Mad Hedge Technology Letter

January 28, 2019

Fiat Lux

Featured Trade:

(BUY DIPS IN SEMIS, NOT TOPS),

(XLNX), (LRCX), (AMD), (TXN), (NVDA), (INTC), (SOXX), (SMH), (MU), (QQQ)

Mad Hedge Technology Letter

January 28, 2019

Fiat Lux

Featured Trade:

(BUY DIPS IN SEMIS, NOT TOPS),

(XLNX), (LRCX), (AMD), (TXN), (NVDA), (INTC), (SOXX), (SMH), (MU), (QQQ)

Don’t buy the dead cat bounce – that was the takeaway from a recent trading day that saw chips come alive with vigor.

Semiconductor stocks had their best day since March 2009.

The price action was nothing short of spectacular with names such as chip equipment manufacturer Lam Research (LRCX) gaining 15.7% and Texas Instruments (TXN) turning heads, up 6.91%.

The sector was washed out as the Mad Hedge Technology Letter has determined this part of tech as a no-fly zone since last summer.

When stocks get bombed out at these levels - sometimes even 60% like in Lam Research’s case, investors start to triage them into a value play and are susceptible to strong reversal days or weeks in this case.

The semi-conductor space has been that bad and tech growth has had a putrid last six months of trading.

In the short-term, broad-based tech market sentiment has turned positive with the lynchpins being an extremely oversold market because of the December meltdown and the Fed putting the kibosh on the rate-tightening plan.

Fueled by this relatively positive backdrop, tech stocks have rallied hard off their December lows, but that doesn’t mean investors should take out a bridge loan to bet the ranch on chip stocks.

Another premium example of the chip turnaround was the fortune of Xilinx (XLNX) who rocketed 18.44% in one day then followed that brilliant performance with another 4.06% jump.

A two-day performance of 22.50% stems from the underlying strength of the communication segment in the third quarter, driven by the wireless market producing growth from production of 5G and pre-5G deployments as well as some LTE upgrades.

Give credit to the company’s performance in Advanced Products which grew 51% YOY and universal growth across its end markets.

With respect to the transformation to a platform company, the 28-nanometer and 16-nanometer Zynq SoC products expanded robustly with Zynq sales growing 80% YOY led by the 16-nanometer multiprocessor systems-on-chip (MPSoC) products.

Core drivers were apparent in the application in communications, automotive, particularly Advanced Driver Assistance Systems (ADAS) as well as industrial end markets.

Zynq MPSoC revenues grew over 300% YOY.

These positive signals were just too positive to ignore.

Long term, the trade war complications threaten to corrode a substantial chunk of chip revenues at mainstay players like Intel (INTC) and Nvidia (NVDA).

Not only has the execution risk ratcheted up, but the regulatory risk of operating in China is rising higher than the nosebleed section because of the Huawei extradition case and paying costly tariffs to import back to America is a punch in the gut.

This fragility was highlighted by Intel (INTC) who brought the semiconductor story back down to earth with a mild earnings beat but laid an egg with a horrid annual 2019 forecast.

Intel telegraphed that they are slashing projections for cloud revenue and server sales.

Micron (MU) acquiesced in a similar forecast calling for a cloud hardware slowdown and bloated inventory would need to be further digested creating a lack of demand in new orders.

Then the ultimate stab through the heart - the 2019 guide was $1 billion less than initially forecasted amounting to the same level of revenue in 2018 - $73 billion in revenue and zero growth to the top line.

Making matters worse, the downdraft in guidance factored in that the backend of the year has the likelihood of outperforming to meet that flat projection of the same revenue from last year offering the bear camp fodder to dump Intel shares.

How can firms convincingly promise the back half is going to buttress its year-end performance under the drudgery of a fractious geopolitical set-up?

This screams uncertainty.

Love them or crucify them, the specific makeup of the semiconductor chip cycle entails a vulnerable boom-bust cycle that is the hallmark of the chip industry.

We are trending towards the latter stage of the bust portion of the cycle with management issuing code words such as “inventory adjustment.”

Firms will need to quickly work off this excess blubber to stoke the growth cycle again and that is what this strength in chip stocks is partly about.

Investors are front-running the shaving off of the blubber and getting in at rock bottom prices.

