“The path to the CEO's office should not be through the CFO's office, and it should not be through the marketing department. It needs to be through engineering and design.” – Said Co-Founder and CEO of Tesla Elon Musk

“The path to the CEO's office should not be through the CFO's office, and it should not be through the marketing department. It needs to be through engineering and design.” – Said Co-Founder and CEO of Tesla Elon Musk

Mad Hedge Technology Letter

November 12, 2018

Fiat Lux

Featured Trade:

(THE NEXT OVERHYPED TECH PRODUCT TO BOMB)

(SSNGY), (AAPL), (GOOGL)

I’m unimpressed.

The Samsung (SSNGY) Galaxy F foldable smartphone will be a complete failure just like the Google Glass.

Heralding this product as the new disruptor ready to displace the Apple (AAPL) iPhone is a bunch of garbage.

Yes, Korean stalwart Samsung did achieve success with their flagship smartphone device the Samsung Galaxy which took 6 years to produce. But don’t expect anything similar in terms of sales and scale of adoption.

This will be a dud.

I will outline some of the problems creating a foldable smartphone for mass use.

In fact, why not call a laptop a “foldable smartphone”? I routinely wield my Google (GOOGL) Voice and Skype to call my Rolodex of phone numbers around the world from my computer and my laptop definitely folds!

This smells like desperation from Samsung who has grossly miscalculated gimmicky innovation coining it as a true gamechanger.

Illogically, the act of folding creates a second layer that will result in a bulky product. Logically, it makes sense to have one layer and one layer only.

The sleek smartphones of today are trending towards becoming A2 paper thin and lugging around a brick is not what contemporary-minded netizens had in mind.

Naturally, each future iteration will gradually solve this problem just like Moore’s law observes that the number of transistors in a dense integrated circuit doubles about every two years, meaning you can pack more components into a product over time.

But will there be a second version of this foldable phone?

And then manufacturers must keep in mind which addressable market could this foldable device disrupt. Will it replace the smartphone or the tablet?

Smartphone screens have become bigger with each generation eroding the share and application of the tablet once the smartphone eclipsed the 6-inch screen size.

The tablet industry has suffered since with smartphone enhancements only adding to the misery. This is all evident in this year’s tablet sales down 5.4% YOY through September.

If this foldable phone is pigeonholed as a replaceable tablet product, then sales would address a niche market product at best and have a higher chance of being an outsized flop.

No matter how you cut it up, iPhone users won’t gravitate towards this gimmicky device and chuck their iPhones in the bin.

Cost is also a big factor in this type of product because of the capital thrown at it by Samsung.

They no doubt hope to recoup some of the exorbitant R&D that went into building a brand-new product from scratch.

Rumors floating around the Samsung developer conference pin this foldable phone at a retail price of around $2000.

With this high of price point, I would expect the phone to fly out of my pocket by itself and fold out without me physically doing anything or something similarly impressive.

I highly doubt that Samsung can pull off something that innovative.

The nature of Apple producing brilliant smartphones is that to topple the iPhone, something special is needed to clearly surpass the predecessor along with a must have “it” factor.

That is what you got with the hoards of customers camping overnight in a tent outside of Apple stores dotted around the world waiting to be the first to buy the next version of the iPhone.

That type of pandemonium and hoopla surrounding a consumer product hasn’t been replicated since the days of Steve Jobs.

In general, customers want convenience and the arduous nature of folding out a phone will become tedious in actual reality because most phone users have the propensity to check their phone 15 times per hour.

That also means folding out a phone 15 times per hour and that doesn’t dovetail well with most phone users who, as of now, just slip their phone in and out of a coat or trouser pocket ready in half a second to navigate the e-world.

In short, this device isn’t practical and the targeted market who has the cash to pay for this will dislike the inconvenience of the application.

The user experience is demonstrably inferior to the Apple iPhone.

On the surface, the Galaxy F phone looks innovative and the adaptable nature of the foldable screen is a novelty, but Samsung will have to go back to the drawing board on this one.

I incessantly drum up the issue of the lack of visionaries at the helm of tech companies. The number can be counted on one hand, maybe two.

The type of class where you find the Jack Dorsey and Elon Musk level of visionaries is not a dime a dozen.

When you have a lack of vision, consumers get foldable phones.

Forcibly wedging in hyper-charged display technology into a smartphone is a recipe for disaster.

