“Technology is a useful servant but a dangerous master.” - Said Norwegian Historian Christian Lous Lange

“Technology is a useful servant but a dangerous master.” - Said Norwegian Historian Christian Lous Lange

Mad Hedge Technology Letter

July 30, 2021

Fiat Lux

Featured Trade:

(THE BEST WAY TO STREAMLINE YOUR TECH PORTFOLIO)

(MU), (PLTR), (AMD), (AMZN), (SQ), (PYPL)

Overperformance is mainly about the art of taking complicated data and finding perfect solutions for it. Trading in technology stocks is no different.

Investing in software-based cloud stocks has been one of the seminal themes I have promulgated since the launch of the Mad Hedge Technology Letter way back in February 2018.

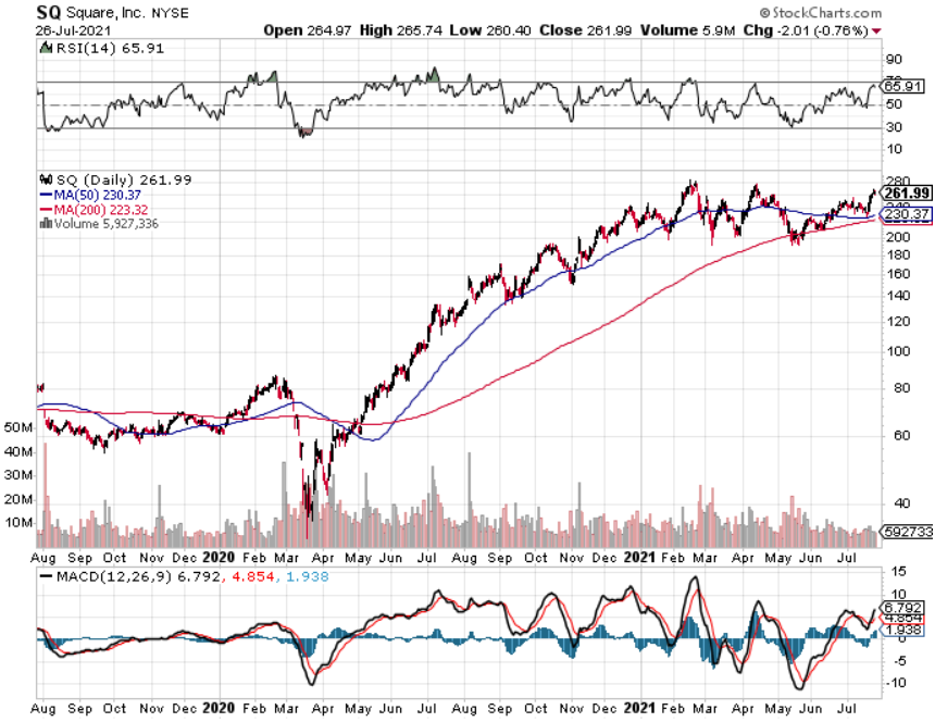

I hit the nail on the head and many of you have prospered from my early calls on AMD, Micron to growth stocks like Square, PayPal, and Roku. I’ve hit on many of the cutting-edge themes.

Well, if you STILL thought every tech letter until now has been useless, this is the one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, I have a quick fix for you and your friends.

