(MARKET OUTLOOK FOR THE WEEK AHEAD or DID JAY POWELL BLOW IT?) and CHASING EARNEST HEMINGWAY),

($VIX), (INTC), (CCI), (TLT), (COPX), (BHP), (USO) (NVDA), (SLV), (FXY), (CAT), (IWM), (IBKR), (AMZN), (GLD), (BRK/B), (DE)

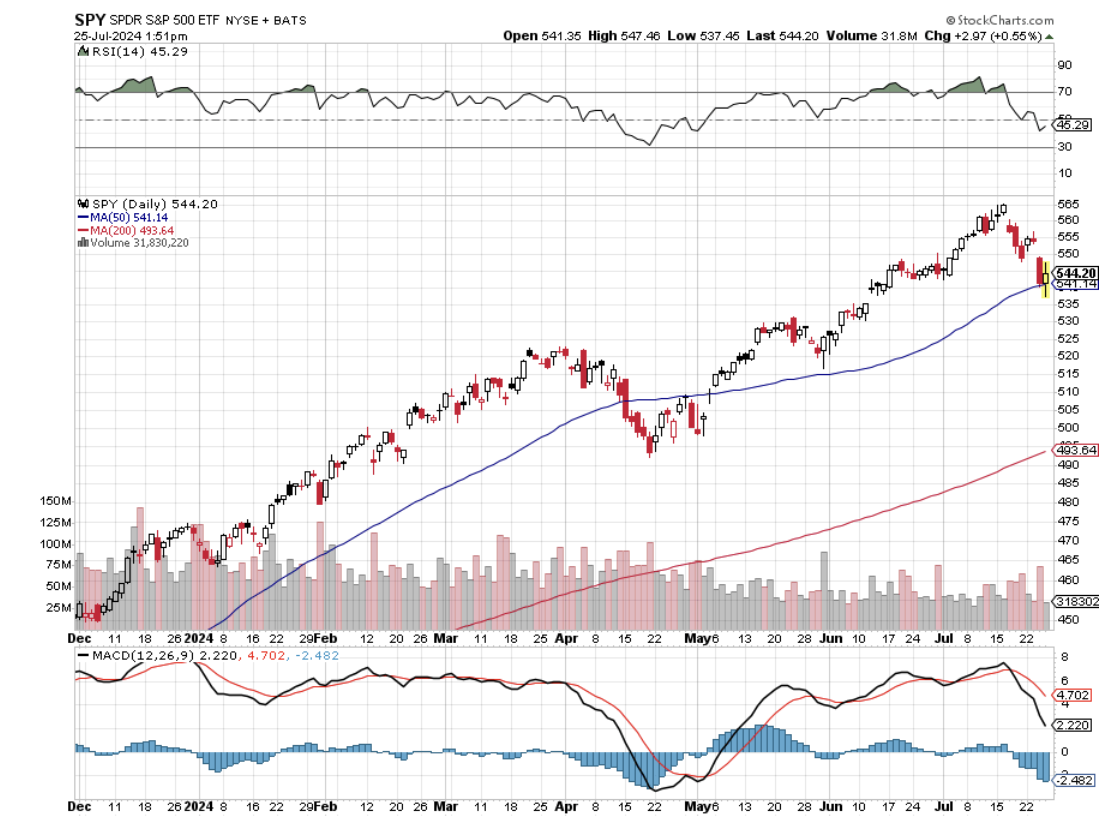

Below please find subscribers’ Q&A for the July 24 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Zermatt, Switzerland.

Q: Does the entry of Kamala Harris into the presidential election have any effect on the stock market?

A: No. I know someone who did research on markets and elections going all the way back to 1792 and the long-term effect has been absolutely zero over the 232-year period. Actually, what happens is you have the two candidates very close to each other in the polls, so uncertainty is at a maximum. Markets hate uncertainty, so they’ll wait until the uncertainty goes away, which will probably be about two weeks before the election. You can expect a really hot 4th quarter in the market though, so get all your cash freed up so you can pour all your money into the market for the last quarter of the year.

Q: How do falling interest rates affect the US dollar (UUP) and the currencies?

A: Currencies (FXE), (FXC), (FXA), (FXB) are always driven by interest rates. Those with high interest rates like the US dollar, are strong; those with low interest rates like Japan, are weak. Japan has had zero rates for over 20 years now. When that reverses, those currencies reverse, ending up with a weak US dollar and a strong euro, pound, etc. These changes in direction for the currency markets only happen every few years, so that will be a reliable trade.

Q: Why is oil (USO) so cheap when the rest of the economy is so strong?

A: There are many reasons. One is that the amount of barrels of oils needed to produce a unit of GDP has been falling for 30 years. That's a function of engines becoming more efficient at using gasoline. Plus more people are switching out of gasoline into electric, and more people flying instead of driving. The “work at home” movement hasn’t helped oil demand either. It’s also the most subsidized industry in the US, and you always get overproduction leading to price crashes, which we now seem to be witnessing.

Q: I have Freeport McMoRan (FCX) as a long-term hold; why has it recently been so weak?

A: Well, the number one reason is China (FXI). China is the biggest consumer of copper in the world and their economy is dead in the water. You know, 4.5% or 4.7% is a long way from the 13% we used to get during the 2000s and when copper was absolutely on fire. Eventually, I expect industrial demand in the US to make up for the shortage of demand from China, but that isn’t happening right now. It isn’t just copper—all the industrial metals have been weak the last couple of months and that is the reason.

Q: Cameco Corporation (CCJ) has been down lately, even with seemingly good news out of Kazakhstan. Is this a good buy here at the 200-day?

A: I would say it is. It’s being dragged down by the rest of the industrial metals and the energy plays. If you watch carefully, the uranium stocks trade very closely with oil, and we have an oil glut, so it tends to drag down all the other energy forms with it, including uranium and natural gas. I love uranium demand long term; it's growing far faster than oil demand and that’s why I own (CCJ).

Q: Do you think falling interest rates will bail out the real estate market?

A: Absolutely, yes. 30-year fixed-rate mortgages hanging around the mid-sixes, you get a couple of rate cuts and we could be back into the fives and even the fours in no time. So yes, big impact on real estate, all the subsidiary plays, on home builders, on the entire economy.

Q: If the market reverses today or tomorrow, what are some of the best call options to put money into?

A: Caterpillar (CAT), Deer & Co. (DE), and you might even go $50 into the money on Nvidia (NVDA). Home builders I would love to get into as well. All of these things have had great runs, but these are just the 1st leg of moves that could go on for years. So yes, this is where the barbell portfolio works: half big tech, half domestic recovery plays.

Q: Are you stopping at Edelweiss for a frosty beer on your hike?

A: Absolutely, I go to Edelweiss every year and don’t mind climbing the 1,200 feet to get there. You certainly have an appetite when you get to the top. It has a fantastic view of the town and you can stay there overnight there as well.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