Maybe someday this technology can be more relevantly applied to a consumer product, but this Frankenstein type product is a mix of two sets of technologies not meant to marry each other.

The act of intent is of equal importance.

The bigger takeaway from this fanciful experiment is that the next wave of innovation to replace the smartphone is in full swing and happening as we speak.

Even though Samsung’s Hail Mary pass looking for that elusive last-second touchdown on the last heave of the game will be a bust. It is only a matter of time before another Steve Job’s lookalike hits the jackpot with the perfect consumer device wooing the billions starting another cult-like phenomenon.

In the next 10 years, display technology will be completely revolutionized adorning our megacities and billboards in ways we never imagined.

This is all just the beginning and filtering out the right formula is what we see taking place from all these tech companies determined to become the king of the jungle.

All of this foldable display technology reverts back to one constant desire – the demand for larger screens.

The 6-inch smartphone was the first baby step to something brilliant.

But ultimately, producing a digital device that can easily fit into our pocket, instantaneously ready for action, possessing beautiful optics with the largest screen possible is the eventual chosen one who will win this sweepstake.

And the first company that can figure out how to get the phone out of our pockets, in front of our eyes without the need for human fingers will have the inside track to revolutionize the world.

We are not there yet, but we are inching closer every day because of the hyper-accelerating rate of technology.

Waiting in the queue are Samsung’s biggest rivals looking to enter the foldable phone market such as Huawei, LG, Lenovo, and many other Chinese Android manufacturers.

There have been whispers that Apple has had some patents filed for foldable technology. And with Sir Jonathan Paul Ive, the Chief Design Officer of Apple, a remarkably special talent designing Apple’s revolutionary products, he certainly has something special to offer hidden up his sleeves.

He always does.

“My style is to have a big vision, a big commitment.” – Said CEO of Softbank Masayoshi Son

If you thought software week at the Mad Hedge Technology Letter was over, you were absolutely wrong.

I have done my best to offer a barrage of cloud-based software stocks with monstrous upside potential that would put any other industry companies six feet under.

Silicon Valley software companies have access to quinine in a mosquito-infested market – digitally savvy talent.

This talent is the best and brightest the world has to offer, and they want to work for a dominant company that gets it.

Much of this involves companies with bright futures, career opportunities galore, solving deep-rooted problems, all applying a treasure trove of data and a mountain of capital your rich uncle would giggle at.

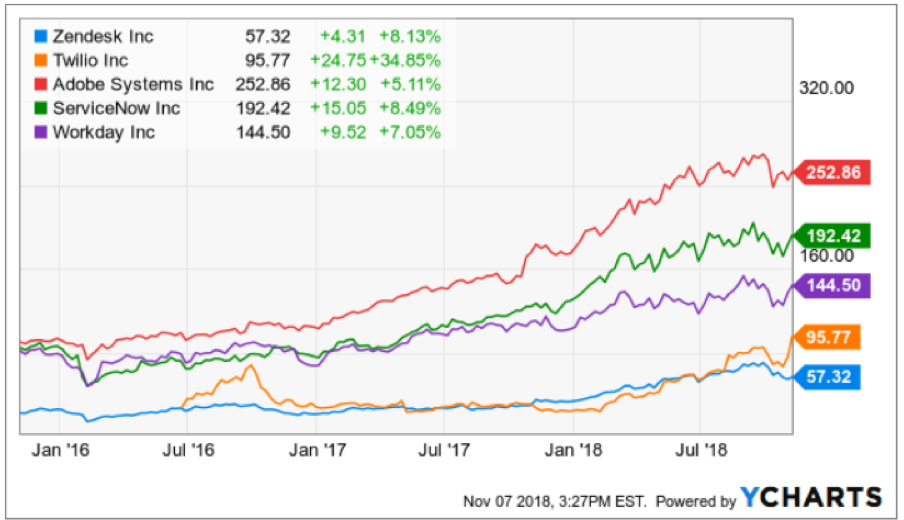

In the short term, I have been succinctly rewarded by my software picks with communication software Twilio (TWLO) rocketing upward 35% intraday at the time of this writing from when I recommended it just a few days ago.

Another Mad Hedge Technology Letter recommendation Zendesk (ZEN), a software company solving customer support tickets across various channels, is up a tame 10% after the election.

All in all, I would desire readers to access due caution as the volatility can bite you badly with crappy entry points, but the upside cannot be denied.

