Mad Hedge Technology Letter

August 14, 2023

Fiat Lux

Featured Trade:

(MACRO RISKS CLOUD THE PICTURE)

(AAPL), (NVDA), ($COMPQ)

Mad Hedge Technology Letter

August 14, 2023

Fiat Lux

Featured Trade:

(MACRO RISKS CLOUD THE PICTURE)

(AAPL), (NVDA), ($COMPQ)

The momentum signals that tech shares ($COMPQ) are still working themselves out and need more time to stomach Fitch’s debt downgrade.

Unfortunately, it hasn’t been a one-day dip buying opportunity and this month has been quite abysmal for the tech sector.

Just look at Apple which lost about 10% in value. That’s almost unheard of in today’s day and age.

Many investors are still recalibrating what it means to be on the end of a stunning sudden downgrade for the biggest economy in the world.

Making matters worse, the empirical data is starting to really show that China is teetering on the edge.

Centrally planned economies can have their time in the sun, but eventually, that system blows up as inefficiencies become a doom loop with no end.

There is a good chance at this point in his leadership that Chinese Communist Party Chairman Xi cannot get the right information about what is going on in China because the ranks have been solidified by cadres that leech off the system.

China could mean another leg down to close off the year instead of the relief rally that is poised to lift us back from the short-term weakness.

The Nasdaq index has dropped 4.2% this month, with top tech companies like Nvidia on the brink of 10% decreases.

Even Microsoft, despite its advancements in AI and partnership with OpenAI, has seen a 4% drop in August. Google has also shed 2.1%.

However, one tech giant that has been able to maintain a positive trajectory is Amazon, with its stock up 4% for the month.

This may be due to the company closely monitoring the productivity of employees returning to the office, as increased productivity can lead to higher profits.

The decrease in tech stocks coincides with the 10-year Treasury yield rising from approximately 3.95% in late July to above 4.1% currently.

Some signals suggest that yields may still go up and Fed futures reflect this with around a 35% chance the Fed will hike another .25% to 5.50%.

We could find us swiveling from the soft landing is complete to a “higher (yields) for longer” pivot which is effectively negative for short-term positive price action in tech stocks.

It’s entirely plausible that yields could retest the highs from 2022, based on the chart and recent trends.

This could spell bad news for tech investors, as tech stocks typically do not perform well in an environment of elevated yields. Higher borrowing costs, more attractive returns on cash, and increased scrutiny of future growth are among the challenges that tech companies face when interest rates rise.

However, the tech story is still intact albeit it a substantial amount more fragile than in early 2023.

The pain trade will be higher, but the fragility exposes itself to quicker external risks than before that could topple the market swiftly.

The United States has nobody but themselves to blame after issuing a mountain of debt and it’s largely true that when China sneezes, the world catches a cold.

Tech shares will be confronted with these two rising risks for the foreseeable future.

Best case scenario will see tech grinding higher into year-end, and don’t expect any gaps up. The low-hanging fruit has already been plucked from the vine this year.

“What all of us have to do is to make sure we are using AI in a way that is for the benefit of humanity, not to the detriment of humanity.” – Said CEO of Apple Tim Cook

Mad Hedge Technology Letter

August 11, 2023

Fiat Lux

Featured Trade:

(SHORT-TERM STUMBLES)

(AAPL), (NVDA)

When Apple and Nvidia go, so does the Nasdaq.

That’s why tech shares have been relatively impotent the past few weeks as Apple, again, revealed they don’t have much more than the iPhone.

This has spooked tech shares.

Combine the lack of innovation from Apple with the scares of Nvidia not being able to sell their chips in China as Washington clamps down on China’s ability to procure semiconductor products, and there you have it.

Growth fears from the biggest and best tech companies mean that as a sector, the Nasdaq shares pull back and investors are feeling the pain.

Apple is experiencing a slowdown in the smartphone market, but will the presumed iPhone 15 release in September change that for Apple?

NVDA shares surged by over 200% year-to-date in 2023 and replicating that for the back half of the year is almost impossible.

A continued drop in Apple’s overall revenue suggests that investors demand Apple to pull another cat out of the hat and at some point find something new.

A bout of inertia from management could force investors to look elsewhere with their capital allocation strategy.

Services did have a good quarter, but moving forward, what is their grand plan?

What does that mean then for this quarter as well as the next quarter, when we get the presumed iPhone 15?

It's something that Apple is going to have to answer once those phones are revealed in September.

They're going to have to have stellar features and not just the same groundhog day with a different color lock screen.

New cameras, new processor, basically looks the same. So can Apple really push the envelope enough to get people back into stores, back online, and picking up their products?

Take what I just said about the iPhone and apply it to the iPad and the Mac businesses too.

It is an industry-wide trend where people bought their PCs or laptops during the government-mandated lockdowns.

Now they just don't need another new one. And so we're seeing that from manufacturers to chip makers as well.

Beyond Apple, what about Nvidia?

There was a massive run-up on NVDA shares throughout the year. And now the question is, can they keep it rolling?

NVIDIA is a unique company when it comes to the AI space. They produce chips that nobody else can. They've perfected this over decades. They made the bet several years ago, and now it's really paying off for them.

