“There’ll always be serendipity involved in discovery.” – Said Founder and CEO of Amazon Jeff Bezos

“There’ll always be serendipity involved in discovery.” – Said Founder and CEO of Amazon Jeff Bezos

Mad Hedge Technology Letter

November 29, 2018

Fiat Lux

Featured Trade:

(SALESFORCE KNOCKS IT OUT OF THE PARK)

(CRM), (AAPL), (PYPL), (ADBE), (TWLO), (MSFT), (AMZN)

It’s been a grueling winter for tech stocks and countless number of positive earnings reports have fell on deaf ears.

Will the bloodletting stop?

Not if Salesforce (CRM) has something to say about it!

And if you thought that tech’s secular tailwinds had vanished, this latest earnings report confirmed that software stocks are alive and are as potent as ever.

That is why I have identified software stocks as the best tech play in the current late-stage economic cycle.

At the Mad Hedge Lake Tahoe Conference, I clearly telegraphed that companies do not pour capital into capex for large and risky projects at this late stage, they search for the additional incremental dollar by arming their staff with optimal and efficient software programs to squeeze more juice out of the lemon.

Salesforce is a great example of this.

Moving forward, Salesforce is on the A-team of the software squad, and ideally positioned to harpoon any whales that come near their boat.

Companies are looking to double down on software initiatives at this point which is another reason why annual IT budgets have shot through the roof.

I have met countless CEOs who guide thousands of staff throughout branches around the world and they told me that one of the big in-house additions has been integrating Salesforce as the main customer relationship management system deleting legacy systems of yore that have pooped out.

The switch bears fruits immediately with operations supercharged like a 5-star high school football prospect on his first month of ‘roids.

Simply put, everything just works a lot better with access to this software.

What CEO wouldn’t want that?

Even more salient is that Salesforce has promoted itself as the emblematic tech growth stock promising to smash $16 billion of annual revenue by next year.

I love that Salesforce commits to ambitious sales targets and always delivers the goods.

A talking head on a prominent financial TV show went on record saying that Apple is the key to the tech narrative perpetuating, I would completely disagree with this statement.

Everyone and his mother have absorbed that Apple iPhones sales have plateaued, I am honestly sick of hearing the same story in the news over and over again.

That is why Apple has been trying to morph into a software and service stock. They are doing a great job at it by the way.

The real conclusive acid test to the tech story are these high growth software stocks because they should be the ones outperforming at this stage in the economic cycle.

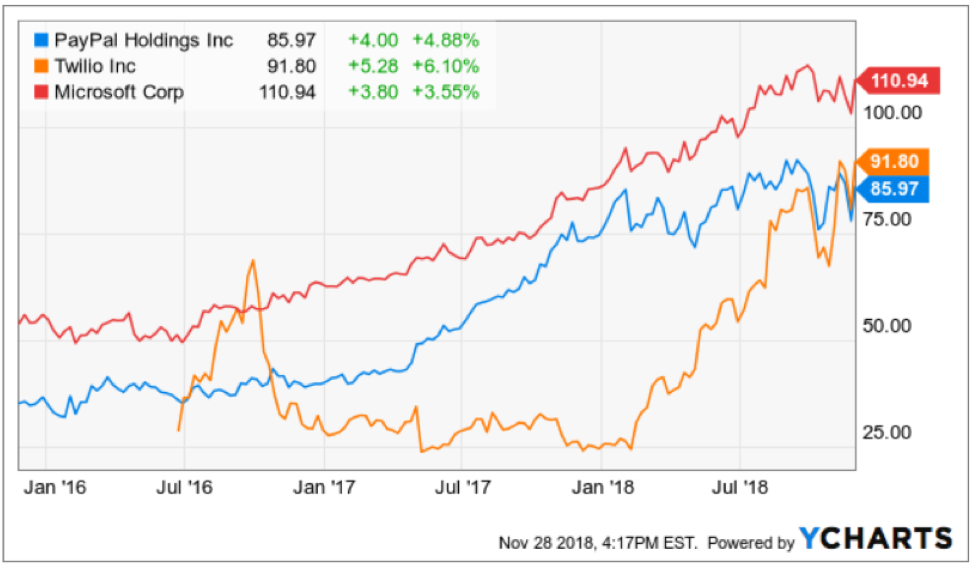

If companies tilted towards software like Salesforce, Twilio (TWLO), PayPal (PYPL), Microsoft (MSFT), and Adobe (ADBE), just to name a few of the crown jewels of software stocks, start laying eggs then I would admit the tech story is dead.

