Mad Hedge Technology Letter

November 26, 2018

Fiat Lux

Featured Trade:

(WILL THE FAANGS FINALLY KILL OFF TELEVISION?)

(AMZN), (DIS), (FOX), (ROKU), (FB), (AAPL), (GOOGL)

Mad Hedge Technology Letter

November 26, 2018

Fiat Lux

Featured Trade:

(WILL THE FAANGS FINALLY KILL OFF TELEVISION?)

(AMZN), (DIS), (FOX), (ROKU), (FB), (AAPL), (GOOGL)

If you were waiting for the other shoe to drop, well, it dropped.

That is the takeaway from finding out that Amazon (AMZN) is making a daredevil bid to pry away the last remaining crown jewels from the traditional television dinosaurs.

In the first round of bidding, Amazon has flexed its muscles and is going after live sports content which Disney (DIS) has limited time to sell off.

The package Amazon desires includes 22 regional sports TV networks that Disney must divest after acquiring Twenty-First Century Fox (FOX).

Professional sports leagues usually engage in auction-based models to sell programming rights.

This auction takes place every few years and has largely eluded the big tech firms.

This gives Amazon another chance to permanently crack the live sports market by buying up the sports networks themselves.

Amazon’s sports strategy is a work in progress.

It started when they introduced NFL’s Thursday Night Football to its prime members a few years ago.

Amazon followed that up by successfully bidding on a 20-match package of English Premier League matches in a 3-year deal thought to be around $135 million.

These games are free of charge if you are an Amazon prime member.

The amount was quite large considering Amazon only coughed off $50 million for 10 Thursday night games.

Even more intriguing is the possibility of Amazon’s digital ad business collaborating with the live sports content.

Professional sports would serve as the ideal platform to dish out targeted digital ads to its prime viewership, and nobody has better sets of data to place the right products in front of the right eyeballs than Amazon.

Marketers would pay top dollar for this type of gilt-edged opportunity.

Half of product searches already start on Amazon and the number is rising.

Patiently, Amazon has sat back and bided its time to make a monumental splash for the right type of sports assets.

And that time has now come.

Remember that live sports are one of the last bastions of premium television content for the traditional players.

Professional sports are optimally enjoyed in the moment gripped by emotion, watching on replay doesn’t cut it in a cutthroat on-demand world.

Traditionally, advertisers have blissfully paid top advertising dollar to paint firm’s logos on television sets knowing that a guaranteed set of viewers will tune in.

This has made ESPN the most exorbitant affiliate fee of any cable network and they do not apologize for it.

It is also part of the reason why they are hamstrung by a dwindling viewer base.

ESPN has lost an astounding 11 million subscribers since 2013.

The value of ESPN has been heavily diluted because of professional sports leagues offering proprietary content directly through their own websites in a subscription style format slicing off the value of sports networks like ESPN.

ESPN is no longer the one-stop shop for live sports like it used to be.

In the past year, ESPN, owned by Disney, launched ESPN+ for $4.99 per month that signaled ESPN’s foray into online streaming that CEO of Disney Bob Iger has made the utmost priority.

The sign of intent telegraphs the beginning of traditional network television’s attempts to move into the online streaming tech ecosphere.

Disney’s ESPN+ has been tepid at best as the content is mainly second-string content of American soccer matches and alternative sports leagues.

This appears like a testing phase for Disney as they hope to smoothly roll out their flagship online content platform in 2019.

At worst, if Amazon and the rest of the FANGs pour into the auction bidding process for the sports assets, Fox or other suitors will have to pay through the nose for these regional sports networks.

Facebook (FB) was interested in the Indian Cricket League's broadcasting rights and only offered $600 million.

The winner won with a bid of over $2.5 billion.

Obviously, Facebook underestimated the level of cricket fanaticism in India. These types of assets can’t be bought at a discount.

Facebook’s consolation prize was claiming the rights to broadcast La Liga soccer from Spain in eight South Asian countries including India, Pakistan, and Sri Lanka.