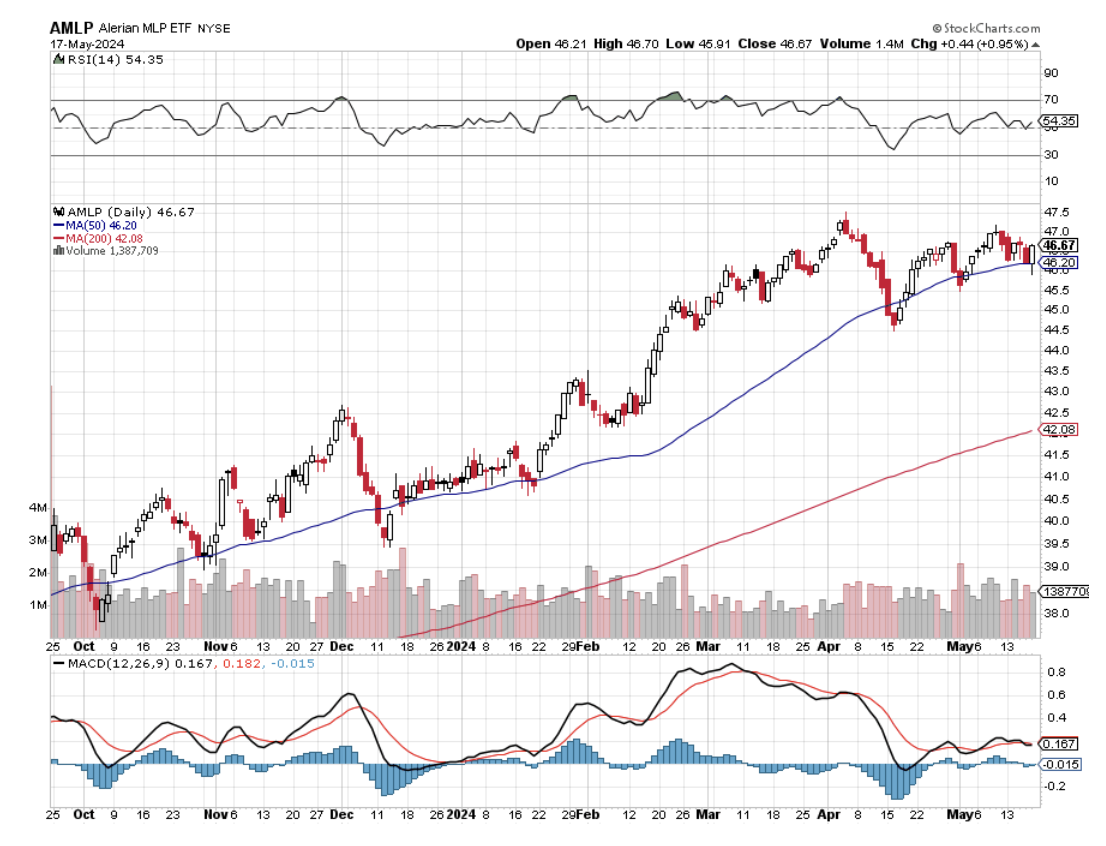

There was probably no more broken promise in the investment world over the last several years than that energy master limited partnerships (MLPs) would hold up even if the price of oil fell.

These guys were toll takers, it was said, and profited from the volume of crude pumped through their pipelines. The price of oil was somebody else’s problem.

In any case, double-digit yields would provide more than ample support in any kind of sell-off.

It didn’t quite work out like that.

Once the price of Texas tea (USO) began its plunge in 2014 from $107 to negative $37 at the pandemic low, any investment tarred with an oil connection got slaughtered.

It was the classic flash fire in the movie theater.

Bids for MLP’s vaporized.

Making matters worse is that many retail investors bought highly leveraged MLPs on margin, turning 10% yields into 20% ones. When the sushi hit the fan, it didn’t take long for those positions to go to zero.

Most of the leveraged plays went bankrupt or were unwound in a variety of creative ways with enormous losses.

I always find it a useful exercise to sift through the wreckage of past investment disasters. Not only are there valuable lessons to be learned, but sometimes great trades emerge.

I have been doing that lately in the energy sector, a hedge fund favorite these days, and guess what?

MLPs are back. And no, I’m not talking about the Maui Land and Pineapple Company (MLP) (yes, there is such a thing!).

But these are not your father’s MLPs.

Let me start with my investment thesis.

It is always better to invest in an asset class that has its crash behind it (energy) than ahead of it (the US dollar).

And let’s face it, the final bottom for oil this year at $68 is in.

We may bounce around a bottom for a while as recession fears prevail. But eventually, I expect a global synchronized economic recovery to take it sustainably higher, $100 a barrel or better.

And while I have never been a fan of OPEC, they are showing rare discipline in honoring the production quotas negotiated in November.

That eliminates much of the downside from MLPs and makes it one of the more attractive risk/reward trades out there.

Except that this time it’s different.

Thanks to hyper-accelerating technology (yes, there’s that term again), new wells employ a fraction of the labor of the old ones and are therefore more profitable.

That means they can function, and even prosper, with a much lower oil price.

The surviving MLPs are now a much better quality investment.

Balance sheet quality has improved as a result of deleveraging in the last 14-18 months, and the worst of the rating downgrade cycle is likely behind us.

Importantly, some $50 billion‒$60 billion of growth opportunities for MLPs are expected during FY2024-2025.

That makes the industry one of the great secular growth stories out there today.

As an old fracker myself, I can tell you that the potential of the revolutionary new technology has barely been scratched.

Thanks to technology that is improving by the day, Saudi Arabia’s worth of energy reserves remains to be exploited, potentially turning the US into an energy-exporting powerhouse as the world’s largest producer at 13 million barrels a day.

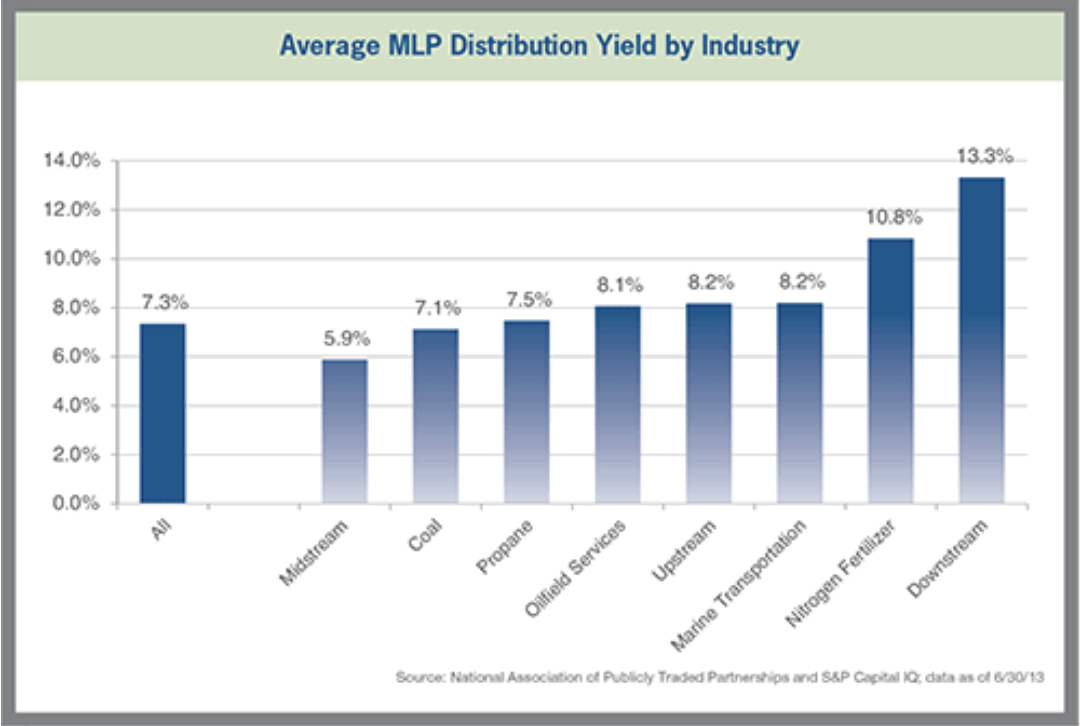

Industry experts expect MLP distributions to grow by 3%‒5% annually over the coming years. Few other industries can beat this.

That means avoiding upstream Exploration and Production companies; where there is still a ton of risk, and placing your bets on midstream companies that operate pipelines. And by midstream, I don’t just mean pipelines but also processing facilities for natural gas liquids and storage and terminal facilities.

You especially want to look at companies with high barriers to entry and attractive assets in high-growth and low-cost production regions. I’m all about big moats (see (NVDA)).

Companies with a sustainable cost advantage, operated by experienced management with proven geological are further pluses.