But it’s not.

Salesforce is poised to continue its ascent and that basically means quarterly sales growth in the mid-20s for the foreseeable future.

There is an addressable market of $200 billion and the pipeline is rich as ever could be.

Salesforce has really turned the corner with free cash flow and profitability. It was only a few years ago they were turning in heavy losses, but this new Salesforce will be even more profitable as the network effect makes the sum of the parts and each add-on cloud-based software tool even more valuable.

Companies just love the breadth of functionality that Salesforce offers and their pension for product enhancement is really owed to CEO Marc Benioff who never shies away from calling his peers out and never cuts corners.

In fact, Marc Benioff is one of the good guys in an increasingly rotting Silicon Valley, part of this has to do with him growing up as a local lad in Burlingame, just a stone throw from his newly built palatial Salesforce Tower gracing downtown San Francisco’s picturesque skyline.

Benioff has more skin in the game as a local and publicly supported Proposition C, effectively a bill that would charge a homeless tax on big earning corporations in San Francisco.

Benioff has also promised to fund any subsequent legal attack that attempts to unravel this homeless tax putting his money where his mouth is.

Benioff noted that he has seen no softness in the macro spending environment.

And even with all the crazy headlines spinning around in the media, there has been no material impact from any supposed peak or downshift in the business environment.

Not only is Salesforce dredging up SME deals at a fast rate, they are quickly targeting the big kahunas.

The number of deals generating more than $1 million was up 46% YOY in the third quarter.

The volume of $20 million-plus relationships is also growing significantly.

In the past quarter, Salesforce renewed and expanded a 9-figure relationship with one of the largest banks in the world.

Salesforce is able to upsell their cloud tools to customers and these firms eat up the Einstein built-in functionality that uses artificial intelligence to improve the existing software.

North America comprised 71% of total revenue which is why this software company will reap the rewards for any extension of this economic cycle because they are largely domestic and best in show.

Salesforce beat and raised its outlook calming the frayed nerves of investors looking to dump software stocks.

Just look at the billings growth that was anticipated at 19%, Salesforce smashed it by 8% coming in at 27%.

Not only are they scooping up new customers, but renewals have been just as robust.

The truth is that Salesforce can’t roll out enough cloud-based software products to meet the insatiable demand.

All of this backs up my thesis that software stocks will be the outsized winners of 2019.

The FANGs are not dead, I rather hold an Amazon (AMZN) or Apple (AAPL) long term if I had the choice.

But at this stage, investors should be piling into all the crème de la crème software stocks.

Avoid them at your peril.

“Technology's always taken jobs out of the system, and what you hope is that technology's going to put those jobs back in, too. That's what we call productivity.” – Said CEO of Salesforce Marc Benioff

Mad Hedge Technology Letter

November 28, 2018

Fiat Lux

Featured Trade:

(TRUMP'S TARIFF THREAT FOR APPLE))

(AAPL), (BABA), (EBAY), (WMT), (FB), (MSFT), (AMZN)

The administration’s threat of levying 10% on iPhones is a great sign for the technology sector as a whole.

The short-term media sensationalism has flipped this story the other way around crying about this as if it is a major penalty to Apple (AAPL).

Don’t get me wrong, these potential stiff tariffs have the possibility of triggering a $1 billion loss on Apple’s revenue, but this is all about protecting American technology long term.

This is not like taking a sledgehammer and ruining their business model, and it will not strip away this brilliant wealth creation vehicle.

Apple remains a cheap stock to buy for patient long-term holders and is one of the best run companies in the world with an operating maestro executing the roll-out of premium products named Tim Cook, the CEO of Apple.

The administration might not like some of technology firms’ tactics, but in reality, they are a pivotal reason why the economy has been humming along in the longest bull-market ever.

Effectively, the administration has put Apple and its peers up on a pedestal and is defending them from Chinese competition.

What industry wouldn’t want this?

Most of 2018, the current administration presided over a stock market that was going up in a straight line and the bulk of those gains were harvested by the major tech companies, mainly the FANGs.

The administration was quick to take credit for a strengthening stock market and would like to see rates suppressed to engineer more upside.

The FANGs are going through a reversion to the mean after 100% gains and giving back 20% or 30% of profits offer opportune entry point for long-term investors.

The only FANG that needs a structural change is Facebook (FB) and has the funds to do it. The other three plus Microsoft (MSFT) will lead the tech charge when the short-term weakness subsides.