Amalgamate the revelation that demand is relatively healthy due to the next leg up in the technology race requiring companies to hem in adequate orders of next-gen chips for 5G, data servers, IoT products, video game consoles, autonomous vehicle technology, just to name a few.

But this demand is expected to come online in the late half of 2019 if management’s wishes come true.

To minimize unpredictable volatility in this part of tech and if you want to squeeze out the extra juice in this area, then traders can play it by going long the iShares PHLX Semiconductor ETF (SOXX) or VanEck Vectors Semiconductor ETF (SMH).

In many cases, hedge funds have made their entire annual performance in the first month of January because of this v-shaped move in chip shares.

Then there is the other long-term issue of elevated execution risks to chip companies because of an overly reliant manufacturing process in China.

If this trade war turns into a several decades affair which it is appearing more likely by the day, American chip companies will require relocating to a non-adversarial country preferably a democratic stronghold that can act as the fulcrum of a global supply chain channel moving forward.

The relocation will not occur overnight but will have to take place in tranches, and the same chip companies will be on the hook for the relocation fees and resulting capex that is tied with this commitment.

That is all benign in the short term and chip stocks have a little more to run, but on a risk reward proposition, it doesn’t make sense right now to pick up pennies in front of the steamroller.

If the Nasdaq (QQQ) retests December lows because of global growth falls off a cliff, then this mini run in chips will freeze and thawing out won’t happen in a blink of an eye either.

But if you are a long-term investor, I would recommend my favorite chip stock AMD who is actively draining CPU market share from Intel and whose innovation pipeline rivals only Nvidia.

“Simply put: We don't build services to make money; we make money to build better services.” - said Facebook CEO Mark Zuckerberg.

Mad Hedge Technology Letter

January 24, 2019

Fiat Lux

Featured Trade:

(ACTIVISTS LAY IN ON EBAY),

(EBAY), (AMZN), (PYPL), (GOOGL)

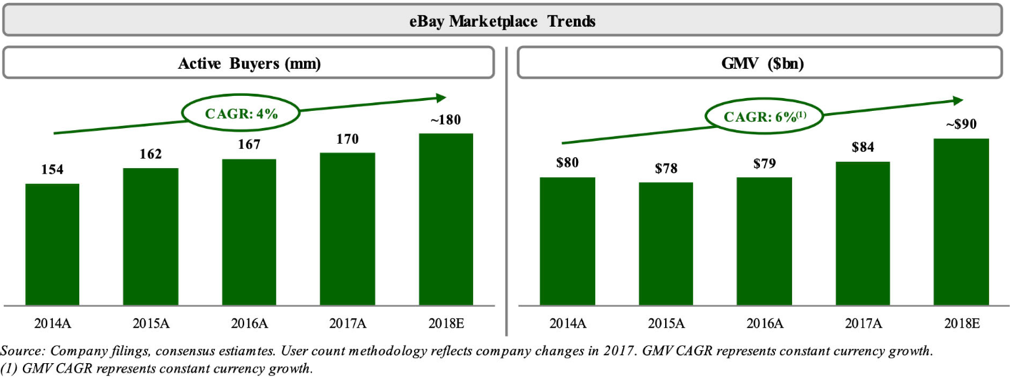

A highly compelling argument – that was my initial reaction after diving into Elliot Management’s letter to eBay’s (EBAY) shareholders after the ruthless investor activist announced an over 4% stake in one of the original online marketplace giants.

Not only that, hedge fund Starboard Value LP also has gotten in on the act with a position of less than 4%.

Starboard has doubled down agreeing with the general points of Elliot Management’s prognosis on the weakness of eBay’s business model

There are no two ways about it - eBay has been condemned to tech purgatory as of late and is in dire need of a facelift.

If you’re a manager of any sort of magnitude at e-commerce platform eBay, this was the letter of doom and gloom you hoped you would never get.

The equity Gods have been harsh to eBay as PayPal (PYPL), one of the Mad Hedge Technology Letter’s favorite picks in 2019, has risen over 130% after spinning off from eBay in 2015.

eBay is down substantially since that point in time reflecting a poorly run business in a secular growth industry that has produced home runs most evident in the performance of Jeff Bezos’ Amazon.com (AMZN).