The turbocharged price action means the pivot to software with its new best friend, the software as a service (SaaS) pricing model, encapsulates the outsized profits this industry will rake in going forward.

Without further ado, I’d like to slip in two more companies rounding out a robust quintet of software companies – I bring to you Workday (WDAY) and Service Now (NOW).

Workday is a software company based on a critical component of every successful company – human resources.

Unsurprisingly, human resources are tardy to this wave of software modernization.

Sensibly, companies have chosen short-term software fixes that drive profits with instant success rather than to update its human resource department’s processes.

Big mistake.

I would argue that getting the right people in the doors is paramount and can save substantial time because of the wasted time rooting out toxic employees who weren’t suitable fits.

Ultimately, I have concluded the worst-case scenario entails the enterprise resource planning market stagnating driving minimal growth to the cloud, however, this minimal growth would be substantial enough for Workday to outperform.

The landscape as of now only involves several vendors with a competitive (SaaS) solution auguring well for Workday allowing them to capture a further chunk of market share.

Workday’s growth metrics back up my thesis with its businesses posting a 3-year EPS growth rate of 291% and a 3-year sales growth rate of 36%, painting a picture of a company that will turn profitable in the next few years.

They can even showboat their glittering array of heavy-hitting customers who purchase their software that include Walmart (WMT), Target (TGT), and Bank of America (BAC).

The one headwind tarnishing these types of software companies is the stock-based compensation awarded to employees.

SBC rose 21% YOY and is slightly worrying in an otherwise stellar company. This method of compensation only works when the stock is rising and is a major issue for new Facebook (FB) hires who will prefer cash over its burnt-out share price.

If Workday doesn’t whet your appetite, then how about sampling a main dish of ServiceNow.

This company completes technology service management tasks offering a centralized service catalog for workers to request technology services or information about applications and processes that are being used in the system.

Admirably, this software helps IT workers fix IT system problems which in this day and age is useful considering the bottleneck of chaos many tech and non-tech companies face.

And more often than not, the chaos inundates the in-house IT departments causing the whole business to go offline.

Putting out digital fires is a perpetual business that will never flame out.

As websites and enterprise systems become more complicated, a bombardment of errors are prone to crop up and instant remedies are crucial to carrying out businesses in a time sensitive manner.

Even ask the best tech company in the universe Amazon (AMZN), whose move off Oracle’s (ORCL) database software was the ultimate reason for a serious outage in one of its biggest warehouses on this past Amazon Prime Day, according to Amazon’s internal documents.

The faux paux underscores the hurdles Amazon and other companies could face as they seek to move completely off the Oracle legacy database software whose development has stayed relatively stagnant for a generation.

The slipup was minutes and snowballed into excruciating hours on Amazon Prime Day resulting in over 15,000 delayed packages and roughly $90,000 in wasted labor costs.

Crikey!

These numbers didn’t even consider the wasted man-hours spent by developers troubleshooting and solving the errors or any potential lost sales.

When these mammoth tech giants are running at an incredible scale, a small blip can result in job losses, lost revenue, lost time, a slew of IT engineer sackings, and for some smaller companies, an existential crisis.

The large-scale acts as a powerful multiplier to the lost resources and cost, and as you can see with the Amazon debacle, a few hours can make or break a developer’s career.

Fortunately, IT budgets are higher up the food chain than human resource budgets while more than inching up every year. This is the main reason why I believe ServiceNow will outperform Workday.

The proof is in the pudding and when I scrutinize various metrics, the truth is filtered out.

