Shake off the rust.

That is exactly what management of a fast-growing tech company doesn’t want to hear.

Losing money isn’t fun. And investors only put up with it because of the juicy growth trajectories management promises.

Without the expectations of hard-charging growth, there is no attractive story in a world where investors need stories to rally behind.

Setting the bar astronomically high in the approach to management’s execution and product development will always be, the single most important element in a tech company.

This is the secret recipe for thwarting entropy and rising above the rest.

You might be shocked to find out that most tech firms die a harrowing death, the average Joe wouldn’t know that, with constant headlines glorifying our tech dignitaries.

Just look at the pageantry on display that was Amazon’s (AMZN) quest to find a second headquarter.

According to Apex Marketing, the hoopla that coalesced around Amazon’s year-long search netted Amazon $42 million in free advertising by tracking the absorbed inventory of exposure from print, TV, and online.

Social media traffic by itself rung up $8.6 million of freebies.

These days, tech really does sell itself, and I didn’t even mention the billions in tax breaks Amazon will harvest from their Willy Wonka and the Chocolate Factory style headquarter search.

The only thing I would have changed would have been extending the contest into the second year.

Amazon’s brand is probably the most powerful in the world, and that is not because they are in the business of only selling chocolate bars.

One company that might as well sell chocolate bars and has been stymied by the throes of entropy is TiVo (TIVO).

TiVo was once the darling of the technology world.

It was way back in 1999 when TiVo premiered the digital video recorder (DVR).

It modernized how television was consumed in a blink of an eye.

Broad-based adoption and outstanding product feedback were the beginning of a long love affair with diehard users wooed by the superior functionality of TiVo that allowed customers to record full seasons of television shows, and, the cherry on top, fast-forward briskly through annoying commercials.

The technology was certainly ahead of its time and TiVo had its cake and ate it for years.

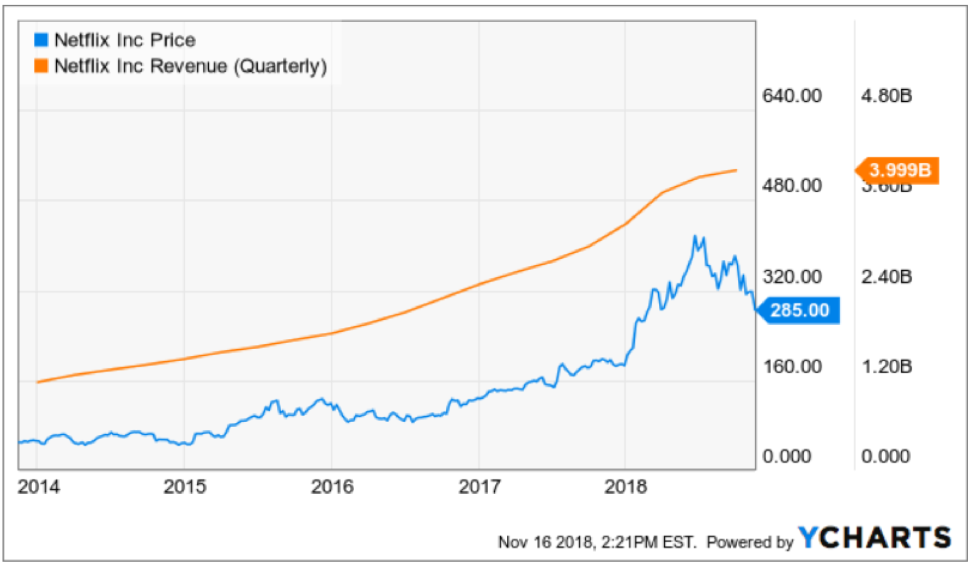

The stock price, in turn, responded kindly and TiVo was trading at over $106 in August of 2000 before the dot com crash.

That was the high-water mark and the stock has never performed the same after that.

TiVo’s cataclysmic decline can be traced back to the roots of the late 90’s when a small up and coming tech company called Netflix (NFLX) quickly pivoted from mailing DVD’s to producing proprietary online streaming content.

