Mad Hedge Technology Letter

May 28, 2021

Fiat Lux

Featured Trade:

(THIS CUTTING-EDGE CHIPS STOCK IN HYPERGROWTH MODE)

(NVDA)

Mad Hedge Technology Letter

May 28, 2021

Fiat Lux

Featured Trade:

(THIS CUTTING-EDGE CHIPS STOCK IN HYPERGROWTH MODE)

(NVDA)

Nvidia (NVDA) is another multilayered business with revenues coming from east and west and basically everywhere and really at a time when the gaming market is the largest ever.

Let’s make this clear: Nvidia isn’t a gaming stock, but its best business is centered around the secular gaming trend.

They have this massive installed base of GeForce users (Nvidia branded graphics processing units).

They have reinvented computer graphics as well as resetting the install base — created a pipeline of profits that take advantage of the boom in gaming which many as you know went gangbusters because of the shelter-at-home conditions.

There has been substantial development on the gaming front — at a time when gaming market is expanding fast, and peeling back the layers it sports — eSports — it's infused into art.

It is infused into social.

And so, gaming has such a large cultural footprint now, even to the point that it’s the largest form of entertainment in the world.

The emphasis of this experience is going to resonate for the long term and not only that, the phenomenon called crypto — Nvidia’s Crypto graphic cards named CMP will funnel GeForce supply to gamers.

The Nvidia CMP 30HX is a dedicated crypto mining card. The CMP 30HX is essentially a mid-range graphics card powered by Nvidia’s TU116 processor.

There is strong demand for this product, and I expect to see elevated sales for quite some time because of the dynamics of crypto and the avalanche of capital gravitating towards it not only institutional but from retail too.

And hopefully, in the combination of gaming, crypto, and data, Nvidia is primed to experience strong growth in core businesses through the year.

The data backs up Nvidia’s ambition with Q1 exceptionally strong with revenue of $5.66 billion and year-on-year growth accelerating to 84%.

They set a record in total revenue in Gaming, Data Center, and Professional Visualization, driven by their best product lineups and structural tailwinds across our businesses.

Starting with Gaming, revenue of $2.8 billion was up 11% sequentially and up 106% from a year earlier.

Channel inventories are still leading and Nvidia expects to remain supply-constrained into the second half of the year.

Now Laptops continue to drive strong growth this quarter with all major PC original equipment manufacturers (OEM) launching GeForce RTX 30 Series laptops based on the 3080, 3070, and 3060, as part of their spring refresh.

This is the largest ever wave of GeForce gaming laptops, over 140 in total as OEMs address the rising demand for gamers, creators, and students for NVIDIA's powered laptops.

They believe gaming also benefited from crypto mining demand, and Nvidia is separately addressing mining demand with cryptocurrency mining processors or CMPs.

The crypto CMP revenue was $155 million in Q1, reported as part of the OEM and other category. And our Q2 outlook assumes CMP sales of $400 million.

Data Center continues to be a growth driver with revenue topping $2 billion for the first time, growing 8% sequentially and up 79% from the year-ago quarter, which did not include acquisition Mellanox.

And then lastly, supercomputing; supercomputing centers all over the world are building out and Nvidia is in a great position to fuse together time simulation-based as well as data-driven-based approaches, which are called artificial intelligence.

Across the board, data center is gaining momentum and is the largest segment of computing and will continue to train deep neural networks with rising computational intensity led by two of the fastest growing areas of AI; natural language understanding.

Demand is booming across Nvidia’s markets and readers can expect increase in CMP, but they still expect the lion share of growth to come from Data Center and Gaming.

In Data Center business, their product lineup couldn't be better and they have a strong overall portfolio both for training and inferencing and they are experiencing strong demand across hyperscales and vertical industries.

The foundation has been laid to be a three-chip data center scale computing company with GPUs, DPUs and CPUs.

Fortunately for Nvidia, AI is the most powerful technology force of our time.

