“Apple doesn't do hobbies as a general rule.” – Said Apple CEO Tim Cook

“Apple doesn't do hobbies as a general rule.” – Said Apple CEO Tim Cook

Mad Hedge Technology Letter

November 1, 2024

Fiat Lux

Featured Trade:

(WILL THE TRIFOLD PHONE SAVE TECH?)

(HUAWEI), (AAPL)

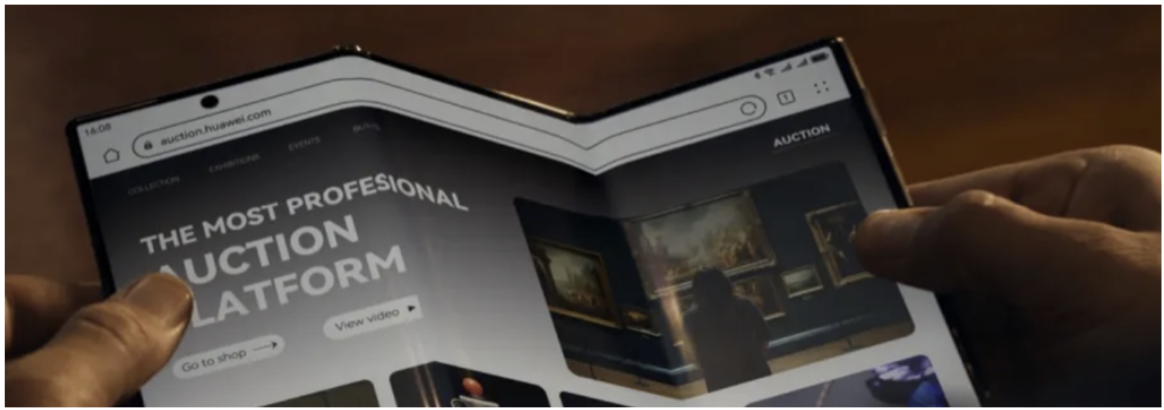

Silicon Valley is usually on top of the innovation game, and as Huawei announced the launching of its trifold smartphone, one must ask whether Silicon Valley is late to the party or if this technology is even worth their time.

My guess is that foldable devices won’t move the needle, and these announcements aren’t really about moving revenue but to offer bluster in a global game of cat and mouse.

In general, the smartphone super cycle is about tapped out, and I don’t see a foldable phone as a reason for another re-acceleration of revenue.

There is a higher chance that in the next few years, this foldable technology is adapted for some other technology and written off on the balance sheet.

To think it could be some revolutionary new trend is beggars’ belief.

To be honest, many consumers are tired of screen time and can’t get off their screen because work duties connect them to the screen.

When needing a bigger screen to watch global sporting events, many would prefer a large-screen TV that doesn’t fold. This phone has no TV screen – not by a long shot.

It is a little difficult for me to understand the use case here for Huawei going big in the foldable screen business.

It’s not like the new phone will be cheap either, the new trifold smartphone will start at around $2,800, which is more expensive than most premium laptops.

Huawei announced its foldable product on the same day as Apple unveiling the new iPhone.

Apple announced its iPhone 16 Pro Max will start at $1,199 and the iPhone 16 at $799.

The first set of Apple Intelligence AI features will be available in a free software update next month.

Huawei’s Mate XT also comes with artificial intelligence features, such as text translation and cloud-based content generation.

The device is 3.6 millimeters thick when unfolded, with a 10.2-inch screen.

More than 3.5 million people had pre-ordered Huawei’s trifold Mate XT smartphone as of midday Tuesday.

The Chinese company has sought to make a comeback in the smartphone industry, which was hard hit after the U.S. slapped sanctions on the company in 2019. The U.S. in October 2022 imposed broader restrictions on American sales of advanced chips to Chinese businesses.

Apple fell out of the list of top five smartphone vendors in China in the second quarter of this year. It was the first time that domestic players held all five spots.

Clearly, Chinese tech views Apple as the top dog to compete against, but I would say that Apple’s star is waning in China.