Arrogant and set in their old ways, TiVo failed to capture the tectonic shift from analog television viewers cutting the cord and migrating towards online streaming services.

Consumer’s viewing habits modernized, and TiVo never developed another game-changing product to counteract the death of a thousand cuts to traditional television and its TiVo box that is still ongoing as I write this.

Like a sitting duck, Charter Communications (CHTR) and Dish Network (DISH) devoured TiVo’s market share in the traditional television segment constructing DVR’s for their own cable service.

And instead of licensing their technology before their enemies could build an in-house substitute, TiVo chose to sue them after the fact, resulting in a one-time payment, but still meant that TiVo was bleeding to death.

Enter Project Griffin.

Netflix (NFLX) spent years developing Project Griffin, an over-the-top (OTT) TV box that would host its future entertainment content and poured a bucket full of capital into the software and hardware of this revolutionary product.

Making the leap of faith from the traditional DVD-by-mail distribution model that would soon be swept into the dustbin of history was an audacious bet that looks even better with each passing year.

This Netflix branded OTT box was specifically manufactured for Netflix’s Watch Instantly video service.

In 2007, Netflix was just week’s away from rolling out the hardware from Project Griffin when CEO of Netflix Reed Hastings decided to trash the project.

His reason was that a branded Netflix box would hinder the software streaming content confining their growth trajectory to only their stand-alone platform.

This would prevent their streaming service to populate on other networks.

To avoid discriminating against certain networks was a genius move allowing Netflix to license digital content to anyone with a broadband connection, and giving them chance to make deals with other companies who had their own box.

It was the defining moment of Netflix that nobody knows about.

Netflix became ubiquitous in many Millennial households and Roku (ROKU) was spun-out literally bestowing new CEO of Roku Anthony Woods with a de-facto company-in-a-box to build on thanks to old boss Reed Hastings.

Woods cut his teeth borrowing TiVo’s technology and developed the digital video recorder (DVR) as the founder of ReplayTV before he joined Netflix and was the team leader of Project Griffin.

Now, he had a golden opportunity dropped into his lap and Woods ran with it.

Woods quickly became aware that hardware wasn’t the future of technology and switched to a digital ad-based platform model allowing any and all streaming services to launch from the Roku box.

No doubt Woods understood the benefits of being an open platform and not playing favorites to certain networks in a landscape where Apple (AAPL), Google (GOOGL), Facebook (FB), and Amazon have made “walled gardens” an important part of their DNA.

Democratizing its platform was in effect what the internet and technology were supposed to be from the onset and Roku has excavated value from this premise by playing nice with everyone.

This also meant scooping up all the ad dollars from everyone too.

At the same time, Wood’s mentor Hastings has rewritten the rules of the media industry parting the sea for Roku to mop up and dominate the OTT box industry with Amazon and Apple trailing behind.

Roku was perfectly positioned with a superior finished product, but also took note of the future and zigged and zagged when they needed to which is why ad sales have surpassed their hardware sales.

By 2021, over 50 million Americans will say adios to cable and satellite TV.

The addressable digital ad market is a growing $80 billion per year market and Roku will have a more than fair shot to secure larger market share.

The rock-solid foundations and handsome growth story are why the Mad Hedge Technology Letter is resolutely bullish on Roku and Netflix.

Roku and Netflix have continued to evolve with the times and TiVo is now desperately attempting to sell the remains of itself before the vultures feast on their corpse.

What is left is a portfolio of IP assets that brought in $826 million in 2017, and they have exited the hardware business entirely halting production of the iconic TiVo box.

Digesting 100% parabolic moves up in the share price is a great problem to have for Roku and Netflix.

These two are set to lead the online streaming universe and stoked by robust momentum to go with it.

The Mad Hedge Technology Letter currently holds a Roku December 2018 $30-$35 in-the-money vertical bull call spread bought at $4.35, and it is just the first of many tech trade alerts that will be connected to the rapidly advancing online streaming industry.