These are the lengths that American tech companies will go to lure in additional users.

In fact, American tech companies do not need to profit from these live sports deals.

They merely view it as a traffic acquisition cost (TAC), in the same vein as Google (GOOGL) paying Apple (AAPL) $8 million in 2017 to plop its search engine on Apple iOS devices.

That number will rise to $12 billion in 2018, and it’s worth every penny for Google.

How can traditional linear television stations compete with tech titans who are content with losing money on live sports?

The answer is they can’t, and they should be frightened to death about these developments.

And I would argue that Facebook would much rather get into the live sports businesses than moderate fractious elections around the world which has been a suicide mission tearing apart the company.

I am completely aware that the NFL has had its issues with the kneeling of the national anthem, but in general, live sports is safer content than politics and should be the clinching reason why every FANG should migrate to live sports.

And that is what will happen.

I bet that the likes of Apple or Facebook will pony up a bid too.

CEO of Apple Tim Cook has been as stern as a prison warden overseeing Apple’s content.

He is cautious about the quality of content delivered to iOS customers and wants to avoid anything controversial.

The NFL might be too risky for Cook, but European soccer seems like it would fit the iOS ecosystem perfectly.

After all, soccer is the number one growing sport in America and is an absolute hit with the younger generation.

The real victor out of all of this is Roku (ROKU).

It could be a real high flyer in 2019 with the pivot to online streaming picking up steam.

First, Disney’s platform is coming online in a few months.

It’s a godsend that big tech is looking to dive into the live sports market for industry-leading OTT TV box company Roku.

Roku doesn’t care which company is producing content as long as it is quality online content, and it is on Roku.

At some point, Roku will be a must-have for sports fans who want to follow their favorite sports teams because the content could be spread out through a plethora of online streamers.

Roku is the best system to select a la carte content, and the dispersion of content across many online channels makes content aggregators a critical need going forward.

Take Amazon, for instance, the bulk of the 20 English Premier League matches will be broadcasted during Boxing Day holiday in England.

This would give the British massive incentive to sign up for Amazon prime for one month during the winter holidays to watch the matches while using Amazon’s free 2-day shipping to buy gifts on Amazon’s e-commerce platform.

Effectively knocking out two birds with one stone.

A substantial percentage of British soccer viewers will presumably retain Amazon Prime the following months as the soccer package concludes ushering in a new wave of prime converts.

Roku makes watching Amazon Prime for just a month less painful because habitual Roku viewers are familiar with the Roku platform and can sign up quickly.

This will be the new way of enticing viewers with luxury on-demand content enabling the cross-selling of other services on offer.

After all, Amazon cares deeply about growing prime members that effectively bring down the cost of executing the free 2-day shipping because of the massive economies of scale.

This all bodes well for Roku to outperform in 2019.

“I’m a big believer in the free market. But we have to admit when the free market is not working. And it hasn’t worked here. I think it’s inevitable that there will be some level of regulation.” – Said CEO of Apple Tim Cook

Mad Hedge Technology Letter

November 21, 2018

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO SELL SHORT ON THE NEXT RALLY)

(WDC), (SNAP), (STX), (APRN), (AMZN), (KR), (WMT), (MSFT), (ATVI), (GME), (TTWO), (EA), (INTC), (AMD), (FB), (BBY), (COST), (MU)

Next year is poised to be a trading year that will bring tech investors an added dimension with the inclusion of Uber and Lyft to the public markets.

It seemed that everything that could have happened in 2018 happened.

Now, it’s time to bring you five companies that I believe could face a weak 2019.

Every rally should be met with a fresh wave of selling and one of these companies even has a good chance of not being around in 2020.

Western Digital (WDC)

I have been bearish on this company from the beginning of the Mad Hedge Technology Letter and this legacy firm is littered with numerous problems.

Western Digital’s structural story is broken at best.

They are in the business of selling hard disk drive products.

These products store data and have been around for a long time. Sure the technology has gotten better, but that does not mean the technology is more useful now.