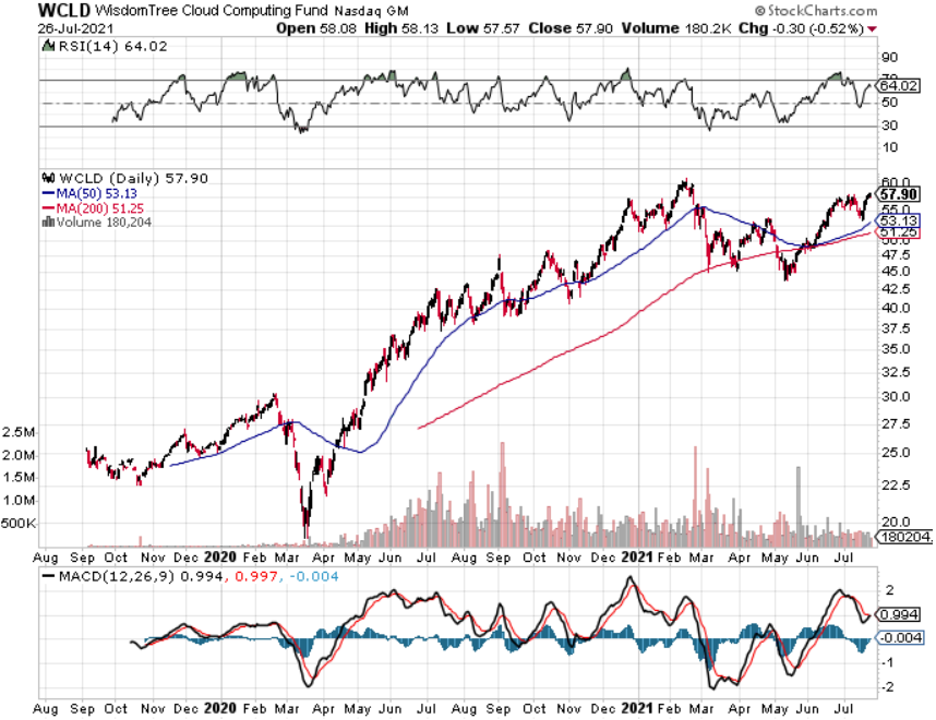

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

Yes, something like this does exist and we have been chronicling the development of the cloud since this tech letter’s launch.

The cloud is the concept powering the “shelter-at-home” trade which has been hotter than hot since March 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge of overwhelming the rest of the business world due to advancements in artificial intelligence and the Internet of Things (IoT) hyper-improving efficiencies.

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry.

Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise and often manually. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Speed, Ease, and Low Cost of Implementation – cloud software is installed via a network connection; it doesn’t require the higher cost of on-premise infrastructure setup maintenance, and installation.

Efficient Software Updates – upgrades and support are deployed via a network connection, which shifts the burden of software maintenance from the client to the software provider.

Easily Scalable – deployment via a network connection allows cloud SaaS businesses to grow as their units increase, with the ability to expand services to more users or add product enhancements with ease. Client acquisition can happen 24/7 and cloud SaaS companies can easily expand into international markets.

Business Model Advantages

High Recurring Revenue – cloud SaaS companies enjoy a subscription-based revenue model with smaller and more frequent transactions, while traditional software businesses rely on a single, large, upfront transaction. This model can result in a more predictable, annuity-like revenue stream making it easy for CFOs to solve long-term financial solutions.

High Client Retention with Longer Revenue Periods – cloud software becomes embedded in client workflow, resulting in higher switching costs and client retention. Importantly, many clients prefer the pay-as-you-go transaction model, which can lead to longer periods of recurring revenue as upselling product enhancements does not require an additional sales cycle.

Lower Expenses – cloud SaaS companies can have lower R&D costs because they don’t need to support various types of networking infrastructure at each client location.

I believe the product and business model advantages of cloud SaaS companies have historically led to higher margins, growth, higher free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must satisfy critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device, or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based, or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD component are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 100% from the nadir we saw in March 2020 and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many tech portfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a pure play on cloud computing software, because they do have other hybrid-sort of businesses, but the elements of its cloud business are nothing short of brilliant.

ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So, you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more chutzpah because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger precisely because they take advantage of the law of small numbers.

One stock that has the chance for a legitimate 10-bagger is my call on Palantir (PLTR).

Palantir is a tech firm that builds and deploys software platforms for the intelligence community in the United States to assist in counterterrorism investigations and operations.

This is one of the no-brainers that procure revenue from Democrat and Republican administrations.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a tech portfolio to target those extraordinary, extra-salacious tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner, and don’t forget about PLTR while you’re at it.

“When we launch a product, we're already working on the next one. And possibly even the next, next one.” – Said Current CEO of Apple Tim Cook

Mad Hedge Technology Letter

July 28, 2021

Fiat Lux

Featured Trade:

(THE REAL RULES OF TECH)

(MSFT), (FB), (GOOGL), (AAPL), (AMZN), (NFLX), (TSLA)

Northern Californian tech companies stopped innovating because of the monopolistic nature of current business models that nestle nicely in unfettered capitalism.

