“Growth and comfort do not coexist.” – Said CEO of IBM Ginni Rometty

“Growth and comfort do not coexist.” – Said CEO of IBM Ginni Rometty

Mad Hedge Technology Letter

October 30, 2018

Fiat Lux

Featured Trade:

(HOW ARTIFICIAL INTELLIGENCE WILL ENHANCE OR DESTROY YOUR PORTFOLIO)

(TSLA), (AMZN), (FB)

Anti-AI physicist Professor Stephen Hawking was a staunch supporter of preserving human interests against the future existential threat from machines and artificial intelligence (AI).

He was diagnosed with motor neuron disease, more commonly known as Lou Gehrig's disease, in 1963 at the age of 21 and sadly passed away March 14, 2018, at the age of 76.

Famed for his work on black holes, Professor Hawking represented the human quest to maintain its superiority against quickly advancing artificial acculturation.

His passing is a huge loss for mankind as his voice was a deterrent to AI's relentless march to supremacy. He was one of the few who had the authority to opine on these issues. Gone is a voice of reason.

Critics have argued that living with AI poses a red alert threat to privacy, security, and society as a whole. Unfortunately, those most credible and knowledgeable about AI are tech firms. They have shown that policing themselves on this front is remarkably unproductive.

Mark Zuckerberg, CEO of Facebook (FB), has labeled naysayers as irresponsible and dismissed the threat. After failing to prevent Russian interference in the last election, he is exhibiting the same defensive posture translating into a de facto admission of guilt. His track record of shirking accountability is becoming a trend.

Share prices will materially nosedive if AI is stonewalled and development stunted. Many CEOs who stake careers on doubling or tripling down on AI cannot see it die out. There is too much money to lose.

The world will see major improvements in the quality of life in the next 10 years. But there is another side of the coin in which Zuckerberg and company refuse to delve into the dark side of technology.

Defective Amazon (AMZN) Alexa has been producing unexplained laughter because of a mistaken command to start laughing. Despite avoiding calamity, these small events show the magnitude of potential chaos capable of haywire AI functions. If one day, a user attempts to order a box of tissues and Alexa burns down the house, who is liable?

Tesla's (TSLA) CEO Elon Musk has shared his anxiety about robots flipping the script on humans. Elon acknowledges that AI and autonomous vehicles are important factors in the battle for new technology. The winner is yet to be determined as China has bet the ranch with unlimited resources from Chairman Xi.

Musk has hinted that robots and humans could merge into one species in the future. Is this the next point of competition among tech companies? The future is murky at best.

Bill Gates noted that robots should be taxed like humans. This reflects the bubble in which the ultra-elite reside. This comment implies that humans and robots are on the same level and shows a severe lack of empathy for the 40% of working Americans who will be replaced by machines over the next 10 years.

The West is comprised of a deeply hierarchical system of winners and losers. Hawking's premise that evolution has inbuilt greed can be found in the underpinnings of America's economic miracle.

Wall Street has bred a culture that is entirely self-serving regardless of the bigger system in which it finds itself.

Most of us are participating in this perpetual money game chase because our system treats it as a natural part of life. AI will help more people do well in this paper chase to the detriment of the majority.

Quarterly earnings performance is paramount for CEOs. Return value back to shareholders or face the sack in the morning. It's impossible to convince anyone that America's capitalist model is deteriorating in the greatest bull market of all time.

Wall Street has an insatiable hunger for cutting-edge technology from companies that sequentially beat earnings and raise guidance. Flourishing technology companies enrich the participants creating a Teflon-like resistance to downside market risk.

The issue with Professor Hawking's work is that his time frame is too far in the future. Professor Hawking was probably correct, but it will take 25 years to prove it.

The world is quickly changing as science fiction becomes reality. The year 2019 will signal the real beginning of AI in tangible form when autonomous fleets flood main streets.

People on Wall Street are a product of the system in place and earn a tremendous amount of money because they proficiently execute a specialized job. Traders are busy focusing on how to move ahead of the next guy.

Firms building autonomous cars are free to operate as is. Hyper-accelerating technology spurs on the development of AI, machine learning and enhanced algorithms. Record profits will topple and investors will funnel investments back into an even narrower grouping of technology stocks.

Professor Hawking said we need to explore our technological capabilities to the fullest in order to avoid extinction. In 2018, exploring these new capabilities still equals monetizing through the medium of products and services.

