“Technology is a useful servant but a dangerous master.” - Said Norwegian historian, teacher, and political scientist Christian Lous Lange

“Technology is a useful servant but a dangerous master.” - Said Norwegian historian, teacher, and political scientist Christian Lous Lange

Mad Hedge Technology Letter

May 12, 2021

Fiat Lux

Featured Trade:

(THE EXPLODING PROGRAMMATIC AD SPACE)

(TTD)

Annual advertising budgets are often being reset and reconsidered in Q1, but as the economy is roaring back, digital ad deliverers are set to make hay.

The Trade Desk (TTD) specializes in programmatic ad buying.

What is it?

It’s the deployment of software to buy digital advertising.

Previously, the traditional way included requests for proposals, tenders, quotes, and human negotiation, but programmatic buying uses machines and algorithms to purchase display space.

Humans now have more time for the optimization and evolution of ads.

Ad agencies will always need to optimize advertising to meet consumers’ needs on a deeper level.

Programmatic-centric software will deliver a better set of tools to plan, optimize and target advertising effectively.

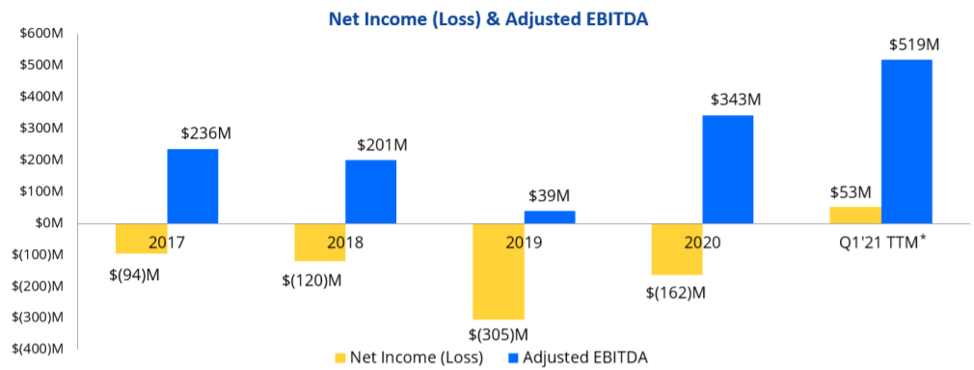

Since TTD doesn’t make anything physical, margins are usually a lot higher and that certainly showed with Q1 producing adjusted EBITDA of a record $70.5 million.

This Q1 record is on both an absolute basis and a percentage of revenue basis.

As TTD continues to grow and represent more large brands and a larger percentage of ad agencies' brands, they will continue to become an accurate bellwether for the open Internet and advertising spend.

When you consider their performance in the context of the health of the overall advertising industry, you can see how they continue to outperform the industry and gain market share.

WPP's GroupM predicts worldwide advertising revenue will increase 10% in 2021. Publicis Groupe's Zenith expects overall U.S. ad spending to rise 3.2% in 2021, following a drop of 5.4% last year. GroupM also predicts digital advertising will surge 14% to nearly $400 billion.

Almost all major content owners put more premium inventory online.

Today, TV providers are fighting for consumer attention and there is more competition than ever.

The gap in cost-adjusted efficacy between linear and Connected TV (CTV) has stayed strong. However, as advertisers embrace CTV to leverage data and relevance, the power of data-driven targeting is quickly becoming more apparent.

Only effective data-driven targeting can achieve the value sought after by advertisers.

In other words, TV advertisers now have a choice. They have the ability to differentiate between content across channels more than ever. And that's critical to a healthy and competitive CTV market.

Now just to put the CTV market scale in perspective, according to Omdia's latest research, there are now more than 200 million active Advertising-Based Video on Demand (AVOD) users in the U.S. alone.

By 2024, Omdia predicts that annual CTV advertising revenue will top $120 billion, outperforming subscription revenue by more than 20%.

More and more of the world's top advertisers are making programmatic buys a larger component of their upfront commitments.

Advertisers want more data-driven flexibility in TV advertising campaigns. They believe their digital buys should be a core element of their upfront commitment. And the networks are adapting to that demand.

