risk is spread all over the economy right now. Those who rode the bandwagon up will ride it back down.

Q: Is Boeing (BA) a long-term buy?

A: Yes, especially because the 737 Max is back up in the air and China is back in the market as a huge buyer of U.S. products after a four-year vacation. Airlines are on the verge of seeing a huge plane shortage.

Q: What about Ags?

A: We quit covering years ago because they’re in permanent long-term downtrends and very hard to play. US farmers are just too good at their jobs. Efficiencies have double or tripled in 60 years. Ag prices are in a secular 150-year bear market thanks to technology.

Q: Is this recorded to watch later?

A: Yes, it goes on our website in about two hours. For directions on where to find it, log in to your www.madhedgefundrader.com account, go to “My Account,” and it will be listed under there, as are all the recorded webinars of the last 12 years.

Q: Would you buy Canadian Pacific (CP) here, the railroad?

A: No, that news is in the price. Go buy the other ones—Union Pacific (UNP) especially.

Q: What are your thoughts on Bitcoin?

A: We don’t cover Bitcoin because I think the whole thing is a Ponzi scheme, but who am I to say. There is almost ten times more research and newsletters out there on Bitcoin as there is on stock trading right now. They seem to be growing like mushrooms after a spring storm. There are always a lot of exports out there at market tops, as we saw with gold in 2010 and tech stock in 2000.

Q: What do you think about Juniper Networks (JNP)?

A: It’s a Screaming “BUY” right here with a double ahead of it in two years. I’m just waiting for the tech rotation to get going. This is a long-term accumulate on dips and selloffs.

Q: Did the Archagos Investments hedge fund blow threaten systemic risk?

A: No, it seems to be limited just to this one hedge fund and just to the people who lent to it. You can bet banks are paring back lending to the hedge fund industry like crazy right now to protect their earnings. I don’t think it gets to the systemic point, but this is the Long Term Capital Management for our generation. I was involved in the unwind of the last LTCM capital, which was 23 years ago. I was one of the handful of people who understood what these people were even doing. So, they had to bring me in on the unwind and huge fortunes were made on that blowup by a lot of different parties, one of which was Goldman Sachs (GS). I can tell you now that the statute of limitations has run out and now that it's unlikely I'll ever get a job there, but Goldman made a killing on long-term capital, for sure.

Q: Will Tesla benefit from the Biden infrastructure plan?

A: I would say Tesla is at the top of the list of companies the Biden administration wants to encourage. That means more charging stations and more roads, which you need to drive cars on, and bridges, and more tax subsidies for purchases of new electric cars. It’s good not just Tesla but everybody’s, now that GM (GM) and Ford (F) are finally starting to gear up big numbers of EVs of their own. By the way, I don't see any of the new startups ever posing a threat to Tesla. The only possible threats would be General Motors, Ford, and Volkswagen, which are all ten years behind.

Q: Would you put 10% of your retirement fund into cryptocurrencies?

A: Better to flush it down the toilet because there’s no commission on doing that.

Q: Is growing debt a threat to the economy? How much more can the government borrow?

A: It appears a lot more, because Biden has already indicated he’s going to spend ten trillion dollars this year, and the bond market is at a 1.70%—it’s incredibly low. I think as long as the Fed keeps overnight rates at near-zero and inflation doesn't go over 3%, that the amount the government can borrow is essentially unlimited, so why stop at $10 or $20 trillion? They will keep borrowing and keep stimulating until they see actual inflation, and I don’t think we will see that for years because inflation is being wiped out by technology improvements, as it has done for the last 40 years. The market is certainly saying we can borrow a lot more with no serious impact on the economy. But how much more nobody knows because we are in uncharted territory, or terra incognita.

To watch a replay of this webinar just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/12/john-thomas-lakeshore-e1608229033313.png338450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-01 11:02:522021-04-01 14:14:23March 31 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the March 3 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Are SPACs here to stay?

