Mad Hedge Technology Letter

April 19, 2024

Fiat Lux

Featured Trade:

(TECH EARNINGS IS THE NEXT CATALYST)

(SMCI), (NVDA), (MSFT)

Mad Hedge Technology Letter

April 19, 2024

Fiat Lux

Featured Trade:

(TECH EARNINGS IS THE NEXT CATALYST)

(SMCI), (NVDA), (MSFT)

It’s been a slap in the face lately in the tech market as the market has realized that rate cuts are not imminent.

The party is over in the short term until a catalyst re-ignites the bull market rally.

The softness has put a real dent into the momentum and trajectory of tech stocks.

Now we are confronted with the sad reality that inflation is here to stay because hot report after hot report is confirming tech investors' greatest fear, that inflation is not transitory like the Fed once said.

In fact, inflation has been a serious problem now for over 4 years and the same Fed that botched the transitory inflation issue is still in charge.

My bet is that they won’t ease prematurely with all the heat they received from the failed transitory inflation call.

Yet here we are with the tech market selling off in the short-term and healthily pulling back.

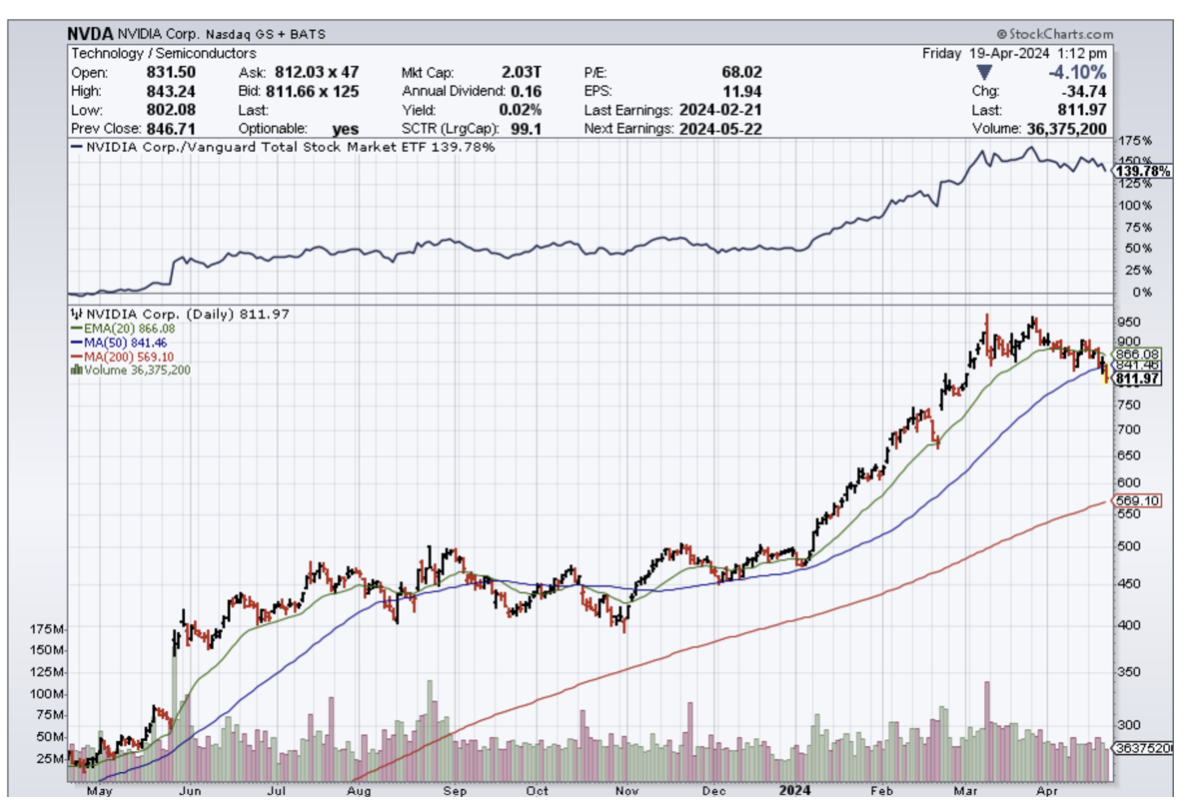

Even AI chip stock Super Micro Computer (SMCI) is back around $750 per share after skyrocketing past $1,200 per share.

The froth for now is ebbing.

Readers had to expect that a consolidation of some kind was in the cards and that is what we are going through right now.

In the near term, earnings are our best hope for a positive catalyst to offset all the negativity about inflation and interest rates.

There is a good chance we don’t even get one rate cut this year with all the hot job numbers, because the data is just too good to ignore.

In the recent stretch of the bull run, investors looked past higher rates, based in part on their belief that policy cuts were around the corner.

With wage growth starting to cool and excess savings draining, asset markets have seemingly stepped in to help sustain US consumption, adding more than $10 trillion to household net worth in the past year.

Companies need to show that they’re capitalizing on economic strength to expand earnings.

The tech market needs to show in the upcoming earnings season that the artificial intelligence optimism that started with the launch of ChaptGPT is more than hype.