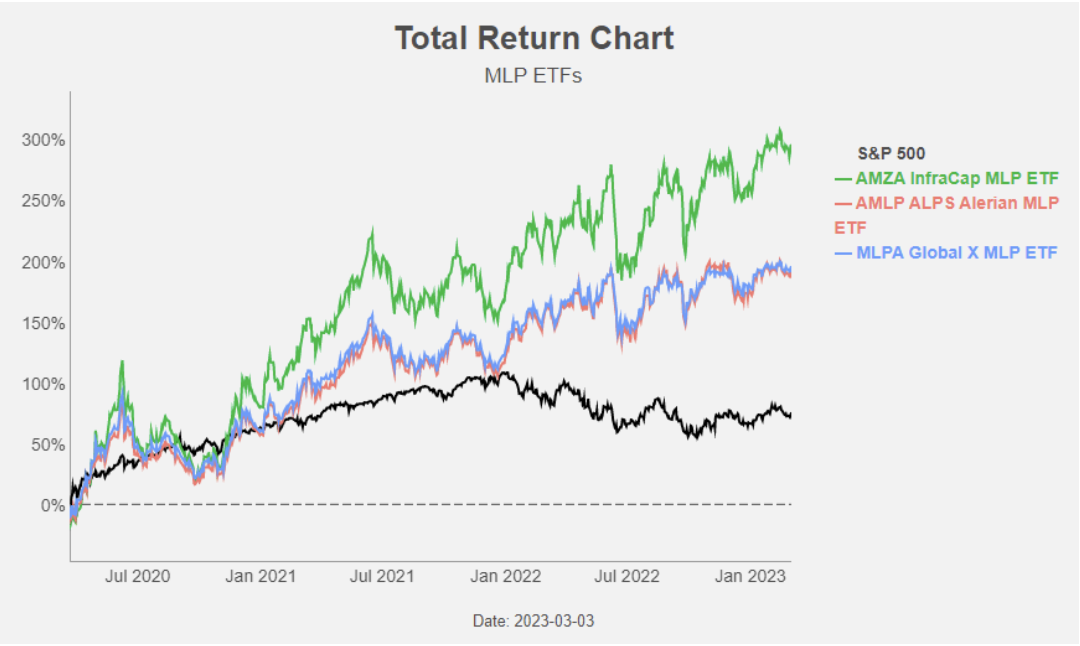

MLPs also stack up nicely as a diversifier for your overall portfolio.

Over longer time periods, MLPs have generated similar returns to equities, with similar to slightly higher levels of volatility.

Historically they have traded at lower yields than high-yield bonds, but currently, they are yielding 150 basis points more.

And now for the warning labels.

This is not a new story.

As you can see from the charts below, MLPs have been rallying hard since oil bottomed at the pandemic low in April 2020.

And if my oil forecast is wrong and we plumb new generational lows once again, investment in this sector will suffer.

Still, with yields in the 7%-10% range, a certain amount of pain is worth it.

Still interested?

Take a look at the Alerian MLP ETF (AMLP) (7.36%) and the Global X MLP Energy Infrastructure ETF (MLPX) (4.91%), Western Midstream Partners (WES) (9.20%), and Energy Transfer LP (ET) (7.96%).

https://www.madhedgefundtrader.com/wp-content/uploads/2017/02/Pipelines-e1487795183955.jpg266400The Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngThe Mad Hedge Fund Trader2024-05-22 09:02:042024-05-22 12:36:59The Rebirth of the Master Limited Partnership

Below please find subscribers’ Q&A for the May 15 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

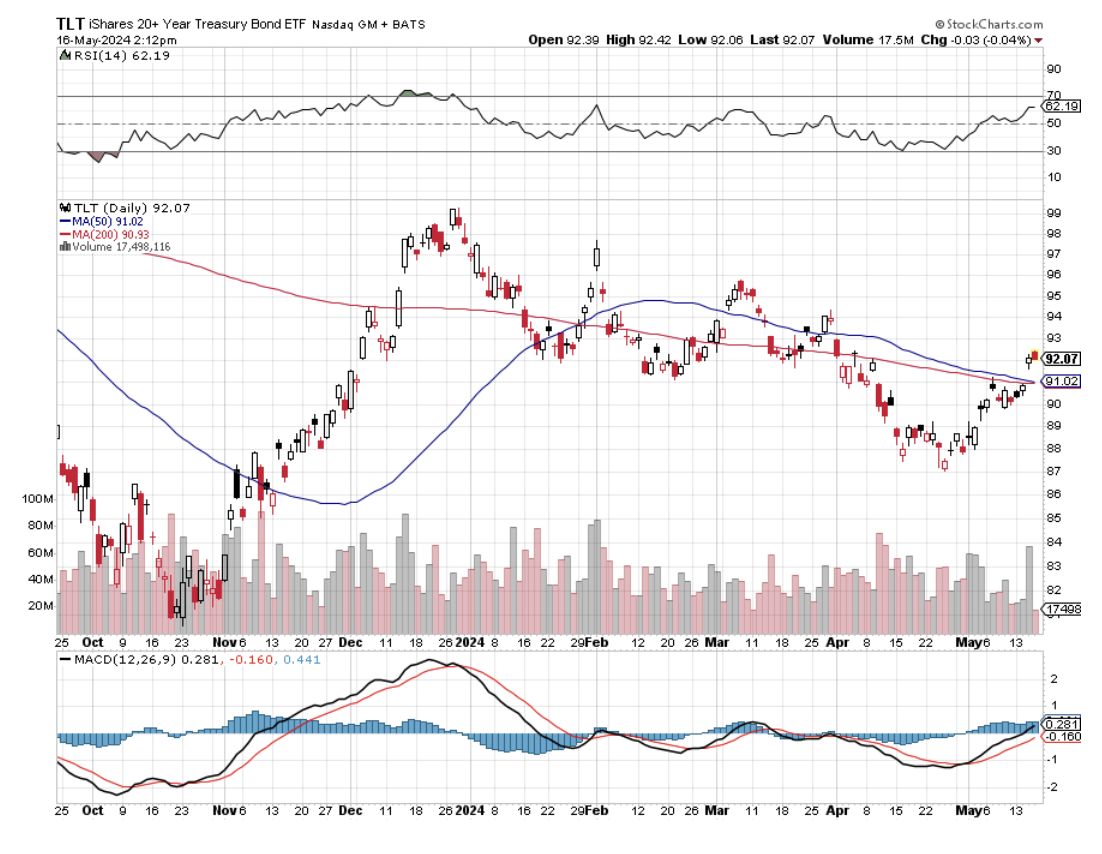

Q:Is it time to get out of the 94/97 (TLT) spread?

A: No. We're getting close to a stop, but I think markets will peak out in the next couple of days and we can get out with a small profit. The weak PPI/CPI/Nonfarm, payroll was a game changer. So watch carefully as always. I could have come out of that with 2/3 of the profit last week, but who knew the market would go up 10 out of 11 days?

Q: What are your thoughts on meme stocks? I see that GameStop (GME) is up 550% in a week.

A: This is not investment, it's pure gambling. And if you do want to gamble, there are much better games to play than meme stocks. For example, Blackjack gives you a 51-49% risk in your favor, and slot machines are not too far off at 55-45%. This is not the same meme stock run that we had three years ago. Back then, the short interest in (GME) was 125%, which is more than the outstanding shares that existed. People are still trying to figure out how that happened. Now, the short interest is only 20%, so this may peak out a lot quicker than last time. In any case, it’s a totally random movement. It's just for kids to do because if kids lose all their money, they can start over again and still have enough money to retire. Chances are if you lose all your money, you won't have enough money to retire, so just another reason to stay out of meme stocks.

Q: I'm noticing the REITs are beginning to make a comeback. Can you comment?

A: They've actually been on a terrific run the last several weeks. Some of my favorites like Crown Castle Inc. (CCI) have had really big moves, and this is just the beginning of a major upside; and not only REITs, but all interest rate plays, and it turns out almost everything is an interest rate play when you look at it. Utilities, secured loans, junk bonds—it's a huge universe. So that's why I say buy everything; everything that's going to go up at all is especially positively affected by lower rates, especially precious metals—gold and silver. And when things go up, the definition of a precious metal expands. It now includes copper, palladium, and platinum, which has had an enormous run.