The underlying issue with their business model is that companies are moving data and operations into cloud-based products like the Microsoft (MSFT) Azure and Amazon Web Services.

Why need a bulky hard drive to store stuff on when a cloud seamlessly connects with all devices and offers access to add-on tools that can boost efficiency and performance?

It’s a no-brainer for most companies and the efficiency effects are ratcheted up for large companies that can cohesively marry up all branches of the company onto one cloud system.

Even worse, (WDC) also manufactures the NAND chips that are placed in the hard drives.

NAND prices have faltered dropping 15% of late. NAND is like the ugly stepsister of DRAM whose large margins and higher demand insulate DRAM players who are dominated by Micron (MU), Samsung, and SK Hynix.

EPS is decelerating at a faster speed and quarterly sales revenue has plateaued.

Add this all up and you can understand why shares have halved this year and this was mainly a positive year for tech shares.

If there is a downtown next year in the broader market, watch out below as this company is first on the chopping block as well as its competitor Seagate Technology (STX).

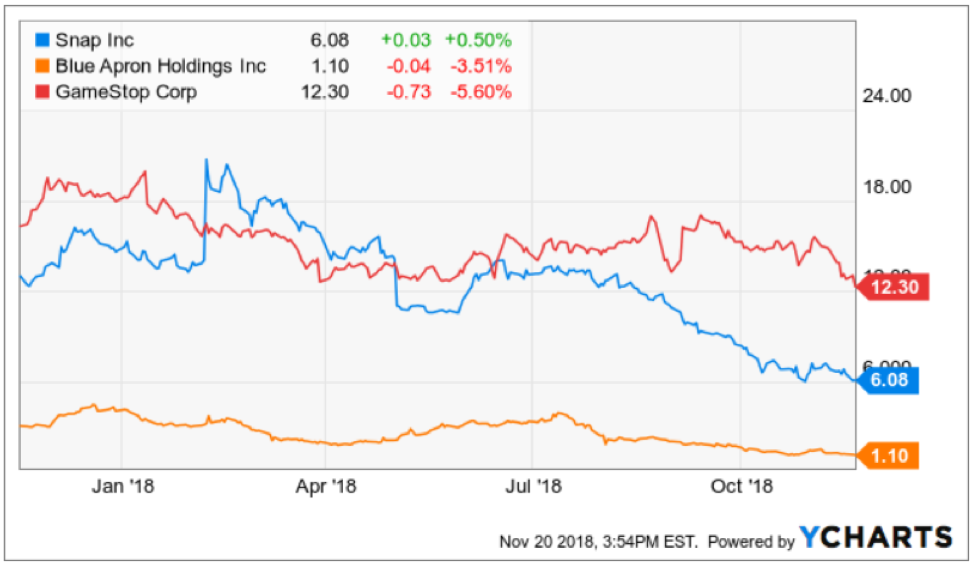

Snapchat (SNAP)

This company must be the tech king of terrible business models out there.

Snapchat is part of an industry the whole western world is attempting to burn down.

Social media has gone for cute and lovable to destroy at all cost. The murky data-collecting antics social media companies deploy have regulators eyeing these companies daily.

More successful and profitable firm Facebook (FB) completely misunderstood the seriousness of regulation by pigeonholing it as a public relation slip-up instead of a full-blown crisis threatening American democracy.

Snapchat is presiding over falling daily active user growth at such an early stage that usership doesn’t even pass 100 million DAUs.

Management also alienated the core user base of adolescent-aged users by botching the redesign that resulted in users bailing out of Snapchat.

Snapchat has been losing high-level executives in spades and fired a good chunk of their software development team tagging them as the scapegoat that messed up the redesign.

Even more imminent, Snapchat is burning cash and could face a cash crunch in the middle of next year.

They just announced a new spectacle product placing two frontal cameras on the glass frame. Smells like desperation and that is because this company needs a miracle to turn things around.

If they hit the lottery, Snap could have an uptick in its prospects.

GameStop (GME)

This part of technology is hot, benefiting from a generational shift to playing video games.