This is all bullish for equities as the leading companies associated with AI will not be subject to any imminent regulation, blowback or government intervention.

The only solution is keeping companies accountable by a function of law or creating a third-party task force to regulate AI.

In 2018, the thought of overseeing robots sounds crazy. However, by 2019, it might be as normal as uncontrollable laughter from your smart home.

Mad Hedge Technology Letter

October 29, 2018

Fiat Lux

Featured Trade:

(THE DIGITAL NOMAD ISSUE)

"As tech leaders, we have to admit that we are hugely disconnected with our nation. I don't like it but have to recognize this issue," - said current CEO of Uber Dara Khosrowshahi in 2016.

Mad Hedge Technology Letter

October 25, 2018

Fiat Lux

Featured Trade:

(HOW ENVIRONMENTALISTS MAY KILL OFF BITCOIN),

(BTC), (ETH), (TWTR), (SQ)

If Jack Dorsey's proclamation that bitcoin will be anointed as the global "single currency," it could spawn a crescendo of pollution the world has never seen before.

In a candid interview with The Times of London, Dorsey, the workaholic CEO of Twitter (TWTR) and Square (SQ), offered a 10-year time horizon for his claim to come to fruition.

The originators of cryptocurrency derive from a Robin Hood-type mentality circumnavigating the costly fees and control associated with banks and central governments.

Unfolding before our eyes is a potential catastrophe that knows no limits.

Carbon emissions are on track to cut short 153 million lives as environmental issues start to spin out of control while the world's population explodes to 9.7 billion in 2050, from 8.5 billion people in 2030, up from the 7.3 billion today.

All these people will need to barter in bitcoin, according to Jack Dorsey.

Cryptocurrency is demoralizingly energy-intensive, and the recent institutional participation in crypto server farms will exacerbate the environmental knock-on effects by displacing communities, destroying wildlife, and climate-changing carbon emissions.

This seemingly controversial means to outmaneuver the modern financial system has transformed into a murky arms race among greedy cryptocurrency miners to use the cheapest energy sources and the most efficient equipment in a no-holds-barred money grab.

Bitcoin and Ethereum mining combined with energy consumption would place them as the 38th-largest energy consuming country in the world - if they were a country - one place ahead of Austria.

Mining a bitcoin adjacent to a hydropower dam is not a coincidence. In fact, these locales are ground zero for the mining movement. The common denominator is the access to cheap energy usually five times cheaper than standard prices.

Big institutions that mine cryptocurrency install thousands of machines packed like a can of sardines into cavernous warehouses.

In 2015, a documentary detailed a large-scale foreign mining operation with an electricity outlay of $100,000 per month creating 4,000 bitcoins. These are popping up all over the world.

An additional white paper from a Cambridge University study uncovered that 58% of bitcoin mining comes from China.

Cheap power equals dirty power. Chinese mining outfits have bet the ranch on low-cost coal and hydroelectric generators. The carbon footprint measured at one mine per day emitted carbon dioxide at the same rate as five Boeing 747 planes.

The Chinese mining ban in January set off a domino effect with the Chinese mining operations relocating to mainly Canada, Iceland, and the United States.

Effectively, China has just exported a tidal wave of new pollution and carbon emissions.

Bitcoin is mined every second of every day and currently has a supply of approximately 17 million today, up from 11 million in 2013.

Bitcoin's electricity consumption has been elevated compared to alternative digital payment currencies because the dollar price of bitcoin is directly proportional to the amount of electricity that can profitably be used to mine it.

To add more granularity, miners buy more servers to maintain profitability then upgrade to more powerful servers. However, the new calculating power simply boosted the solution complexity even faster.

Mines are practically outdated upon launch and profitability could only occur by massively scaling up.

Consumer grade personal computers are useless now because the math problems are so advanced and complicated.

Specialized hardware called Application-Specific Integrated Circuit (ASIC) is required. These mining machines are massive, hot, and guzzle electricity.

Bitcoin disciples would counter, describing the finite number of bitcoins - 21 million. This was part of the groundwork laid down by Satoshi Nakamoto (a pseudonym), the anonymous creator of bitcoin when he (or they) constructed the digital form of money.

Nakamoto could not have predicted his digital experiment backfiring in his face.

The bottom line is most people use bitcoins to literally create money out of thin air in digital form, rather than using it as a monetary instrument to purchase a good or service.