They only go by one principle these days – to crush anything remotely resembling competition and they are damn good at doing it.

This has been going on in Silicon Valley for years and the government has turned a blind eye since the beginning of it.

The end result is the absence of competition.

At a higher tech level, the strong get stronger by stockpiling cash and resources, all while taking advantage of historically low rates to finance their growth models.

Why does the U.S. government largely sit on the sidelines and act if nothing has really happened?

If I deploy the concept of Occam's razor to this situation, a philosophical rule that entities should not be multiplied unnecessarily which is interpreted as requiring that the simplest of competing theories be preferred, my bet is that most of U.S. Congress own stock portfolios, even if they are the index variety, and these portfolios are spearheaded by the likes of Apple (AAPL), Facebook (FB), Amazon (AMZN), Google (GOOGL), Microsoft (MSFT), Netflix (NFLX), and of course Tesla (TSLA).

This has come into the open frequently with members of Congress even front-running the March 2020 sell-off with their own portfolios like U.S. senator Kelly Loeffler from Georgia selling $20 million in stock after attending special intelligence briefings in the weeks building up to the coronavirus pandemic.

We definitely don’t get invites to those special intelligence briefings, but Loeffler getting off scot-free by mainly just playing down what she did proves the immunity that politicians accrue from their lofty positions.

It’s a direct conflict of interest, but that's not surprising for politics in 2021 and I would say it epitomizes the era we are in.

It’s also why Congress hasn’t acted on Silicon Valley’s excessive abuse of power, which is so glaringly blatant that excuses must be crafted just to make it seem they aren’t as bad as they are.

The government likes to jawbone to the public saying they will make competition a level playing field, but actions show they are doing the opposite.

Ultimately, Silicon Valley whispers in the ear of Congress and they listen.

Well, what now?

Tech has now turned mostly into a digital marketing lovefest harnessed around the smartphone and tablet with cheap shortcuts which is partly why the efficacy of the internet has dropped greatly.

The advent of 5G has also been a bust because these titans don’t feel the need to reinvest to make that killer 5G app when they don’t need to.

The truth is Silicon Valley couldn’t be more complacent in 2021.

They are the ultimate corporate entity and more monolithic than ever.

Smart CFO’s are continuing the gravy train by diving deep into stock buybacks to boost stock prices and the dividends are the extra kicker.

The iPhone maker repurchased $19 billion of stock in the first quarter, bringing the total for the past fourth quarters to $77 billion.

GOOGL repurchased a record $11.4 billion of stock in the first quarter, up from $8.5 billion a year earlier, and FB bought back $3.9 billion, triple the total a year ago.

Now, they even got the White House to do their dirty work.

Huawei, the Chinese telecom company, has been the punching bag for the White House’s tech war with China.

In remarks to reporters in March 2019, Chinese politician Guo Ping said, “The U.S. government has a loser’s attitude. They want to smear Huawei because they can’t compete with us.”

Let’s get this straight, U.S. tech was never behind China and still isn’t, but I do believe the U.S. should simply outcompete with Huawei because I know they can and have the capacity to do so.

China hasn’t done much with 5G as well aside from amassing the patents, but they haven’t made it quite practical to the Chinese public as a use case for consumer products.

Instead of competing, we have Facebook tapping the political back channels to encourage the U.S. government to ban TikTok, not because it threatens Facebook’s model but because Facebook is concerned about national security.

This is from the same Mark Zuckerberg that has been attempting to destroy Snapchat (SNAP) for years after SNAP’s CEO Evan Spiegel refused to sell it to Zuckerberg.

So why innovate? Why deploy capital into research and development when you can just nick a crown jewel and make it your own?

Exactly, so innovation does not happen and will not happen.

We, as consumers, have been thrust into the cluster of ever-degrading smartphone apps that offer less and less utility.