The gist of Elliot’s diagnosis centered around the terrible operational execution at the Silicon Valley firm.

It essentially repeats this premise over and over throughout the content.

Current management is historically bad that any efficiencies implemented into the platform would boost growth reverting it back to a point closer to a trajectory that echoes closer to a normal high growth e-commerce company.

How did eBay peter out to mediocrity?

Let me explain.

There is a time-established pattern that Elliot Management identified – eBay management increasing spend to stimulate growth, failing to deliver the goods and reverting back to square one.

The result is paltry growth in the mid-single digits which can be seen in minimal growth numbers in the gross merchandise volume (GMV), a metric established to gauge the total amount of volume pushed through eBay.

The activist hedge fund claimed that shares could potentially double if their calculated plan could shortly be deployed.

The plan was straight forward and there was no innovative x-factors described or pivot to augmented reality or machine learning that many firms like to hype up.

Elliot’s strategy is purely operational relating to the core business – where is Tim Cook when you need him!

The argument originates from whether eBay management can allocate resources more efficiently, focus on boosting foundational growth in the core marketplace, and develop new verticals that were completely missed in its development, then the stock would react favorably.

I would even double down and say that if they do half of what they promise in the Elliot’s letter, shares should pop at least 30%.

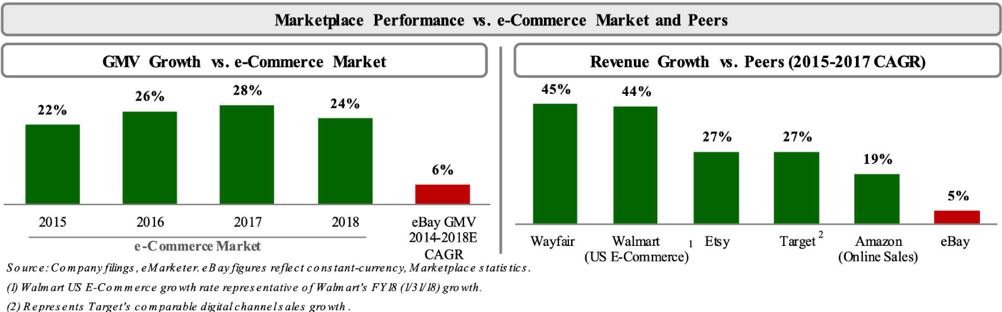

eBay exists under a backdrop of massive secular drivers fueling e-commerce.

The industry is the most robust in the economy and is expanding in the mid-20% even as global sales are about to eclipse the $3 trillion mark.

E-commerce just has a penetration rate of 10% and the runway is long which should enable mainstay companies to grow their top and bottom line if not botched completely.

Average consumer spending is in the throes of major disruption from analog brick and mortar stores to digital e-commerce, and eBay’s strategic position offers an advantageous platform to carve out e-commerce success moving forward.

The first thing Elliot wants to do is reach up their sleeve for a little financial engineering magic by spinning out in-house mega-growth assets of StubHub, the e-ticket event vendor, and its portfolio of premium classified properties that possess double-digit sales growth and elevated margins.

Elliot argues that these two assets would perform better on a standalone basis because they wouldn’t be bogged down by eBay turning around the core business which could possibly result in some misallocated capital and delays.

The valuation of eBay’s Classified Groups assets is around $4.5 billion, but segment that out and the value could represent $10 billion.

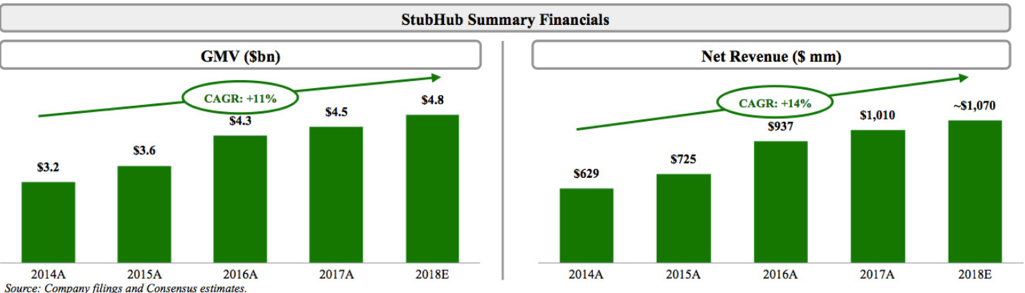

The same boost in valuation applies to event ticket seller platform StubHub. The company is valued at just $2.2 billion under the umbrella of eBay but tear the baby out of eBay’s uterus and suddenly the valuation balloons to a rosier $4 billion.