That is why people mine cryptocurrency, period.

Now, excuse me while I go into the weeds for a moment.

Enter hard fork.

A finite 21 million coins is a misnomer.

A hard fork is a way for developers to alter bitcoin's software code. Once bitcoin reaches a certain block height, miners switch from bitcoin's core software to the fork's version. Miners begin mining the new currency's blocks after the bifurcation creating a new chain entirely and a brand-spanking new currency.

Theoretically, bitcoin could hard fork into infinite new machinations, and that is exactly what is happening.

Bitcoin Cash was the inaugural hard fork derived from the bitcoin's blockchain, followed by Bitcoin Gold and Bitcoin Diamond.

Recently, the market of hard fork derivations includes Super Bitcoin, Lightning Bitcoin, Bitcoin God, Bitcoin Uranium, Bitcoin Cash Plus, BitcoinSilver, and Bitcoin Atom.

All will be mined.

The hard fork phenomenon could generate millions of upstart cryptocurrency server farms universally planning to infuse market share because new currencies will be forced to build up a fresh supply of coins.

If Peter Thiel's prognostication of a 20% to 50% chance of bitcoin's price rising in the future is true, it could set off a cryptocurrency server farm mania.

By the way, Thiel also believes that there is a 30% chance that Bitcoin could go to zero.

A surge in the price of bitcoin results in mining cryptocurrency operations everywhere by any type of electricity, especially if the surge maintains price stability. Even mining in Denmark, where one finds the world's costliest electricity at $14,275 per bitcoin, would make sense.

Recently, miners' appetite for power is causing local governments to implement surcharges for extra infrastructure and moratoriums on new mines. Even these mines built adjacent to hydro projects are crimping the supply lines, and consumers are forced to buy power from outside suppliers. Miners are often required to pay utility bills months in advance.

By July 2019, mining will possibly need more electricity than the entire United States consumes. And by February 2020, bitcoin mining will need as much electricity as the entire world does today, according to Grist, an environmental news website.

Geographically, most locations around the world were profitable based on May's bitcoin price of $10,000.

However, the sudden slide down to $6,400 reaffirms why the Mad Hedge Technology Letter avoids this asset class like the plague.

The most unrealistic operational locations are distant, tropical islands, such as the Cook Islands at $15,861, to mine one bitcoin.

If you'd like to drop your life and make a fortune mining bitcoin, then Venezuela is the most lucrative at $531 per bitcoin.

As bitcoin's nosedive perpetuates, Venezuela might be the last place on earth with mining farms.

Who doesn't like free money? Set up a few devices, crank up the power, collect the coins, pay off the electricity bill, pocket the difference and hopefully the world - or Venezuela - hasn't keeled over by then.

"If privacy is outlawed, only outlaws will have privacy," - said Philip R. "Phil" Zimmermann, Jr., creator of the most widely used email encryption software in the world.

Mad Hedge Technology Letter

October 24, 2018

Fiat Lux

Featured Trade:

(HERE'S AN EASY WAY TO PLAY ARTIFICIAL INTELLIGENCE),

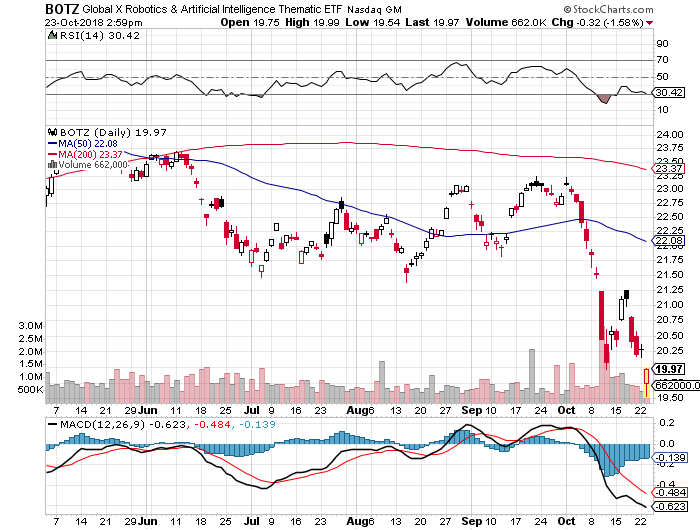

(BOTZ), (NVDA), (ISRG)

Suppose there was an exchange-traded fund that focused on the single most important technology trend in the world today.

