“The business model of social media companies, of pure advertising, is problematic. It turns out the huge winner is low-quality content.”– Said Founder of Wikipedia Jimmy Wales

“The business model of social media companies, of pure advertising, is problematic. It turns out the huge winner is low-quality content.”– Said Founder of Wikipedia Jimmy Wales

Mad Hedge Technology Letter

November 13, 2019

Fiat Lux

Featured Trade:

(WHY YOUR NEXT TAXI RIDE COULD BE BY AIR),

(UBER), (TSLA), (GOOGL)

San Francisco is 49.2 square miles of pure innovation – at least historically.

The most creative solutions to the world’s most complex problems have been generated from this diminutive peninsula that juts out into the Pacific Ocean.

But when it comes to transportation, and by that, I mean the public transportation efficiently operated in most European and Asian cities like Seoul, Korea and Frankfurt, Germany, San Francisco epically fails at delivering an adequate system to the masses.

Instead, the stopgap solution gave us Uber (UBER), the rideshare company, and the fall out is more cars clogging up a bigger portion of the roadways and bridges.

And then there is Tesla (TSLA), whose enigmatic CEO loves to tell investors that electric is the panacea to the world’s economy.

Is Silicon Valley that far off from solving the conundrum of smooth public transportation by applying technology?

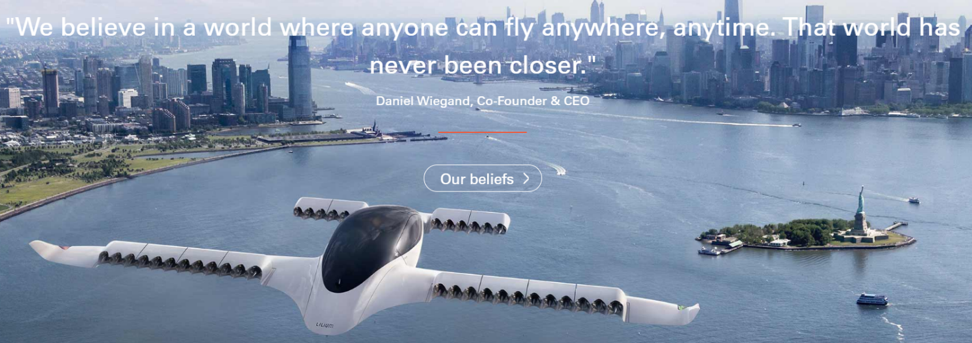

The solution might be percolating in Wessling, Germany by a company named Lilium who developed the Lilium Jet, an electrically powered commuter aircraft capable of vertical taking off and landing (VTOL) flight.

Moving forward, it’s black and white that the answer is 3D and not 2D.

Lilium was founded in 2015 by four engineers and PhD students at the Technical University of Munich.

In 2017, The Lilium Eagle, an unmanned two-seat proof of concept model, performed its initial flight at the airfield Mindelheim-Mattsies near Munich, Germany.

The successful test led the company to launch the 5-seat Lilium Jet and they hope by 2025, to roll out a full-fledged aerial taxi service.

Co-Founder and CEO Daniel Wiegand swears that within five years, a fleet of them could offer a 10-minute trip from Manhattan to Kennedy International Airport for $70.

Expectations that aerial taxis will be a reality in the coming years are quickly skyrocketing.

Companies like Lilium are researching, testing, and laying the groundwork for wider production and hankering for support from government officials.

At least 20 companies have skin in the game, which Morgan Stanley estimates will become a $850 billion market by 2040.

Larry Page, the billionaire co-founder of Google (GOOGL), is financially buttressing Kitty Hawk, a Palo Alto company run by the first engineers on Google’s autonomous car.

Uber is developing an air taxi service, with plans to operate by 2023, but I highly doubt that investors would give the go ahead if the cash burn overwhelms them.

The Federal Aviation Administration (FAA) is another tripwire that could knock the 2025 schedule off kilter and their notorious bureaucratic ways do not infuse certainty into the project.

Can Lilium build a platform that is broadly accessible and efficient?

That answer will be unpacked in the next few years.

The aerial vehicle has a carbon fiber body, 36-foot wingspan, and is battery powered, providing a range of 186 miles and a top speed of nearly 190 mph.

Inside the oblong-shaped cabin, posh seats await four passengers and a pilot.

The aircraft can take off and land vertically like a helicopter and is even quieter than a helicopter.