Watching from afar, Elliot has pinpointed management’s “self-inflicted mis-execution” and management must summon all their power and resources to direct “singular attention to growing and strengthening marketplace.”

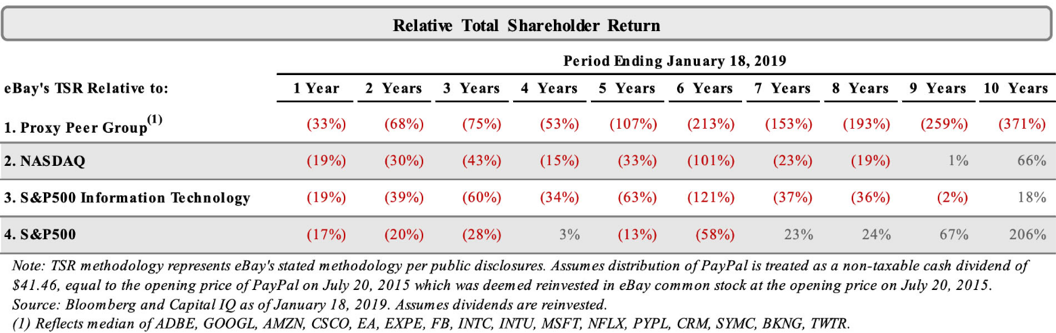

eBay has severely underperformed in share price relative to its peers by 107% in the past 5 years. Extrapolate the time horizon to 10 years and the underperformance shoots up to 371%.

These have been the tech golden years and there is no feasible excuse to why this company hasn’t been able to perform better or equal relative to their peer group.

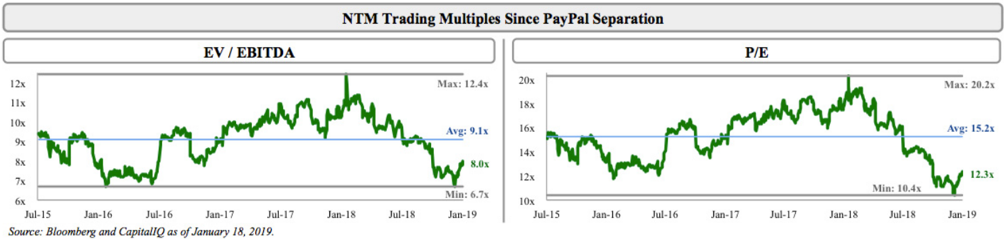

eBay is the second biggest e-commerce platform in the world but only trades at a PE of 12 showing the malaise of investor sentiment surrounding this name.

This is unfortunate because eBay has strong embedded actionable communities in South Korea, Australia, Italy, Germany, U.K., U.S., and Canada.

The tools are there but it is hard to take a stab when the tool is blunted by poor management.

Compare slow growth with the rocket-fueled growth of asset StubHub which has almost doubled revenue in the past 5 years.