Video games are now seen as a full-blown cash cow industry attracting gaming leagues where professional players taking in annual salaries of over $1 million.

Gaming is not going away but the method of which gaming is consumed is changing.

Gamers no longer venture out to the typical suburban mall to visit the local video games store.

The mushrooming of broad-band accessibility has migrated all games to direct downloads from the game manufacturers or gaming consoles’ official site.

The middleman has effectively been cut out.

That middleman is GameStop who will need to reinvent itself from a video game broker to something that can accrue real value in the video game world.

The long-term story is still intact for gaming manufactures of Activision (ATVI), EA Sports (EA), and Take-Two Interactive (TTWO).

The trio produces the highest quality American video games and has a broad portfolio of games that your kids know about.

GameStop’s annual revenue has been stagnant for the past four years.

It seems GameStop can’t find a way to boost its $9 billion of annual revenue and have been stuck on this number since 2015.

If you do wish to compare GameStop to a competitor, then they are up against Best Buy (BBY) which is a better and more efficiently run company.

Then if you have a yearning to buy video games from Best Buy, then you should ask yourself, why not just buy it from Amazon with 2-day free shipping as a prime member.

The silver lining of this business is that they have a nice niche collectibles division that hopes to deliver over $1 billion in annual sales next year growing at a 25% YOY clip.

But investors need to remember that this is mainly a trade-in used video game company.

Ultimately, the future looks bleak for GameStop in an era where the middleman has a direct path to the graveyard, and they have failed to digitize in an industry where digitization is at the forefront.

Blue Apron

This might be the company that is in most trouble on the list.

Active customers have fallen off a cliff declining by 25% so far in 2018.

Its third quarter earnings were nothing short of dreadful with revenue cratering 28% YOY to $150.6 million, missing estimates by $7 million.

The core business is disappearing like a Houdini act.

Revenue has been decelerating and the shrinking customer base is making the scope of the problem worse for management.

At first, Blue Apron basked in the glory of a first mover advantage and business was operating briskly.

But the lack of barriers to entry really hit the company between the eyes when Amazon (AMZN), Walmart (WMT), and Kroger (KR) rolled out their own version of the innovative meal kit.

Blue Apron recently announced it would lay off 4% of its workforce and its collaboration with big-box retailer Costco (COST) has been shelved indefinitely before the holiday season.

CFO of Blue Apron Tim Bensley forecasts that customers will continue to drop like flies in 2019.

The company has chosen to focus on higher-spending customers, meaning their total addressable market has been slashed and 2019 is shaping up to be a huge loss-making year for the company.

The change, in fact, has flustered investors and is a great explanation of why this stock is trading at $1.

The silver lining is that this stock can hardly trade any lower, but they have a mountain to climb along with strategic imperatives that must be immediately addressed as they descend into an existential crisis.

Intel (INTC)

This company is the best of the five so I am saving it for last.

Intel has fallen behind unable to keep up with upstart Advanced Micro Devices (AMD) led by stellar CEO Dr. Lisa Su.

Advanced Micro Devices is planning to launch a 7-nanometer CPU in the summer while Intel plans to roll out its next-generation 10-nanometer CPUs in early 2020.

The gulf is widening between the two with Advanced Micro Devices with the better technology.

As the new year inches closer, Intel will have a tough time beating last year's comps, and investors will need to reset expectations.

This year has really been a story of missteps for the chip titan.

Intel dealt with the specter security vulnerability that gave hackers access to private data but later fixed it.

Executive management problems haven’t helped at all.

Former CEO of Intel Brian Krzanich was fired soon after having an inappropriate relationship with an employee.

The company has been mired in R&D delays and engineering problems.

Dragging its feet could cause nightmares for its chip development for the long haul as they have lost significant market share to Advanced Micro Devices.

Then there is the general overhang of the trade war and Intel is one of the biggest earners on mainland China.

The tariff risk could hit the stock hard if the two sides get nasty with each other.

Then consider the chip sector is headed for a cyclical downturn which could dent the demand for Intel chip products.