If you think Chinese consumers would bail on Apple products because of the trade war, then you are wrong.

Apple has been grandfathered into Chinese society and it is one of the few iconic American products that can boast this achievement.

Apple is a luxury brand produced by an epochal superpower.

The presence of Apple products reverberates around China’s economic landscape, and even if Chinese people do not like America, they respect its economic prowess and wish to learn from its capitalistic ways.

This is the main reason they send their kids to American universities.

Historically, China was once entirely dependent on Russia to fill in its economic and social vision with the communist party sending its best and brightest to Moscow to study the Soviet Union’s secret sauce.

If you go to Beijing now, most of the second ring road of flats conspicuously remind me of Khrushchyovkas, the unofficial name of a type of low-cost, concrete-paneled or brick three- to five-storied apartment building which was developed in the Soviet Union during the early 1960s.

During this time, its namesake Nikita Khrushchev directed the Soviet government.

Pre-Deng Xiaoping Soviet influences can still be found everywhere in central Beijing.

Once the Chinese communist government realized that the Soviet model impoverished large swaths of society, they went on the open market to find a more optimal method to run their economy that could take advantage of their monstrous man power.

The model they decided on was a fusion of communism and capitalism, and for 30 years, this system fueled Chinese peasants out of poverty and to the promenades of Saint-Tropez.

Because of Chinese laser-like obsession on social status, material possessions are the most important way for them to differentiate against each other.

For Chinese women, the x-factor is skin tone, but for Chinese men, it is the brand, quality, and volume of possessions.

Even if rich Chinese hate Apple and their iPhones, they are permanently married to this product because owning a Chinese smartphone would be a monumental faux pas on the same level as American First Lady Melania Trump shopping for her new clothes at Walmart (WMT).

This is the same reason why every political who’s who in China drives an Audi A6, and every successful Chinese business executive drives a BMW.

Luxury brands are closely associated to the person’s social status in China and these unwritten rules have even more weight than the official rules in China partly because most Chinese over 40 are uneducated, plus China’s lack of public trust.

Apple’s tentacles reaching deep into Chinese society have in fact led to a situation where Apple-related jobs for Chinese citizens add up to over 5 million jobs which is over double the number of jobs Apple supports in America.

The result of Apple morphing into a pseudo-Chinese company is that pain for Apple means a loss of Chinese jobs on a large scale at a time when the Chinese economy is becoming more precarious by the day.

The Chinese economy is softening under a massive burden of crippling public and private debt that is putting the cap on growth.

As a result of the trade skirmish, China has temporarily halted its deleveraging effort that was intended to remedy the health of the economy and has reverted back to the China of old, low-quality infrastructure projects and heavily polluted coal production.

China’s rapid ascent to prosperity could also mean the Chinese consumer and economy could go through a reversion to the mean scenario with private and public companies loaded to their eyeballs with debt going bust and a looming economic stimulus in the cards if this plays out.

All this means is that Apple is too big to fail in China and CEO of Apple Tim Cook absolutely knows this.

Theoretically, Chinese consumers absolutely have access to local smartphone substitutes for $200 that would do the same job as a $1,000 iPhone.

I have tested out Huawei and Xiaomi premium smartphones costing $400, and they have more than enough firepower to be a reliable everyday smartphone and some.

The fact is that Chinese consumers intentionally choose not to substitute Apple products.

And I would go deeper than that by saying Steve Jobs is revered in China like a demigod and his passing turned him into a sort of tech martyr with a level of status that not even Alibaba (BABA) originator Jack Ma can touch.

Jack Ma performed miracles by copying eBay’s (EBAY) blueprint of e-commerce from a shabby Hangzhou flat ditching his former job as an English teacher then copying Amazon (AMZN) to juice up growth.

But Jack Ma never created the iPhone, iPod, tablet, or Apple app store from thin air. That he never did.

Making matters even more ironic is that most Chinese communist members actually use an Apple iPhone for the same reasons I mentioned earlier.

Not only that, the children of Chinese communist politicians take lavish vacations to Silicon Valley to take selfie’s in front of Apple’s spaceship headquarters in Cupertino and upload them onto social media.

They then proceed to visit the nearest Apple store right next door at the Apple Park visitor center which is essentially an Apple store on steroids to make bulk purchases of Apple tablets, watches, computers, iPhones for their extended circle of friends and distant relatives because they are “cheaper in America than in China” mainly due to the heavy import duties levied on Apple products in China.

