"The greatest enemy of knowledge is not ignorance, it is the illusion of knowledge," said the late Professor Stephen Hawking.

"The greatest enemy of knowledge is not ignorance, it is the illusion of knowledge," said the late Professor Stephen Hawking.

Mad Hedge Technology Letter

May 8, 2023

Fiat Lux

Featured Trade:

(DON’T LET THESE 3 GET AWAY)

(SNOW), (WDAY), (NOW)

Even though the tech market isn’t in a renaissance, that doesn’t mean there aren’t any good choices to park capital.

I’d like to bring readers' attention to 3 cloud stocks that still have some upside.

It’s true that tech stocks no longer go up in a straight line, that auto-pilot mindset blew up spectacularly in 2022 when tech stocks finally stopped defying gravity.

The 16% the Nasdaq has gained this year is somewhat due to the expectations of a rebound and better-than-expected earnings.

With that in mind, software still has legs and it would be a shame to not go where the value is in tech.

After the big 7 behemoths, there are some tech plays that readers need to target because workloads will migrate to the cloud over the next decade.

There has been a significant shift to the cloud in recent years from legacy on-premise workloads and infrastructure. Cloud computing allows organizations to rent rather than buy IT and other functions.

Given the cost savings, scalability, flexibility, productivity gains, and improved security features, it’s obvious why this shift is happening.

These advantages mean more workloads will continue moving to the cloud. SaaS growth stocks are expanding despite the current macro uncertainty.

IT service management giant ServiceNow (NOW) is one to slide into your black leather wallet.

The company is a leader in the cloud-based IT service management and digital workflow solutions sphere. Its software helps businesses streamline operations, automate workflows and improve customer experience.

NOW recently grew revenues by 24% year-over-year last quarter.

It reported a healthy 35% free cash flow margin, which ranks in the top quartile among SaaS growth stocks.

Another one to keep an eye on is Snowflake (SNOW).

Data migration to the cloud is a secular trend that will support growth for years. Snowflake is a cloud-based data warehousing, processing, and analytics company.

Their data platform provides businesses with a scalable and flexible service for managing their data. It enables organizations to store, analyze and share large amounts of data in real-time, helping them to make better decisions and improve their operations.

Over the last five years, it has reported a net revenue retention rate above 150%.

Its platform capabilities are critical for any enterprise, and it has been winning customers in various industries.

On March 1, they reported quarterly revenues of $589 million, a 53% year-over-year growth rate.

Just as impressive, the company announced a plan to return cash to shareholders through a $2 billion buyback.

Lastly, Workday (WDAY) is a cloud-based software company that provides businesses with human capital management, financial management, and analytics solutions.

The company’s cloud software helps businesses improve workforce management, financial management, and decision-making processes.

It counts many Fortune 500 companies as customers. The company hit the 10,000 customers milestone lately with revenue increasing 19.6% year-over-year.

The runway is long for WDAY with a total addressable market for this subsector at $73 billion, respectively. Considering that organizations will continue to modernize HR and finance operations, Workday is one of the top SaaS stocks to buy to play this trend.

Mad Hedge Technology Letter

May 5, 2023

Fiat Lux

Featured Trade:

(HIGHER FOR LONGER)

(AAPL), (JOBS)

