Why has there been a dearth of Mad Hedge Tech trade alerts to start the year?

Let me explain.

Love it or hate it – earnings' season is about to kick off.

And now, this is the part where it starts to get ugly with consensus of a 2% year-over-year decline in fourth-quarter S&P 500 earnings.

Banks are expected to be a rare bright spot and JPMorgan (JPM) delivered us stable results as one of the first to report.

The unfortunate part of the equation is that a lot has to go right for tech shares to go unimpeded for the rest of the year.

What we have seen in the first 2 weeks of the year is a FOMO (fear-of-missing-out) environment in which valuations have lurched forward to 20 times forward earnings.

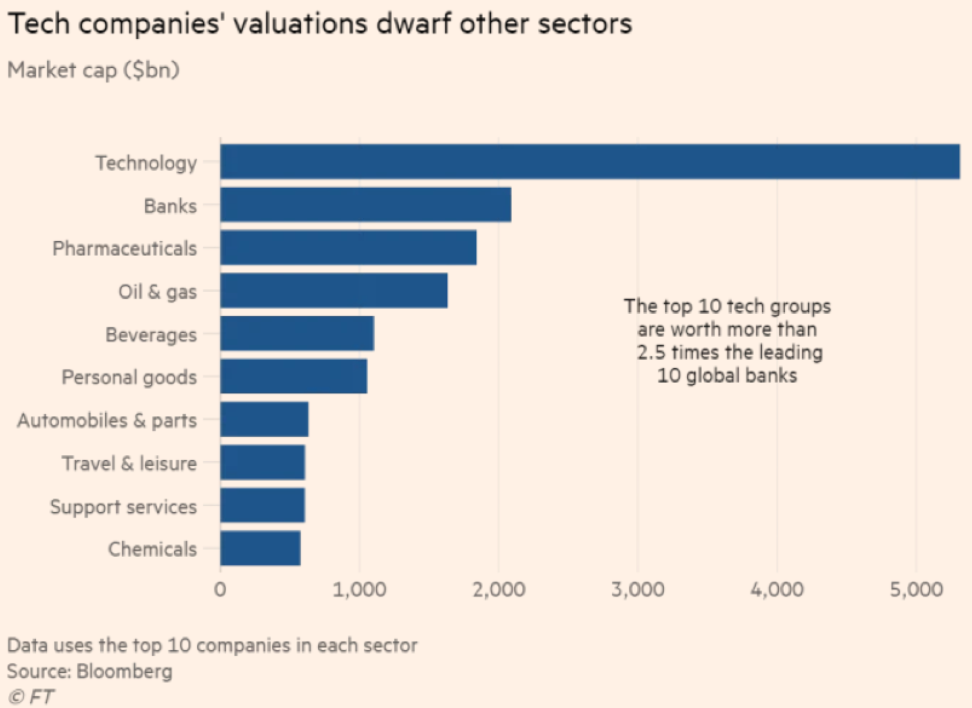

Tech is overwhelmingly carrying the load and I have banged on the drums about this thread advising readers to be acutely aware of a heavy positive bias towards the FANGs in 2020.

Well, that is already panning out in the first two weeks.

Examples are widespread with Facebook (FB) up over 8% and Apple (AAPL) already topping 6% to start the year.

It would be farfetched to believe that the tech sector can keep pilfering itself higher in the face of negative earnings growth.

However, behind the scenes, relations between China and America are improving, the threat of war with Iran is subsiding, and the Fed continues strong support tempering down risk to tech shares.

The situation we find ourselves in is that of an expensive tech sector that will again guide down on upcoming earnings’ reports telegraphing softness moving into the middle part of the year.

The ensuing post-earnings sell-off in specific software stocks will offer optimal short-term entry points.

The current risk-reward of chasing FANGs at these levels is unfavorable.

Another glaring example of the FANG outperformance is Alphabet who rose 26% last year.

They are on the brink of joining the $1 trillion club that Apple and Microsoft (MSFT) have joined.

Its market value currently sits idling at $985 billion and its surge towards the vaunted trillion-dollar mark is more of a case of when than if.

Alphabet (GOOGL), more or less, still expands at the same rate of low-20% annually that it did 10 years ago.

Sales have ballooned to $160 billion annually and they sit at the forefront of every cutting-edge sub-sector in technology from artificial intelligence, autonomous driving, and augmented reality.

The engine that drives Google is still its core advertising business and strategic premium acquisitions like YouTube and penetration into other fast-growing areas such as cloud computing.

It has rounded out into a broad-based revenue accumulator.

Apple was the first public company to surpass a $1 trillion market cap and ended the year up 86% in 2019, and it has only gone up since then currently checking in at a $1.36 trillion market cap.

Microsoft followed Apple, hitting the $1 trillion mark during the first half of 2019, and it is now worth $1.23 trillion.

Amazon fell back after surging past the $1 trillion mark but inevitably will achieve it on the next heave up.

Amazon shares have been quickly heating up since its capitulation from $2,000 in July 2019 and round out the group of overperforming tech behemoths.

Although the rush into big-cap tech stocks in the first two weeks has been a bullish signal, it still doesn’t marry up with the lack of earnings growth in the overall tech sector.

Companies beating meager expectations will experience strong share appreciation although not at the pace of last year and will still serve investors pockets of overperformance.

We will find our spots to trade shortly, but better to keep our gunpowder dry at the moment.