“Our philosophy is that we care about people first.” – Said Seller of User Data Mark Zuckerberg

“Our philosophy is that we care about people first.” – Said Seller of User Data Mark Zuckerberg

Mad Hedge Technology Letter

January 31, 2020

Fiat Lux

Featured Trade:

(APPLE OUTSHINES THE REST)

(AAPL)

I'll give credit when credit is due.

Apple CEO Tim Cook pulled off a quarter to remember.

And yes, I've been hypercritical of his lack of innovation, but I can't question the way he’s insulated the company from being exposed to softness in mainland China.

Analysts expected $88 billion in revenue and Apple easily surpassed this number by posting $91 billion.

When you look under the surface, there are usually some chinks in the armor.

But this time around Apple's quarter was practically flawless albeit with some frosty guidance.

It's no secret that the quality of a Chinese smartphone has picked up and now rivals some of Apple's best products.

However, Apple turned a weakness into a strength and sales of iPhones was one of the highlights of an outstanding quarter.

In fact, it was the iPhone 11 that carried the load this time.

In total, iPhone Revenue rose 8% to almost $56 billion and they shipped 72.9 million units.

The outperformance doesn't just end there.

Wearables have become a meaningful revenue driver in itself.

Specifically, ear buds and the Apple watch have captivated Apple customers who are scooping up these products in droves.

In the prior quarter, 75% of people who bought the Apple watch were first time buyers.

This added up to wearables clocking in $7.3 billion in revenue this past quarter.

Apple’s outperformance dovetails nicely with my overarching theme of the FANG group plus Microsoft separating themselves from the other tech companies in 2020.

The network effect that these companies possess is unrivaled and the longer they stay in business, the stronger these effects seep in.

If there was a negative part of the quarter, Tim Cook failed to delve into the new Apple streaming product and avoided giving too much detail.

Fortunately, Apple has not bet the ranch on streaming and have stuck to what they know best.

Ultimately, Cook struck a lukewarm tone, especially with the spread of China’s coronavirus threatening to shut down production operations for several manufacturers.

The company has restricted employee travel and shut one store due to the outbreak.

Looking forward, management said “there will definitely be an impact on China in terms of consumption.”

Apple is slated to release its first 5G phone later this year which has been the catalyst for the price appreciation in shares.

Apple continues to be a multiprong revenue machine and any dip should be bought.

This is the type of company that should be part of any multi-asset portfolio.

“I love museums but I don't want to live in one.” – Said CEO of Apple Tim Cook

Mad Hedge Technology Letter

January 29, 2020

Fiat Lux

Featured Trade:

(THE NEW NORMAL FOR THE INTERNET)

Russia can now “unplug” from the internet, is this a sign of things to come?

Since 2010, the internet has become the de-facto global cock pit.

A breaking up of the internet is heavily negative for American tech companies who vie for overseas revenue.

The more unified the internet is, the easier and more cost effective it is to scale up a business and sell software and hardware to the customer.

The advent of the Russian intranet could lay the groundwork for other sovereign nations to build their own version of an intranet.

This could lock out foreign companies from doing business or only allow them access if they play by unfair rules.

There is also the dual objective of keeping close tabs on local dissidents and controlling the media which countries like Iran have found convenient and mightily effective.

The internet is not a simple place anymore.

Cross border digital transactions and cooperation of it is diminishing at a rapid pace.

Take for instance Russia’s third-largest internet company Rambler which sued Amazon-owned Twitch platform for 180 billion rubles ($2.87 billion) over illegal streams of soccer matches from the English Premier League.

Russia is the third-largest user of Twitch worldwide which could eventually lead to a ban of the service.

Where does this eventually stop?

Next on the chopping block could be Google search and then YouTube.

Many of these free services make money by serving up ads and revenue would be seriously hit if a wide swath of usership are taken offline.

The announcement merely noted that Russia successfully tested a country-wide alternative to the global internet, but the devil is usually in the details.

Either way, pulling out the rug from underneath Russian netizens is a serious option for the Kremlin.

The results will now head to the higher ups to conclude when and how the new Russian intranet will be implemented.

There are still loose ends that Russia needs to sort out like integrating a separate DNS system.

A new system connecting the physical infrastructure directly to the rest, which at present must do so through international connections. And that’s just to create the basic possibility of a working Russian intranet.

Russia has taken comfort in knowing that China has its own version of the internet aptly named the Great Firewall, but China has not cut off access to abroad merely focusing on pressure points and content not supportive of its government.

Authoritarian countries want to rule with an iron fist, and this will help them do so, the added bonus is stonewalling American capitalism inside their border in digital form.

How would a domestic internet work?

By bottlenecking the points at which Russia's version of the net connects to its global counterpart.

Domestic ISPs [internet service providers] and telcos would need to route the internet only within the digital border of Russia.