But ultimately, even if you hate Silicon Valley at a personal level, it is literally impossible to bet against them, because all this posturing behind the scenes does boost the share price and that’s what this technology letter is about.

As we are whipsawed into this muddling world of partially vaccinated economies, tech will consolidate after they deliver earnings only to prepare for the next leg up in shares.

Sure, this year’s growth and EPS estimates have been priced perfectly, but we will start to move onto next years’ bounty and these models have never been more profitable.

Don’t fight the trend.

“A good boss is better than a good company.” – Said Founder of Alibaba Jack Ma

Mad Hedge Technology Letter

July 26, 2021

Fiat Lux

Featured Trade:

(YOUR NEW FULFILLMENT CENTERS)

(AMZN), (WMT), (TGT)

Mad Hedge Technology Letter

July 23, 2021

Fiat Lux

Featured Trade:

(NEURALINK WILL CHANGE THE WORLD AND YOUR BRAIN)

(TSLA), (SPACEX), (NEURALINK), (BORINGCOMPANY)

Founder of Tesla Elon Musk is on record confessing that it would be a “good idea” to bring his four businesses — Tesla, SpaceX, Neuralink, and The Boring Company — under a giant holding company.

Doing this would encourage more talented engineers to work for Musk and allow the four companies to combine human resources and marketing departments.

The synergies would be countless.

Most of you know three of the four, so let me explain to you about Neuralink.

In short, Neuralink Corporation is an American neurotechnology company developing implantable brain-machine interfaces.

You would think this is straight out of science fiction, but mark my word that in our lifetime, we could all be operating digital devices from our heads if Musk gets his way.

And he often does get his way.

Scary as it seems now, this will probably be the first of many artificial intelligence procedures to infuse humans with layers of artificial intelligence.

Musk believes humans will go the way of robot hybrid in the future because the natural development of competition is trending in that way and sadly, this direction in humanity is ultimately existential for every one of us.

Improvements in technology will periodically be announced and iterations will need to be adopted because software is upgraded.

Fortunately, we are nowhere close to the actual implementation of these neuro devices let alone trying to analyze the consumer and economic implications of this technology.

As for today and now, we are in the early innings and testing it out on pigs.

Better them and not me.

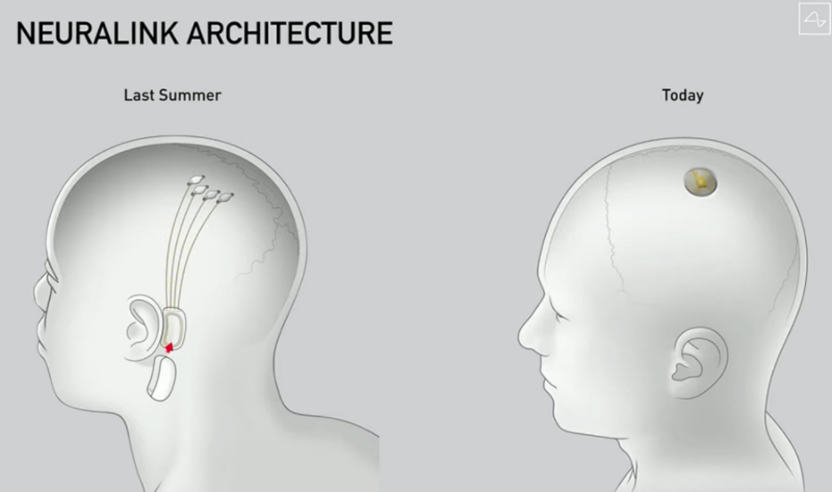

Neuralink’s dramatically simplified design for an implant that hopes to create brain-to-machine interfaces is a big deal and partly because of the star power backing the project that can literally move mountains.

The previous design consisted of a bean-shaped device that would sit behind the ear, but now it is the size of a large coin, and it goes in your skull.

I expect the final iteration to be a millimeter wide.

The in-brain device could enable humans with neurological conditions to control technology, such as phones or computers, with mere thoughts.

The other use case is solving neurological disorders from memory, hearing loss, and blindness to paralysis, depression, and brain damage which is a tad more altruistic.