Once scaled out, production costs will run in the several hundred thousand dollars for each aircraft-making profitability realistic.

There will be lower maintenance costs because there are fewer mechanical components, and rides should cost less than Uber.

If rolled out on a mass scale, cityscapes will be revolutionized.

San Francisco and California effectively could bypass proper land public transport and skip straight to aerial vehicles as taxis.

Lilium’s plane has packed 36 smaller engines in its rotating wings that act as thrusters for takeoffs, landings, and subtle movements forward and back. Encasing the engines in the wings reduces friction and noise.

Lilium’s performance is currently unmatched but its secretive nature of the technology means it’s hard to quantify where they are now in the development.

With the funneling of capital to solve global transportation issues, aerial aspects will definitely be intertwined into the solution.

The race is on to capture the first-mover advantage and my bet it will be Lilium.

“This is the perfect means of transportation, something that can take off and land everywhere.” – Said Co-Founder and CEO Lilium Daniel Wiegand

Mad Hedge Technology Letter

November 11, 2019

Fiat Lux

Featured Trade:

(WALKING A TIGHT ROPE IN MENLO PARK),

(FB),

The countdown has started.

Will regulation meaningfully hit Facebook (FB) where it hurts in 2020 – the wallet?

There is only so much that Co-Founder Mark Zuckerberg and executives in Menlo Park can do to keep regulators at arm’s length.

The Federal Trade Commission (FTC) and Department of Justice (DOJ) want to rearrange Facebook’s business model potentially making it uncompetitive.

In an unusual move, the California's State Attorney General publicly stated that his office has been investigating Facebook's privacy dealings over the past 18 months and the reason we know that is because Facebook is stonewalling the process and actively avoiding the authorities.

The State Attorney General has asked for additional information related to the Cambridge Analytica scandal that rocked Facebook shares last year and the company has yet to fully recover from that strong blow.

Undoubtedly, Facebook wants to conceal its self-inflicted wounds and actively rebuff document request signals that Facebook is ready to withstand the pain.

This is also after Zuckerberg decided to allow politicians to buy ads without any sort of third-party fact-checker.

My guess is that Facebook management has been blackmailing companies left and right and only working with companies in a reasonable way if they are paying Facebook for digital ads.

This is a massive conflict of interest at the heart of Facebook’s practices.

If any company could be labeled amoral and completely indifferent to the gargantuan social cost piling up in the U.S. because of the fallout from their toxic services, Facebook is at the top of the list.

But as long as Zuckerberg keeps inflating the bottom line, which mind you he definitely is and great at, board members dare to speak up.

It’s not like they can do anything anyways, Zuckerberg cannot be fired because of holding generous voting rights.

Facebook is also at the heart of several lawsuits claiming that as soon as Facebook identified them as a serious competitive threat, Facebook pulled their file and denied access to data.

Many companies cannot function without access to Facebook’s platform.

The attorney general is attempting to scoop up the meatiest part of communications between Mark Zuckerberg and Facebook COO Sheryl Sandberg detailing changes to the social network's privacy settings, as well as documentation of the company's privacy program.

There is no way in hell Facebook will let the cat get out of the bag and certainly there is explosive material that would dig the ditch even deeper.

Recently, Zuckerberg has been on the warpath shouting from the hills urging the government to shut down Softbank funded short-form video app TikTok created by Chinese company Bytedance which has gone viral as a social media alternative to Instagram.

Even with a storm brewing ahead, Facebook continues to be a buy on the regulatory dip as investors should not ignore the cash cow digital ad business.

Digital ad buyers aren’t yet diverting ad budgets elsewhere mostly because there aren’t other places to allocate huge amounts of ad dollars to and Facebook knows this.

Another front has opened up as well in the privacy wars with Facebook suing Israel’s NSO Group for selling software allowing governments to spy by breaking into their WhatsApp chat history.

The tracking software named Pegasus even allows for comprehensive access to the camera and microphone and was meant to “fight terrorism.”

As you might believe, governments have liberally applied this software to individuals across the board for their own zero-sum interests.

These revelations could slow down the rollout of digital ads on WhatsApp which Zuckerberg is hellbent on in the next calendar year to drive revenue growth.

A recent report showed that 93% of global internet users are tracked posing a serious threat to the integrity of the internet.

Not only is the government using it for their own economic and political gains, but Facebook is up there pulling the strings behind the scenes too and Facebook’s shares keep climbing.