This would require close partnership with domestic ISPs which would be easy to facilitate since state-owned firms have oversized clout inside of Russia.

The more networks and connections a country has, the more difficult it is to control access.

Countries receive foreign web services via undersea cables or "nodes" - connection points at which data is transmitted to and from other countries' communication networks.

These would need to be blocked too.

Then Russia would need to create something new from scratch.

In Iran, the National Information Network allows access to web services while policing any digital content and is operated by the state-owned Telecommunication Company of Iran.

A “walled garden” would nullify the usage of virtual private networks (VPNs).

At this point, netizens can still tap outside internet sources by connecting to different servers abroad through VPNs.

Russia already has an army of tech talent it can employ through heavyweights Yandex and Mail.Ru.

The handful of entrenched behemoths would benefit greatly from Russia shutting off itself to the outside world.

Russia has even banned the sale of smartphones that do not have Russian software pre-installed and this is just the next step.

The Russian government has had their hand in online censorship before, such as its failure to block Russians from accessing encrypted messaging app Telegram.

The state-owned Tass news agency reported the tests had assessed the vulnerability of internet-of-things (IoT) devices as we step into the era of 5G.

The cybersecurity element of this cannot be diminished, and what this tells us is that your smartphone and smart home devices aren’t safe at all.

Even though American tech companies won’t be widely affected in 2020, foreign revenue will start deteriorating in piecemeal fashion.

This will likely turn into a whack-a-mole problem with American companies hoping to plug the gaps but helpless if wide audience purges ruins numerous digital audiences.

There is a reason why YouTube isn’t successful in China and there is a reason why Mail.Ru isn’t the main internet provider in the U.S.

“Invention is by its very nature disruptive. If you want to be understood at all times, then don’t do anything new.” – Said Founder and CEO of Amazon Jeff Bezos

Mad Hedge Technology Letter

January 27, 2020

Fiat Lux

Featured Trade:

(HOW TO PLAY THE CHINESE PANDEMIC)

(TRIP), (TCOM), (GOOGL), (EXPE)

Am I going to rant about Peloton today?

No, I’ll save that for another day.

Let’s get straight to the chase – the epidemic from Wuhan is crushing tech stocks.

If you want a way to play the Chinese coronavirus outbreak, then look no further than Trip.com Group Limited (TCOM).

This company owns a series of reputable Chinese travel apps from Trip.com, Skyscanner, and Ctrip.com.

The Mad Hedge Technology Letter doesn’t tend to do tech alerts on Chinese companies listed in America as American depository receipts.

We rather not expose readers to the high risk of one of them suddenly being kicked off of one of the exchanges.

American investors have zero rights of recouping any losses if Alibaba or Baidu delists or even announces to switch its listing on the Shenzhen tech exchange.

Remember that founder of Alibaba Jack Ma signed over the PayPal of China Alipay to himself without even telling Yahoo about it.

Yahoo was also locked out of any profits from the decision as well even though they were seed investors in Alibaba.

That is China in a nutshell for you!

So what’s happening now? Tourists are staying home in droves and the ones that support the economy which are the Chinese ones during the peak travel season of Chinese New Year.

Cities are getting quarantined left and right in China and the mainland has ordered all travel agencies to suspend sales of domestic and international tours.

Chinese shares have felt the pain with shares of China Southern Airlines Co. – the carrier most exposed to the site of the outbreak – cratering 20% since the second death from the virus was confirmed.

If the situation unfolds like the SARS outbreak of 2003, things could turn bleak quickly.

Remember that in just one month of the SARS outbreak, Chinese air passenger traffic fell 71%, and Trip.com was rerated and has fell off the face of the earth.

I am predicting the same type of devastating numbers to the online travel world.

Trip.com has struggled to keep up with competition from digital rivals like Meituan Dianping and Alibaba, and even if the virus is conquered, business might never come back.

Despite the trade war and Hong Kong’s protests, the world has been held up by the Chinese tourist.