A: Yes, but I think that in the next bear market, 80% of these SPACs (Special Purpose Acquisition Companies) will disappear, will deliver large losses, and will continue charging you enormous fees until then. It’s either that or they won’t invest their money at all and give it back, net of the fees. So, I’m avoiding the SPAC craze unless it's associated with a very specific investment play that I know well. The problem with SPACs is that they all come out expensive—there are no bargain basement SPACs on launch day. Me, being the eternal cheapskate that I am, always want to get a great bargain on everything. The time to buy these is actually in the next bear market, if they still exist, because then investors will be throwing their positions away at 10 or 20% discounts. That’s always what happens with specialized ETF, closed-end funds, and so on. They are roach motel investments; you can check-in, but you can never check out.

Q: What do you think of Elizabeth Warren's asset tax idea?

A: It’s idiotic. It would take years to figure out how much Jeff Bezos is worth. And even then, you probably couldn't come within ten billion dollars of a true number. We already pay asset taxes, our local county real estate taxes, and those are bad enough, delivering valuations that are miles from true market prices. There are many other ways to fix the tax system and get billionaires paying their fair share. There are only three things you really have to do: get rid of carried interest so hedge funds can’t operate tax-free, get rid of real estate loss carry forwards which allow the real estate industry to basically operate tax-free, and get rid of the oil depletion allowance, which has enabled the oil industry to operate tax-free for nearly 90 years. So those would be three easy ones to increase the fairness of the tax system without any immense restructuring of our accounting system.

Q: When will share buybacks start?

A: They’ve already started and have been happening all year. There are two ways the companies do this: they either have an outside accounting firm, buying religiously every day or at the end of every month or something like that, so they can’t be accused of insider trading; or they are in there buying on every dip. Certainly, all the big cash-heavy companies like Berkshire Hathaway (BRKB) or Apple (AAPL) were buying their shares like crazy last March and April because they were trading such enormous discounts. So that is another trillion dollars sitting under the market, waiting to come in on any dip, which is yet another reason that we are not going to see any major sell-offs this year—just the 5%-10% variety that I have been predicting.

Q: Is it time to buy Salesforce (CRM)?

A: Yes, Marc Benioff’s goal is to double sales in two years, and the stock is relatively cheap right now because they’ve had a couple of weak quarters and are still digesting some big acquisitions.

Q: Is CRISPR Therapeutics (CRSP) good buy?

A: Yes, I would be buying right here; it’s a good LEAP candidate because the stock could easily double from here. We’ve only scratched the surface on CRISPR technology being adopted and the potential growth in this company is enormous—I'm surprised they haven’t been taken over already.

Q: Will you start a letter for investing advisors on how to deal with the prolific numbers of Bitcoin?

A: There are already too many Bitcoin newsletters; there are literally hundreds of them and thousands of experts on Bitcoin now because there’s nothing to know and nothing to analyze. It’s all a belief system; there are no earnings, there are no dividends, and there is no interest. So, you purely have to invest in the belief that somebody else is going to take you out at a higher price. I think there is a big overhang of selling in that when they raise the number of Bitcoin, we’ll get another one of those 90% crashes that Bitcoin is prone to. So, go elsewhere for your Bitcoin advice; your choices are essentially unlimited now, and they are much cheaper than me. In fact, people are literally giving away Bitcoin advice for free, which means you’re getting what you’re paying for. I buy Bitcoin when they have a customer support telephone number.

Q: Zoom (ZM) has come down a lot after a big earnings report—do you like it?

A: Long term, yes. Short term, no. You want to avoid all the stay-at-home stocks because no one is staying at home anymore. However, there is a long-term story in Zoom once they find their bottom because even after we come out of the pandemic, we’re all still using Zoom. I have like five or ten Zoom meetings a day, and my kids go to school on Zoom all day long. They’re also bringing out new products like telephone servers. They’re also raising their prices—I happen to be one of Zoom’s largest customers. I’m paying $1,100/month now, and that’s rising at 10% a year.

Q: What would be the best LEAP for Salesforce (CRM)?