Ultimately, this will lead to the development of a new programmatic forward market for CTV inventory.

Broadcasters are also applying the same innovation focus to the world of identity. Recently, TTD has announced collaborations with OpenAP and Blockgraph.

This discussion on identity is bigger than cookies. It's bigger than any company or any channel. Cookies are not present in CTV. However, a privacy-safe identifier for CTV will be a major factor in driving relevant ads and managing reach and frequency across apps, channels, and devices.

CTV needs this kind of approach in order to maintain pricing power in a way that helps fund the high quality content that has kept most consumers binge-watching during this pandemic.

The current TV content arms race cannot be financially sustained for providers or consumers without relevant ads.

UID or user ID number is the identification number of your user account.

Remember how UID works, consumers sign in once with their email address and then opt-in site by site, just once per site or app, or channel.

This is a significant improvement to the consumer Internet experience today, where intrusive toasts or cookie pop-ups appear on almost every premium content site and seemingly every time you go there.

It's a common ID that can be used by many different advertisers and publishers.

It often originates from publishers with existing sign-on systems.

Consumers can then engage with privacy settings and opt out directly from the services they know.

The Wall Street Journal reported 50 million UID authenticated users in the U.S. a couple of months ago.

There's no point in building walls around it. Brands will, over time, always gravitate to places where they can be deliberate and where they can measure ad impressions across channels.

There are some companies, mostly those with a dominant walled garden approach, that believe the Internet can be controlled by a few.

Then there's the rest who believe that an open, competitive Internet marketplace is the only real viable approach that preserves value and opportunity for all participants.

And that has meant that cord-cutting in linear or cable television has accelerated and that people are looking more and more at Internet-fueled TV.

Because there are also more apps than there have ever been, content discovery is tougher in CTV than it’s ever been.

TTD’s Q1 revenue was $220 million, a 37% increase from a year ago and TTD benefited from improvement in the digital advertising environment from both agencies and brands.

Video, which includes CTV, again, led growth during the quarter followed by audio.

While improving, the travel and entertainment verticals still lag compared to others, but both are showing signs of a rebound so far in Q2. There is still a massive recovery ahead in these segments and starting to see green shoots.

TTD estimates Q2 revenue to be between $259 million and $262 million, which would represent growth of between 86% to 88% on a year-over-year basis because Q2 last year was the nadir of TTD’s Covid problems to the ad buying industry.

That said, in the second half of 2021, TTD expects year-over-year total revenue growth rates to decelerate significantly on a sequential basis because comparable data will be hard to beat from Q3 and Q4.