Also, what happens when companies, this kind of hyperscaler companies, go out and begin putting their own chips into their own servers?

We know that Microsoft is working on it, Google is working on it, Amazon's working on it; Tesla has their own supercomputer that they're building with their own chips.

They already use NVIDIA as well and Elon Musk had said, look, we'll order as many as we can.

I don’t believe that will bite Nvidia in the short term, but it’s definitely a long-term risk.

As long as Nvidia produces the quality required to stay ahead of the competition, the stock market will pick back up after it has time to digest the rally in the first half of the year.

Ultimately, these are great companies, but faster than we know it, solutions are demanded for structural problems.

“When something is important enough, you do it even if the odds aren't in your favor.” – Said Tesla CEO Elon Musk

Mad Hedge Technology Letter

August 9, 2023

Fiat Lux

Featured Trade:

(YOU’LL BE DRIVING CHINESE SOON)

(BYD), (TSLA), (GM), (LCID), (SAIC), (GEELY), (CATL)

You’ll most likely be driving a Chinese car soon.

It’s not because I want you to.

The trend is headed that way and the trend is usually your friend in economics and the stock market.

In the past year, China has blazed past Germany and Japan to become the world’s biggest exporter of cars for better or worse.

They shipped 1.07 million abroad in the first quarter of 2023.

At the same time, net zero rules are set to outlaw the sale of conventional petrol cars from 2030 in the UK and 2035 across the rest of Europe.

This is a golden opportunity for entrenched Chinese brands including SAIC, BYD, and Geely.

With rivals such as Volkswagen, Ford and Toyota scrambling to catch up, Chinese manufacturers are poised to offer cars costing as much as €10,000 (£8,600) less than their European, Japanese, and American competitors.

Beijing has sought to dominate the electric vehicles global market as part of its Made in China 2025 strategy.

More than half of the electric cars on roads worldwide are now in China, according to the International Energy Agency, while in 2022 the country accounted for around 60pc of all BEVs sold.

They have been focused on having an industrial upgrade in China, moving from lower value-added production to higher value-added, higher-technological production.

The strategy has worked like clockwork as Chinese-produced cell phones have achieved flagship levels.

Contemporary Amperex Technology Limited (CATL), based in the city of Ningde in the Fujian province, is now the world’s biggest lithium battery manufacturer.

In 2023, the country is set to export 1.3 million BEVs, up from 679,000 last year when government lockdowns were still in force.

Not only are these vehicles tick the box of high quality, they also boast long ranges, attractive designs, and smart interiors, they are also extremely cheap.

One brand British motorists should expect to see more of is BYD, which recently unveiled an electric hatchback that it plans to sell for less than £8,000 – far cheaper than many petrol-fueled models.

The approach contrasts sharply with that of America, where Joe Biden is showering firms that set up BEV factories with subsidies and hitting Chinese car imports with tariffs of 27.5%.

Ominously, however, China’s lead in EV technology is now so great that it “cannot be bridged” by 2030 – when Britain and Europe will impose restrictions on the sale of new petrol cars – and Europe should cut its losses by encouraging Chinese car makers to set up factories here instead.

For US EV makers like Tesla, the protectionist restrictions placed on foreign EVs will mean that it will take longer for the Chinese EVs to penetrate the US vehicle market.

However, the tsunami of deflation is coming whether the Chinese need to add an intermediary or not before they can start pouring the products into the United States.

If China is able to breach the US market, this would pose a severe test for US EV makers like GM, Tesla, Ford, and Lucid.

The Europeans are asleep at the wheel and could expose their consumers to a bevy of Chinese cars.

Don’t be shocked to see a stream of Chinese EVs when you cruise around Rome instead of Fiats and Vespas.

I expect restrictions to ramp up even more against foreign-made EVs and lithium batteries in the short term.

This could also set the stage for Tesla getting kicked out of Shanghai and a massive forced technology transfer which the Chinese are famous for.

The Chinese are playing the long game and that’s highly negative for American EV makers who are hell-bent on short-term profits.

Mad Hedge Technology Letter

August 7, 2023

Fiat Lux

Featured Trade:

(WHAT THE DOWNGRADE MEANS FOR TECH)

(AA+)