Q: Can we expect a recession to hit in 2025?

A: Absolutely not. We're in the early stages of a golden age of a decade, of appreciating assets of all kinds; not only stocks and bonds, but real estate, collectibles, baseball teams—you name it. So don't leave the game after the first inning, to use a baseball metaphor. And for you foreigners out there who know nothing about baseball, that means don't leave too early.

Q: Is the housing market overvalued in the US?

A: Good question, you'd certainly think that if you're out there trying to buy a house (and I've been shopping myself lately). The answer is absolutely not. It may be overpriced in the most expensive US markets like Manhattan, Honolulu, Hawaii, or San Diego, but it's still a fraction of what you have to pay in Hong Kong, Australia, or Vancouver, Canada. So prices can go a lot higher. Remember, we have a structural shortage of 10 million homes in the US and they’re not building new ones fast enough. They could double in price from here, especially if the Fed starts to cut interest rates, which they have promised to do. I think we're on the verge of another big housing boom, which will create more home equity, and guess what happens to that home equity? It eventually ends up in the stock market. It becomes a virtual love fest with housing prices making stocks go up and stocks making housing prices go up.

Q: Would you consider Bitcoin now?

A: Absolutely not, especially when you can buy things like Wheaton Precious Metals (WPM) and Barrick Gold (GOLD), which will probably double in the next year and actually have real assets with real earnings flows. With Bitcoin, you're essentially buying ether, and the time to buy Bitcoin was at $6,000, not at $60,000. You don't buy stuff after it's gone up 10 times. So again, just from a market timing point of view, it's a terrible idea. So there are better things to do. You can buy high-quality stocks at reasonable multiples right now.

Q: Is Airbnb (ABNB) a buy here?

A: I would. It is the world's largest hotel in an economic recovery. There's a huge demand for hotels and revenge travel. They're also branching out into higher-margin items like experiences. So yes, I do love the company and the quality of its management for sure.

Q: Markets are all-time high. Should I sell in May and go away?

A: Only if you're a short-term trader. If you’re a long-term investor and you sell now, I guarantee you'll miss the next bottom to get back in. So for short-term traders, yes, take profits like crazy—markets are way overbought. They either need some kind of correction or flat-line move for a period of time.

Q: Is buying American farmland a good investment for buying an index fund?

A: Well, if you look at the big portfolios of the great wealthy names like the Rockefellers, the Duponts, and all of my former clients at Morgan Stanley basically; they have loads of farmland and loads of forests—lots of forests. In fact, forests are trading at a big premium right now. It's considered the world's safest long-term asset. And as long as you don't have debt on it, it always goes up in value over time. So yes, that is a good investment. US farmland is the most productive in the world, and the number of people in the world isn't shrinking. In fact, the main reason China will never start a war with the US is because they're dependent on the US for about half its total food supply. So that's why I can always ignore all these China or Taiwan invasion warnings.

Q: Should I take a look at defense stocks?

A: Absolutely, yes, thanks to the invasion of Ukraine. Virtually every country in the world that has any money is expanding defense spending. This is not a short-term thing. Defense is a very long-time lag industry. When countries like the US buy planes, it's often for ten or twenty years, and then you have the upgrades to follow that, and third-country sales. So the big stocks are Lockheed Martin (LMT) and Raytheon (RTX). I would buy both of those on the dips. They have already had good moves, but what hasn't? Though there are not a lot of bargains left in this market after a heroic six to seven-month run.

Q: Is the webinar recorded for replay?

A: Yes, just go to our website madhedgefundtrader.com. Log in, go to My Account, and you'll see the opportunity to review the video of this presentation.

Q: Is it time to buy Google (GOOG)?

A: Yes, I think we're on an uptrend that continues for the rest of the year, and Google will keep leaking out its advantage in AI in bits and pieces. I saw the video you were talking about; you just leave the phone’s video on all the time, and then you could say, “Where are my glasses?” and it'll tell you where your glasses are: “You left them on the table in the dining room.” That's one of the many millions of applications we will see.

Q: Thoughts on Tesla (TSLA)?

A: We're trying to put in a bottom here. Get ready for the buy alerts—I think on the next plunge down I may actually jump in. We still have a very high volatility, and you have plenty of great pickings in the options market with high implied volatilities.

Q: Where are we on refilling the strategic oil reserves (USO)?

A: Biden made no effort to refill them. They were about at half-full levels when we hit the bottom last time, so maybe he will next time. I think he's more interested in just getting out of the oil business altogether, moving to alternative energy, and getting rid of the strategic oil reserve since we are now a net energy producer, net oil exporter, the world's largest oil producer in the world. We don't really need emergency reserves like we did in 1970 when these were first set up.

Q: Sometime back, you said to avoid miners of precious metals. Is that still your opinion?

A: No, I think we're in a position now where the miners can start to catch up with the metals. In the beginning of the year, it was clear the metals were going to outperform the miners because the miners were seeing their margins cut by high inflation. That's still the case. My first choice is still the metal, but you could get a big catch-up trade in the silver and gold miners. So, as I keep saying, buy Barrick Gold (GOLD) and (WPM).

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

There comes a time in every trader’s life when it’s time to face harsh reality and admit that you’re just dead wrong.

As much as I thought a I had strong case for the best stocks to move sideways before continuing their upward drive, the markets decided otherwise. One thing I have learned over my half-century of trading is that you never argue with Mr. Market. He is always right.

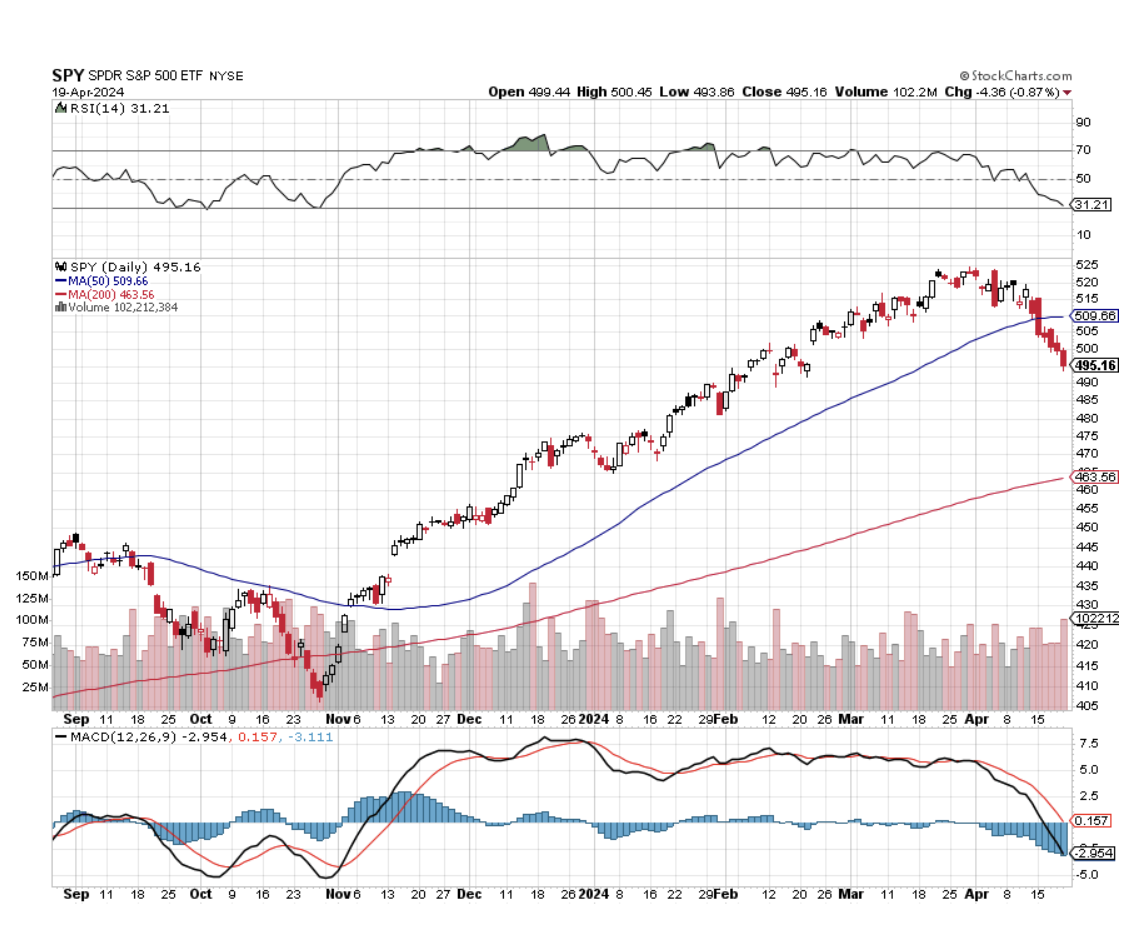

So it was with some dismay that on Friday, I watched NVIDIA (NVDA) shares slice through its 50-day moving average at $840 like a hot knife through butter putting the shares into a free-fall. Virtually the next print was the low of the day at $760, down 10% on the day.

