Mad Hedge Technology Letter

February 4, 2019

Fiat Lux

Featured Trade:

(WHY AMAZON IS TAKING OVER THE WORLD),

(AMZN)

Mad Hedge Technology Letter

February 4, 2019

Fiat Lux

Featured Trade:

(WHY AMAZON IS TAKING OVER THE WORLD),

(AMZN)

Amazon, being the best publicly traded company in America, has more than one way to skin a cat.

That is what I took away during the mixed bag of an earnings call.

The road forward for most companies are defined by one maybe two unforgiving directions that the company has no choice but to migrate down through no fault of their own due to market forces.

Amazon operates in a different universe and the breadth of optionality for Amazon is breathtaking.

They have chosen to try to spike their future core business which has traditionally proven to pay dividends within three years or less.

Investors have always allowed Amazon to revert back to the reinvestment blueprint for added profitability - profits should reaccelerate once more in 2020.

Take into consideration that 2018 was a “light” year in Amazon’s reinvestment cycle in which Amazon only grew its fulfillment and shipping square footage by 15% and its headcount by 14%.

Amazon has used this playbook before. The warehouse efficiencies that benefited margins in 2018 was a direct result of massive capital expenditures into robot technology in the preceding years before that.

Amazon guided weakly on top line growth because of several regulation quagmires in India.

The Indian government began banning foreign online retailers from selling products from marketplace vendors that they have an equity stake in, leading Amazon to shelf items from its Indian site including its popular Echo speakers.

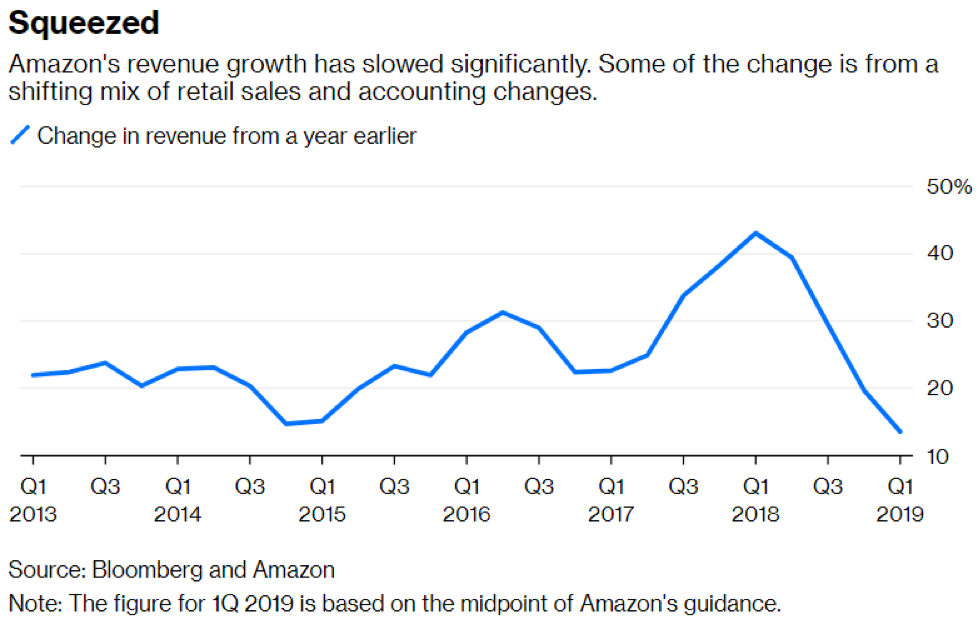

The $72.38 billion translating into 20% YOY fourth quarter revenue growth was its weakest since 2015.

They still have some work to do with physical stores, mostly Whole Foods, which saw a dip of 3% YOY in revenue.

Investors shouldn’t worry too much about this because Amazon can quickly switch back and ramp up revenue expansion when need be.

India is what China was 15 years ago and will morph into its own consumer supergiant with a population to service Amazon sales in the future.