Until users refuse to log in to Facebook in droves and stop gifting them free data, Facebook continues to be a buy on any pullback.

Sure, the regulatory pressure could eventually blow up in Facebook’s face, but until we receive meaningful signals that Facebook’s ad model is dead, investors shouldn’t write off Zuckerberg and his digital ad money-making machine.

“By giving people the power to share, we're making the world more transparent.” – Said Co-Founder and CEO of Facebook Mark Zuckerberg

Mad Hedge Technology Letter

November 8, 2019

Fiat Lux

Featured Trade:

(WANDERLUST TAKES A HIT),

(TRIP), (EXPE)

I have slaughtered travel tech nonstop for quite a while now and today is the day that the bearishness turned ugly.

Let’s take a look at why.

I believe travel tech is a vulnerable group waiting to be taken to the emergency room.

We are approaching the dying embers of the economic bull cycle for better or worse, mostly the latter.

Europe is already mired in a recessionary-like environment and hiring has ground to a halt.

When German automobile manufacturers aren’t doing well, usually the rest of the continent follows suit.

No new jobs mean no new money to travel with and austerity usually whacks off luxuries like hotel stays and cross border travel.

Reading the tea leaves, it’s hard not to think that travel tech could be in for a rough next year with revenue growth sliding like Expedia’s vacation rental business in the third quarter.

The company is signaling slowed momentum in its high growth category leading to a lowered profit forecast for 2020.

The short-term rental unit reported revenue growth of 14% to $467 million, lower than the 17% rate in the previous period and missed analysts’ estimates of $462.4 million.

Total revenue grew 8.6% to $3.56 billion, in line with consensus but as we turn the page, there’s not much to like.

Expedia attempts to juice up home-sharing division, VRBO, in a quest to unseat rivals Airbnb Inc. and Booking Holdings Inc. in the booming home-share market will fall flat.

While VRBO is strong in the U.S. for purely vacation rentals, Airbnb and Booking capture a much larger share of the broader global $34 billion alternative accommodation market, which also includes non-traditional hotels and home-sharing.

Expedia is now set for 2020 adjusted Ebitda growth of 5% to 9%, down from a previous forecast of 15% growth.

VRBO only pulls in just over 10% of Expedia’s overall revenue, but its growth prospects revolve around this one asset.

To reach its targets, Expedia will need a greater dependence on higher-cost marketing channels in a secular flat hotel ADR (average daily rate) environment while grappling with the uncertainty around VRBO weathering a change in brand name.

Many tech companies are finding out that now is the wrong time to champion growth at any costs and travel tech is grossly reliant on exorbitant marketing costs to drive incremental home-sharing revenue.

I can’t say what TripAdvisor (TRIP) is doing is much better than Expedia because it is certainly not.

They have just announced a joint venture and global licensing agreement with China’s Trip.com Group which includes assets Ctrip, Trip.com, Qunar, and Skyscanner.

This is probably the worst time in the past 30 years for an online travel company to dive straight into China.

As I read through the detail, there was one red flag that stood out and that was the bit about “sharing inventory.”

I am doubtful that TripAdvisor is able to have an enforceable mechanism for misbehavior.

For example, if a hotel booked through TripAdvisor China is rerouted into the Trip.com portfolio and executed by the Chinese mainland array of digital assets, how would TripAdvisor respond?

There are too many lurking risks that could easily result in Trip.com Group gaming this agreement to tilt the benefits in their favor.

A cynical part of me tells me that this is just a ruse for Trip.com Group to use TripAdvisor’s brand name which dominates in western developed countries to siphon away foreign tourism revenue.

On a personal level, I have found that Trip.com Group has subsidized its prices which is a boon to consumers but is a way to undercut and pervert competition.

TripAdvisor can’t operate freely in China as it stands, but I wouldn’t desperately decide on a joint venture just to get a shoe in the door.

Better off looking elsewhere or keeping their ammunition dry.

Whether its weakness in VRBO in Expedia or a poor licensing agreement between TripAdvisor and China’s Trip.com Group, there is a lack of good ideas since Airbnb created this industry out of thin air.

Probably better to wait for Airbnb to go public if you want to get into travel tech, they have revolutionized the industry and are profitable or invest in Google who is stealing market share from the old guard.

The higher competition will certainly lead to higher marketing costs, lower growth, and a race to zero commissions.

“If there's lots of technology, we won't understand it.” – Said American Investor Warren Buffett