A: The rule of thumb is that you want to go 30% out of the money on your first strike. So, find a current stock price; your first strike is up 30%, and then your second strike is up 35%. And all you need to double your money on that is a bounce back to the highs for this year, which is not unrealistic. That’s the lay-up there with Salesforce. That’s the basic formula; Advanced Micro Devices (AMD), Walt Disney (DIS), Berkshire Hathaway (BRKB), Palantir (PLTR), and Nvidia (NVDA) are all good candidates for LEAPS.

Q: How often do you update the long-term stock portfolio?

A: Twice a year, and we just updated in January, which is posted on the website in your membership area. If you can't find it, just email customer support at support@madhedgefundtrader.com and they’ll tell you where to find it. And we only do this twice a year because there just aren't enough changes in the economy in six months to justify a more frequent update.

Q: When do you think real estate will come back?

A: It never left. We’ve had the hottest real estate market in history, with 20% annual gains in many cities in 2020. And that will continue, but not at the 20% rate, probably at a more sustainable 5% or 6% rate. Guess what the best inflation play in the world is? Real estate. If you’re worried about inflation, you want to run out and buy a house or two. The only thing that will really kill that market is a rise in 30-year fixed-rate mortgages to 5%, and that is years off. Or a rise in the ten-year treasury to 5% or 6%—that is several years off also. So, I think we’ve got a couple of good years of gains ahead of us. I at least want the market to stay hot until my kids get out of high school, and then I can sell my house and go live on some exotic tropical island with great broadband.

Q: When you’re doing LEAPS, do you just do the calls only or do you do these as spreads?

A: You can do both. Just do the math and see what works for you on a risk/reward basis. You can do a 30% out of the money call 2 years out and get anywhere from a 1,000% to a 10,000% return—people did get 10,000% returns buying deep out of the money LEAPS in Tesla (TSLA) a year ago (that’s where all the vintage bourbon is coming from). Or you can do it more conservatively and only make 500% in two years on Tesla spread. For example; do something like a Tesla January 2023 $900-$950 call spread. If Tesla shares rise to $950, that position is an easy quadruple. But do the numbers, figure out the cost today, what the expiration value is in two years, and there you go.

Q: Do you think overnight rates could go negative as some people predict?

A: Not for a long time. They will go negative at the next recession because we’re starting off such a low base—or when we get the next pandemic, which could be as early as next year. We could get another one at any time from a completely different virus, and it would generate the same stock market results that we got last time—down 40% in a month. We’re not out of the pandemic business, we’re just having a temporary break waiting for the next one to come along out of China or some other country, or even right here in the USA. So that may be a permanent aspect of investing in the future. It could be the price we pay having a global population that's at 7 billion heading to 9 billion.

Q: Expiration on LEAPS?

A: I always go out two years. The second year is almost free, that’s why. So why not go for the second year? It gives you twice as much time to be right, always useful.

Q: My two-year United States Treasury Bond Fund (TLT) $125 put LEAPS have turned very positive. Is this a good trade?

A: That is a good trade, which you should put on during the next (TLT) rally. If you think we’re going to $105 in 2 years, do something like a $127-$130 two-year put LEAP, and there's a nice four bagger right there.

Q: Your Amazon (AMZN) price target was recently listed at $3,500, below last year's high, but I’ve also seen a $5,000 forecast in two years. Are you sticking with that?

A: Yes, I think when you get a major recovery in the economy, Amazon will be one of the only pandemic plays that keeps on going. It’s just taking a rest here with the rest of big tech. The breakup value of Amazon is easily $5,000 a share or more. Plus, they’re still going gangbusters growing into new industries that they’ve barely touched so far, like pharmaceuticals, healthcare, and so on. So yes, I would definitely be a buyer of LEAPS, and you could do something like the January 2023 $3700-$4000 LEAP two years out and make a killing on that.

Q: Anything you can do in gold (GLD)?