Even with these headwinds that could frustrate operating margins and top-line revenue, Amazon still has some robust drivers in its portfolio in the form of cloud division Amazon Web Services (AWS) that grew 45% YOY and its advertising business which will perpetuate 50% YOY growth trajectory going forward.

Some other highlights were outperformance in voice tech with Amazon CEO Jeff Bezos gloating that “Echo Dot was the best-selling item across all products on Amazon globally, and customers purchased millions more devices from the Echo family compared to last year.”

In hindsight, the report wasn’t bad considering Q4 is the quarter Amazon usually diverges the most with expectations because of the sky-high expectations of the Christmas season.

Digital advertising is already a $12 billion-plus annual business and earned Amazon over $3 billion last quarter.

These lucrative businesses give Amazon more leeway into combatting headwinds that slow down its e-commerce engine.

The e-commerce side of business changes rapidly causing capital to be earmarked for reinvestment as others catch up to its latest iteration of Amazon.com.

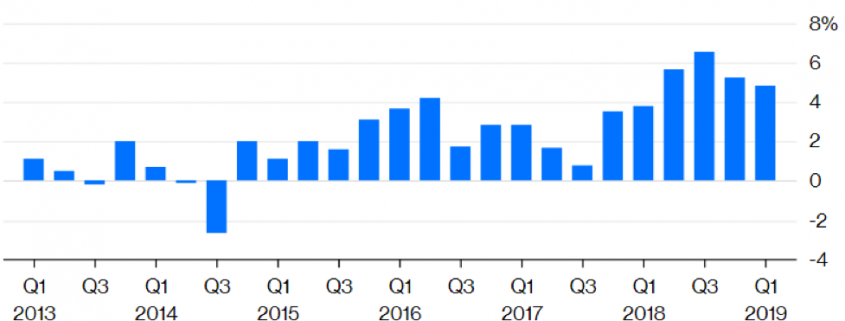

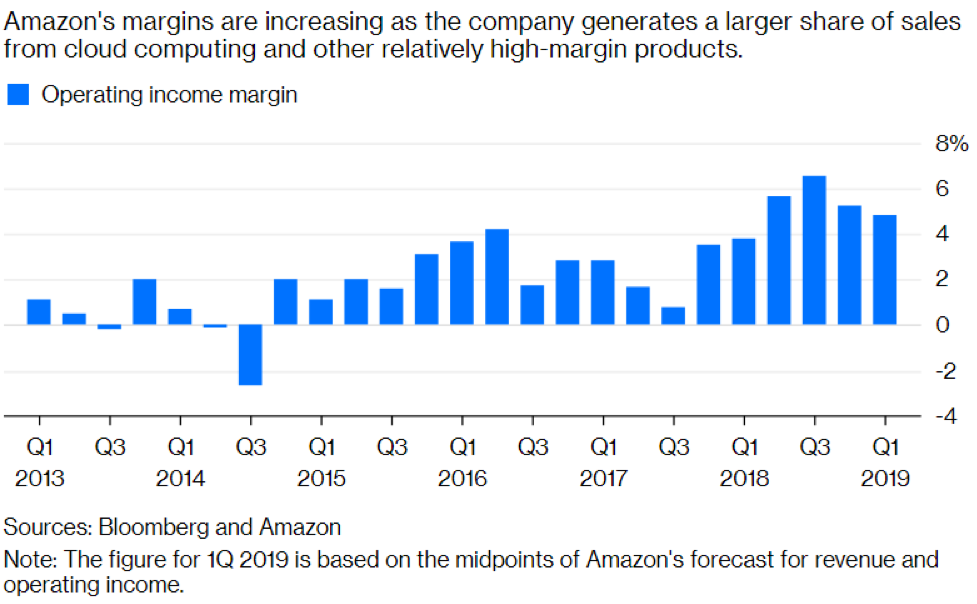

That being said, operating income margins are still over 4% and for the business model Amazon is trotting out, it is still a healthy number.

