Mad Hedge Technology Letter

February 19, 2021

Fiat Lux

Featured Trade:

(ARE TECH STOCKS IRRATIONAL?)

(TSLA), (PYPL), (BIG TECH)

Mad Hedge Technology Letter

February 19, 2021

Fiat Lux

Featured Trade:

(ARE TECH STOCKS IRRATIONAL?)

(TSLA), (PYPL), (BIG TECH)

It’s no joke – we are in the nosebleed section with tech stocks here.

But that doesn’t mean there is no more room to run.

Euphoria can continue until it doesn’t, and that’s where we are right now in the Nasdaq as we close in on 14,000 points.

If we take a minute to understand the different opinions out there, overall, people think tech isn’t cheap right now and rightly so.

Out of all assets, bitcoin and U.S. tech stocks are considered in bubble territory right now.

A survey contributed by market professionals in late January found that 89% of professionals believe we are in a bubble.

In the bubble, bitcoin is the posterchild of bubble activity.

The next so-called bubble poster child is big cap U.S. tech stocks.

Hard not to say no when the likes of fintech giants PayPal (PYPL) are up 25% YTD.

Another name that has seen insatiable appreciation in underlying shares is electric vehicle (EV) maker Tesla (TSLA) peaking at $880 and consolidating back to $790 today.

Tesla, meanwhile, also saw a massive climb in its share price in 2020 and that has extended into the new year.

CEO Elon Musk was crowned the world’s richest person.

The stock is up more than 700% year over year.

It is not exactly certain what might take down these robust names.

The number of tailwinds is still plentiful.

Loose monetary situations supportive of bubbles will stick around with the public health situation lingering for longer than first anticipated.

The health dilemma is highly likely to spill over into 2022 at this point.

More investors say the rollout of vaccines deployment is failing (41%) than those who said it’s been better than expected (22%).

Only half of those surveyed see normality returning by December.

Then checking in with the latest from a big American investment bank validated these survey numbers with massive in-flow of equity capital.

Brokers have been busy and rightly so as equities have been frontpage news lately with speculative mania reaching fever pitch.