They are being pushed out by the Chinese government, who are indirectly suggesting to Chinese consumers to go with domestic alternatives.

National champions and protecting them are the modus operandi in the age of deglobalization, and that will not change anytime soon.

As for the tech, foldable screens are a mediocre and lateral upgrade.

The size of a screen has a size limit to its usefulness, and building gargantuan screens does not suggest that it could trigger some new wave of untapped profits.

I believe Apple is smart in not aggressively pursuing foldables, and the quest continues to find the new killer tech that will take over.

Until then, tech stocks should grind up, but not in a dramatic fashion.

Mad Hedge Technology Letter

October 30, 2024

Fiat Lux

Featured Trade:

(LACK OF AI ROCKS THE KOREAN HEAVYWEIGHT)

(SAMSUNG), (SK HYNIX)

It’s not just about smartphones for Samsung anymore, their stalwart chip business is in full-blown crisis mode as they have been too slow to adapt to the artificial intelligence revolution.

It shows that if a company is asleep at the wheel, how quickly and how far they can fall back.

Samsung is Korea’s flagship tech company, and it is like the Titanic in a way because it is hard to turn around with the amount of employees it has.

Old habits die hard, and management simply wasn’t prepared for the giant leap forward in semiconductor chips.

Remember when their flagship smartphone, named the Galaxy, was the best phone in the world?

Oh, have times changed?

Concerns are piling up that the company is losing out to smaller rival SK Hynix in AI memory and failing to gain on Taiwan Semiconductor Manufacturing.

Overseas investors have sold about $10.7 billion worth of the South Korean company’s shares on a net basis since the end of July.

That hope has been snuffed out with the company admitting delays with its latest-generation HBM chips in early October, soon after SK Hynix said it had begun volume production. Meanwhile, US rival Micron Technology is stepping up efforts in HBM as well and has reported strong demand for its offerings.

Beyond its lag in AI memory, Samsung has struggled with a costly, yearslong effort to close the gap with TSMC in the foundry business. Like Intel— which has run into similar difficulty with plans to expand its outsourced chipmaking operations — the Korean firm is now moving to cut jobs and make other efforts to stop the bleeding.

Jay Y. Lee — a grandson of Samsung’s founder who was appointed executive chairman two years ago — was acquitted of stock manipulation charges in February after years of legal issues. Three months later, the company unexpectedly replaced its semiconductor division head with Jun Young-hyun, a memory chip veteran.

Samsung executives and engineers are now in full unison, heading towards the exits, looking for greener pastures, and that is a massive red flag.

It certainly isn’t a good optics when the best talent is looking for another job, but that is where we are at with Samsung.

In the short term, I don’t expect a quick turnaround because the management problems are real, and to get competitive in AI is a tall order.

Just look at AMD, they are about a year behind Nvidia, and Samsung isn’t even in the ballpark.

I expect a slow slide into irrelevancy and foreign shareholders dumping big swaths of Samsung stock backs this theory.

In the short term, readers shouldn’t get too fancy with picking AI stocks because there is a massive risk to the downside, considering how expensive the equity market is right now.

Samsung won’t be the last company to be swept up by the dustbin of tech firms.

In the U.S., it is clear which companies are behind and which are leading.

Microsoft is definitely one to buy the dip on.

I definitely envision at least one fiercer rally in AI stocks as we cruise past the U.S. election.

Mad Hedge Technology Letter

October 28, 2024

Fiat Lux

Featured Trade:

(THE FUTURE OF TECH STOCKS)

(AI), (NVDA), (XLU), (XLE), (AAPL), (GOOGL), (AMZN), (META), (MSFT)

Through the vast whole spectrum of public markets, the U.S. stock market, and specifically technology stocks, are dominating versus their peers from other countries.

Heck, even Apple, just one company from a small suburb in California, is valued at a price that is greater than the entire German economy.

Does that speak to how bad the German economy is, or does it speak to the potency of public tech companies in America?

