“I think that you do it exactly the same way that you regulated the cigarette industry. Here’s a product: Cigarettes. They’re addictive, they’re not good for you.” – Said Founder and CEO of Salesforce Marc Benioff when asked about Facebook

“I think that you do it exactly the same way that you regulated the cigarette industry. Here’s a product: Cigarettes. They’re addictive, they’re not good for you.” – Said Founder and CEO of Salesforce Marc Benioff when asked about Facebook

Mad Hedge Technology Letter

October 23, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

"Life is not fair; get used to it," said the founder of Microsoft, Bill Gates.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Technology Letter

October 22, 2018

Fiat Lux

Featured Trade:

(FACEBOOK’S DARPA DALLIANCE),

(FB), (GOOGL), (AAPL)

How far will society and government allow tech companies to adventure before there is some blowback?

Honestly, it’s hard to say when to put the shackles on these companies that are getting too powerful for their own good.

Tech companies have been pedal to the medal pushing the limitations of what the human world can offer.

The hoard of profits showered on the tech giants is one thing, but should they be held accountable for the unintended consequences that there robot-like profit-making operations dump on society?

Each company has chosen different ways to deploy the capital. Apple decided to reward shareholders by executing a $100 billion share buyback program.

The stock has performed great this year.

Apple (AAPL) and CEO Tim Cook have been keen to show a trustful face among a growing phalanx of data misusers.

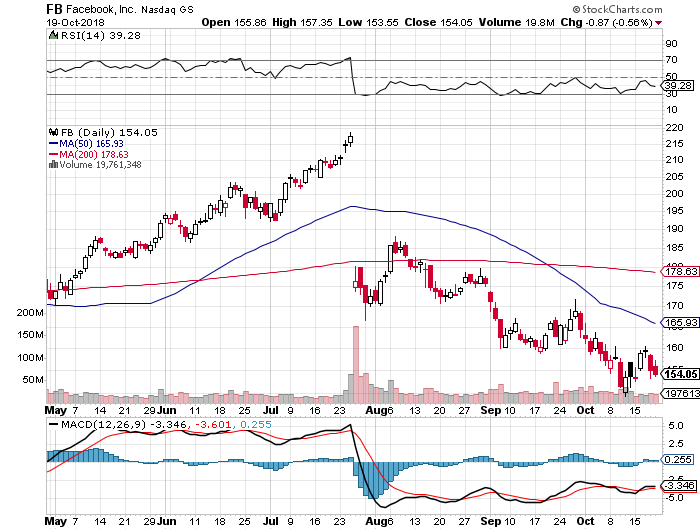

Facebook (FB) has used the surplus capital to build a secretive research center modeled after the Defense Advanced Research Projects Agency (DARPA) called Building 8.

DARPA is an agency of the United States Department of Defense responsible for the development of emerging technologies for military use.

The division of the government was launched in 1958 by United States President Dwight D. Eisenhower to counteract the Soviet launching of Sputnik 1 in 1957.

DARPA smartly partnered together with America’s business leaders, academia, and other talents dotted around the government and military branches to develop projects that would broaden the frontiers of technology and science far beyond immediate U.S. military current needs.

Building 8 met the real world for the first time when its first product Portal, a vertically-shaped display screen attached to a smart camera, debuted with befuddlement.

How does a company that just announced a breach of 50 million accounts, after a torrid string of mishaps which made a mockery of Facebook’s use of big data, launch a device that gives Facebook unfettered access into the confines of one’s personal home?

A Facebook spokesman said that Facebook will “use this information to inform the ads we show you across our platforms. Other general usage data, such as aggregate usage of apps, etc., may also feed into the information that we use to serve ads.”

Executives at Facebook know that this product would be a commercial write-off, but the sunk cost associated with this project forced them to throw it on the market with reckless abandon.

And at the end of the day, some data is better than no data at all and that is what the earth’s existence is boiling down to.

So, if you thought that Facebook might finally decide to stop being your effective cyber-stalker, you are wrong.

And this is all just the beginning, it gets a lot worse than this, let me explain.

In fact, Facebook’s Building 8 was led by the former Director of the Defense Advanced Research Projects Agency Regina Dugan.

The more I sniff around, the more I see her pawprints everywhere she went.