There was no new news about (NVDA). Its prospects look as bright as ever, and there are a series of conferences of earnings reports over the coming month to remind us of that. But sometimes, the market just doesn’t care.

(NVDA) has had a great run, up some 144% since October. During this time, I executed a dozen profitable long-side trades. But when you’re that aggressive you know in advance that the last trade is going to kill you and that is the case today. (NVDA) is falling because of the sheer weight of its price.

New flash: while (NVDA) is still the cheapest big tech stock in the market, cheap stocks can get cheaper as we all know.

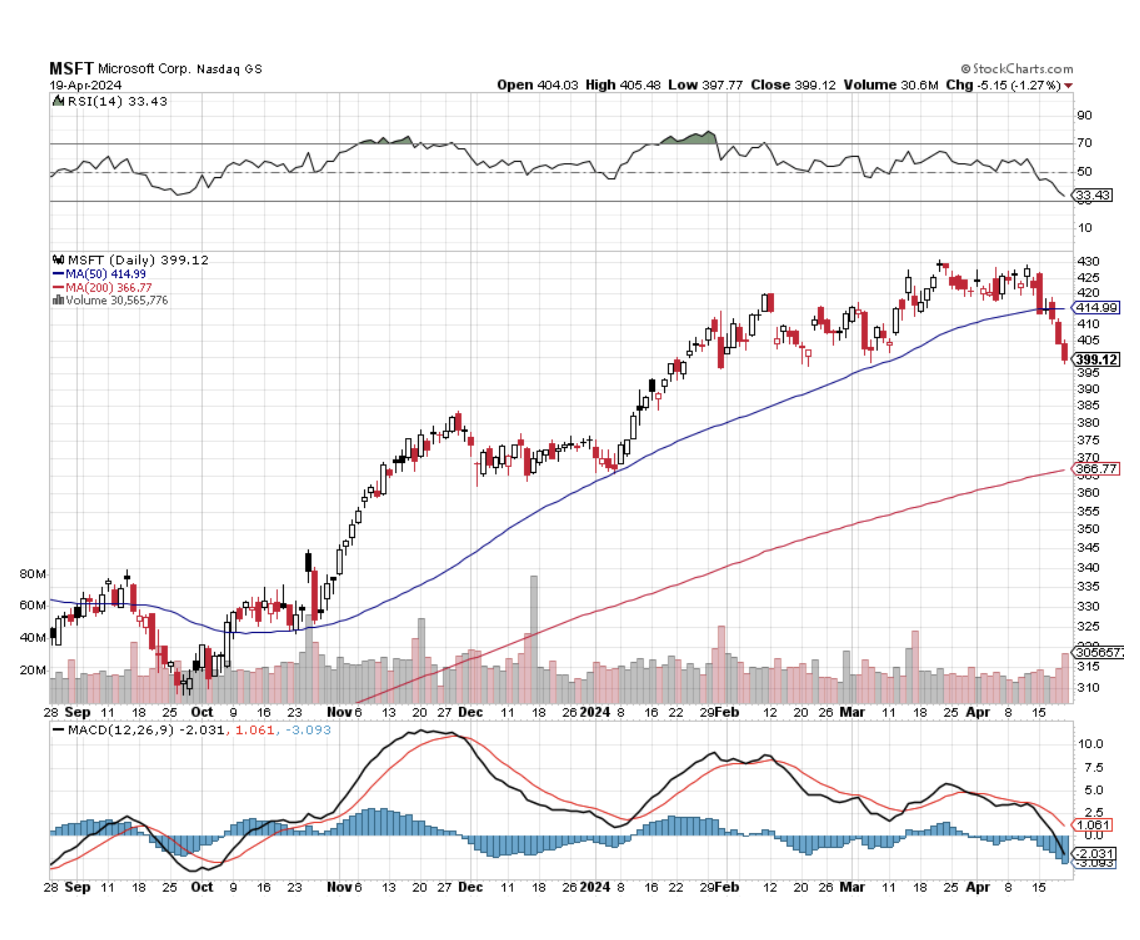

With the advantage of 20/20 hindsight, I should have been paying more attention to the Magnificent Seven 50-day moving averages which have been falling like dominoes. First went Tesla (TSLA) in February and Apple in March. The S&P 500 (SPY) gave it up on Monday and Microsoft (MSFT) on Wednesday. Amazon (AMZN), (META), and (NVDA) were the last to go on Friday.

Sure you can blame the April 19 option expiration when traders were loaded to the hilt with expiring longs with all these stocks they had to dump. The dreaded month of May, when traders go to die, and the summer doldrums are just two weeks away. Algorithms poured gasoline on the fire exaggerating the moves, as they always do. But still, wrong is wrong.

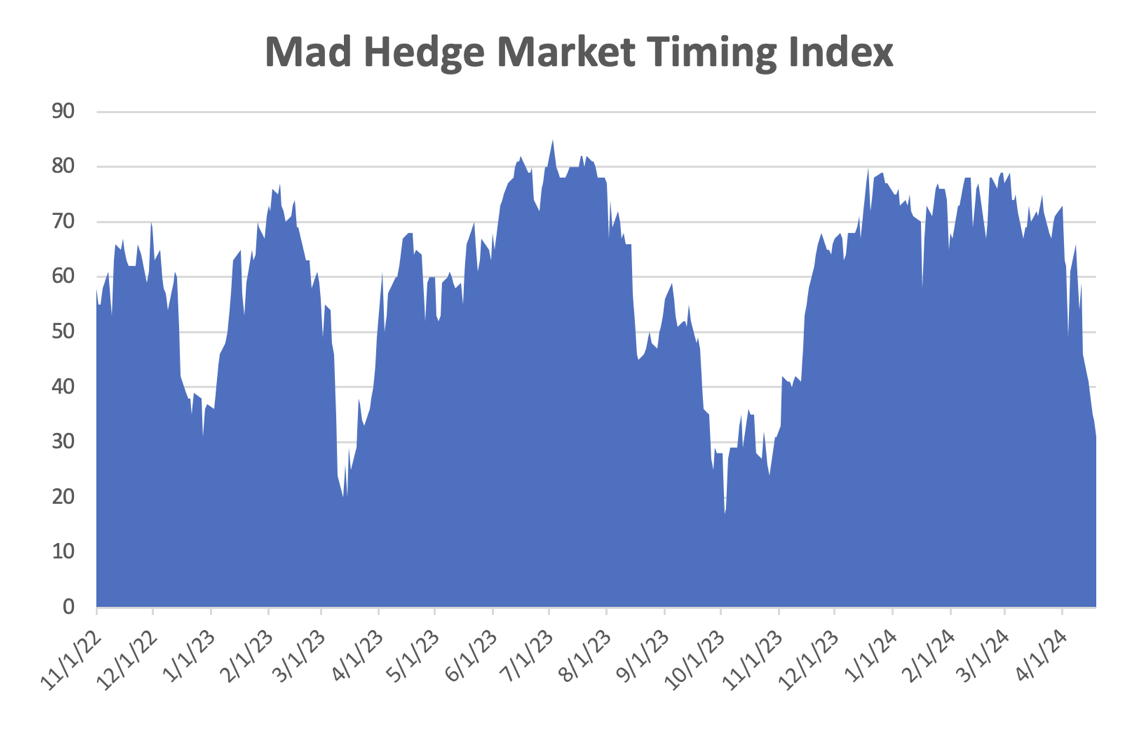

And there’s my mea culpa for 2024. I am human after all. I’m not right all the time, I just act like it. If the horrific market action last week has one silver lining, it’s that it sets up the next great trades, for which there will be many. With my Mad Hedge AI Market Timing Index down to a lowly 31 that may not be far off.