Nvidia partners with cloud and consumer Internet companies to scale out and commercialize AI-powered services.

They are democratizing AI for every enterprise and every industry.

With pre-trained models for conversational AI, language understanding, recommender systems, and broad partnerships across the IT industry, Nvidia is removing the barriers for every enterprise to access state-of-the-art AI.

From gaming, metaverses, cloud computing, AI, robotics, self-driving cars, genomics, computational biology, Nvidia is engaging in important work and innovating in the fastest-growing markets today.

Now to look at our outlook for Q2, revenue is expected to be $6.3 billion, and remember that the prior year when Q2 revenue was $3.87 billion.

This company is mesmerizing, growing from $11 billion in annual revenue to $16.68 billion in just one year says it all.

Growing revenue in the mid-80% means it will easily surpass the $9 billion in the first two quarters of the year paving the way for an almost $20 billion per year business.

Sure it’s not Apple or Microsoft but for what it does, they are best in show in an industry that is going through a massive supply headwinds.

The quarterly performance only reinforces the thesis that chip companies are a great place to allocate funds to and the support is there for a buy the dip investor attitude because of growing EPS which promotes share buy backs and capital returns to shareholders.

It’s hard to believe that investors could put their money elsewhere because tech still secures the vast majority of earnings in the business world and that train isn’t slowing down and the bullet train is clearly the chip sector in 2021.

“One machine can do the work of fifty ordinary men. No machine can do the work of one extraordinary man.” - Said American Writer Elbert Green Hubbard

Mad Hedge Technology Letter

May 26, 2021

Fiat Lux

Featured Trade:

(SHOULD READERS DIP BACK INTO AIRBNB AT $135?)

(ABNB)

Airbnb (ABNB) was disproportionately affected by the public health crisis because tech firm relies on travelers booking accommodation on their platform which they pocket a substantial commission.

To learn they only lost revenue of 22% over the past year was quite extraordinary because it could have been worse.

Looking forward, this is an intriguing stock that is trading around $135 today which is a more reasonable valuation from the $220 it was trading at after its direct listing.

I am net positive on Airbnb because the business is dramatically improving with the rollout of vaccines and the easing of some travel restrictions.

While conditions aren’t back to what they were, they are improving.

People's desire to travel combined with tightly managed expenses drove a return to positive top-line growth and materially improved adjusted EBITDA last quarter when Airbnb did quarterly revenue of $887 million.

It was an increase of 5% year over year, and it exceeded Q1 2019 levels as well.

Their business improved without the recovery of two of the strongest historical segments: urban travel and cross-border travel.

They expect the return of urban and cross-border travel to be significant tailwinds over the coming quarters.

What are some of the new trends from the travel data?

Travelers are visiting smaller cities, towns, and rural communities. And when people do travel, they’re staying longer. 24% of nights booked in Q1 were for stays of 28 nights or longer. People are not just traveling in Airbnb, they’re now living on Airbnb.

In New York City, in Los Angeles, they had almost as many nights booked for stays longer than 28 days as they had stays under 28 days.

Why do I see sustained health in this business?

Listing growth has stayed strong with more than 5.6 million listings which is more than 1 million more than they had this time in 2019.

The growth is in nonurban listings.

Their host churn in Q1 is actually lower than host churn in the same period in 2019.

The 30% growth in nonurban and vacation rental listings is a harbinger for growth to come and shows that Airbnb was able to build out more capacity for the future travel mania once borders open up.

One interesting thing to note is that business travel appears to be never coming back because many employees are working remotely. They're going to need to go back to headquarters occasionally. You're going to see longer stays going in cities and accessing offices in a hybrid sort of way.

But the bigger trend is going to be flexibility. I think that most of us working around the world if we are privileged enough to say this, are more flexible than we were before the pandemic. Because the world of Zoom means a world where we can work anywhere, it is a world where many people are also choosing to live anywhere.