The truth is probably a bit of both.

Then, take a second and try to absorb the fact that Apple hasn’t even integrated AI into its own products yet.

The future is bright for many tech stocks, and the rally will broaden out to non-Magnificent 7 stocks.

More granularly, the US will continue to lead by market cap share as artificial intelligence benefits expand beyond a few large tech names that have dominated the market rally over the past year to companies in various industries.

Revenue production and margin improvement will be the critical levers of expansion.

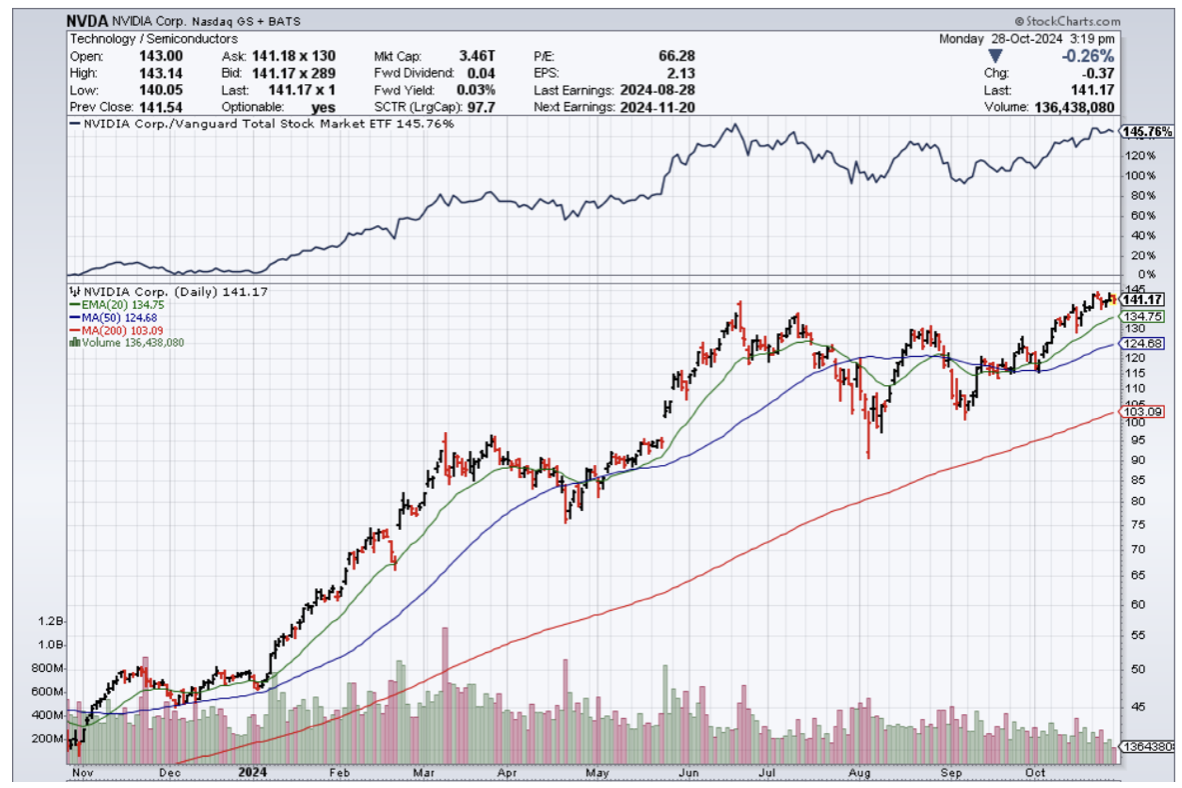

The first will come from the money pouring into AI benefiting companies outside of Big Tech. This plays out as tech companies buy AI chips from the likes of Nvidia (NVDA), and as they need more power, these AI operators are forced to spend with companies in the Utilities (XLU) and Energy (XLE) sectors.

As AI makes companies more efficient and eliminates the simplest work, eventually cutting down costs, US corporates should get a boost to profit margins.