Your next question is “How far down is down?” In the worst-case scenario, the 200-day moving average is in play for all of these. That is pegged at $463 for the S&P 500, $569 for (NVDA), $377 for (MSFT), $150 for (AMZN), and $308 for (META). (AAPL) and (TSLA) already lost their 200-days a long time ago. In other words, the market is in the process of giving up all its 2024 gains and then some.

Sure, the 200 days are all rising sharply so it's unlikely we’ll hit these dire numbers. Still, it's best to prepare your boss for the worst and then let serendipity work its magic.

Remarkably, my commodity and precious metal stocks, where I had eight of ten long positions, stuck to the script and moved sideways instead of down. If you throw bad news on a stock and it refuses to fall, you buy the hell out of it. So that will be my next move in the market, once I clean all the mud off my face and pull the arrows out of my rear.

Those of us who have been trading gold for a long time, I’ve been doing it for 50 years and 60 if you count the Kennedy silver dollars I collected, will tell you that this new bull market in the barbarous relic is a very strange one.

None of the traditional factors that drive gold up are present. Interest rates have lately been rising, not falling. ETF financial demand fell all last year, and much of that money was diverted to Bitcoin. Retail demand, especially from Asia, has also been falling off a cliff. Gold miners have in no way been leading the price of the yellow metal because of their excess leverage as they usually do. But gold has seen a 34% rally off the October low.

Go figure.

It turns out that central bank buying has increased dramatically, especially from China, enough to offset all the other no-shows. The conflict in the Middle East is also drawing in more flight to safety demand. The good news is that the Chinese buying will continue. The bad news is that this might be a precursor to the invasion of Taiwan as it flees the Western financial system.

What does all this mean? When the traditional demand for gold returns, interest rates, ETFs, and retail, the price of gold will move a lot higher. The barbarous relic can easily reach $2,800 this year and possibly $3,000. The miners will play catch up. Buy (GLD) on dips and silver (SLV) as well, which has a lot of catching up to do.

I just thought you’d like to know.