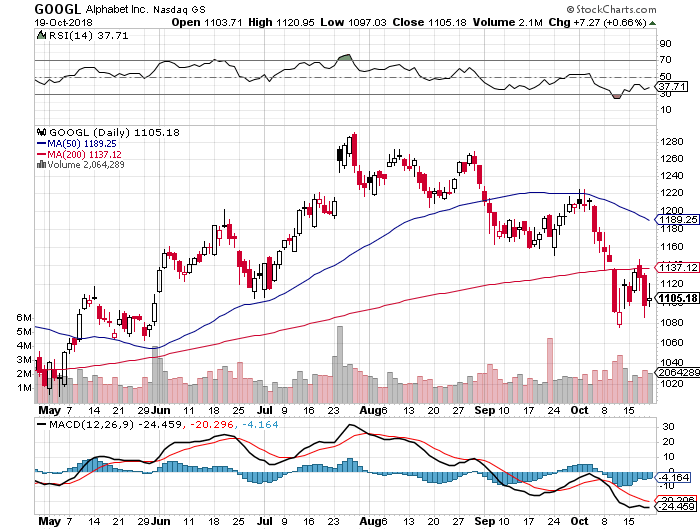

Dugan used her elite role at DARPA to score a job at Google’s (GOOGL) Advanced Technology and Projects (ATAP) group before she jumped ship to Facebook’s secretive research center Building 8.

Dugan’s tenure at DARPA from 1996 to 2012 meant she was privy to the LifeLog project which was developed for just one year and subsequently shut down.

This program was cancelled after heavy criticism from activists advocating privacy and rightly so.

But, was this program really shut down?

Lifelog was a program with the mission to effectively record all of an individual’s physical movements, conversations and everything they listened to, ate, read and bought.

Everything!

The premise of this program was to cultivate a permanent searchable record of one’s life.

The daredevil program was light years ahead of its time predating the iPhone, tablet, and the current wave of populism engulfing the free world.

Back then, the weaponizing of consumer technology was largely absent from the world, and the top brass of DARPA surely wasn’t naïve enough to believe that this technology could only be applied to create an epic cyber-diary of one’s life.

In any case, Dugan conveniently was employed by Google and Facebook and her knowledge of Lifelog was fluid, deep and comprehensive.

Unintended consequences are rife and, if I connect the dots, it appears that DARPA’s Lifelog found new spawning grounds in Silicon Valley’s richest companies, or at least two of them.

There is no way to know for sure, but monetizing Lifelog’s cyber-record technology to harness it as a tool to collect personal information for the use of digital ad targeting has rained profits down on these two companies.

Building 8 is serving up round two of its DARPA-esque mission by announcing that they have built a prototype producing an armband that will facilitate the understanding of oral language “through a person’s skin.”

It was in January 2017 when Dugan took the stage in San Jose at a conference to announce this project.

It was mostly dismissed as fantasy and something out of science fiction.

Well, it’s one more step closer to being rolled out in mass market form.

The way the language process works is that vibrations allow for the roots of words to be transformed into silent speech.

If scientists manage to do this, it would give deaf people a new lifeline giving them the capability to understand what people are saying without the need for lip reading.

However, on the other side of the coin, the technology could be modified to aid spies in eavesdropping if the range of the vibrations allows them to.

The second project announced by Dugan that same night in San Jose was Facebook’s bold attempt of a noninvasive brain sensor designed to turn thoughts into text.

This would require brain surgery to install a sensor, and the plan for this technology is for people to access devices from their brain without the need to physically or orally communicate with it.

I suspect that Facebook would collect the data from this brain sensor and the sensor would be in contact with the Facebook infrastructure sharing the performance and state of operations.

If the sushi hits the fan and a person dies from the sensor, Facebook would need to analyze the specific details in the malfunction.

What a scary thought.

Facebook adopting the DARPA blueprint from its halted project of Lifelog to respawn similar technology that painstakingly retrieves as much data about our lives as possible is the first step to something substantially bigger.

However, the digital ad business has made Facebook and Google insanely rich and they want an encore.

I am surprised that other Silicon Valley cash-rich companies avoid tapping up the offspring of other military-grade technology to join the profit parade.

Apparently, there has been zero backlash from it.

If Facebook somehow manages to roll-out a commercialized brain sensor giving Mark Zuckerberg access to our minds, I wonder what on earth could round three entail for Zuckerberg…

Nothing is impossible.

“What’s dangerous is not to evolve.” – Said Founder and CEO of Amazon Jeff Bezos

Mad Hedge Technology Letter

October 18, 2018

Fiat Lux

Featured Trade:

(UNDERSTANDING THE REAL COMPETITION),

(SPOT), (AAPL), (GOOGL), (MSFT), (HUAWEI)

Microsoft sells computers?

That was the bizarre look I got after telling my friend that Microsoft (MSFT) is in the business of selling laptops, desktop computers, and tablets that convert into laptops from a product line called Microsoft Surface.

This is not your father’s Microsoft.

Things are different now.

Everything changed once they got rid of Steve Ballmer whose inertia prevented Microsoft from taking advantage of the huge influence they culled in the tech sector from being the universal operating system for PCs.

Ballmer’s lack of technical expertise was his own downfall stemming from his terrible decision to buy Nokia’s handset business for $7.6 billion.

The board of directors forced him out and was a blessing in disguise.