As hosts begin to ramp up for the summer travel season, Airbnb is seeing Average Daily Rates (ADRs) in Q1 up 35% year over year. That was after being up 13% year over year in Q4. But the year-on-year comparable data were up against March 2020 that had a catastrophic performance.

Right now, 80% of nights booked in Q1 were domestic, and with domestic travel being consistent is now the main strength all around the world.

The rebound has been drastically earlier in the U.S., which has a higher average daily rate.

The incremental growth is in the non-urban single-family home and even larger homes, and those are just, on average, a higher ADR because bigger homes go for higher prices.

The problem I have is that the business model has changed away for this cash cow of cross-border travel where it used to be 50% of total nights were cross-border nights.

International travelers are usually willing to pay a premium when they go to different countries compared to domestic travelers who understand the local pricing better.

If net cross-border nights don’t come back to pre-2020 numbers, and I don’t think they would completely, it’s clearly a net negative for the company.

Management has kept saying, “Our model is inherently adaptable”, yet what is the game plan if the blur between work and life corresponds to more 6-month and 1-year leases signed which would cut out the need for Airbnb?

Is Airbnb so adaptable they can slug it out in the property management business?

Management kept saying that trends are a “little hard to pinpoint” but it's clear that if these 28 days or more stayers get more comfortable with a location and start dabbling more with long-term leases or even long-term property ownership, or might I even say, for the elite to purchase multiple vacation homes, then the use case for using Airbnb is minimized greatly.

What I understood from this public health crisis is that consumers have become a great deal savvier in how they allocate money to housing and that means vacation housing too along with what they demand and expect from it.

This new machination inherently means that servicers and listings will need to increase the quality of their listings since workers who work from home will be living in the home more and not just drop their bags upon entrance and go to the beach for a day or 2.

Many listings have incomplete kitchen equipment and the lowest option internet and other ugly shortcuts.

Yes, I do believe there will be a revision to the mean via the “tailwind to urban travel and cross-border” but that mean has a lower ceiling than before 2020 which will cap the underlying shares’ potential appreciation.

I also believe that non-urban, suburban homes won’t be able to meet capacity for the U.S. demand because of HOA rules and stringent enforcement of them. Just read about the Lake Tahoe ordinances to get a little flavor about how difficult it is to put Airbnb places where they don’t fit naturally. It’s easier to get away with it in big cities when entire buildings and even blocks are Airbnb investment properties, but not in suburbia.

Travel will come back hardcore and even 8% of Google search today is travel-related.

I do believe Airbnb is a good stock to buy right now, but the world has forever changed, and their business model has been damaged by it.

I’ll go for the low-hanging fruit now in Airbnb, but their growth story has been in fact pulled backwards instead of forward, and that wasn’t supposed to happen to “tech” companies.

That being said, they are good for a short-term trade today, but I would have said it was a buy-and-hold before the pandemic.

Enjoy this recovery story but remember to take profits when momentum fizzles out.

“The Internet is so big, so powerful and pointless that for some people, it is a complete substitute for life.” - Said English Journalist Andrew Brown

Mad Hedge Technology Letter

May 24, 2021

Fiat Lux

Featured Trade:

(THE MOST UNIQUE SOFTWARE COMPANY TODAY)

(MSTR)

Here is an interesting “software” company for you.