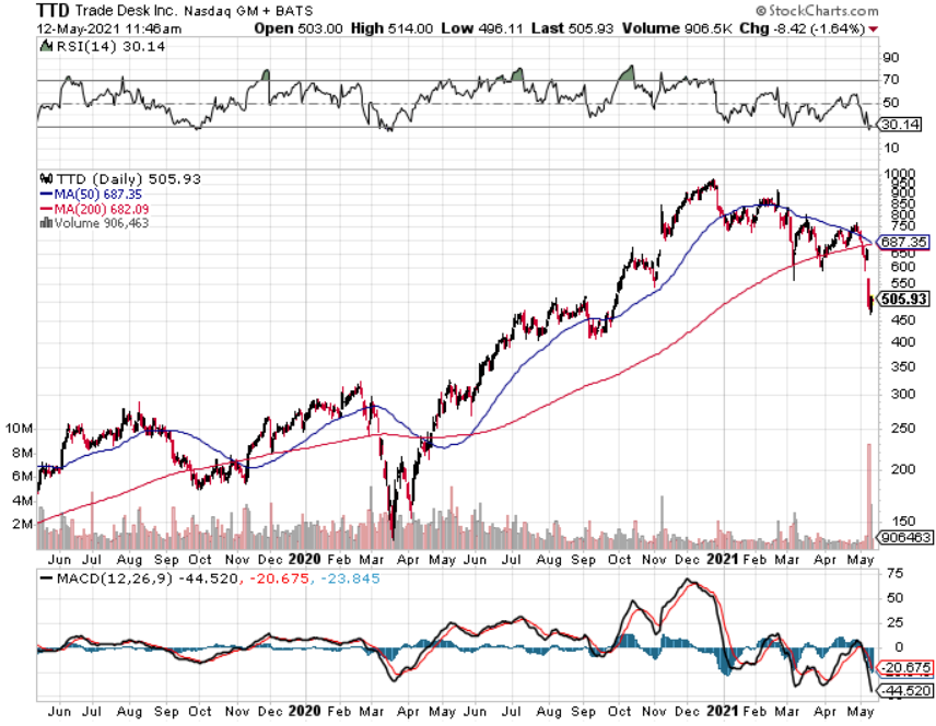

This was the cue for a massive selloff in TTD shares.

Don’t forget that the 2020 U.S. Election produced a tsunami of ad buying in the 2nd half of 2020.

The company is still firing on all cylinders, justifying the move from $160 in March 2020 to $950, but price action in shares is volatile.

The stock has pulled back to around $500 and has technical support at $450, I would look for an entry point around there if the broader market calms down.

“Everybody gets so much information all day long that they lose their common sense.” – Said American novelist, poet, playwright Gertrude Stein

Mad Hedge Technology Letter

May 10, 2021

Fiat Lux

Featured Trade:

(WILL INVESTORS PAY THE HIGH PREMIUM FOR ZILLOW?)

(Z)

In a typical year, spring begins the traditional home-buying season. But we know that this past year was anything but ordinary.

An internal Zillow (Z) report indicated that the pandemic has indeed caused people to rethink where they live and concludes that approximately 8 million existing homeowner households that have been on the sidelines may enter a real estate market already beset by unrelenting demand.

Also, 8.9% of consumers plan to purchase a home in the next six months near a 20-year high per the conference board's April consumer confidence survey.

The housing market is underpinned by demographic and economic tailwinds that will persist for the foreseeable future.

Millennials are moving up.

Baby Boomers are downsizing and in between, people of all generations are rethinking their lives.

Zillow (Z) is the most popular real estate portal in the country with hundreds of millions of consumers visiting the platform.

It’s easy to put up an advertisement on Zillow, while other competitors need to spend tens of millions of dollars to generate those leads.

It’s a sustainable competitive advantage which is one of the main factors for the stock going from $20 to $200 last year.

This effectively makes Zillow’s customer acquisition cost zero!

And because of that, it’s disappointing that they aren’t more profitable.

The PE ratio is currently 517 and as we look forward, we need to ask ourselves, will investors continue to bid up this high growth real estate tech stock?

This past quarter’s revenue growth was strong with Zillow reporting Q1 revenue of $1.2 billion, exceeding the high end of the forecast.

Q1 Internet, media, and technology (IMT) segment revenue was $446 million, grew 35% year-over-year, as this company continues to see accelerated growth in Premier Agent and strong growth in rentals.

This is Zillow’s bread and butter and represented over 37% of their total revenue.

Premier Agent revenue that connects realtors to consumers grew 38% year-over-year in Q1, the accelerated growth was primarily driven by connections growing faster than traffic, as well as focus on providing outstanding service and optimizing to connect high intent customers with high performing partner agents.

The inherent strength of the company lies in being the Uber of real estate and matching up ad-paying agents to customers.

However, I do believe we are hitting the high-water mark in the short-term as housing inventory levels hit generational lows and sellers stop putting their homes up for sale.

Therefore, it’s easy to argue that Zillow and its revenue growth will have a hard time pushing incremental growth now, and like many other tech firms, are facing tough metrics to beat year-over-year in for next earnings’ season.

Cratering interest rates of 2020 was the catalyst that drove the incremental buyer into the market, and I believe that harvest has mostly been collected.

Prospective buyers simply are at the extreme upper limit of affordability, now that the median house for sale in the U.S. is around $400,000.

Growth in Zillow Offers which is direct purchase and sale of homes continued to reaccelerate in Q1.

Zillow reported home segment revenue of $704 million, which exceeded the high-end outlook with 1,965 home sales.