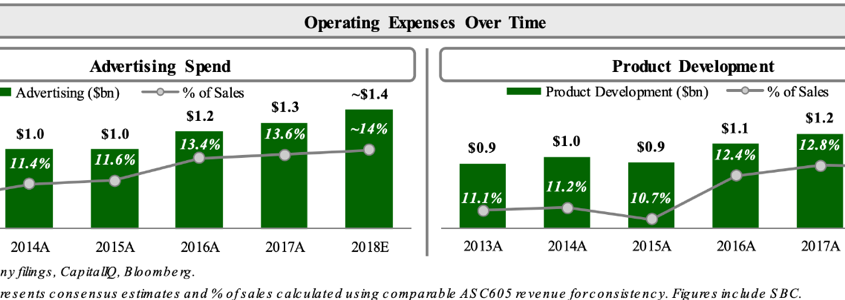

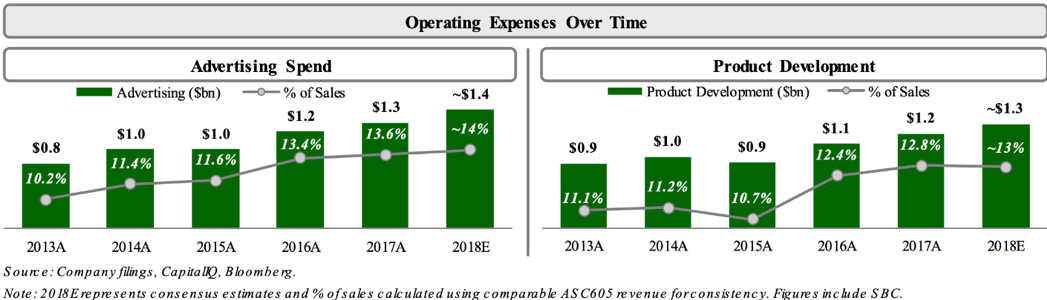

eBay has lifted advertising spend by 70% since 2013 and revved up product development by 45% as well. This has surprisingly led to material margin declines because of the failure of these initiatives to take hold.

One of the missteps resulting in this margin softness is the dysfunctional execution of its online platform infected by technical problems and operational headwinds.

A few notable events were a 2014 broad-based password hack and the botched fix to that problem exacerbated by a muddied communication strategy.

During this time, eBay was outmaneuvered by Google’s (GOOGL) search algorithm resulting in a massive decline in traffic as a result of this painful change.

The next year was similarly awful with a shoddy mobile application that did not resonate with customers and was put out to pasture shortly after rolling it out.

An online marketplace offering a platform for over four million buyers and sellers to carry out business requires high-level functioning. A failure to deliver this experience has caused long-time users to jump ship to other niche vertical platforms.

Innovative endeavors aren’t part of this new strategy to remake the company.

The underlying strategy effectively spells out that eBay needs to become more like Amazon and any sort of moderate success in doing that will positively boost the stock price – let’s call it what it is – an operational overhaul and nothing more than that.

The complaints don’t stop there and last year eBay was inundated with technical issues that included incorrect billing, deleted photos, warped title presentation, and senior management took the blame in a podcast confessing that management needs to pull things together and they “don’t want to repeat (the same mistakes) on a number of levels. And the technology issues that we have had with the platform are on top of the list.”

eBay is not a startup and presides over a profitable business.

Returning capital to shareholders was part of the plan as well.

This entails repurchasing shares of up to $5 billion which was $1 billion more than the original guidance – Elliot Management is an activist investor after all hoping to super-charge shareholder income streams.

Elliot wants to implement a 1.5% dividend yield due to eBay’s high free cash flow model.

After 2020, Elliot wants to allocate 80% of free cash flow for share repurchases and earmark the other 20% for M&A activity.

It is difficult to surmise if this plan will work smoothly or not, but if Elliot can bring in the correct team to execute this plan, I would give them the benefit of the doubt as making this plan into a viable success seems realistic.

But it is yet to be seen how laborious it will be to get the people they want through the door.

eBay is truly a unique asset and the chopped-down nature of its shares would stage a remarkable turnaround if some proven management from Amazon’s executive team could be captured and convinced that eBay is a legitimate option.

Easier said than done, but this is a step in the right direction.

My Luger is firmly in my holster and waiting for some action - if there are any whiffs of a real turnaround then I’ll shoot out some eBay trade alerts.

“Intellectual property has the shelf life of a banana.” – Said Founder of Microsoft Bill Gates

Mad Hedge Technology Letter

January 23, 2019

Fiat Lux

Featured Trade:

(WHY TECH IS FLEEING SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)

When did Marc Benioff become a real estate agent?

That is the main takeaway from the interview he gave to the world from the annual powerful people conference in Davos, Switzerland.

During the interview, he cut straight to the chase and described the cocktail of negative unintended consequences that the tsunami of tech profits has spawned.

His thesis, though not new, parlayed admirably with Bridgewater Associates Founder Ray Dalio interview in chronicling an economic landscape in which geopolitical turmoil finally catches up meaningfully with the movement of tech shares because of the underlying threat to influence concrete economic policy moving forward.