Global equity markets, including retirement allocations to equities, are basically leveraged to Nvidia.

A non-US tech company will rise over the next decade and unseat the large tech companies currently driving the US market share, like Apple (AAPL), Nvidia, Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), and Meta (META) are almost zero.

When we look at the revenue possibilities and understand that AI will directly cut expenses by creating efficiencies, it’s hard to see tech stocks do anything but go higher in the long term.

Even then, there will be some dips, and they should absolutely be characterized as buying opportunities.

Just look at a 3-month chart of Apple, and each month has presented a dip buying opportunity on August 6th, September 16th, and October 7th.

Apple stock is up 7.5% in the past 3 months.

When everyone complains that tech stocks are too expensive, well, they will get more expensive.

As long as leverage is able to be tapped, institutions will tap it and look for that asymmetric trade to the upside.

Tesla has also proved how hard it is to bet against tech and Elon Musk.

It usually is a terrible idea.

The setup to Tesla’s earnings meant a very low bar, and Musk jumped over it to the tune of a 22% pop in Tesla stock.

Tech is clearly in a secular bull trend, and trying to get artsy to squeeze in a microdip on the short side usually has meant a loss-taking event.

Why even try?

It’s my job to tell readers to bet on tech going to the upside, especially the quality companies that accelerate revenue by harnessing the superpowers of AI.

Mad Hedge Technology Letter

October 25, 2024

Fiat Lux

Featured Trade:

(EXPENSIVE ENERGY A BIG WORRY FOR THE FUTURE OF AI)

(AI)

One of the forgotten risks of AI is the energy capacity situation in the United States.

Many people forget that AI will require immense energy with a hoard of energy-guzzling data centers to facilitate the next tech revolution.

Many consumers have come to realize how the cost of energy has skyrocketed lately with no breaks in sight.

There is an increasingly real chance that Silicon Valley might not be able to afford AI simply because the costs of energy will deem the AI concept unworthy.

Green energy hasn’t developed as fast as many experts once thought, and the United States is still very much dependent on fossil fuels to facilitate tech and business in general.

A pressing question that is popping up is whether the United States can deliver the energy capacity that AI chips demand.

The question is hard to dissect because the situation is always changing.

Numbers need to make sense, just like how builders build when they think they can sell houses and apartments for a profit to the end buyer.

The military conflict in Eastern Europe has forced German manufacturing to deindustrialize because producing without that cheap Russian energy is loss-worthy. AI could follow a similar pattern.

The data grid will become strained, but by how much is the next most important matter?

A ChatGPT query, on average, requires almost 10 times as much electricity to process as a Google search does.

The rise of generative AI coincides with a heightening of other factors increasing energy demand, from the electrification of transportation and infrastructure to the on-shoring of US manufacturing. Adding yet another acute demand: AI systems need power all the time.

Critics of AI fanaticism point to potential wastefulness, and this could end up morphing into a government regulatory quagmire like so many industries that are overburdened by government agency overreach.

If, in the case, the energy demands spiral out of control with everyone going the AI route with every country building AI data centers, the exploding costs will mean that tech won’t be able to profit from AI as quick as it wants.

Many analysts are already raising the flag as to whether all these billions poured into AI investments will really pan out or not. AI isn’t free to produce, but shares of it are priced as such.

Much of this hot money is migrating into companies that haven’t proven anything or never even turned a profit. Look at OpenAI, it started out as a non-profit.

The issue I have is that generative AI is priced to have zero pushback of its revenue trajectory, and I do believe that is wrong.

When there is a pullback, it will be deep and sharp, even if not long.

I believe that would be a healthy event for AI because the stock shares of AI have gone parabolic.

In short, ride up the momentum until the wave crashes, but watch out for the canary in the coal mine, which will foreshadow a deep dip in AI shares.

Mad Hedge Technology Letter

October 23, 2024

Fiat Lux

Featured Trade:

(ANOTHER GEM IN THE CHIP INDUSTRY)

(TSM), (NVDA)