Purchases increased to 1,856 homes in the quarter from 1,789 homes purchased in Q4, but not quite at the rapid pace planned as Zillow continued to work on retooling algorithm models to catch up with the rapid acceleration in home price appreciation.

The flipping game is just becoming too expensive, even for a subsidized tech corporation like Zillow and the algorithms are having a hard time competing with properties selling for $50,000 over the asking price!

Zillow is now competing with Qatar Sheikhs, sovereign wealth funds, and family offices of the elite who are piling into U.S. residential real estate at the same time.

Management has said they “buy homes at the median”, but wait, I thought technology would find the market inefficiencies in the pricing and Zillow would be able to find discounts.

Apparently not and that goes out of the window in an era of ultra-liquidity.

Management also claims they avoid buying houses in “really wealthy or really unique neighborhoods because they’re harder to resell and harder to price.”

The problem I have with Zillow Offers is that this division would be sucker-punched by a devastating blow from a property market pullback and be stuck with the carrying costs of thousands of mortgages and homeowner association fees per month.

That’s most likely the real reason for avoiding pricey areas.

Also, there is the conundrum that in market downdrafts, pricing power in the neighborhoods that Zillow targets fall fastest in terms of velocity of price and quality of buyer.

Even more worrying, Zillow charges the seller a fee of about 7.5% on average, which is notably higher than the traditional 6% commission a seller pays to realtors.

I thought technology was supposed to incite a deflationary effect?

Apparently not.

Mortgages segment revenue increased 169% year-over-year in Q1 to $68 million and was primarily driven by mortgage loan origination volume, which was up more than 8x year-over-year.

Sure, the 8x growth looks great on paper, but this division is still only 5% of total revenue and is a recipient of the law of small numbers looking better than they are.

In Q1, refinance loan origination volume comprised 90% of total origination volume.

There will be no refi boom in 2021.

Zillow really missed a gold mine in the mortgage division last year when they couldn’t even turn a profit in this division.

For the IMT segment, Zillow is forecasting 66% year-over-year revenue growth in Q2.

This is Zillow’s strength and you can expect Premier Agent revenue to be between $342 million to $350 million up 80% year-over-year.

On a sour note, they expect mortgage segment revenue to be down from Q1 and with respect to margins, Zillow’s Q2 IMT margin is expected to be 41% down sequentially from the 47% in Q1.

It’s clear that on the horizon, margins will shrink and nascent businesses will stall, and that’s a poor recipe for short-term price action in shares.

I don’t think investors will pay the current high premium for Zillow at these inflated levels, and yes, it’s a great buy and hold long term company, with a superior ad business that connects agents, but I do not see the case for the next leg up in the next few months.

This year will be remembered as a consolidation year as a few years of revenue were brought forward because of a once-in-a-lifetime interest rate collapse and pandemic tailwind.

Unfortunately, this year might just be too boring to 10X Zillow’s stock.

“It is only when they go wrong that machines remind you how powerful they are.” – Said Australian Journalist Clive James

Mad Hedge Technology Letter

May 7, 2021

Fiat Lux

Featured Trade:

(TWITTER LOOKING MORE ATTRACTIVE AFTER THE DIP)

(TWTR)

Selling off from $77 — Twitter is an internet stock to put on the watchlist.

Twitter is a unique asset that is enriching and powerful, especially for the long tail of niche topics.

If I had to point to one area that will accrue a meaningful impact on people’s experience, and business as a whole, this would be it.

Topics and interests are good for businesses on Twitter too, especially for local small businesses, as they contribute stronger signals around intent, and Twitter profits by serving relevant ads, which will ultimately lead to a transaction like a donation, subscription, or purchase.

These ads that are distributed and embed around the tweets are called Twitter’s Mobile App Promotion (MAP) business.

This division was up more than 50% year over year revenue growth in the fourth quarter of 2020 thanks to the public health situation making Twitter more relevant than ever.

Twitter is taking steps to make the platform more attractive now. For instance, take audio rooms, which they call Spaces, and long-form newsletters, made possible by the acquisition of Revue.