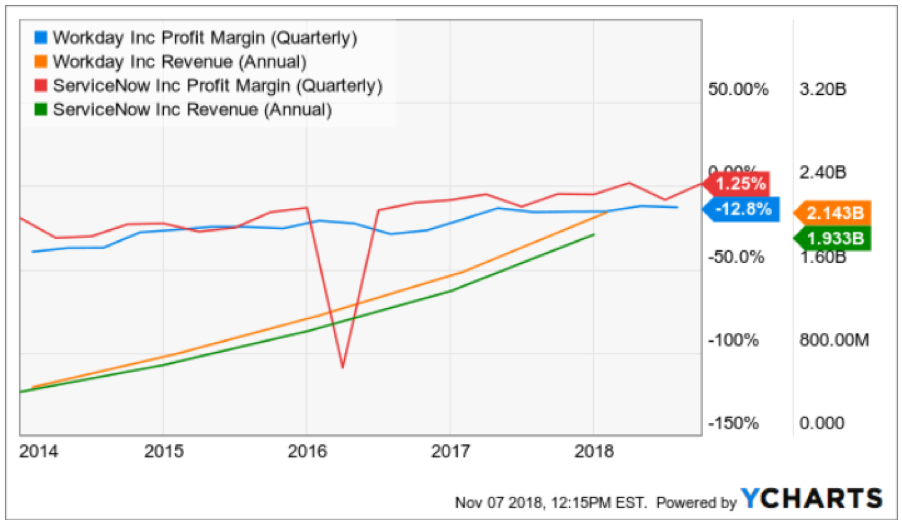

ServiceNow’s quarterly growth rate is 35% which is higher than Workday’s who slipped back to 28% last quarter even though the 3-year growth rate is in the mid-30%.

Put mildly, accelerating sales growth is better than decelerating sales growth.

Both companies have a market cap in the low $30 billion and almost identical annual sales in the $2 billion range.

However, ServiceNow presides over significantly higher quarterly profit margins than Workday and will achieve profitability sooner than Workday.

In short, Workday loses more money than ServiceNow.

I believe in the underlying thesis of HR modernization underpinning Workday’s rapidly growing revenue and this secular trend is here to stay.

But I much rather put my hard-earned money on a company tied to IT modernization which is imminent and harder to put on the backburner because of its strategic position at the forefront of the tech curve.

HR CAN be put on the backburner and kept analog longer, and as the economy inches closer to a recession, this expense will be shifted further away from greener pastures supported by the fact that companies decelerate hiring new talent in poor economic environments.

To wrap it up, I do believe ServiceNow is the Burmese python consuming a cow, but that doesn’t mean I am bearish on Workday.

Workday will flourish, just not as much on a relative basis as ServiceNow.

Effectively, these stocks are well placed to move higher even after the violent moves upward this year. As the economic cycle moves further into the late innings, the importance of cloud-based software companies will become magnified further.

As for the software week at the Mad Hedge Technology letter, these solid five picks will offer deep insight into one of the most compelling parts of the internet sector.

As many observers have found out, not all tech firms are created equal and that is made even trickier with the existence of the vaunted FANGs who are the real Burmese python in the current tech landscape.

“I don't write about Google except to insult the company.” – Said Co-Founder of Recode Kara Swisher

Mad Hedge Technology Letter

November 7, 2018

Fiat Lux

Featured Trade:

(THE RELIABILITY OF ADOBE)

(ADBE), (GOOGL), (ZEN), (TWLO), (SQ)

Tech companies have a habit of suddenly coming and going because of the nature of the relentless environment that spits out losers and celebrates winners.

It’s hard-pressed to find software companies that pass the test of time but there is one that is healthily chugging along that most people know quite well.

Adobe (ADBE) was established 35 years ago in co-founder John Warnock's garage.

This legacy software company’s name, Adobe, was named after the Adobe Creek in Los Altos, California, which ran behind Warnock's house.

Adobe cut its teeth in an era when tech CEOs were not larger-than-life cult figures, and all Adobe has done is quietly infiltrating its way into everybody’s devices by way of Adobe Flash Player and its smorgasbord of useful software applications.

Adobe acquired Macromedia in 2005 which was responsible for building Adobe Flash Player.

This Macromedia software has been developed and distributed by Adobe Systems ever since the purchase and its functions involve viewing multimedia contents, executing rich internet applications, and streaming audio and video. Flash Player can run from a web browser as a browser plug-in or on supported mobile devices.

Flash player was its second hit success software program after its Adobe Acrobat and Reader software introduced PDF, the Portable Document Format, which is still ubiquitously used today even after all these years.

Most software companies are relatively new to the scene and like companies I have recently written about such as Zendesk (ZEN) and Twilio (TWLO), they can brag about growing sales of 30% or 40% plus per year.

Adobe isn’t too shabby itself growing sales at over 24% annually – remarkably high for such an ancient tech company.

The company’s strengths are similar to that of Apple (AAPL) – high-quality products and high profitability.

There will be no back-to-back doubling of the stock like some hyper-growth tech stocks because Adobe doesn’t subscribe to the type of growth trail that Square (SQ) has blazed.

What you can expect from Adobe is a slow grind up in share price stoked by its outperforming EPS expansion and acceptable sales growth of mid-20%.

Its annual operating margins have essentially tripled since the beginning of 2015 from around 10% and now boasts an Apple-like 30%.