Not all earnings outlooks are created equal, of course, and one can imagine a scenario in which AI darlings Nvidia and Microsoft fan optimism.

Consensus is that we will experience about 5% earnings growth for the S&P 500 from the same period last year excluding the volatile energy sector.

Meanwhile, the economy probably grew about 2.9% in the first quarter, according to the Atlanta Fed’s GDP Now tracker, and that should translate into encouraging earnings and outlooks.

I am of the opinion that all the heavy lifting will be done by several tech behemoths that also double-dip in the AI narrative.

This has also created a massive vacuum of weakness after the likes of MSFT and NVDA.

The narrowness of leadership is a result of a winner takes all of the economy and just several corporations consolidating at the top.

Competition is so fierce that it has left Apple and Tesla by the wayside.

We will reach that 5% earnings growth, but strip out a few tech stocks, and that number is likely to be flat or minus.

I believe the narrowness of leadership will be a hallmark of the future bull market and not just some one-off exception.

Some readers have no idea how ultra-competitive it is at the top of the stock market pyramid with companies fighting for the incremental investment dollar.

“I don't look to jump over 7-foot bars: I look around for 1-foot bars that I can step over.” – Said Warren Buffett

Mad Hedge Technology Letter

April 17, 2024

Fiat Lux

Featured Trade:

(AI AND LOWER EMPLOYEE WAGES)

(TSLA)

Students hoping to become bankers shouldn’t study finance, they should dive into programming.

This is the big takeaway from how investment banks are run these days.

Gone are the moments when finance degrees were the hottest commodity, now it is all about generative AI.

Artificial intelligence (AI) could replace the equivalent of 300 million full-time jobs, a report by investment bank Goldman Sachs says.

It could replace a quarter of work tasks in the US and Europe but may also mean new jobs and a productivity boom.

And it could eventually increase the total annual value of goods and services produced globally by 7%.

Generative AI, able to create content indistinguishable from human work, is "a major advancement", the report says.

Silicon Valley is keen to promote investment in AI in not only the United States but in a way that will ultimately drive productivity gains across the global economy.

The report notes AI's impact will vary across different sectors - 46% of tasks in administrative and 44% in legal professions could be automated but only 6% in construction and 4% in maintenance, it says.

Journalists will therefore face more competition, which would drive down wages unless we see a very significant increase in the demand for such work.

Consider the introduction of GPS technology and platforms like Uber (UBER). Suddenly, knowing all the streets in London had much less value - and so incumbent drivers experienced large wage cuts in response, of around 10% according to our research.

The result was lower wages, not fewer drivers.

Over the next few years, generative AI is likely to have similar effects on a broader set of creative tasks.

According to research cited by the report, 60% of workers are in occupations that did not exist in 1940.

However, other research suggests technological change since the 1980s has displaced workers faster than it has created jobs.

Nobody understands how the technology will evolve or how firms will integrate it into how they work.

Lower wages and higher output are a perfect recipe for higher technology share prices and that is exactly what we will get.

Currently, we are experiencing a mild pullback from the AI mania, but that is simply because it got too far ahead of its skis.

I am quite disappointed in the price action in a stock like Tesla (TSLA) which announced a major cut to its global workforce to trim costs.

The staff cut of 10% could result in exactly what I mentioned more output for less pay, but in terms of hiring more workers, they have decided to force fewer workers to do more.

This type of management behavior doesn’t usually pan out well, because it usually leads to an employee rebellion and cratering employee satisfaction.

They will certainly be a major investor in AI chips to outfit their EV cars, but they have signaled to investors that they are experiencing trouble reaching that “2nd wave” of incremental buyers for their car.

Tech as a whole is not in trouble, but individual companies will find an imbalance treatment to their stock.

The AI pixie dust might have leveled off in the short term, and the broader tech market is being dragged down by a confluence of headwinds like spiking interest rates, geopolitical strive, beaten-up consumers, and diminishing addressable market revenue.

I do believe in the AI hype, but these trends don’t go up in a straight line and need time to digest which often results in short-term pullbacks.

Mad Hedge Technology Letter

April 15, 2024

Fiat Lux

Featured Trade:

(APPLE RUNNING OUT OF TIME)

(AAPL)

At some point, Apple (AAPL) might realize that they won’t be able to find that “next big thing.”

That would be a death sentence.

I’ve been warning Apple shareholders for years that they are headed into a growth winter if they can’t find the next big thing to replace the iPhone.

The consensus was that Apple had time to figure it out.

When I say time, Apple management was quite relaxed about it because the iPhone had been making so much money for years.

Management didn’t think they had much to worry about for 5 to 7 years.

But that was then and things have changed.

Tech has advanced with lightning speed and has left Apple in the dust.

The iPhone numbers keep getting worse and Apple is still scratching their head.

The insurmountable lead they had in smartphones should have been used as a springboard into something even grander and more impressive.

Yet here we are over a decade later with Apple barely moving the needle such as changing the color of the lock screen and trying to pass over other minuscule changes as real upgrades.

Other tech behemoths migrating into artificial intelligence have made Apple look even more outdated in 2024.

Reports show Apple has been exploring a mobile robot that can follow users around their homes.