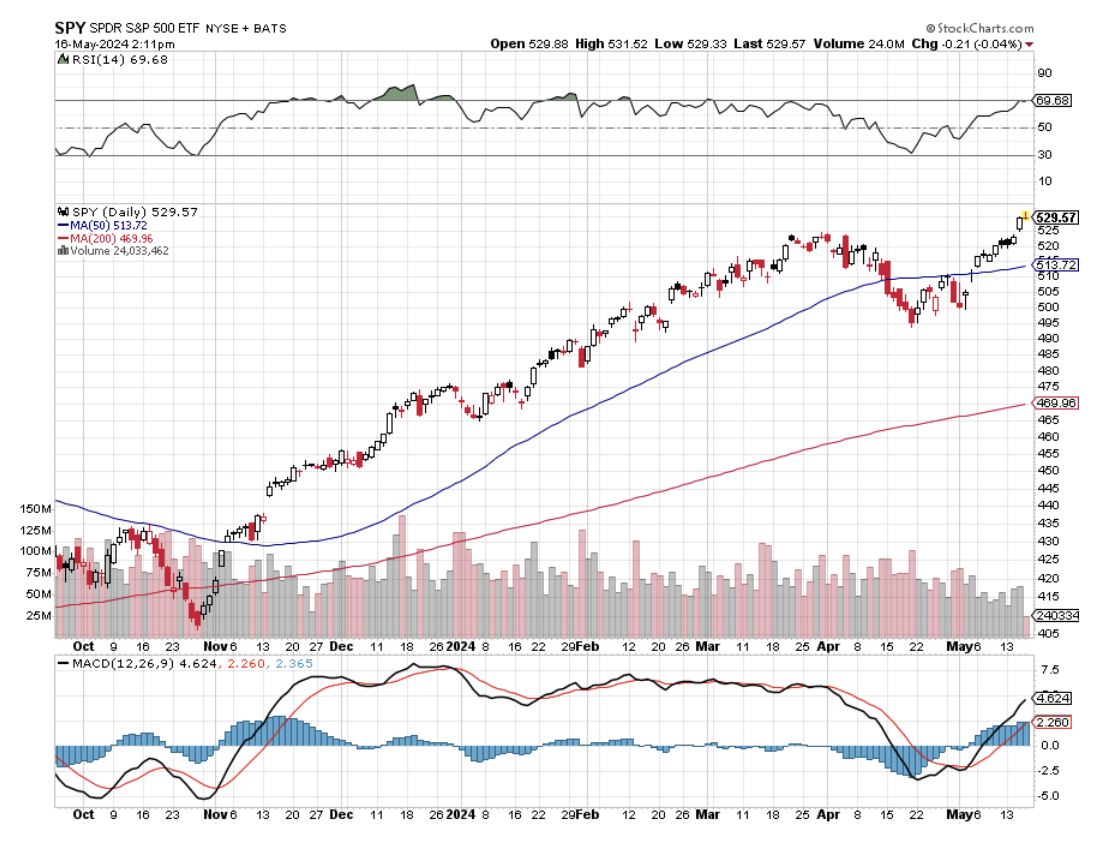

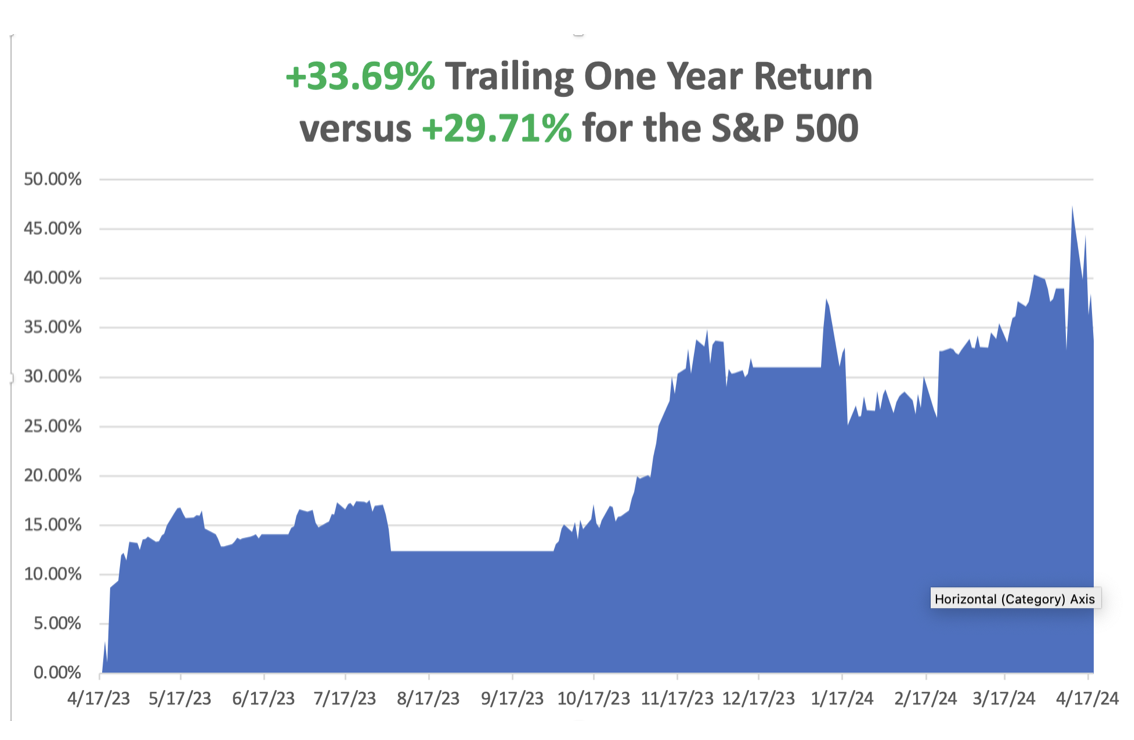

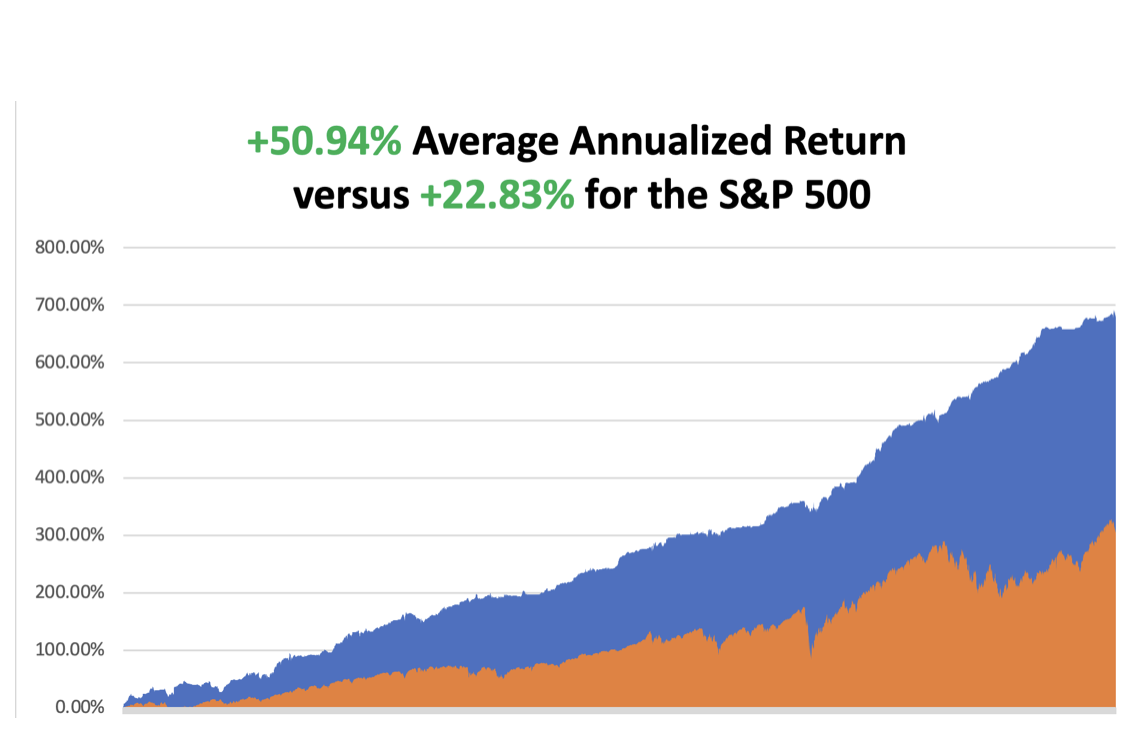

So far in April, we are down a heartbreaking -6.69%. My 2024 year-to-date performance is at +14.47%.The S&P 500 (SPY) is up +2.68%so far in 2024. My trailing one-year return reached +33.69% versus +29.71% for the S&P 500. That brings my 16-year total return to +676.63%.My average annualized return has recovered to +50.94.

Some 63 of my 70 round trips were profitable in 2023. Some 20 of 28 trades have been profitable so far in 2024.

I stopped out of my long in Tesla last week at cost, expecting further downside, which happened. A week early the position had been at max profit. I let my April longs expire at a max profit on April 19 in Freeport McMoRan (FCX), Occidental Petroleum, ExxonMobile (XOM), Wheaton Precious Metals (WPM), and Gold (GLD).

That leaves me with my remaining May longs in (TLT) and (FCX) a double long in (NVDA) and 60% in cash. Volatility Index ($VIX) Hits Six-Month High, on threats of a New Iran War, Oil Supply Cut-offs, and topping stocks. It’s been a long and dry desert crossing, but we are finally back to reach the $20 handle. The volatility trade is back. For a double bonus, the Mad Hedge Market Timing Index also dropped below 50 for the first time since October. Options traders will love it!

Junk Bonds See Biggest Outflows in a Year, as the Federal Reserve’s hawkish approach to inflation makes investors wary, sending yields soaring to 6.33%. Yields won’t peak until the Fed actually cuts rates. Buy (JNK) and (HYG) on dips.

Netflix (NFLX) Adds 9.33 Million New Subscribers, nearly double analyst forecasts, including my five kids who aren’t allowed to share my password anymore. But the shares dropped on weak Q2 guidance. Netflix has rebounded from a slowdown in 2021 and 2022 to grow at its fastest rate since the early days of the coronavirus pandemic. That is due in large part to its crackdown on people who were using someone else’s account. The company estimated more than 100 million people were using an account for which they didn’t pay.

Mortgage Rates Top 7.0% for the first time in 2024, adding dead weight to the housing market. Most borrowers are now taking out adjustable 5/1 ARMS and then praying for a Fed rate cut later this year.

Existing Home Sales Dive by 4.3% in March to 4.19 million units on a sign-contract basis. Inventories rose 4.47% to a 3.2-month supply, up 14% YOY. The median price of an existing home sold in March was $393,500, up 4.8% from the year before. Regionally, sales fell everywhere except in the North, where they rose 4.2% month-to-month. Sales fell hardest in the West, down 8.2%. Prices are highest in the West. Housing Starts Plunge, down 14.5% in March. Permits for future construction of single-family houses fell to a five-month low. Residential investment rebounded in the second half of 2023 after contracting for nine straight quarters, the longest such stretch since the housing market collapse in 2006. But the recovery appears to be losing steam. China Surprises with Q1 GDP Growth at 5.3%, but who knows how real these numbers really are? They don’t line up with individual data like international trade. Peak China is behind us. Avoid (FXI).

Tariff Wars Heat Up, US President Joe Biden is threatening China again, and this time he wants to triple the China tariff rate on steel and aluminum imports. On Wednesday, the president will visit the United Steelworkers headquarters in Pittsburgh and has vowed his saber-rattling is not just empty threats. His rhetoric on China could make relations between the US and the Middle Kingdom that much frostier as we enter into the heart of the US election race.

Biden Boosts the Cost of Alaska Oil Drilling Leases, from $10,000 to $160,000, the first increase since 1920. There is also a bump in the royalty on extracted oil, from 12.25% to 16.27%. The government is no longer giving away oil found on its land for free. Coddling of the oil companies is over. Oil companies will no longer bid for cheap oil leases with the intention of sitting on them for decades. The US is currently the largest oil (USO) producing country in history at 13 million barrels/day and hardly needs any subsidies, which date back to the Great Depression. Buy energy stocks on dips, like (XOM) and (OXY), which are posting record profits.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 22, at 7:00 AM EST, the Chicago Fed National Activity Index is announced.

On Tuesday, April 23 at 8:30 AM, New Home Sales are released.

On Wednesday, April 24 at 2:00 PM, Mortgage applications come out.

On Thursday, April 25 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, April 26 at 8:30 AM, Consumer Expectations. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I spent a decade flying planes without a license in various remote war zones because nobody cared.

So, when I finally obtained my British Private Pilot’s License at the Elstree Aerodrome, home of the WWII Mosquito twin-engine bomber, in 1987, it was cause for celebration.