Why is he a real estate seller?

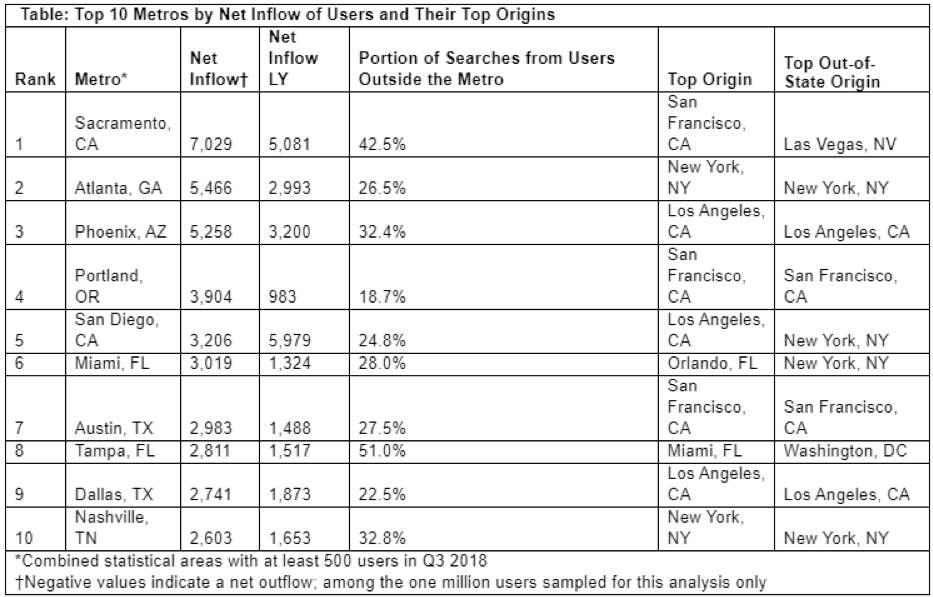

Well, he might as well be one in second-tier cities with copious amounts of tech talent such as Austin, Nashville, Sacramento, Atlanta, and Portland because these metro areas are about to experience a wild ride in the property market rollercoaster.

Benioff just added fuel to this fire.

The robust housing demand, lack of housing supply, mixed with the avalanche of inquisitive tech money will propel these housing markets to new heights and this phenomenon is happening as we speak.

Benioff lamented that San Francisco, where ironically he is from, is a diabolical “train wreck” and urged fellow tech CEOs to “walk down the street” and see it with their own eyes to observe the numerous homeless encampments dotted around the city limits.

The leader of Salesforce doesn’t mince his words when he talks and beelines to the heart of the issues.

After relinquishing some of his CEO duties to newly anointed Co-CEO Keith Block, Benioff will have the operational time and a wealth of resources to get on top of the pulse of not only tech issues but bigger picture stuff and he now has a mouthpiece for it with Time magazine which he and his wife recently bought.

In condemning large swaths of the beneficiaries of the Silicon Valley ethos, he has signaled that it won’t be smooth sailing for the rest of the year in tech wonderland, and he urged companies to transform their business model if they are irresponsible with user data.

The tech lash could get messier this year because companies that go rogue with personal data will face a cringeworthy reckoning as the tech lash fury seeps into government policy and the social stigma worsens.

I have walked around the streets of San Francisco myself. Places around Powell Bart station close to the Tenderloin district are eyesores. South of Market Street isn’t a place I would want to barbecue on a terrace either.

Summing it up, the unlimited tech talent reservoir that Silicon Valley gorged on isn’t flowing anymore because people don’t want to live there now.

This tech talent, equipped with heart-tugging stories from siblings and anecdotes from classmates getting shafted by the San Francisco dream, has recently put the Bay Area in the rear-view mirror for many who would have stayed if it were 20 years ago.