The iPhone company also has developed an advanced tabletop home device that uses robotics to move a display around.

It shelved an electric vehicle project in February, and a push into mixed-reality goggles is expected to take years to become a major moneymaker.

With robotics, Apple could gain a bigger foothold in consumers’ homes and capitalize on advances in artificial intelligence. But it’s not yet clear what approach it might take. Though the robotic smart display is much further along than the mobile bot, it has been added and removed from the company’s product roadmap over the years.

The iPhone accounted for 52% of the company’s $383.3 billion in sales last year leading to many calling the company the iPhone company.

A car had the potential to add hundreds of billions of dollars to Apple’s revenue.

If the work advances, Apple wouldn’t be the first tech giant to develop a home robot. Amazon.com Inc. introduced a model called Astro in 2021 that currently costs $1,600.

A silver lining to Apple’s failed car endeavor is that it provided the underpinnings for other initiatives. The neural engine — the company’s AI chip inside of iPhones and Macs — was originally developed for the car. The project also laid the groundwork for the Vision Pro because Apple investigated the use of virtual reality while driving.

Apple stock is slightly down from the end of 2021.

That’s disheartening news for many shareholders because this stock was the perennial gem that overdelivered on every metric including the share price which is what matters most.

Apple was once the cornerstone of the stock market, and that title has disappeared unceremoniously with its smartphone lead.

With earnings fast approaching, I expect a lackluster report from Apple at best.

Any rallying will be done on less bad news than first expected and many companies already know that is a game you cannot win.

Even worse, the price to find the “next big thing” has multiplied significantly from 10 years ago with the cost of labor, supply parts, and the regulatory mood has soured.

The longer this goes on, the more Apple will be forced to deliver a royal flush when least expected.

The probability of Apple taking back the mantle as the forerunner of tech is dissipating by the day, and I would avoid the stock in the short term.

There is a reason why the stock has slightly down over the past 365 days.

If the stock pops on the earnings, I would be inclined to sell the rally.

Mad Hedge Technology Letter

April 12, 2024

Fiat Lux

Featured Trade:

(THE NEW COMPETITION IN EVS)

(XIAOMI)

It’s a little weird seeing Janet Yellen road-tripping to China to ask the Chinese to stop making such cheap products.

I’ll give her a hint - they won’t stop making cheap products to supply the world.

The U.S. could use cheaper products, especially at the dinner table, but that is another story.

Let’s talk about China and how they are reaching up the value-added tech food chain to fiercely compete with expensive tech products.

Dumping or the non-dumping of “clean energy” products is not something a U.S. Secretary of the Treasury should fly halfway across the world to Asia to lecture a government about what the costs of their products, but that is what Janet did.

It really is the antithesis of a free market economy.

I would argue that lower-cost Chinese products have been rocket fuel for many small American businesses over the past 30 years.

Competition is largely a good phenomenon in the technology sector and brings out the best in terms of quality and price for the end consumer.

Who wants to pay $1 million for a Tesla?

It appears that Janet Yellen wouldn’t mind.

Yellen was not only referencing EVs, but her speech also dived into the cheap pricing of solar power and lithium-ion batteries.

China has been pouring billions into clean energy for years, outpacing the rest of the world including the US in the energy transition and the results are there for the agnostic consumer to see.

Not only are Chinese cell phones just as good as Apple iPhones for half the price, but the new bombshell to rock the menu of tech products is the new EV made by Chinese cell phone company Xiaomi.

Buyers have been told they may have to wait up to 8 months for the car to be delivered.

Xiamo is the third-largest seller of smartphones in the world with a market share of about 12%.

The standard Xiaomi SU7 model is priced at $30,000.

The SU7, which has drawn comparisons with Porsche's Taycan and Panamera models, has a minimum range of 435 miles, beating the Tesla Model 3's 567km.

Xiaomi and its new car, the SU7, will share an operating system with its in-house phones, and other smart devices.

Xiaomi's EVs are made by a unit of state-owned car manufacturer BAIC Group at a plant in Beijing that can produce as many as 200,000 vehicles a year.

Xiaomi has said it will invest $10 billion in its vehicles business over the next 10 years.

Here is the quick hot take from all this geopolitical and economic activity.

EVs are about to get a whole lot cheaper without sacrificing the quality thanks to China. The days of $100,000 EVs are about to be swept into the tech dustbin of history.

The trend mirrors closely the trajectory of Chinese smartphone evolution so much so that consumers will have a chance at real cost savings.

Any non-Chinese automotive company will need to come to the realization that if they don’t compete at the brand-new Chinese price points, demand will evaporate.

It’s a massive dose of reality to stomach for many German car makers, and imagine all those jobs that would be cut in one fell swoop.

The Chinese just know how to make stuff cheaper and nothing will get in the way of that. I urge other companies to embrace this fact and not fight it.

Get ready for a smattering of luxury EV vehicles for $30,000 a pop made from China.

This is no joke.

China has made it their mission to reach up the value-added product chain, and if this isn’t it then I don’t know what is.

“An investment in knowledge pays the best interest.” – Said Benjamin Franklin