As for tech equities, what this does is blunt short-term positive sentiment for tech stocks and particularly chip stocks that I have told readers to stay away from like the plague.

Apple’s supply chain frenemies don’t have the luxury of selling 80 million luxury phones at $1,000 per quarter and are often the recipient of indiscriminate sell-offs shellacking shares.

Even with the overhanging issue of rising tariffs, tech stocks should produce great earnings next year.

Look at Apple and the consensus EPS outlook for next quarter comes in at $4.73 and that is after EPS increasing 41% sequentially from the quarter before.

Apple will soon become a $300 billion of sales per year company with profitability expanding at a rapid clip.

They are a company that prints money then buys back their own stock profusely. Not many companies can do that.

These negative reports that have been coming fast and furious don’t help the momentum, but the share’s weakness solely means that better entry points are available for investors before Apple launches over $200 again.

There is a high chance that the administration is using Apple as a bargaining chip and nothing will come of it.

Think about it, after all this commotion about the trade war with China, revenue was up almost 20% last quarter in greater China, so what gives?

It means that things aren’t as dire as it seems. A lot of hot steam over nothing is a gift to long-term investors, but short-term traders will feel the pain of the temporarily elevated headline risk.

“There is an undeclared Cold War underway now in the IT sector” – Said Former Australian Prime Minister Kevin Rudd

Mad Hedge Technology Letter

November 27, 2018

Fiat Lux

Featured Trade:

(ONLINE COMMERCE IS TAKING OVER THE WORLD)

(AMZN), (ADBE), (WMT), (KSS), (TGT), (LOW), (EA), (ATVI), (TTWO), (ETSY)

At our weekly Monday staff meeting, coworkers were griping and grimacing about their failed internet connections and annoying glitches to their favorite e-commerce sites during the mad rush to find the best deal during Black Friday and Cyber Monday.

Internet traffic was that torrential when sites were driven offline for minutes and some, hours by a bombardment of gleeful shoppers hoping to splash their credit card numbers all over the web on sweet discounts.

The crashing of system servers epitomizes the robust transition to online commerce that has most of us pinned to our devices surfing our go-to platforms all day long.

According to data from Adobe (ADBE) analytics, Black Friday sales jumped 23.6% YOY to $6.22 billion, and it was the first time in history that mobile sales broke the $2 billion threshold.

It is a clear victory for e-commerce and, in particular, mobile shopping that has become more integrated into modern tech DNA.

Mobile sales comprised 33.5% of total sales and were up from 29.1% last year, signaling that more is yet to come from this transcending movement that is shoving everything from content, digital ads, entertainment, banking and pretty much everything you can think of to your handheld smartphone.

CEO of Kohl’s (KSS) Michelle Gass confirmed the e-commerce strength by saying, “80 percent of traffic online came from mobile devices.”

The beauty of this movement is that it’s not an “Amazon (AMZN) takes all” scenario with other players allowed to feast on a growing size of the e-commerce pie.

“Click and collect” has been a strategy that has paid off handsomely with sales up 73% YOY during the shopping holidays.

This all supports my prior claim that e-commerce is one of the most innovative and dynamic parts of technology especially the grocery space, and the buckets full of capital attempting to reconfigure the e-commerce spectrum is creating an enhanced customer experience for the final buyer resulting in better products, superior delivery methods, and cheaper prices.

Some other retailers spicing up their e-commerce strategy are dinosaur big-box retailer’s intent to defend their business from the Amazon death star.

If you can’t innovate in-house, then “borrow” the innovation from somewhere else.

That is exactly what Target (TGT) has chosen to do announcing last week that it would grant free 2-day shipping with no minimum sale threshold.

The tactic is bent on undercutting Walmart (WMT) who currently operate a 2-day free shipping policy with a minimum order of $35.

Most shoppers will buy in bulk easily eclipsing the $35 per order mark minimizing the rot of small orders.

And if they aren’t eclipsing the $35 per order mark, it demonstrates the firm’s offerings lack the diversity and quality to compete with Amazon.

Capturing the incremental sale squarely rests on the e-tailers ability to coax out the buyers’ impulses to move on the can’t-miss items.

The lesser known retailers fail miserably at matching the lineup of products that Amazon can roll out.

The bountiful product selection at Amazon leads customers to pay for 3, 4, 5, 6 or more items on Amazon.com.

That said, I am bullish on Walmart’s e-commerce strategy. The “click and collect” strategy has shown to be an outsized winner increasing industry sales of this type 120% YOY.