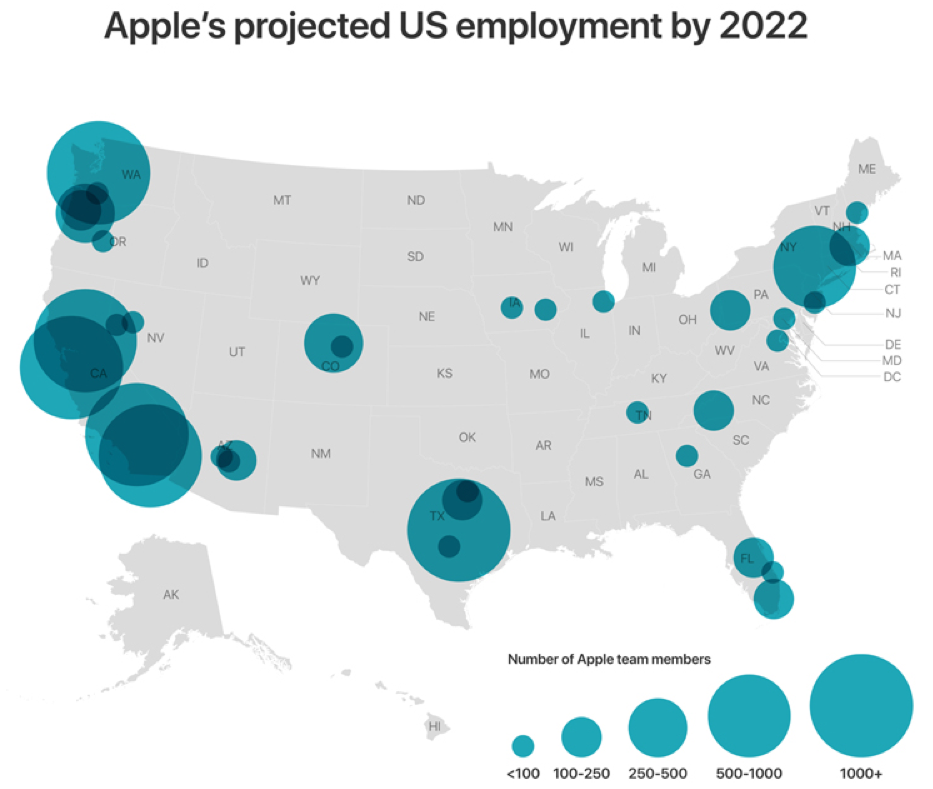

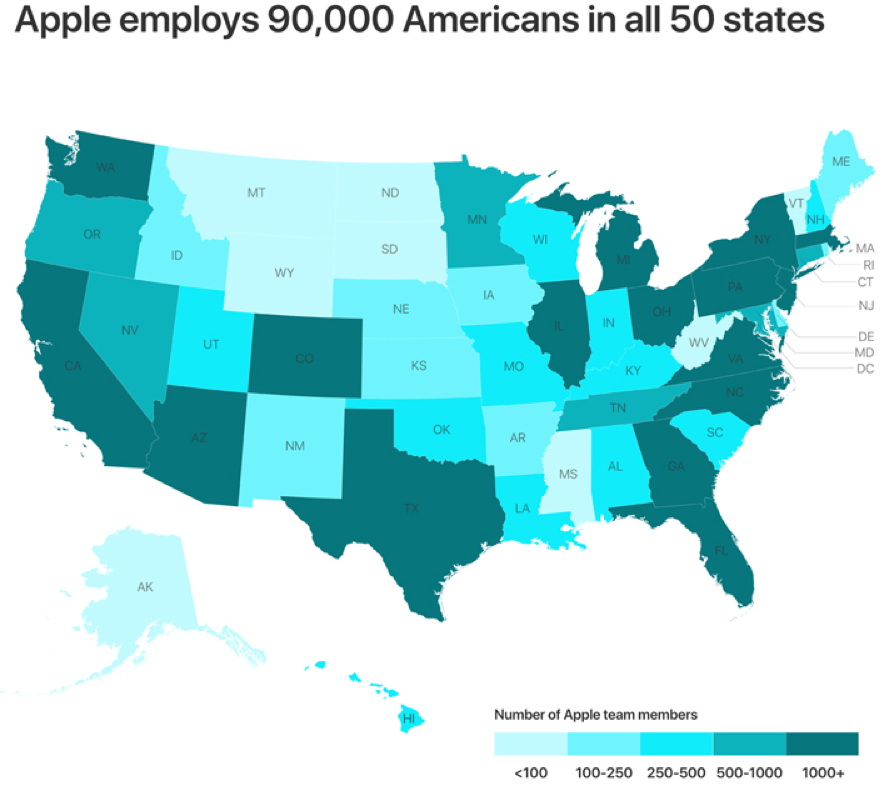

This is exactly what Apple’s $1 billion investment into a new tech campus in Austin, Texas and Amazon adding 500 employees in Nashville, Tennessee are all about. Apple also added numbers in San Diego, Atlanta, Culver City, and Boulder just to name a few.