A: Not really. Although gold and silver (SLV) have been a huge disappointment this year, I think this could be the beginning of a capitulation selloff in gold which will bring us a final bottom, but it may take another month or two to get there.

Q: How can I sell short the dollar?

A: You sell short the (UUP), or there are several 1X and 2X short ETFs in the currencies that you can do, like the ProShares Ultra Short Euro ETF (EUO). That is the way to do it.

Q: What is the best timing for buying LEAPS?

A: Buy at market bottoms. A year ago, I was sending out lists of 10 LEAPS at a time saying please buy all of these. You need both a short-term selloff in the stock, and then an upside target much higher than the current price so your LEAP expires at its maximum profit point. And if you’re in the right names, pretty much all the names that we talk about here, you will have 30%, if not 300% or 3,000% gains in them in the next two years.

Q: Do you think Tesla’s Starlink global satellite system will disrupt the cell tower industry?

A: Yes, that is the goal of Starlink—to wipe out all ground communication for WIFI and for cell phones. It may take them several years to do it, but if they do pull it off, then it just becomes a matter of pricing. The last Starlink pricing I looked at cost about $500 to set up, open the account, and get your dish installed. And the only flaw I see in the Starlink system is that the satellite dishes are tracking dishes, which means they lock onto satellites and then follow them as they pass overhead. Then when that signal leaves, it locks onto a new satellite; at any given time they’re locked onto four different satellites. That means moving parts, and you want to be careful of any industry that has moving parts—they wear out. That’s the great thing about software and online businesses; no moving parts, so they don’t wear out. And that’s also why Tesla has been a success; they eliminated the number of moving parts in cars by 80%. I’m waiting for Starlink to get working so I can use it, because I need Internet access 24 hours a day, even if all the local hubs are out because of a power outage. I’m now using something called Viasat (VSAT), which guarantees 100 megabyte/second service for $55 a month. It's not enough for me because I use a gigabyte service landline, but when that’s not available then I can go to satellite as a backup.

Q: Is there too much Fed liquidity in the market already? Why is the $1.9 trillion rescue package still positive for the market?

A: Firstly, there is too much liquidity in the market; that is screamingly obvious. If you look at liquidity over the decades, we are just staggeringly high right now. M2 is growing at 26% against the normal rate of 5%-6%. What the stimulus package does is get money to the people who did not participate in the bull market from last year. Those are low-income people, cities, and municipalities that are broke and can’t pay teachers, firemen, and policemen. It also goes to individual states which were not invested in the stock market. It turns out that states that were invested in the stock market like California have money coming out of their ears right now. And it gets money to low wage workers with kids who are certainly struggling right now. So, it is rather efficiently designed to get the money to people who need it the most. There is still half the country that doesn't own any stocks or even have savings of any kind. One or two people might get it who don’t deserve it but try doing anything in a 330 million population country and have it be 100% efficient.

Q: Is inflation coming?

A: Only incrementally in tiny pieces, so not enough to affect the stock market probably for several years. I still believe technology is advancing so fast that it wipes out any effort to raise prices or increase wages, and that may be what the perennially high 730,000 weekly jobless claims is all about. Those jobs that might have been there a year ago have been replaced by machines, have been outsourced overseas, or the demand for the product no longer exists. So, as long as you have a 10% unemployment rate and a weekly jobless claim at 730, inflation is the last thing you need to worry about.

Q: Is there any way to cash in on Reddit’s Wall Street Bets action?

A: No, and I would bet the majority of people who are trading off of these emojis and Reddit posts are losing money. You only hear about these things after it’s too late to do anything about them. I don't think you’ll get any more $4 to $450 moves like you did with GameStop (GME) because in that one case only, there was a short interest of 160%, which should have been illegal. All the other high short interest stocks have already been hit, with short interests all the way down to 30%, so I think that ship has sailed. It has no real investing merit whatsoever.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-05 10:02:582021-03-05 11:46:15March 3 Biweekly Strategy Webinar Q&A

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-19 10:04:152021-02-19 10:28:18February 19, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.