Walmart is at the center of this strategy and they are refurbishing their supercenters to accommodate this growth in collecting from the curb.

Effectively, this gives customers the option to skip the queue instead of bracing the hoards and navigating the crowds of shoppers in the supercenter.

Other changes are minor but will help, such as offering online product location maps to customers beforehand and allowing customers to pay for large items like big-screen televisions on the spot.

The biggest windfall is derived from the cataclysmic demise of Toy “R” Us, giving Walmart a new foothold into the toy business.

Walmart is beefing up toy items by 40% in the stores and layering that addition with another 30% increase in their e-commerce division.

Adobe’s upper management recently said in an interview that interactive toys have been a wildly popular theme this year amid a backdrop of the best holiday shopping season ever recorded.

Another attractive gift selling like hotcakes are video games, titles boding well for sales at Activision (ATVI), EA Sport (EA), and Take-Two Interactive (TTWO).

Reliant IT infrastructure will be a key component to executing these holiday sales bonanzas.

Clothing retailer J. Crew and home improvement chain Lowe's (LOW) were grappling with sudden disruptions to their IT systems before they managed to get back online.

More than 75 million shoppers parade the internet to shop during Black Friday and Cyber Monday, and the opportunity cost swallowed to a tech glitch is a CEO’s worst nightmare.

Ultimately, what does this all mean?

Focusing on the positive side of the surging holiday sales is the right thing to do because the avalanche of momentum will have a knock-on effect on the rest of the economy.

Certain companies are positioned to harvest the benefits more than others.

Amazon guided its 4th quarter estimates conservatively and is in-line to beat top and bottom line forecasts.

Other pockets of strength are Walmart’s tech pivot, albeit from a low base. Walmart still has more room to maneuver and they are in the 2nd inning of their tech transformation snatching the low-hanging fruit for now.

Another interesting e-commerce company swinging its elbows around is Etsy (ETSY).

They sell vintage and handmade craft adding the personalized touch that Amazon can’t destroy.

Margins will be higher than the typical low-cost, value e-commerce platform, but scaling this type of business will be more difficult.

Sales grew 41% sequentially and just in time for a winter holiday blowout.

Etsy became profitable in 2017 after three straight loss-making years, and 2018 is poised to become its best year ever.

The profitability bug is hitting Etsy at the perfect time with its EPS growth rate up 36% sequentially.

They report at the end of February and I expect them to smash all estimates.

There are some deep ramifications for the long term of e-commerce that is beginning to suss itself out.

For one, shipping times will continue to be slashed with a machete. If you are enjoying the 2-day free shipping from Amazon and Target now, then wait until 2-day becomes 1-day free shipping.

Then after 1-day free shipping, customers will get 10-hour shipping, and this won’t stop until goods are shipped to the customer’s door in less than 1-hour or less.

This is what the massive $50 billion in logistical investments over the next five years by the likes of Uber and Amazon are telling us.

It will take years for the efficiencies to come to fruition, but it is certainly in the works.

In the next five years, America’s logistics infrastructure will have to accommodate the doubling of e-commerce packages from 2 billion to 4 billion per year.

Another trend is that omnichannel offerings are sticking and won’t go away anytime soon.

It was once premised that online sales would destroy brick and mortar, yet moving forward, a mix of different sales channels will be the most efficient way of moving goods in the future.

Pop-up stores have been an intriguing phenomenon of late, and surprisingly, 60% of consumers still require interaction with the product to be convinced it's worthy of buying.

Certain products such as fashionable dresses and designer shoes must be given a whirl before a decision can be made. This won’t change anytime soon.

The timing of the sales and marketing push has been moved forward as competitors are eager to get a jump on one another.

Management is agnostic to the timing of the sale.

Thus, discounted sales will show up a week before Thanksgiving as pre-Thanksgiving sales in the future elongating the holiday shopping season cycle by starting it early and delaying the finish of it.

Lastly, the record numbers prove that the e-commerce renaissance and the pivot to mobile is not just a flash in the plan.

What does this mean for tech equities?

The temporal tech sell-off of late is largely a result of outside macro forces and is not indicative of the overall health of the tech sector that has experienced record earnings.

If the markets can keep its head above the February lows, it sets up an intriguing December fueled by Americans flashing their digital wallets on online platforms.

“Collectively, dominant online platforms have more power to shape public opinion than newspapers or the television ever had, yet they face very little regulation or liability.” – Said CEO of IBM Ginni Romett