Not only that, AWS’ margins still remain intact at a robust 29%.

Consumers will agree with you admitting they can visibly notice the e-commerce platform improving over time.

The mixed results dinged shares 4% and I would classify this as a positive down day considering that from peak to trough, Amazon gained 35% after the December sell-off.

If these earnings came out in December, I would not have been shocked with a 15% haircut, but this speaks volumes to how tech shares have been resilient.

And tech earnings, for the most part, have been encouraging relative to expectations.

The change in rules has bred uncertainty in its Indian operation and management will wait for the dust to settle to carve out a plan ahead, but this is small potatoes in the larger picture because of the cash cow that is rich western countries.

To sum things up, Amazon’s services and e-commerce platform is still humming along, but growth is tapering off just a tad.

Amazon plans to juice up their business model by reinvesting into their model extracting the bounty in the years ahead.

The lead up to this will be a broad-based harvest resulting in stock price acceleration.

Do not forget we just went through a global growth scare, and I still believe that if the overall market will rise, the tech sector will need to participate with the bigger names carrying a substantial load.

An even more positive signal are the likes of Facebook, Apple, and Netflix buoying nicely, boding well for short-term price action.

This all means that Amazon should be a buy on the dip company with its long-term growth story more attractive than any other tech name, and by a wide margin.

Margins could come down temporarily in the spring and summer offering weakness for investors to buy into.

Amazon is truly a multi-dimensional beast that uses its capital wisely to create red hot businesses that never existed before.

Such is the magnitude of innovation at Amazon to the point that I would argue that Amazon is the most innovative American company today, period.

I sit on the edge of my seat to see what Amazon does next and you should too.

The easiest way to play this is to buy and hold shares for the long term on any major ephemeral stock offloading because they dominate like any other company in their field in relative terms.

Amazon will be back above 2,000 later in 2019 or early 2020.

“One of the huge mistakes people make is that they try to force an interest on themselves. You don’t choose your passion; your passion chooses you.” – Said CEO of Amazon Jeff Bezos

Mad Hedge Technology Letter

January 31, 2019

Fiat Lux

Featured Trade:

(APPLE SEIZES VICTORY FROM THE JAWS OF DEFEAT),

(AAPL)

After an almost 40% swan dive, Apple has found solid footing at these levels for the time being. 40% seems to be the magic number. Declines ALWAYS end at 40% with Apple.

About time!

It’s been an erratic last few months for the company that Steve Jobs built and this last earnings report will go a long way to somewhat stabilize the short-term share price.

The miniscule earnings beat telegraphs to investors that the bad news has been sucked out.

That is what Tim Cook wants the investor community to think.

But is he right?

I would argue that the bad news is over for the short-term but could rear its ugly head again later – it all rides on China’s shoulders.

Let’s take a look at the numbers.

Chinese revenue was down 27% YOY locking in $13.17 billion in quarterly revenue compared to $17.96 billion the prior year.

There is no two ways about this – it’s an awful number and a hurtful manifestation of the Chinese economy decelerating.

The unrelenting pressure of the geopolitical trade war has handcuffed Beijing’s drive to deleverage its balance sheet and steer its economy to a more consumption-supportive model.

China is lamentably back to its traditional ways - the old economy - infusing $2.2 trillion into its balance sheet along with cutting the reserve ratio for state banks hoping to incite economic growth.

Positive short-term catalyst but negative long-term consequences.

This is why I urged Apple lovers to stay away from this stock earlier because of the uncertainty of its current strategic position.

It makes no sense to place an indirect on the current Washington administration navigating a China soft landing.

As it stands, most of Apple’s supply chain is in China and moving it out will be done in piecemeal which is happening behind the scenes and will cause massive job loss in China further hurting the Chinese economy.

The ratcheting up of tensions signals the untenable end of American tech supply chains in China and no new foreign investment will pour into China.

Maybe even never.

I wholeheartedly blame CEO of Apple Tim Cook for not foreseeing this development.

That is what he is paid to do.