Apple currently employs 90,000 people in 50 states and is in the works to create 20,000 more jobs in the US by 2023.

Most of these new jobs won’t be in Silicon Valley.

Since the tech talent isn’t giddy-upping into Silicon Valley anymore, tech firms must get off their saddle and go find them.

The tables have turned but that is what happens when the heart of western tech becomes unlivable to the average tech worker earning $150,000 per year.

I also mind you that these external forces have nothing to do with pure technology, pure technology improves with each iteration and gaps up with each revolutionary idea.

That will not change.

Driving out young people who envision a long-term future elsewhere than the San Francisco Bay Area forces Silicon Valley to adapt to the new patterns revealing themselves.

Sacramento has experienced a dizzying rise of newcomers from the Bay Area itself.

Some are even commuting, making that 60-mile jaunt past Davis, but that will give way to entire tech operations moving to the state capitol.

Millennials are reaching that age of family formation and they are fleeing to places that are affordable and possible to become a new home buyer.

These are some of the practical issues that tech has failed to embrace and to maintain the furious pace of growth that investors' capricious expectations harbor.

Silicon Valley will have to become more practical adding a dash of empathy as well instead of just going by the raw and heartless data.

We aren’t robots yet, and much of the world still augurs to emotional decisions and disregards the empirical data.

My favorite tech companies are not only saying the right things but are doing the right things as well.

Microsoft (MSFT) just laid down a marker promising $500 million to build more affordable housing in Seattle.

Sustainability does not only mean building a sustainable business model on the balance sheet, but this definition is growing to be inclusive of upholding the stability and long-term prospects of a local area.

Microsoft has put the trust in its products at the fore of their business model.

Each time CEO of Microsoft Satya Nadella interviews, he preaches about the universal trust that consumers possess in Microsoft.

He is not off on his claims and Microsoft is riding this mantra all the way to the bank while sidestepping regulatory scrutiny.

Nadella is always smartly one step ahead.

All this screams going long Microsoft by buying the dips.

Sell the rallies in the names that have a crisis of trust such as Facebook (FB) and Google (GOOGL).

I was recently gouged $250 on my monthly phone bill by Google because of a technicality from cell phone service Google Fi.

All a specialist said was that according to the data, I should be charged almost as if I should be shamed for even questioning their business model.

Not only that, the best and brightest from Stanford, University of California at Berkeley, and Ivy league schools do not want to work for Facebook and Google anymore.

These brands have been tainted.

The result will be needing to overpay to secure the able forces needed to pursue growth and success.

Not only that, upper management has left in droves “pursuing new opportunities.”

Google is also grappling with an Apple problem - no new innovative products and it’s yet to be seen if Waymo, the autonomous driving business, can be that solid growth driver going forward.

As the economy creeps closer and closer to the end of the cycle, investors won’t be willing to drain money down some loss-making outfit in the name of growth.

Therefore, software companies based on innovation fused with stable profits will be the go-to formula in tech investing in 2019 and Amazon (AMZN), Salesforce (CRM), and Microsoft (MSFT) are ahead of the curve.

Don’t get me wrong - Silicon Valley is still alive and kicking.

But, instead of physical offices being planted in the Bay Area, the tech industry will give way to the “spirit” of Silicon Valley with offices in far-flung places.

And remember that all of these new tech talent strongholds will need housing, and housing that an IT worker making $150,000 per year desires.

“I strongly believe the business of a business is to improve the world.” – Said Founder and Co-CEO of Salesforce Marc Benioff

Mad Hedge Technology Letter

January 22, 2019

Fiat Lux

Featured Trade:

(HOW TO PLAY TECHNOLOGY STOCKS IN 2019),

(NFLX), (AAPL), (TSLA), (STT), (BLK)