The risks to this stock are endless and even though Intel registered a good earnings report last out, 2019 is set up with landmines galore.

If this stock treads water in 2019, I would call that a victory.

“If you can’t tolerate critics, don’t do anything new or interesting.” – Said Founder and CEO of Amazon Jeff Bezos

Mad Hedge Technology Letter

November 20, 2018

Fiat Lux

Featured Trade:

(A LESSON IN BLITZSCALING)

(UBER), (LYFT), (GRUB), (DPZ), (AMZN), (BABA), (SQ), (PYPL), (NFLX)

One of the fastest parts of technology growing at a rapid clip is fintech.

Fintech has taken the world by storm threatening the traditional banks.

Companies such as Square (SQ) and PayPal (PYPL) are great bets to outlast these dinosaurs who have a laser-like focus on technology to move the digital dollars in an efficient and low-cost way.

Another section of the technology movement that has caught my eye morphing by the day is the online food delivery segment that has soaring operating margins aiding Uber on their quest to go public next year.

There have been whispers that Uber could garner a $120 billion valuation dwarfing Chinese tech giant Alibaba’s (BABA) IPO which was the biggest IPO to date at $25 billion.

Uber is following in Amazon’s footsteps executing the “blitzscaling” method to suppress competition.

This strategy involves scaling up as quick as possible and seizing market share before anyone can figure out what happened.

The growth explodes at such speed that investors pile in droves throwing inefficient capital at the business leading the company to make bold bets even though profit is nowhere to be seen.

Blitzscaling has fueled American and Chinese tech to the top of the global tech charts and the trade war is mainly about these two titans jousting for first and second place in a real-time blitzscale battle of epic proportion.

The audacious stabs at new businesses usually end up fizzling out, but the ones that do have the potential to blaze a trail to profitability.

One business that has Uber giving hope of one day returning capital to shareholders is Uber Eats – the online food delivery service.