Then there is the issue of iPhone sales in China.

Chinese citizens aren’t buying iPhones because of three reasons.

The cohort of wealthy Chinese who can afford a $1,000 iPhone might think twice if they want to be seen outside with a product from a country that is becoming adversarial. Apple has incurred hard-to-quantify brand damage to its once pristine brand in a land that once worshipped the company.

The refresh cycle has elongated because Apple manufactures great smartphones and iPhone holders are waiting it out on the sidelines two or even three iterations down the road to upgrade because that is when they can unearth the relative value of the product.

Lastly, local Chinese smartphone markers have greatly enhanced their products because of a function of time and borrowed Western technology. It is now possible to buy a smartphone that offers around 80% of performance and functionality of an iPhone but for less than half the price.

The customers on the fence who once viewed iPhones as a must-buy are now migrating to the local Chinese competitor because they are a relatively good deal.

I can surmise that these three headwinds are just beginning and will become more entrenched over time.

If the trade war becomes worse, the brand damage will accelerate. iPhones are becoming incrementally better which will delay new iPhone upgrades unless something revolutionary comes out that requires customers to upgrade to be a part of the new technology.

And sadly, Chinese competition is catching up quicker than Apple can innovate and that will not stop.

However, the silver lining is that the worst-case scenario won’t happen in the next quarter and the market won’t get wind of this until the second half of the year.

Instead of a meaningful sell-off because of this earnings report, Cook chose to front-run the weakness by reporting the hideous performance at the beginning of January.

Cook knew he needed to come clean with the negative news and the reformulated projections that were re-laid a few weeks ago were the same ones that Apple barely beat by one cent on the bottom line by posting EPS of $4.18 and marginally on the top line by $420 million.

I am in no way saying that this was a great earnings report – it wasn’t.

Apple mainly delivered on the mediocrity that they discussed a few weeks ago lowering the bar to the point where it would be a failure of epic proportions if Apple couldn’t beat significantly revised down earnings.

Then the outlook for the next quarter wasn’t as bad as people thought, but that doesn’t mean it was good.

When you start playing the game of not as bad as the market thought – it is a slippery slope to head down and halfway to the CEO getting sacked down the road.

I mentioned before that the macro headwinds came 2 years too early for Cook and pegging 60% of company revenue to a smartphone which has trended towards mass commoditization is a bad bet.

Cook has been painstakingly slow rewriting Apple as a service company which is his current get-out-of-jail-free card dangling in front of him like a juicy carrot.

iPhone gross margin is now 34.3% which is lower than the other Apple products whose margins are 38%.

Their flagship product isn’t as profitable on a per-unit basis as it once was highlighting the necessity for refreshing the product lines with not just new iterations but game-changing products.

The type of products that Steve Jobs used to mushroom popularity would suffice.

Gross margins will continue to come down as the smartphone market is saturated and customers won’t buy iPhones now unless they receive a drastic price reduction.

The result is that Apple no longer publishes iPhone unit sales to conceal the worst number for their most important and volume-heavy product.

A little too late if you tell me and irresponsible to investor transparency if you ask me.

Apple Pay, Apple Music, and iCloud storage eclipsed $10.9 billion demonstrating a 19% YOY increase.

This shows that this company still has strengths, but don’t forget that services are still less than 15% of total revenue even though they are the fastest growth part of their portfolio.

Cook isn’t doing enough to supercharge the content and services at Apple.

The top line number was $84.3 billion, a 5% YOY decline in revenue – a YOY decline hasn’t happened in 18 years and this is deeply troublesome.

Let me explain why Cook is the center of the problem.

The underlying issue is Cook doesn’t know what product should be next for Apple.

Apple dabbled with the Apple TV which didn’t pan out.

Then the autonomous vehicle unit just closed down sacking 200 employees.

And the content side of it hasn’t been developed fast enough relative to the slowing down of iPhone sales which is why you can blame Cook for being reactive instead of proactive.