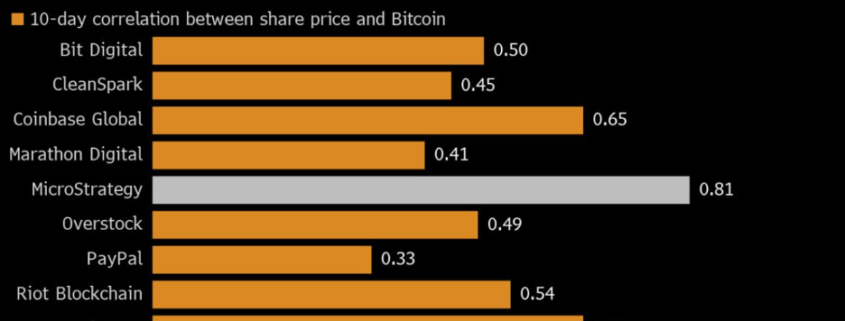

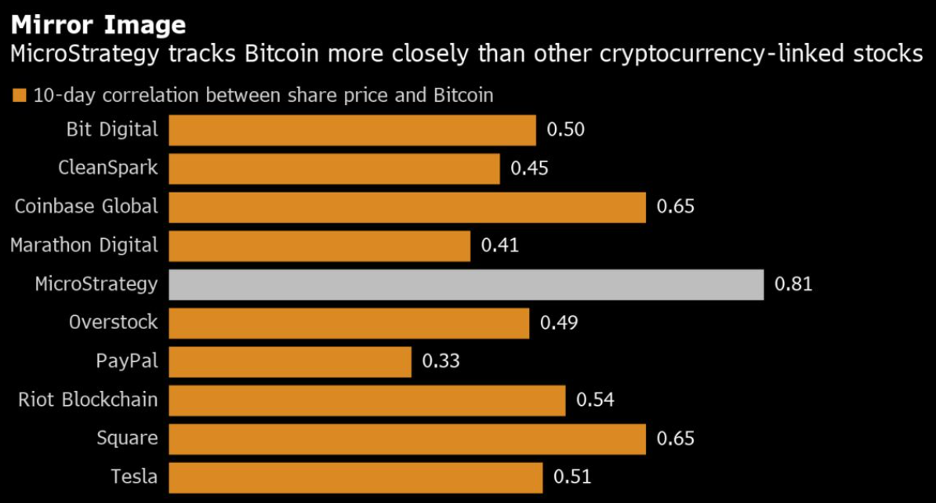

MicroStrategy Inc. (MSTR) is a tech company offering business intelligence, mobile software, and cloud-based services but is it really?

From last year, they have transformed into a de-facto bitcoin proxy because of a relatively progressive strategy of pouring their financial resources into the digital gold asset Bitcoin.

Sure, when riding high, it looks great on the balance sheet, but don’t get me wrong, this is a high-risk proposition for a tech firm that is supposed to be selling business intelligence software.

We all like short-cuts and this is the mother of them as the CEO of MicroStrategy Michael J. Saylor hatched a plan to leapfrog the crowded software scene to make a name for himself.

This is definitely an indictment on smaller software companies showing their plight. It’s not easy competing against the big boys.

In 2017, when the firm had no Bitcoin strategy, MicroStrategy earned $504 million in total annual revenue.

Fast forward to 2020, they did $481 million in revenue.

That is terrible.

A company this small and flaccid isn’t going to find an incremental buyer when they are contracting total revenue.

The game just doesn’t work like that.

It’s plausible to say that Saylor was in desperate straits and his reach for an ultra-high risk, high reward strategy has paid off handsomely so far.

If we roll the clock back a year ago, MSTR had approximately $500 million of cash assets and no expectation of any investment gain from alternative assets.

And as of their earnings report, they had $5 billion in Bitcoin assets, but more like around $2.5 billion today.

If Bitcoin grows, the company is going to benefit, the shareholders will benefit.

Clearly, if you’re a MicroStrategy shareholder and you have a negative sentiment on Bitcoin, then MSTR is not the right company for you, but if you have a positive sentiment about where Bitcoin is headed, it’s worth a look.

MSTR has aligned its balance sheet and shareholders' interests with that sentiment.

Not only does MicroStrategy benefit from the profitability of bitcoin, but they are parlaying it into favorable debt issuances like the past quarter’s convertible debt issuance.

From a revenue standpoint, total revenues in the quarter grew 10% year-over-year which is the strongest quarterly performance in five years, and it beats negative growth.