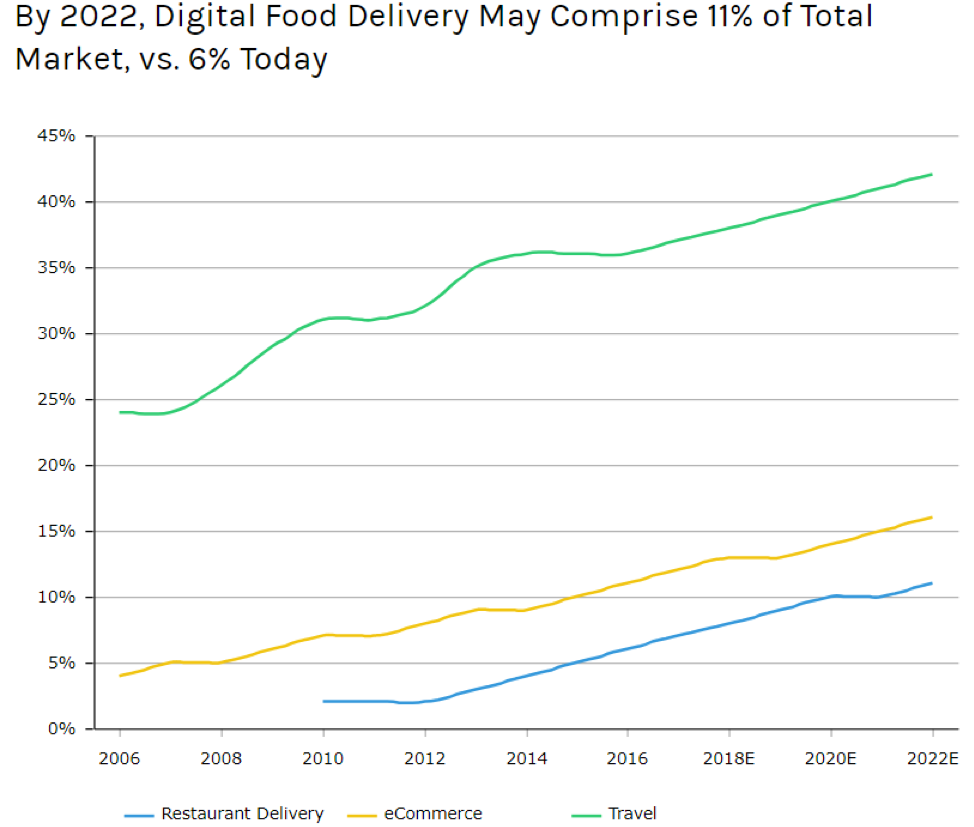

Total sales of restaurant deliveries will hit 11% of revenue if the current trend continues in 2022 marking a giant shift in consumer attitudes.

No longer are people eating out at restaurants, according to data, younger generations view ordering from an online food delivery platform as a direct substitute.

This mindset is eerily similar to Millennials attitude towards entertainment.

For many, Netflix (NFLX) is considered a better option than attending a movie theatre, and all forms of outdoor entertainment are under direct attack from these online substitutes.

One firm on the forefront of this movement has been Domino’s Pizza (DPZ).

You’d be surprised to find out that over half of the Domino’s Pizza staff are software developers.

They have focused on the customer experience doubling down on their online platform to offer the easiest way to order a pizza.

In 2012, the company was frightened to death that it still took a 25-step process to order a pizza.

By 2016, Domino’s rolled out “zero-click ordering” offering 15 different ways to order their product across many major platforms including Amazon’s Alexa.

This has all led to 60% of sales coming from online and rising.

The consistency, efficiency, and seamless online payment process has all helped Dominoes stock rise over 800% since May 2012 and that is even with this recent brutal sell-off.

Uber is perfectly positioned to take advantage of this new generation of dining in.

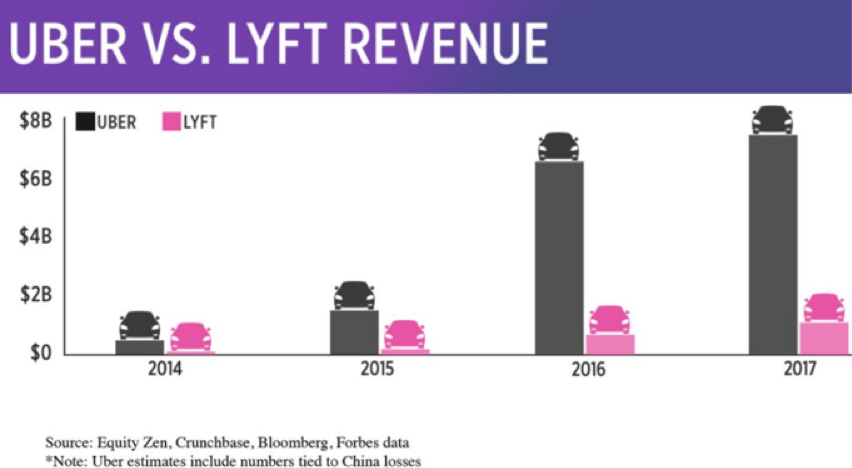

In the third quarter, Uber booked $2.1 billion of gross booking volume in their powerful online food delivery service.

The 150% YOY rise makes Uber Eats a force to be reckoned with.

Uber’s investment into e-scooters and bike transportation stems from the potential synergies of online food delivery efficiency.

It’s cheaper to deliver pizzas on a bicycle or anything without an internal combustion engine.

If you ever go to China, the electric powered three-wheel modified tuk-tuk with a storage compartment in the back instead of passenger seating is pervasive.

Often navigating around narrow alleyways is inefficient for a four-wheel automobile, and as Uber sets its sights on being the go-to last mile deliverer of food and whatnot, building out this vibrant transport network is vital to its long-term vision.

In fact, Uber is not an online ride-sharing platform, it will be something grander and its Uber elevate division could showcase Uber’s adaptability by making air transport cheap for the masses.