It’s not like he can claim that his head was in the sand and couldn’t take note of what Netflix was doing and had gotten into that original content game sooner.

The hesitation is exactly what worries me with Cook. Cook is a great operations guy and can take an existing product, beef up margins, shave down expenses, streamline execution and boost top and bottom line profits.

Cook is being painfully exposed now that he is out of his comfort zone and must aggressively move in a direction that doesn’t have a red carpet laid out for him.

Even though the pre-earnings red flag raised many questions, Cook only satisfied these red flags on a short-term basis and Apple still needs to reconfigure its product roadmap for the long term.

If Cook plans to milk more out of the iPhone story, Apple becomes a sell the rallies stock, but the market will give the benefit of the doubt to Apple for a quarter or so.

The 800-pound gorilla in the room is the Chinese economy which could go into a hard landing if the stimulus fails to deliver economic respite or if the trade war tensions are exacerbated.

At the bare minimum, the waterfall of downgrades should be over for the time being, but this will come to the fore in a quarter or so when Apple will need to shine light on its plans moving forward.

I wouldn’t bet the ranch on Cook being innovative.

It looks like Apple will start to trade in a range.

It’s hard to believe any bad news superseding what came out at the beginning of this month in the short-term, but at the same time, there are no idiosyncratic catalysts to cause this stock to bullishly break out.

We are at an inflection point in Cook’s career and he is finding out that it's not as easy to be Apple as it used to, and mammoth decisions are on the horizon that must be addressed or possibly become the next IBM.

If you ask me, I’ve been calling on Apple to replace Cook for a while with Jack Dorsey as the signal caller, I still believe this is the only way to stay in the heavyweight division of tech titans five years from now.

Such is the competitive nature of the tech landscape these days.

Mad Hedge Technology Letter

January 30, 2019

Fiat Lux

Featured Trade:

(IS THE BOTTOM IN FOR FACEBOOK?),

(FB)

As much as I malign Facebook (FB) CEO and Founder Mark Zuckerberg, the risk-reward for Facebook’s earnings that come out after Wednesday’s close favor the upside.

Let me explain.

I have been bearish on this name for quite a while and I have been rewarded in spades.

From the Cambridge Analytica leak to firing the heads of Instagram and WhatsApp, last year was a year to forget and the stock was crushed.

This time, it’s a little different.

I believe the saturated business model has largely been priced in to the stock and the company is transitioning to a more lucrative side of the business with other levers they can pull.

Facebook can’t move mountains to raise the needle in the number of users in the western developed world.

The rich western world is Facebook’s profit engine with average revenue per user remarkably higher than its emerging user audience.

The company will change tact and seek to increase average revenue per user because of decelerating usership.

Emerging markets are the last bastion of growth for its user base, but unfortunately, this source of new users cannot be lucratively monetized like its staunch North America and Western European cash cows.

The lion's share of new users are from countries including India, Indonesia and Philippines where advertisers focus more on TV, print and physical advertising.

Expect Facebook to announce slowing user growth in the low single digits.

This likely won’t be a surprise to markets along with more rumblings about the average age of user increasing as Generation Z flees the platform.

The silver lining in this development is that Generation Z is fleeing Facebook and migrating to Instagram which is also owned by Facebook and a hyper-growth engine.

Even with the younger generation deleting Facebook in droves, Facebook still has a base of over 2 billion and every one of these customers use one of Facebook’s four services every day.

That is partly why it is attractive to digital advertisers and Facebook culls 98% of total revenue from ads.

If you forgot about last quarters earnings, Facebook handily beat EPS forecasts by 30 cents and barely missed on the top line, and that was in the face of disturbing ructions of a full-on regulation tech lash.

The first stage of negative regulation and the fallout have effectively been absorbed by the market and the second stage isn’t visible on the horizon as of today.

That day will eventually come but not before they come out with earnings later today, and not where near-term guidance will be materially affected.