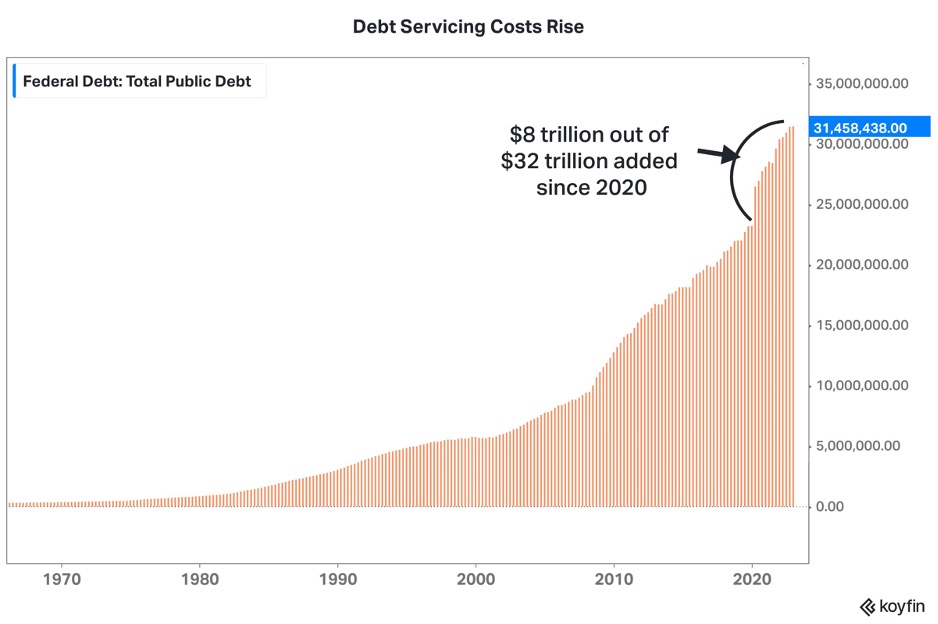

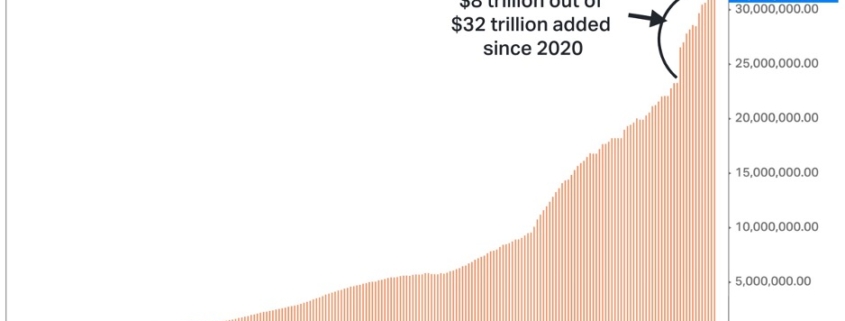

Fitch Ratings’ decision to strip the US of its AAA credit ranking to AA+ sets the stage for inflation to come roaring back, and tech stocks to underperform in the short term.

Why?

The downgrade risks bond yields blowing out, which in turn will potentially cause the U.S.’s interest payments on the debt to shift substantially higher.

That is exactly what investors don’t want to hear, in particular concerning technology stocks.

Tech stocks, along with U.S. housing prices, are most susceptible and sensitive to interest rate shocks and this could be a doozy.

The smaller the tech company is, the more reliant they are on initial debt funding to develop the company.

Big tech will be more insulated from this chaos because they are the equivalent of the reams of home buyers that purchased homes at a sub-3% interest rate that is fixed for 30 years.

As long as revenue is growing okay-ish, big tech will be fine, and the latest earnings reports have proved that with big tech’s unimpressive single-digit growth.

It’s nothing special but good enough for the times.

The booming federal deficits are the heart of the bear case for Treasuries and, even more poignant, the massive federal mismanagement of the country, no matter which political party has been in charge.

Take for instance, over 20 years and 3 presidents, a certain country would spend over $10 trillion in Afghanistan and the result is replacing the Taliban with the Taliban.

Many would say that wad of federal money probably wasn’t worth the paltry result.

Now, what we finally have is a real-life example of the consequences of government underperformance.

The U.S. economy is the most vibrant, productive, and profitable economy in the world.

Free market capitalism has catapulted the U.S. to build the largest and most successful tech industry in the world that is the envy of the rich world.

Now, exploding bond yields move to the fore as the largest risk for technology stocks.

The downgrade also means that Fed Chair Jerome Powell and the Central Bank will have a harder time pivoting when they want to because yields could spike and could have another dose of inflation to fight against.

The downgrade could invite a horde of algo traders and hedge fund pros to pile into the short-bond trade because where there is smoke, there is fire.

In the short term, don’t expect the 30-year US treasury yield to hit 10% which was the case in 1987.

However, a turn for the ugly and yields surpassing last year’s 4.35% is just in sign after this last melt up.

The stage could be set for the 30-year to reset at higher increments between 5%-6% with no relief in sight.

This sort of level is highly prohibitive to tech stocks in the short term, therefore, I would believe a repricing would need to take place to balance itself out.

In all honestly, tech needs a break and this appears as if it is the trigger to cool down tech stocks which have been on a pulsating trend to the upside in 2023.

Ultimately, I would describe the downgrade as inevitable. The rising (and accelerating) deficit begs the question of fiscal amateurism.

Congress has been behaving as if unlimited dollar binge spending has no consequence.

Furthermore, we can kiss smaller tech companies tapping the debt market goodbye.

Conditions keep tightening in tech and it’s becoming harder to thread the needle for the unknown quantity.

I would stick with investments in known quantities with strong balance sheets, as they will perform better in a spiking bond yield scenario.

Reload the ammo to buy the dip on those guys.

U.S. Congress is now on call to reign in the massive fiscal deficits or face yet another downgrade and even higher interest payments on federal bonds.

That would be materially negative for tech stocks in the medium term.