The current prototype – referred to as version 0.9 – measures 23 millimeters by eight millimeters, and has 1024 electrode "threads" attached to it that are implanted into the brain.

It is designed to replace a coin-sized portion of the skull and sit flush so it would be physically unnoticeable. It would be inductively charged the same way you would wirelessly charge a smartwatch or a phone.

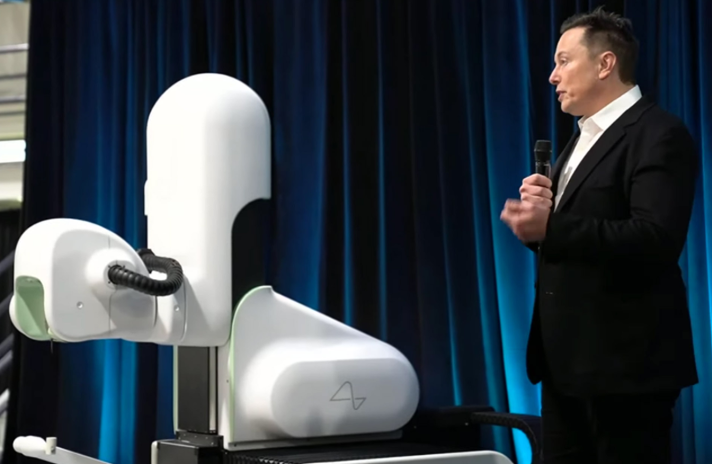

The surgical robot, which is programmed to insert the neural threads safely into the brain, was done by US design company Woke Studios.

Woke Studio’s robot would be able to insert the link in under an hour without general anesthesia, with the patient able to leave the hospital right away.

The robot will eventually do the entire surgery – so everything from the incision, removing the skull, inserting electrodes, placing the device, and then closing things up.

It will be completely automated.

Test pigs are being used to test the device which offers important insights into the process of inserting a chip into a brain.

The implant sends real-time signals from the pig’s brain whenever it touches something with its snout.

Described as "healthy and happy", one of the pigs demonstrated that it is possible to have multiple chips in your head at one time.

Musk also showed a pig that previously had a chip inserted into its brain, but had since been removed, to show that the procedure is reversible without any serious side effects.

Neuralink’s Breakthrough Device designation by FDA supports Musk’s neuroscience objectives. The startup is now preparing for its first human test case, pending required approvals, and further safety testing.

If this technology is green-lighted by the U.S. Federal Government, I envision a free for all into this technology from the likes of Facebook, Google, Apple, and Microsoft, and so on.

If you thought website “cookie tracking” is bad now, then once tech firms are granted access to consumers’ brains, it could open up a pandora's box of moral conflicts of interest, an avalanche of revenue opportunities, and lawsuits galore.

Look at the hesitation and disgruntlement of the health industry hoping to convince Americans to take two jabs of an mRNA vaccine in the arm and now think about trying to convince Americans to implant a brain in their head for the sake of competing.

Will American society really get to the point where Facebook is selling your “thoughts” to neural advertisers?

It’s scary to think about but that is the direction we are headed down for better or worse.

If you view this through the lens of big tech, battering down the hatches to get access to consumer’s “thoughts” is the holy grail of access points and revenue flow.

In 2021, humans still need to digest thoughts and carry out functions through fingers into a phone interface.

We have also allowed big tech into our home feeding them data through smart devices and virtual assistants like Amazon Alexa.

Getting rid of all that “fluff” and extracting data and behavioral results from the original source is potentially worth over 10 trillion dollars along with a recurring revenue source to infinity.

Not only will physical devices be useless at that point, but they will also spawn a mega cloud storage business that is hooked straight to the mind.

An economic analyst can digest how cloud companies like Amazon and Google would rake in the trillions by storing libraries of data that a mind can tap in at any time.

It really is a gigantic step that will digitize and computerize humans - big tech is first in line to reap the profits and literally control our brains.

Maybe by that time, the government will actually lift a finger and regulate since the current crop of Baby Boomers still have no idea what Facebook does and have been turning a blind eye.

This is the future – a future where we coexist with artificial intelligence.