If you read Mark Zuckerberg’s New York Times op-ed, he still believes that any road bump can be parsed over with marketing gibberish, and I would agree that the next stage of regulation that could damage the company is far away enough that this stall tactic will work for this particular earnings report.

However, this myopic and dangerous strategy must be managed quarter to quarter. There will be a time when the market needs to hear how Facebook will actually fix the model if a new wave of tech fury erupts.

The firm is safe now as the general trend for more robust regulation has started muted at the beginning of 2019 with congress and the administration busy with a closed government and political infighting bordering insanity.

This type of national news jumps to the forefront and pushes back the possible timeline for enforced regulation especially when 800,000 government workers were broadsided and couldn’t put food on the table or pay their rent.

To follow up on the political front, management is sure to take last year’s midterm election success and milk it for all its worth.

There were no disastrous scandals, recounts, or platform manipulation that could potentially do harm to the stock.

Facebook will tout this as a sign that its controls are starting to reap dividends and concrete evidence that they have shaped up since the Russian interference compromised the business model during last presidential election.

In late 2018, Facebook forecasted expenses to grow 40%-50% in 2019.

The headline expense number was set astronomically high in order for management to easily beat forecasts and announce that today.

Since management has categorized many material problems as marketing fixes, they have normalized doing the bare minimum as a stopgap measure masquerading as a real, full blown fix.

The one insight that keeps slamming me straight in the face like a gale force wind is that Zuckerberg likes his money which means he needs the stock to go up.

That would be the pitiful reason he offers these half-baked excuses as legitimate fixes because he understands that comprehensive solutions would be too costly damaging future earnings.

He also needs the stock to go up because many of the new faces at Facebook are compensated by stock because of a lack of cash on hand.

What is a meaningful catalyst to take Facebook higher?

The firings of the heads of WhatsApp and Instagram paved the way for the transition to 2019 where Facebook will monetize these other two services as well as integrating the back-end with Facebook.

This is viewed as the holy grail of Facebook growth and Zuckerberg incessantly refuted this would ever happen.

Well, the cat is out of the bag now.

In integrating the back-end of these three services, Facebook will extract a deeper insight into the behavior of their usership with a 360 degree view of their daily habits.

This deeper understanding of behavior will allow them to harvest the data in a way that is more valuable to digital ad buyers.

Facebook plans to compensate the lack of user growth for higher quality ads, and in turn they will be able to charge the ad buyers more per ad.

This strategy is a high risk, high reward maneuver because the company will intrude more into the personal data of their users than ever before.

On a business level, Zuckerberg has few options left up his sleeve and is predictably migrating towards the low hanging fruit as well as his best option today.

There is not much juice he can squeeze out of dinosaur Facebook anymore and margins will come down from now on.

However, WhatsApp and Instagram are fertile pastures for Zuck to wield his ad-hawking expertise.

Readers might forget that there are no ads on WhatsApp yet and its virgin provenance has been left largely unchanged from the beginning offering Zuck a golden project to mold his paws on.

If the CEO of Facebook goes into details about Facebook’s plan to ramp up these two social media platforms, the stock has a good chance to react positively.

The bar has been set quite low and Facebook has targeted this earnings report as an inflection point in the company’s history as they begin to pull alternative levers available to them.

This is a short-term prognosis in an otherwise murky future for the company.

Challenges are endless and part of the ceaseless issues involves Facebook not adding any real value as a technology platform or not possessing any ground-breaking technology or proprietary software.

Facebook is the used car salesman of the tech world and they are doing everything they can to stay relevant.

If Facebook does sell off after the WhatsApp and Instagram integration announcement, it is safe to deduce that Facebook is out of bullets and the stock becomes a sell on the rallies company until they can do something to stem the blood flow.

“We all have shortcomings.” – Said Chief Operating Officer of Facebook Sheryl Sandberg

Mad Hedge Technology Letter

January 29, 2019

Fiat Lux

Featured Trade:

(WHATS BEHIND THE NVIDIA MELTDOWN),

(QRVO), (MU), (SWKS), (NVDA), (AMD), (INTC), (AAPL), (AMZN), (GOOGL), (MSFT), (FB)

Great company – lousy time to be this great company.