Thousands were laid off in the Nokia handset division and a massive write-down was taken.

As big tech spread out their wings and branch off into various businesses they never imagined before, they have reinvented the former images of themselves.

This goes for Microsoft who’s taking their legacy business of Microsoft Office and Windows and leveraging it with the cloud to create a stellar product.

And with the cash hoard, not only are they creating new products by fusing together old products with new technologies, they are overlapping into other big tech companies’ turf.

The overlapping products can be seen in hardware products made by this software behemoth and their neighbors.

The Microsoft Surface division is up 25% YOY speaking volumes to the quality hardware Microsoft produce now even if you didn’t know about it.

Apple (AAPL) has attracted most of the conversation in the "smart" headphones space because of the AirPods.

The sleek white earbuds are becoming ubiquitous with the headphone space trending to a smaller and "true" wireless.

A schism has formed as the AirPods don’t satisfy the entire spectrum of smart headphone fans.

The retro ear-muff shaped headphone with more immersive sound is what I am talking about, and I do recognize that Beats has been in the market for a decade.

Microsoft chose to go this route with their smart headphones and this is their answer to the iconic AirPods and the Google (GOOGL) Pixel Buds.

This smart headphone comes with an embedded digital assistant and integrates noise cancellation.

I tried out the Microsoft's Surface Headphones before they came on the market, and I only had positive things to say about the quality and experience.

They sound impressive, the controls are easy to use, and the modern design is definitely a plus.

The color could use a little reimagination but all in all, I was pleased.

Microsoft Cortana, Microsoft’s digital assistant, for all who don’t know, is also slipped into the experience and a tap on the right earcup will summon Cortana.

It seems that Microsoft still needs a few kinks to work out with Cortana, but voice activation and smart assistants like Siri and Google Assistant can be found in almost every hardware and software product now.

Headphones are city workers’ second most important smart device because of its functionality.

Have you ever been on the New York metro and seen how many people are wearing smart headphones?

Quality headphones shut off the outside world and warm up the insides with the user’s favorites on Spotify (SPOT) or Apple Music.

Stressing out on the commute into work in an Uber is common and calming the frayed nerves before workers enter into the office of dungeons and dragons has a type of value that can never be replicated.

Urban dwellers need high-quality smart headphones and these big tech companies are acutely aware of this.

Google has made an audacious attempt to integrate real-time foreign translation into the Pixel Buds. It only works with Google’s Pixel phones, is hard to operate, and needs the Google Translate app on the phone.

It’s a good first step but the applications using smart headphones are endless.

Smart assistants are the key.

As they become more adept at processing the real world, they streamline and better a human’s life.

Microsoft’s smart headphones have embedded Skype, one of Ballmer’s positive acquisitions during his tenure. And with Cortana integration, it could morph into a natural extension of the Windows 10 experience.

Microsoft’s smart headphones morph into a point of conversion for more of Microsoft’s hardware products as they start to construct an expanding moat.

Headphones used to be more or less the same.

Plug it into the jack and you’re on your merry way.

The headphones of today are looking more different from each other with every iteration.

This was glaringly evident when Apple chose to no longer sell any phones with a 3.5mm headphone jack.

Ironically enough, Google dumped the headphone jack with its Pixel 2 phones a year later even though they bashed Apple for it a few months earlier.

The reason was mainly functional as Google said, “We want the display to go closer and closer to the edge.”

Gradually, smartphones will get rid of everything except a razor-thin screen. All the other clunky business in and around it needs to go. This is the first step and home buttons have been chopped off smartphones as well.

It is fine to get consumed in the battle of smart products between Silicon Valley companies, but there is a larger threat.

Chinese smart products are rapidly catching up to what American companies can produce.

The Middle Kingdom hasn’t surpassed American tech expertise yet but they are debuting devices relative to the competition that could only be dreamed about a few years ago.

Huawei's flagship smartphone Mate 20 and Mate 20 Pro pack a lot of punch and this must be frightening to the FANGs.

The timing of the phone debut is a big victory for American smartphone companies because this phone is good enough to grab market share from existing American companies but aren’t allowed to sell inside America.

Congress putting the kibosh on any sliver of a chance to partner with an American carrier means that there will be no chance of Chinese phones gutting the American smartphone market.

What it does mean is that they will invade and dominate other markets such as South East Asia, Eastern Europe, and Russia.

The same will go for any Chinese smart device.

Huawei has given up trying to circumvent the government blockade.

The Huawei Mate 20 is priced around $800 and the Mate 20 Pro at $1140. They are probably two of the best smartphones ever made and are a direct threat to any American company’s revenue that manufactures smartphones and smart devices.

"The idea of Twitter started with me working in dispatch since I was 15 years old, where taxi cabs or firetrucks would broadcast where they were and what they were doing." - Said CEO of Twitter and Square Jack Dorsey