The prior years’ comp was an easy year over year beat and MSTR was up 69% in perpetual license revenue, and on the cloud side, they were up 26% year over year, and cloud billing is up 19% year over year.

These metrics are some of the best they’ve had in history, and I would say we’ve seen growth because the existing customer base is primarily large enterprises and many are still buying on-prem and obviously, MSTR is not going to turn that down.

The second key factor is they are actively moving people off of perpetual maintenance and moving them to term licenses, which will show up in product license revenue.

HyperIntelligence continues to be an important entrée into new customers and as an important indication to customers of new product innovation. MSTR’s SaaS version of HyperIntelligence has seen increased adoption, as well as serving the foundation of future enterprise business intelligence (BI) SaaS offerings.

That’s great that their business intelligence software is growing 10% year-over-year but it’s their Bitcoin acquisition strategy in the first quarter that is making headlines.

MSTR completed a second convertible notes offering, this time selling $1.05 billion in aggregate principal of notes, and got even better terms than their first convertible notes offering with a 0% coupon and 50% conversion premium.

With this new capital, on April 5, 2021, they announced the purchase of an additional 253 Bitcoins for $15.0 million at an average price of approximately $59,339 per Bitcoin, inclusive of fees and expenses. On April 12, 2021, they announced that going forward, non-employee directors will receive all fees for their services on the company's board in Bitcoin instead of cash.

Before that, they acquired an additional 19,452 Bitcoins for $1.026 billion or approximately $52,765 per Bitcoin. Overall, in the first quarter, they purchased 20,857 Bitcoins for $1.086 billion or $52,087 per Bitcoin and ended the quarter holding 91,326 Bitcoins at an average price of $24,214.

The company estimate that current market value Bitcoin holdings now exceeds $5 billion, including $3.1 billion of unrealized gains, but that amount has halved since Bitcoin sold off.

Management has said they plan “to deploy additional capital into our Bitcoin acquisition strategy.”

I understand they are doing a little “Elon Musk-esque” dip into Bitcoin to gentrify their balance sheet, but what I see is MSTR buying up Bitcoin no matter what the price is even up to the latest peak of around $60,000.

That’s borderline irresponsible.

I get it that their Bitcoin commitment has elevated their brand dramatically in the world and the Bitcoin community is adding something of the order of 10 million people a month, perhaps even more millions a week.

But, and it’s a big but, management shouldn’t be blindly buying up bitcoin with borrowed money at any price.

It’s hard to believe there is no nuance to this strategy.

Aggressively buying Bitcoin with guns blazing is a fool’s game and the balance sheet could get wrecked if Bitcoin has a few bad weeks and drops down to $10,000 which is entirely plausible.

For me, this wreaks of their core products not being able to viably compete with high quality business intelligence products.

I agree that MSTR has a real product, this isn’t a pump and dump scheme, but shareholders really need to question what management is thinking by pouring more capital into Bitcoin at $59,000.

Why not use the debt issuance to build better core products to win more long-dated contracts?

At $59,000, there is a higher chance in the short-term that Bitcoin will retrace to $40,000.

MicroStrategy shareholders must ask themselves at what price will MSTR not buy Bitcoin. I would love to hear that answer.

Especially when investors have seen the asset fringes blow up like the weakness in SPACs and perceived inflation scares running riot all over the news wires.

The stock hit a high of $1,272 in the beginning of February and is down 300% from the peak today which is still 300% higher than where it was before the Bitcoin mania hit in mid-2020.

Got all that?

So again, everything is relative, and I wouldn’t touch this one unless it reverts back to $300 where there is technical support which would mean a substantial drop in Bitcoin from the current price today.

“In the startup world, you're either a genius or an idiot. You're never just an ordinary guy trying to get through the day.” – Said Venture Capitalist Marc Andreessen

Mad Hedge Technology Letter

May 21, 2021

Fiat Lux

Featured Trade:

(THE STRENGTH OF AMD)

(AMD), (INTC), (TSM), (XLNX), (SMH)