You might think that I was smoking California's largest export (it's not grapes). But such a fund DOES exist.

The Global X Robotics & Artificial Intelligence ETF (BOTZ) drops a gilt-edged opportunity into investors' laps as a way to capture part of the growing movement behind automation.

The fund currently has an impressive $2.2 billion in assets under management.

The universal trend of preferring automation over human labor is mushrooming with each passing day. Suffice to say there is the unfortunate emotional element of sacking a human and the negative knock-on effect to the local community like in Detroit, Michigan.

But simply put, robots do a better job, don't complain, don't fall ill, don't join unions, or don't ask for pay rises. It's all very much a capitalist's dream come true.

Instead of dallying around in single stock symbols, now is the time to seize the moment and take advantage of the single seminal trend of our lifetime.

No, it's not online dating, gambling, or bitcoin, it's Artificial Intelligence.

Selecting individual stocks that are purely exposed to AI is a challenging endeavor. Companies need a way to generate returns to shareholders first and foremost, hence, most pure AI plays do not exist right now.

However, the Mad Hedge Fund Trader has found the most unadulterated AI play out there. A real diamond in the rough.

The best way to expose yourself to this AI trend is through Global X Robotics & Artificial Intelligence ETF (BOTZ).

This ETF tracks the price and yield performance of ten crucial companies that sit on the forefront of the AI and robotic development curve. It invests at least 80% of its total assets in the securities of the underlying index. The expense ratio is only 0.68%.

Another caveat is that the underlying companies are only derived from developed countries. Out of the 10 disclosed largest holdings, seven are from Japan, two are from Silicon Valley, and one, ABB Group, is a Swedish-Swiss multinational headquartered in Zurich, Switzerland.

Robotics and AI walk hand in hand, and robotics are entirely dependent on the germination prospects of AI. Without AI, robots are just a clunk of heavy metal.

Robots require a high level of AI to meld seamlessly into our workforce. The stronger the AI functions, the stronger the robot's ability, filtering down to the bottom line.

AI-embedded robots are especially prevalent in the defense industry, automobile manufacturing, and heavy industrial machinery. The industrial robot industry projects to reach $80 billion per year in sales by 2024 as more of the workforce gradually becomes automated.

The robotic industry has become so prominent in the automotive industry that they constitute greater than 50% of robot investments in America.

Let's get the ball rolling and familiarize readers of the Mad Hedge Technology Letter with the most influential weightings in the underlying ETF (BOTZ).

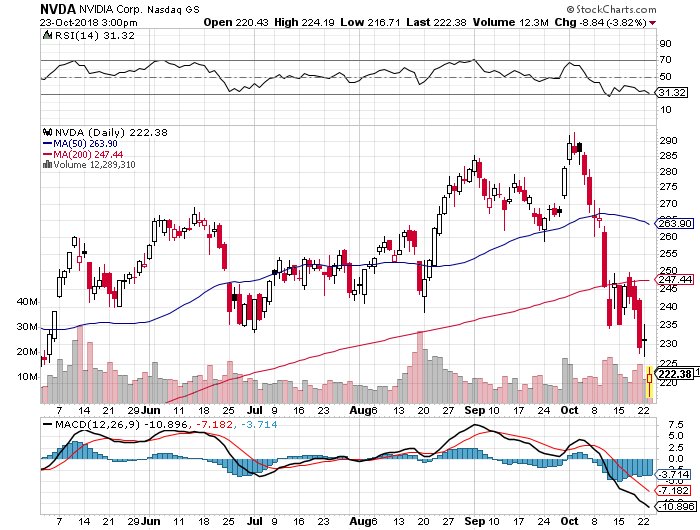

Nvidia (NVDA)

Nvidia Corporation is a company I often write about as their main business is producing GPU chips for the video game industry.

This Santa Clara, California based company is spearheading the next wave of AI advancement by focusing on autonomous vehicle technology and AI-integrated cloud data centers as their next cash cow.

All these new groundbreaking technologies require ample amounts of GPU chips. Consumers will eventually cohabitate with state of the art IOT products (internet of things), fueled by GPU chips, coming to mass market like the Apple Homepod.

The company is led by genius Jensen Huang, a Taiwanese-American who cut his teeth as a microprocessor designer at competitor Advanced Micro Devices (AMD).