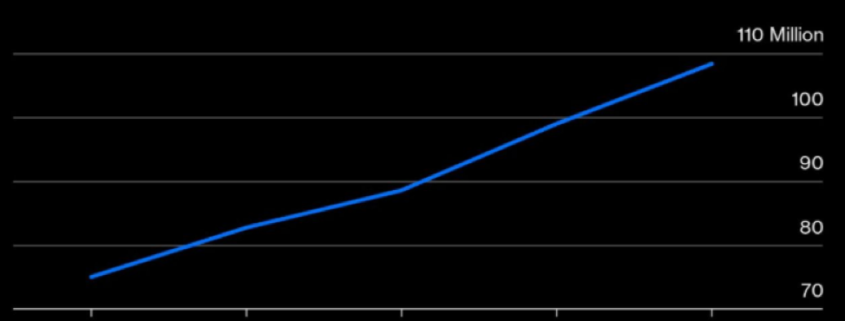

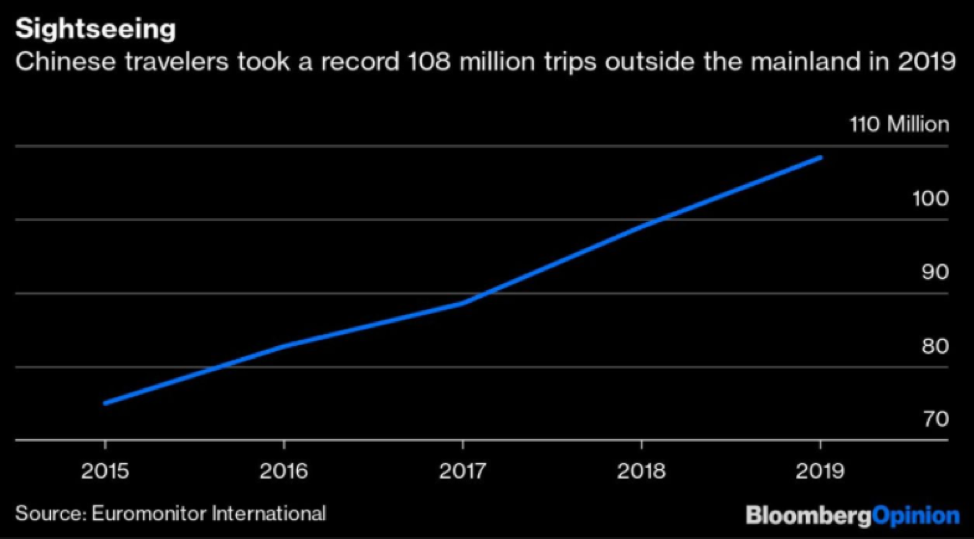

108.39 million Chinese overseas trips were taken last year, a 9.5% gain, after surging 11.7% in 2018.

Flight volume was brimming along nicely until the virus, but the hotel-booking sector is getting crowded.

Meituan Dianping has recently overtaken Trip.com as China’s top site, and now has 47% of China's market, 13% higher than Trip.com.

Now, Meituan is moving further onto Trip.com’s turf with luxury hotels, while chains like Marriott International Inc. are pushing for direct booking on their China websites.

Alibaba said part of the $13 billion it raised from its Hong Kong listing in November would go toward fliggy.com, its online travel group site.

The way the Mad Hedge Technology Letter is playing the sudden drop in overseas travel confidence is through the travel app I dislike the most – TripAdvisor (TRIP).

I actually don’t have a personal problem with the functionality, but the business behind it is terrible.

That was the main reason I strapped on a put spread and I can’t see TripAdvisor outperforming dramatically in the next few weeks in the face of a global pandemic.

This was a short-term trade that TripAdvisor won’t rise 11% in 30 day

I didn’t like this company before the coronavirus and now that Chinese tourists are home sitters for the Chinese New Year, this could put a dent into TripAdvisor’s new China initiative.

Trip.com Group had taken the lead in the day-to-day running of TripAdvisor China. It owns the majority share, with TripAdvisor claiming a 40 percent stake.

Chinese were supposed to increasingly travel the world while its customer base is also becoming more global, in particularly with Trip.com and Skyscanner.

But that is all on hold now.

Yes, it is possible that there could be a dead cat bounce in shares if the virus is tamed, but the 2-week travel season is something you can’t get back once it’s over for TripAdvisor.

I believe this will come out in the numbers along with details about Google’s algorithms further destroying TripAdvisor’s relevancy in the online travel industry.

Then take into account that the company just announced a 200-employee purge for the explicit reason of increased competition from Google and things seem to be going from bad to worse.

The company has done a proverbial deal with the devil by positioning itself to be utterly tied to Google’s search algorithm while Google is going head-to-head with them.

Google has upgraded its travel search tools recently to turn the screws on several trip booking websites like TripAdvisor, Booking.com and Priceline.

In its last earnings release, TripAdvisor noted that Google has placed ads at the top of its search results, forcing companies like it to buy more ads.

The company had a rough last quarter, reporting adjusted earnings of 58 cents a share, down from 72 cents a year earlier and short of analysts’ estimates of 69 cents.

Rhetoric from management was equally as disappointing with them saying, “Google (is) pushing its own hotel products in search results and siphoning off quality traffic that would otherwise find TripAdvisor via free links and generate high margin revenue in our hotel click-based auction.”

“Google has got more aggressive. We’re not predicting that it’s going to turn around.” TripAdvisor CEO Stephen Kaufer said at the time and I don’t see how our put spread will lose money in the short-term.

I will advise readers to take profits when the time comes. Be aware that TripAdvisor also has an earnings report coming up in 2 weeks that could gyrate the stock.

I expect broad-based weakness in guidance and poor performance last quarter in the report.

“I don’t want to be liked.” – Said Founder and Former CEO of Alibaba Jack Ma