It’s easy to imagine starting with a tweet, moving a conversation to real-time audio, and recapping the conversation with long-form text.

It’s this in-between interaction that will prove to be powerful. The same is true for revenue-generating products, as more accessible advertising models will encourage the use of commerce tools and loop back into more advertising.

On the technical side of it, Twitter simply got ahead of itself on the stock chart but cemented its broad strength with an emphatic beat of total revenue reaching $1.04 billion, up 28% year-over-year.

Total ads revenue grew 32% year-over-year, driven by strong brand advertising in March and accelerating year-over-year growth in MAP revenue.

Interestingly enough, topics like sports betting, crypto, and personal investing gained traction in an accelerated way, and these MAP advertisers, who advertise into those areas benefit from a surge in app downloads for crypto or investing or betting.

These specific categories received 10X higher spend in Q1 relative to what they spent last year, demonstrating how Twitter is cleaning up from strong secular trends and with an enormous growing audience.

This active and pertinent conversation around the topic simply allows Twitter to turn on the cash spigots and this ad format delivers relevant ads.

Strength in these MAP advertisers means crypto ads won’t be going away anytime soon and it appears as if these topics have become a bigger conversation in everyday American life among consumers perhaps than they were in years past because the price of bitcoin is at an all-time high.

Also, legal betting is coming to the leagues in the United States, and mainstreaming will cause full-scale adoption, meaning the betting tweets are about to snowball.

Expect a lot more sports betting ads along with your garden variety crypto app download ads on Twitter.

I am optimistic that these are secular trends that can continue for a long time especially when you consider the Millennials' stranglehold on American demographics.

This pivot is also indicative of Twitter’s ability to deliver for advertisers at the right moment aligning the right conversation on Twitter.

Twitter’s tough comparable data to last pandemic season made a selloff in shares inevitable — Q2 2021 metrics will perform poorly against Q2 2020’s.

Management had no choice but to guide down and expect Monetizable Daily Active User (mDAU) growth rates to be “in the low-double digits on a year-over-year basis in Q2, Q3, and Q4, with the low point likely in Q2.”

A period of consolidation is upon us in Twitter, and they will be retooling the wagon.

Another headwind to note that along with Facebook, Twitter has been actively preparing for the changes that Apple just released as part of iOS 14.5 update.

Twitter’s outlook for Q2 and 2021 assumes a “modest impact from the rollout of changes” associated with iOS 14.5 across owned and operated ads.

The covid surge added about 5 million mDAUs in the U.S. and Europe or North America and Europe, to 38 million from 33 million.

The answer is that I do believe that Twitter will retain the cohort that entered with Covid even if Covid will end.

They will stick with the platform because the use case for it enriches their business, personal life, and keeps their pulse on the on-goings in the world and the U.S.

That is very powerful.

Losing this group would mean another leg down for the stock into the low 40s, which would be a no-brainer buy.

What is Twitter’s short-term roadmap?

They plan to double development velocity by the end of 2023, resulting in doubling the number of features per employee that directly drives either mDAU or revenue.

Second, they have a goal of at least 315 million mDAU in the fourth quarter of 2023, which requires continued compounding growth at about 20% per year from the base of 152 million mDAU reported in the fourth quarter of 2019.

Lastly, Twitter’s goal is to more than double total annual revenue to over $7.5 billion in 2023.

This requires Twitter to gain market share with performance ads, grow brand advertising, and expand products to small and medium-sized businesses.

If the investors sniff out they are on the right track to achieve these three initiatives, I do believe Twitter stock will be well over the last peak of $77 in 2022.

Expect Twitter’s shares to appreciate into the year-end.

It’s right to consider a period of consolidation as a reversion to the mean. This was inevitable after the opportunistic covid surge, but the handoff back to 20% growth is not as easy to communicate as it seems.

Twitter is still a great stock to get into if it drops to the $40-$50 range.

“We could use technology to help achieve universal health care, to reach for a clean energy future, and to ensure that young Americans can compete -- and win -- in the global economy.” – Said Former U.S. President Barrack Obama