That is the least I can say for GPU chip company Nvidia (NVDA) who issued a cataclysmic earnings alert figuring it was better to spill the negative news now to start the healing process earlier.

This stock is a great long-term hold because they are the best of breed in an industry fueled by a secular tailwind in GPUs.

But this doesn’t mean they will be gifted any freebies in the short term and, sad to say, they have been dragged, kicking and screaming, into the heart of the trade skirmish along with Apple (AAPL) and buddy Intel (INTC) amongst others.

The best thing a tech company can have going for them right now is to have no China exposure, that is why I am bullish on software companies such as PayPal, Twilio, and Microsoft.

I called the chip disaster back in summer of 2018 recommending to stay away like the plague.

The climate has worsened since then and like I recently said – don’t buy the dead cat bounce in chips because the bad news isn’t baked into the story yet or at least not fully baked.

It’s actually a blessing in disguise if banned in China if you are firms such as Facebook (FB), Google (GOOGL), and Amazon (AMZN).

I recently noted that a material end to this trade war could be decades away and the tech world is already being reconfigured around the monopoly board as we speak with this in mind.

Where do things stand?

The US administration took a scalp when Chinese communist backed DRAM chip maker Fujian Jinhua effectively shuttered its doors.

Victory in a minor battle will likely embolden the US administration into continuing its aggressive stance if it is working.

If you forgot who Fujian Jinhua was… they are the Chinese chip company who were indicted by the U.S. Justice Department for stealing intellectual property (IP) from Boise-based chip behemoth Micron (MU).

The way they allegedly stole the information was by poaching Taiwanese chip engineers who would divulge the secrets to the Chinese company buttressing China in pursuing their hellbent goal of being able to domestically supply enough quality chips in order to stop buying American chips in the future.

Officially, China hopes to ramp up its self-sufficiency ratio in the semiconductor industry to at least 70% by 2025 which dovetails nicely with the broader goal of Chinese tech hegemony.

Fujian Jinhua was classified as a strategically important firm to the Chinese state and knocking the wind out of their sails will have a reverberating effect around the Chinese tech sector and will deter Taiwanese chip engineers to act as a go-between.

According to a research note by Zhongtai Securities, Jinhua’s new plant was expected to have flooded the market with 60,000 chips per month and generate annual revenue of $1.2 billion directly competing with Micron with their own technology borrowed from Micron themselves.

Jinhua’s overall goal was to support a monthly manufacturing target of 240,000 chips spoiling Chinese tech companies with a healthy new stream of state-subsidized allotment of chips needed to keep costs down and build the gadgets and gizmos of the future.

For the most part, it was unforeseen that the US administration had the gall and calculative nous to combat the nurtured Chinese state tech sector.

However, I will say, it makes sense to pick off the Chinese tech space now before they stop needing American chips at all in 5-7 years and when all remnants of leverage disappear.

The short-term pain will be felt in the American chip tech sector which is evident with the horrid news Nvidia reported and the aftermath seen in the price action of the stock.

Nvidia expects top line revenue to shrink by $500 million or half a billion – it’s been a while since I saw such a massive cut in forecasts.

Half of revenue comes from the Middle Kingdom and expect huge downgrades from Apple on its earnings report too.

If this didn’t scare you, what will?

These short-term headwinds are worth it to the American tech sector as a whole.

To eventually ward off a future existential crisis when Chinese GPU companies start offering outside business actionable high quality chips curated with borrowed technology, funded by artificially low debt, and for half the price is worth its weight in gold.

The same story is playing out with Huawei around the globe but at the largest scale possible.

This is what happens when the foreign tech sector is up against companies who have access to unlimited state loans and is part of wider communist state policy to take over foundational technology globally.

I will also emphasize that the Chinese communist party has a seat on every board at any notable Chinese tech company influencing decisions at the top even more than the upper management.