I decided to take on a great challenge to test my newly acquired skills. So, I looked at an aviation chart of Europe, researched the availability of 100LL aviation gasoline in Southern Europe, and concluded that the farthest I could go was the island nation of Malta.

Caution: new pilots with only 50 hours of flying time are the most dangerous people in the world!

Malta looms large in the history of aviation. At the onset of the Second World War, Malta was the only place that could interfere with the resupply of Rommel’s Africa Corps, situated halfway between Sicily and Tunisia. It was also crucial for the British defense of the Suez Canal.

So, Malta was mercilessly bombed, at first by Mussolini’s Regia Aeronautica, and later by the Luftwaffe. By April 1942, the port at Valletta became the single most bombed place on earth.

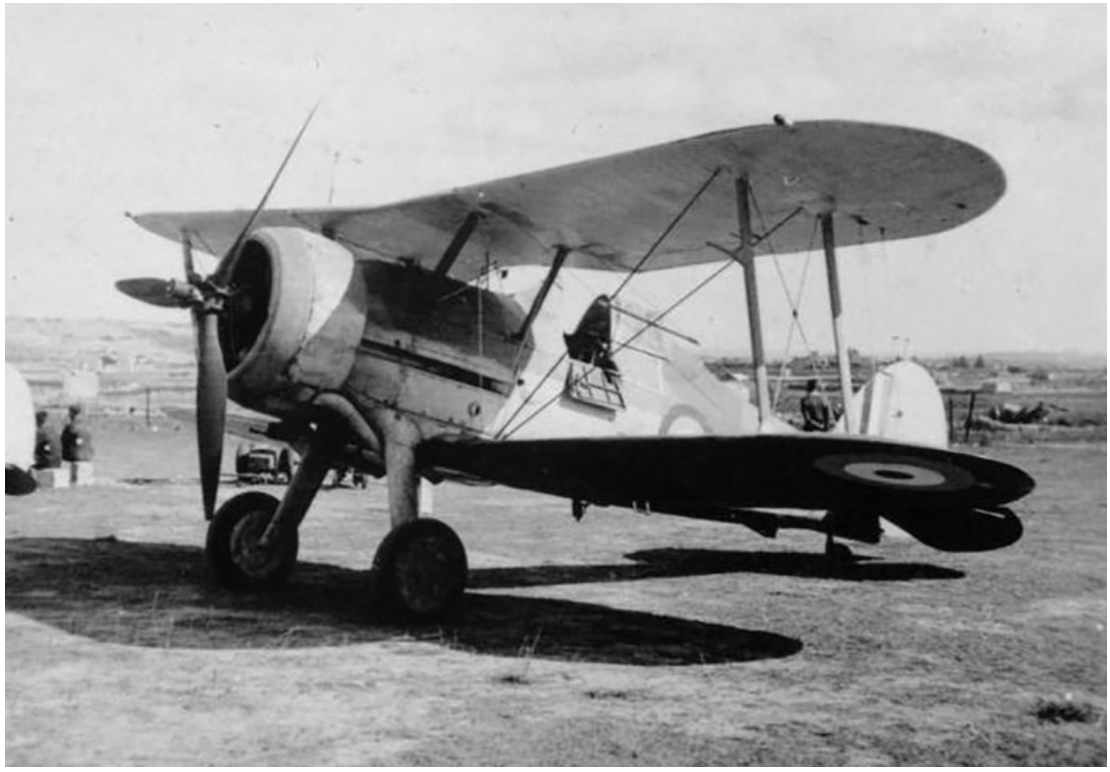

Initially, Malta had only three obsolete 1934 Gloster Gladiator biplanes to mount a defense, still in their original packing crates. Flown by volunteer pilots, they came to be known as “Faith, Hope, and Charity.”

The three planes held the Italians at bay, shooting down the slower bombers in droves. As my Italian grandmother constantly reminded me, “Italians are better lovers than fighters.” By the time the Germans showed up, the RAF had been able to resupply Malta with as many as 50 infinitely more powerful Spitfires a month, and the battle was won.

So Malta it was.

The flight school only had one plane they could lend me for ten days, a clapped-out, underpowered single-engine Grumman Tiger, which offered a cruising speed of only 160 miles per hour. I paid extra for an inflatable life raft.

Flying over the length of France in good weather at 500 feet was a piece of cake, taking in endless views of castles, vineyards, and bright yellow rapeseed fields. Italy was a little trickier because only four airports offered avgas, Milan, Rome, Naples, and Palermo. Since Italy had lost the war, they never experienced a postwar aviation boom as we did.

I figured that if I filled up in Naples, I could make it all the way to Malta nonstop, a distance of 450 miles, and still have a modest reserve.

Flying the entire length of Italy at 500 feet along the east coast was grand. Genoa, Cinque Terra, the Vatican, and Mount Vesuvius gently passed by. There was a 1,000-foot-high cable connecting Sicily with the mainland that could have been a problem, as it wasn’t marked on the charts. But my US Air Force charts were pretty old, printed just after WWII. But I spotted them in time and flew over.

When I passed Cape Passero, the southeast corner of Sicily, I should have been able to see Malta, but I didn’t. I flew on, figuring a heading of 190 degrees would eventually get me there.

It didn’t.

My fuel was showing only a quarter tank left and my concern was rising. There was now no avgas anywhere within range. I tried triangulating VORs (very high-frequency omnidirectional radar ranging).

No luck.

I tried dead reckoning. No luck there either.

Then I remembered my WWII history. I recalled that returning American bombers with their instruments shot out used to tune in to the BBC AM frequency to find their way back to London. Picking up the Andrews Sisters was confirmation they had the right frequency.

It just so happened that buried in my pilot’s case was a handbook of all European broadcast frequencies. I looked up Malta, and sure enough, there was a high-powered BBC repeater station broadcasting on AM.

I excitedly tuned in to my Automatic Direction Finder.

Nothing. And now my fuel was down to one-eighth tanks and it was getting dark!

In an act of desperation, I kept playing with the ADF dial and eventually picked up a faint signal.

As I got closer, the signal got louder, and I recognized that old familiar clipped English accent. It was the BBC (I did work there for ten years as their Tokyo correspondent).

But the only thing I could see were the shadows of clouds on the Mediterranean below. Eventually, I noticed that one of the shadows wasn’t moving.

It was Malta.

As I was flying at 10,000 feet to extend my range, I cut my engines to conserve fuel and coasted the rest of the way. I landed right as the sun set over Africa.

While on the island, I set myself up in the historic Excelsior Grand Hotel. Malta is bone dry and has almost no beaches. It is surrounded by 100-foot cliffs. I paid homage to Faith, the last of the three historic biplanes, in the National War Museum in Valetta.

The other thing I remember about Malta is that CIA agents were everywhere. Muammar Khadafy’s Libya was a major investor in Malta, recycling their oil riches, and by the late 1980s owned practically everything. How do you spot a CIA agent? Crewcut and pressed, creased blue jeans. It’s like a uniform. What they were doing in Malta I can only imagine.

Before heading back to London, I had to refuel the plane. A truck from air services drove up and dropped a 50-gallon drum of avgas on the tarmac along with a pump. Then they drove off. It took me an hour to hand pump the plane full.

My route home took me directly to Palermo, Sicily to visit my ancestral origins. On takeoff to Sardinia, wind shear flipped my plane over, caused me to crash, and I lost a disk in my back.

But that is a story for another day.

Who says history doesn’t pay!

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

“Faith”

The Andrews Sisters

Spitfire

Grumman Tiger

https://www.madhedgefundtrader.com/wp-content/uploads/2024/04/andrews-sisters.png582506april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-04-22 09:02:302024-04-22 12:00:50The Market Outlook for the Week Ahead, or Facing Harsh Reality

(MARKET OUTLOOK FOR THE WEEK AHEAD, or VOLATILITY IS BACK!)

(REMEMBERING TRINITY)

(TLT), (TSLA), (NVDA), (FCX),

(XOM), (WPM), (GLD), (FXI), (FXY), (USO), (GOOGL)

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.