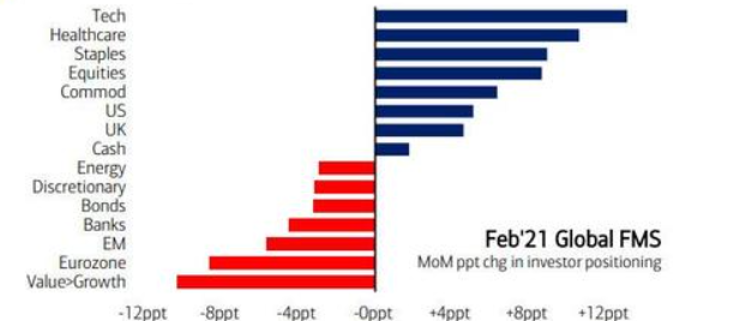

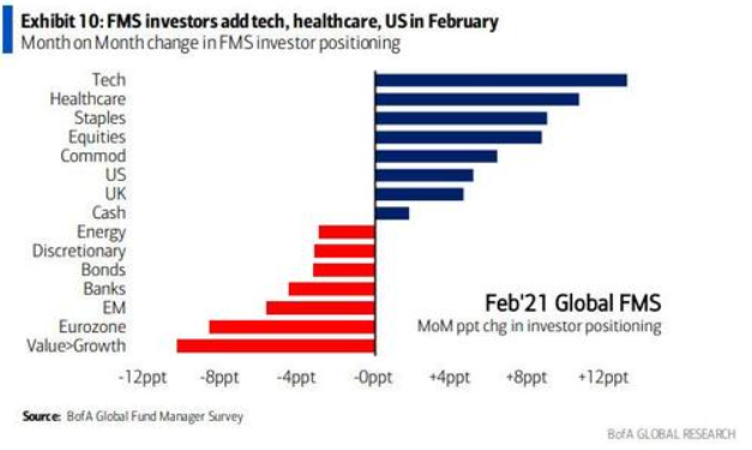

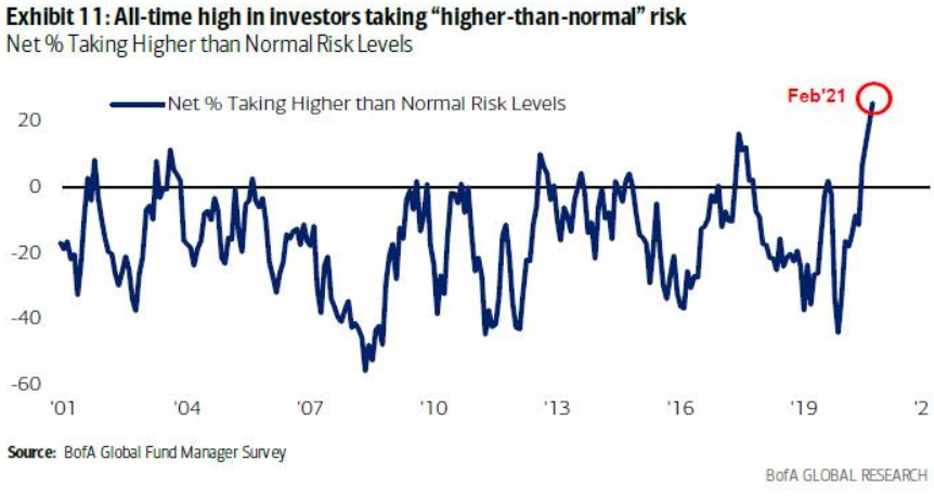

A record net 25% of investors surveyed by the American investment bank this month are taking higher-than-normal risks.

Cash levels slumped to the lowest since 2013, while optimism on cyclical risk assets rose to the highest since 2011.

The yields out there have never been lower and bearing more risk is required to produce the same number of gains.

Unrivaled optimism has been percolating with 84% of fund managers expecting global corporate profits to improve over the next 12 months.

For the first time in a year, investors say companies should focus on spending rather than improving their balance sheets.

We are in the midst of going from balance sheet protection to really letting it loose with capital spending and the synergies that surround it.

Easy money and upcoming health solutions are fueling tech investors into reflation trades of all stripes but mostly trading that is hypertargeting towards the best of tech.

Even if a mini correction presented itself, the mentality of “buy the dip” has strengthened since last March and it will really take a mega black swan event to topple this momentum.

In short, the tech narrative is strengthening with not only the gold standard of tech monopolizing even more revenue, but the second tier is gaining ground in terms of percentage appreciation as well.

The secular trends that buttress tech have also fortified over the pandemic and no government, big or small, has proven a match for proper regulating big tech.

“The bulk of the story will be what happens next.” – Said Co-Founder of Microsoft Bill Gates when talking about the pandemic

Mad Hedge Technology Letter

February 17, 2021

Fiat Lux

Featured Trade:

(THE TECH COMPANY COZYING UP WITH THE WHITE HOUSE)

(PLTR)

I hate to be a cheerleader but that is what I am about to do for the secretive big-data firm Palantir, co-founded by billionaire venture capitalist Peter Thiel.

With funding from the CIA’s non-profit venture capital arm In-Q-Tel, Palantir (PLTR) is named after mystical orbs in J.R.R. Tolkien’s “The Lord of the Rings” universe that can see both the past and present and allow users to communicate over vast distances.

To be concise, PLTR is the gold standard of data mining stocks and I urged readers to pile into this stock at $10.

That was then and this is now.

This stock is clearly a 10-bagger and after surging past $44 in January, the stock has consolidated to $28 today.

The fundamentals supporting this narrative is ironclad with the CIA delivering premium opportunity to accrue recurring government revenue.

We aren’t going into the semantics of how PLTR runs its business but in short, it basically provides customized software to clients analyzing large tranches of data for reasons ranging from finding suspected criminals to improving companies’ manufacturing capabilities.

The company acknowledges that government customers use its technology to kill people, so investors not comfortable with the deeper meaning behind the technology and revenue should steer away from this one and go with the softball versions of big tech.

Palantir gets both criticism and praise for the powerful nature of its data analytics software.

For example, critics allege Palantir's profiling tools used by intelligence and immigration agencies sometimes operate under a cloak of secrecy with zero oversight.

Palantir’s tools are not just for killing bad guys, they have also signed up companies from sectors that include healthcare, energy, and manufacturing.

Palantir has two main services that analyze data: Palantir Gotham and Palantir Foundry.

A customized option, Palantir Gotham is used by companies, government agencies, and law enforcement to combine information to decipher previously unseen patterns and identify relationships between sets of data ranging from social media posts and addresses to license plate numbers and personal relationships.

The algorithm then summarizes content together to make broader conclusions from the data.

Meanwhile, Foundry is a ready-made solution focusing on clients ranging from pharmaceutical and automotive businesses to aviation companies like Airbus and is meant to cut down on the costs associated with Gotham, such as the need for multiple on-site engineers.

Who is the CEO?

Alex Karp.

A graduate of Stanford Law School.

Karp has been explicit in his belief in the need for Silicon Valley companies to work with the U.S. government and law enforcement agencies precisely because they are American companies.

Palantir refers to effective applications of its software such as combatting Ponzi scheme conman Bernie Madoff to disaster recovery to thwarting cyberattacks and fighting child exploitation.

Not only that, Palantir’s software was deployed in the aftermath of Hurricane Florence in 2018 alongside Team Rubicon, an organization of military veterans that responds to disaster areas. With Palantir’s Gotham Operations module, the group identified and responded to neighborhoods in the greatest need of assistance.

How does the software directly help real-time U.S. soldiers in the field?