If upper management stopped paying heed to the communist voice at the table, they would be out of business in a jiffy.

Therefore, Huawei founder Ren Zhengfei standing at a podium promulgating a scenario where Huawei is operating freely from the government is what dreams are made of.

It’s not a prognosis rooted in reality.

The communist party are overlords breathing down the neck of Huawei after any material decisions that can affect the company and subsequently the government’s position in the interconnected world.

The China blue print essentially entails a pan-Amazon strategy emphasizing large volume – low cost strategy.

Amazon was successful because investors would throw money at the company until it scaled up and wiped the competition away in one fell swoop.

Amazon is on a destructive path bludgeoning every American second-tier mall reshaping the economic world.

The unintended consequences have been profound with the ultimate spoils falling at the feet of CEO and Founder of Amazon Jeff Bezos, his phalanx of employees as well as Amazon stockholders which are mostly comprised of wealthy investors.

Well, Chairman Xi Jinping and the Chinese communist party are attempting to Amazon the American tech sector and the broader American economy.

The American economy could potentially become the second-tier mall in this analogy and the game playing out is an existential crisis for the likes of Advanced Micro Devices (AMD), Nvidia, Micron, Intel and the who’s who of semiconductor chips.

If stocks reacted on a 30-year timeframe, Nvidia would be up 15% today instead of reaching a trading day nadir of 17%.

What is happening behind the scenes?

American tech companies are moving supply chains or planning to move supply chains out of China.

This is an epochal manifestation of the larger trade war and a decisive development in the eyes of the American administration.

In fact, many industry analysts understand a logjam of failed trade solutions as a bonus to the Chinese.

However, I would argue the complete opposite.

Yes, the Chinese are waiting out the current administration to deal with a new one that might be more lenient.

But that will take another two years and publicly listed companies grappling with the performance of quarterly earnings don’t have two years like the Chinese communist party.

And who knows, the next administration might even seize the baton from the current administration and clamp down even more.

Be careful what you wish for.

Taiwanese company and biggest iPhone assembler Foxconn Technology Group is discussing plans to move production away from China to India.

India is a democratic country, the biggest democracy in Asia, and is a staunch ally of the United States.

CEOs of Google (GOOGL) and Microsoft (MSFT), some of Silicon Valley heavyweights, are from India and American tech companies have been making generational tech investments in India recently.

Warren Buffet even invested $300 million in an Indian FinTech company Paytm.

When you read stories about India being the new China, well it’s happening faster than anyone thought and on a scale that nobody thought, and the underlying catalyst is the overarching trade war fueling this quick migration.

Apple is already constructing low grade iPhones in India in the state of Karnataka since 2017, and these were the first iPhones made in India.

They won’t be the last either.

Wistron, major Taiwanese original design manufacturer, has since started producing the iPhone 6S model there as well.

And it is no surprise that China and its artificially priced smartphones have undercut Samsung and Apple in India grabbing the market share lead.

This is happening all over the emerging world.

And don’t forget if U.S. President Donald Trump revisits banning American chip companies supply channels to Chinese telecom company ZTE. That would be 70,000 Chinese jobs out the window in a nanosecond.

The current administration has drier powder than you think and this would hasten the deceleration of the Chinese economy and also move forward the American recession into 2019 boding negative for tech shares.

Therefore, I would recommend balancing out a trading portfolio with overweights and underweights because it is obvious that tech stocks won’t be coupled to a gondola trajectory to the peak of the summit this year.

It’s a stockpickers market this year with visible losers and winners.

And if China does get their way in the tech war, American chip companies will eventually become worthless squeezed out by mainland competition brought down by their own technology full circle.

They are first on the chopping board because their overreliance on Chinese revenue streams for the bulk of sales.

Among these companies that could go bust are Broadcom (AVGO), Qualcomm (QCOM), Qorvo (QRVO), Skyworks Solutions (SWKS) and as you expected Micron and Nvidia who are one of the main protagonists in this story.