As soon as the robo-taxi industry gathers steam, Uber will ditch human drivers for self-driving technology saving billions in labor costs.

As it stands, Uber keeps cutting the incentive to drive for them with rates falling to as low as an average of $10 per hour now.

The golden age of being an Uber driver is long gone.

Uber is merely gathering enough data to prepare for the mass roll-out of automated cars that will shuttle passengers from point A to B.

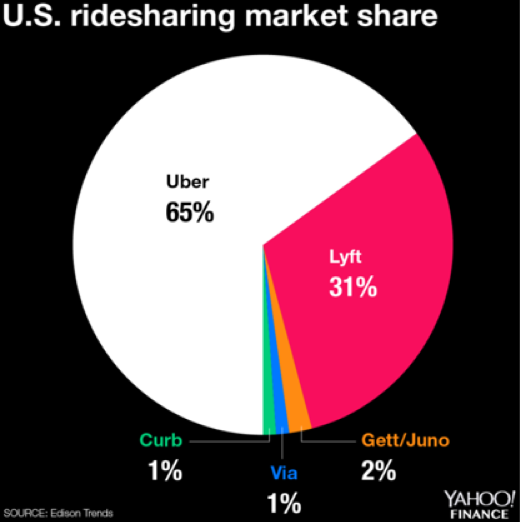

It doesn’t matter that Lyft has gained market share from Uber. Lyft’s market share was in the teens a few years ago and has rocketed to 31% taking advantage of management problems over at Uber to wriggle its way to relevancy.

It does not reveal how poor of a company Uber is, but it demonstrates that Uber’s network is spread over different industries and the sum of the parts is a lot greater than Lyft can fathom.

Lyft is a pure ride-share company and brings in annual revenue that is 4 times less than Uber.

Naturally, Uber loses a lot more money than Lyft because they have so many irons in the fire.

But even a single iron could be a unicorn in its own right.

CEO Dara Khosrowshahi recently talked about its Uber Eats division in glowing terms and emphasized that over 70% of the American population will have access to Uber Eats by the end of next year.

Uber’s position in the American economy as a pure next-generation tech business reverberates with its investors causing Khosrowshahi to brazenly admit that Uber “suffers from having too much opportunity as a company.”

Ultimately, the amped-up growth of the food delivery unit feeds back into its ride-sharing division. These types of synergies from Uber’s massive network effect is what management desires and dovetails nicely together.

In 2018 alone, 40% of Uber Eat’s customers were first-time samplers.

A good portion of these customers have never tried Uber’s ride-sharing service and when they travel for business or leisure, they later adopt the ride-sharing platform leading to more Uber converts.

Uber Freight has enabled truckers to push a button and book a load at an upfront price revolutionizing the process.

The online food delivery service is the place to be right now and it would be worth your while to look at GrubHub (GRUB).

Quarterly sales are growing over 50% and quarterly EPS growth was 61% sequentially for this industry leader.

Profit Margins are in the mid-20% convincingly proving that the food delivery industry will not be relying on razor-thin margins.

Charging diners $5 for delivery and taking a cut from the restaurateurs have been a winning strategy that will resonate further as more diners choose to munch in the cozy confines of their house.

Blitzscaling has led Uber to the online food delivery business and they are pouring resources into it to juice up profits before they go public next year.

The ride-sharing business is a loss-making enterprise as of now, and Uber will need to exhibit additional ingenuity to leverage the existing network to find strong pockets of revenue.

I believe they have the talent on their books to achieve finding these strong pockets making this company an intriguing stock to buy in 2019.

“The first rule of any technology used in a business is that automation applied to an efficient operation will magnify the efficiency. The second is that automation applied to an inefficient operation will magnify the inefficiency.” – Said Co-Founder of Microsoft Bill Gates

Mad Hedge Technology Letter

November 19, 2018

Fiat Lux

Featured Trade:

(ROKU’S UNASSAILABLE LEAD)

(TIVO), (ROKU), (NFLX), (AMZN), (CHTR), (DISH), (FB), (AAPL), (GOOGL)