Nvidia constitutes a hefty 6.60% of the BOTZ ETF.

To visit their website please click here.

Yaskawa Electric (Japan)

Yaskawa Electric is the world's largest manufacturer of AC Inverter Drives, Servo and Motion Control, and Robotics Automation Systems, headquartered in Kitakyushu, Japan.

It is a company I know well, having covered this former zaibatsu company as a budding young analyst in Japan 45 years ago.

Yaskawa has fully committed to improving global productivity through Automation. Yaskawa was recently switched out of the index in favor of an American newcomer John Bean Technologies specializing in the food processing and air transportation industries. Nevertheless, Yaskawa is still a company to have on your radar screen.

To visit Yaskawa's website, please click here.

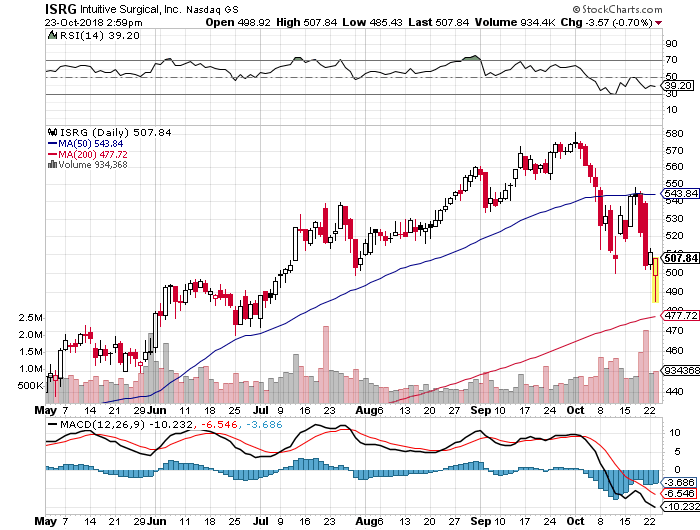

Intuitive Surgical (ISRG)

Intuitive Surgical Inc (ISRG) trades on Nasdaq and is located in sun-drenched Sunnyvale, California.

This local firm designs, manufactures, and markets surgical systems and is industriously focused on the medical industry.

The company's da Vinci Surgical System converts the surgeon's hand movements into corresponding micro-movements of instruments positioned inside the patient.

The products include surgeon's consoles, patient-side carts, 3-D vision systems, da Vinci skills simulators, and da Vinci Xi integrated table motions.

This company comprises 7.71% of BOTZ. To visit their website, please click here.

Fanuc Corp. (Japan)

Fanuc was another one of the hit robotics companies I used to trade in during the 1970s and I have visited their main factory many times.

The 4thlargest portion in the (BOTZ) ETF at 6.11% is Fanuc Corp. This company provides automation products and computer numerical control systems, headquartered in Oshino, Yamanashi.

They were once a subsidiary of Fujitsu, which focused on the field of numerical control. The bulk of their business is done with American and Japanese automakers and electronics manufacturers.

They have snapped up 65% of the worldwide market in the computerized numerical device market (CNC). Fanuc has branch offices in 46 different countries.

To visit their company website, please click here.

Keyence Corp (Japan)

Keyence Corp is the leading supplier of automation sensors, vision systems, barcode readers, laser markers, measuring instruments, and digital microscopes.

They offer a full array of service support and closely work with customers to guarantee full functionality and operation of the equipment. Their technical staff and sales teams add value to the company by cooperating with its buyers.

They have been consistently ranked as the top 10 best companies in Japan and boast an eye-opening 50% operating margin.

They are headquartered in Osaka, Japan and make up 6.10% of the BOTZ ETF.

To visit their website please click here.

(BOTZ) does has some pros and cons. The best AI plays are either still private at the venture capital level taken over by the SoftBank Vision Fund wielding its war chest of $100 billion or a Silicon Valley mainstay such as Andreessen Horowitz.

You also need to have a pretty broad definition of AI to bring together enough companies to make up a decent ETF.

However, it does get you a cheap entry into many for the illiquid foreign names in this fund.

Automation is one of the reasons why this is turning into the deflationary century and I recommend all readers who don't own their own robotic led business, pick up some Global X Robotics & Artificial Intelligence ETF (BOTZ).

And by the way, the entry point right here on the charts is almost perfect.

To learn more about (BOTZ) please visit their website by clicking here.