There are no bones about it – Adobe has high-quality software across its diversified portfolio.

Other Adobe software products universally soaked up are its stable array of graphic design software such as Adobe Photoshop and Adobe Dreamweaver.

Adobe has also ventured into video editing, animation, and visual effects with Adobe Premiere Pro.

Not only that, Adobe has forayed into more conventional types of software such as digital marketing management software and server software.

Simply put, Adobe’s assortment of digital media software products has a religious-like following especially for iOS users.

As you might have guessed correctly, the lion’s share of Adobe’s revenue stream stems from its software as a service (SaaS) segment contributing 80% to the top line.

More narrowly, the digital media segment makes up almost 70% of the subscription-based revenue. This division will expand at least 20% each year boding well for Adobe to maintain its 20% plus sales growth that any legacy software company would sacrifice a right leg to achieve.

It’s digital marketing software products rub up against stifling competition in Alphabet (GOOGL) amongst others and contribute a less robust 30% to overall sales.

I am less bullish on this part of the business because they have it rough competing against one of the Fangs, the path of less resistance clearly sides with its bread and butter of the digital media offerings.

Its subscription-based pricing model was the catalyst for boosting profitability causing the stock to experience massive price gains. The stock has doubled in the past two years which is unheard of for most legacy software companies.

No longer does Adobe need to manufacture the ancient CD of yore physically delivering it to customers, users can briskly download these products directly from the official website, receive constant upgrades over broadband internet, and pay Adobe monthly for their humble services.

In fact, any investors looking for some hot software stocks only need to find companies that recently shifted to a subscription-based pricing model. It’s pretty much a license to print money if the software quality can backup the monthly costs for the user.

I can tell you that Adobe’s software has remained world class, embedded at the heart of most digital devices at home and in the office, and who would have thought that just a little shift to the pricing model would have doubled the stock price?

Well, instead of one-off sales, Adobe can book revenue month after month, and year after year demonstrating the supercharged effect of shifting to a recurring revenue stream model.

Highlighting the pivot to profitability is Adobe’s three-year EPS growth rate of 48% turning this company into a mammoth software company with a $117 billion market cap.

Another positive for Adobe’s future sales are its fertile addressable markets in Europe and Asia.

There is ample room to expand in these geographical regions with Europe already chipping in with almost $2 billion of revenue per year and Asia with another $1 billion.

Future harvests look even more bountiful.

These two regions make up almost 40% of sales and as the Asian middle class is poised to elevate a giant swath of its people to middle class, Adobe will be a handsome beneficiary of this trend as middle-class families tend to pump out more university graduates who migrate to software-based occupations.

Even though Adobe isn’t the sexiest name out there, it certainly is in the category of “safe.”

In no way do I see an eradication of its embedded software spread widely throughout the tech universe.

Its digital media software tools are best-in-show and loyally followed with a long-lasting revenue stream that has room to grow abroad.

Do not expect Adobe to debut any earth-shattering products, but I fully anticipate Adobe to become even more profitable to the point that they might offer a dividend or reallocate capital to shareholders through stock buybacks.

Apple has similar strengths in its business model, albeit on a much grander scale.

I feel that Adobe doesn’t get the credit it deserves because of its steady as it goes drivers that keep motoring higher in an industry that adores groundbreaking products that revolutionize the world.

I would wait for a major sell-off because a double in two years has bid up the stock to expensive levels represented in its premium forward PE multiple of 35.

However, as the conclusion of the mid-term elections offers some certainty to the market, tech stocks could get swept up in a positive rush to round out the year.

Luckily for Mad Hedge Tech readers, this is the golden age for software companies and we are just scratching the surface of the capability software efficiencies can deliver to small and large companies across every bit of the economy.

Another Apple-like similarity is that Adobe is annually voted one of the best places to work according to Fortune, stacked up against companies represented across the full economic spectrum and not just tech.

If you have a kid, tell him to find a job in San Jose, he or she could find worse places to cut a paycheck.

“You are cruising along, and then technology changes. You have to adapt.” – Said Silicon Valley Venture Capitalist Marc Andreessen

Mad Hedge Technology Letter

November 6, 2018

Fiat Lux

Featured Trade:

(THE GREAT TECH COMPANY YOU’VE NEVER HEARD OF)

(TWLO), (ROKU), (MSFT), (SQ), (AMD), (CRM), (SEND)