Its software helped the U.S. military track insurgents in Afghanistan planting improvised explosive devices (IEDs) by finding correlations between weather patterns, command wire IED attacks, and biometric information found on explosive devices.

Palantir has also sold its software to the Salt Lake City Police Department, helping officers reduce the time it takes to perform complex investigations by 95%.

Granted, this tech company is not for everyone, which is why many global brands such as Hershey’s, Coca-Cola, Home Depot, and American Express have terminated relationships.

In the short term, PLTR blistering rally will face an expiration of a lockup that allows 80% of total shares to be sold which could unleash a wave of selling from insiders tempted to cash in their shares.

The company’s market valuation at 39 times 2021 sales estimates implies revenue growth well in excess of 40%, at this pricy level, it makes PLTR an easy sell the news victim.

PLTR has tanked for two consecutive weeks and shares are down 18% from a record high late last month.

The overheating of shares has come back to reality with a tepid annual sales growth forecast of at least 30%. That suggests a significant slowdown from last year.

By comparison, sales growth in 2020 reached 47%, even surpassing $1.1 billion.

The silver lining is that government sales jumped 85% reassuring investors that the quality of sales could not be higher.

The company insiders have waited years to unload shares, and if there is a significant dip, I would put money to work in PLTR.

Shares are going to $100 and readers should ride the ladder up with them.

“Failure is not an option here. If things are failing, you are not innovating enough.”- Said Founder and CEO of Tesla Elon Musk

Mad Hedge Technology Letter

February 10, 2021

Fiat Lux

Featured Trade:

(UBER GETS ANOTHER MULLIGAN)

(UBER)

Great news for tech investors – Uber (UBER) is getting a pass on its almost historic loss-making 2020!

A highly bullish indicator is the broader tech market able to absorb an almost $7 billion annual loss with ease.

This all bodes well for the health of the tech market in 2021 – we should finish this year clearly higher than we are now today albeit with no black swans.

The tech market is iron clad right now with multiple external forces pushing up multiples to historic levels.

Imagine there are copious amounts of better tech companies out there that are actually turning a profit and are even at the vanguard of all the latest tech trends, and Uber definitely isn’t one of them.

Yet, I believe Uber shares will roar higher!

A Nasdaq index brimming with liquidity is the one way to explain this phenomenon because the bar has been set so low for tech companies to jump over that unless there is a bankruptcy or systemic risk, shares will rip higher.

Remove the liquidity subsidy and Uber shares would be headed into the gutter in a flinch.

But here we sit with tech shares going parabolic after a robust breakout.

If this carries on, we will see more abnormal side-effects and I believe the GameStop phenomenon was precisely the precursor to much weirder activity that is about to happen.

I must divulge that part of the narrative driving firms like Uber is the re-opening theme of increased consumer behavior if the population is theoretically inoculated driving a surge in economic activity.

The boom in outdoor consumerism would catapult Uber’s loss-making ride share division which performed poorly grossing only $6.79 billion, down 50% from a year ago.

As many might have guessed, Uber’s pitiful performance in ridesharing in a pandemic was met conversely by heightened food delivery gross volume of $10.05 billion, up 130% from a year ago.

What does this mean?

Uber is turning into a loss-making food deliverer from a loss-making ridesharing company and are still losing vast sums of money.

Their strategy of acquiring other food deliverers like alcohol delivery app Drizly for a deal valued at $1.1 billion in stock and cash combined will scale well and offer cost savings but is no panacea.

They also sealed a deal for a $2.65 billion acquisition of delivery service competitor Postmates in December to help build out its delivery capabilities.

However, where is the light at the end of the tunnel?

Where is that iPhone or YouTube – that game-changing asset?

There is no growth asset here and I still see no proprietary technology other than an app that matches drivers to passengers and a food delivery app that gets a car to its hungry customers.

To Uber’s credit, they revealed 20% improvement in net losses amounting to $6.77 billion, from a jaw-dropping $8.51 billion loss in 2019, and I will agree there is headway to make with such lousy numbers.

As long as Uber is afforded such a long leash and incentivized to perform badly, they can incrementally reign in the net losses and still claim victory.

But I scratch my head thinking how they will finally overcome that “last mile” problem of making this company a true tech giant and not one just brandishing below-average intellectual property and partying for losses that aren’t as bad as expected type of model.

At the end of the day, we can only trade the market we have, and not the one we want.

The broader tech market has given its implicit nod to Uber and this company remains an attractive buy on the dip tech growth company even though I listed a myriad of risks and concerns about its underlying model.

“My goal was never to make Facebook cool. I am not a cool person.” – Said Co-Founder and CEO of Facebook Mark Zuckerberg

Mad Hedge Technology Letter

February 10, 2021

Fiat Lux

Featured Trade:

(THE CORPORATIZATION OF BITCOIN)

(TSLA), (BTC)