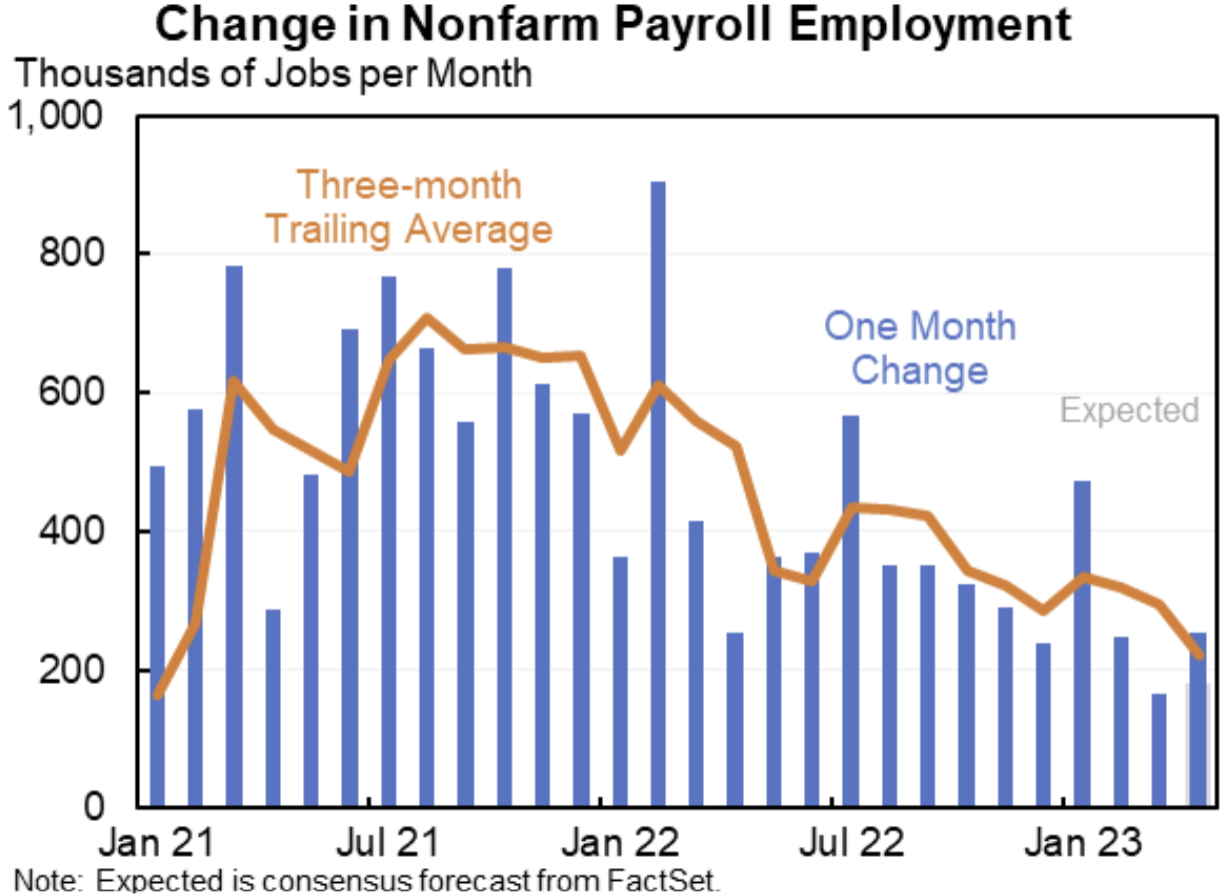

Non-farm payroll matters.

The job numbers have serious consequences for the tech sector - the biggest being there will be no recession in 2023 because everybody has a job.

Not only does everyone have jobs, they are also getting double the wage gains the Fed forecasted at 0.5% annualized to 6% year over year.

The tech sector has gotten rid of many good-paying jobs, many of those jobs were fake jobs that were absorbed to hoard talent when rates were at 0%.

It’s interesting that many of these tech stocks have exploded to the upside upon announcing job cuts, meaning investors don’t view the cuts through the prism of lost revenue but rather increasing productivity and delivering added efficiency.

Now, the entire bond investing complex is waiting on a Fed cut, which is why as of yesterday, 4 quarter percent rate cuts were priced in.

Fast forward 1 day and Fed future pricing is now pricing in 3-quarter percent rate cuts as investors believe we will stay higher for longer.

Higher for longer is bad for tech shares.

This extinguishes any hope of reducing inflation in the medium term.

It could be that we only get 1-2 quarter-point rate cuts in 2023 if the bond market is correct.

The Nasdaq has performed exquisitely in 2023 gaining 15% so far amid a souring backdrop of shrinking margins, increasing interest rates, federal government mismanagement on an epic level, domestic banking contagion from regional banks, and geopolitical strife.

The not so bad – not so good situation in tech stocks has manifested itself in the best tech stock Apple, which reported earnings yesterday.

Apple’s earnings report validated what I am seeing in the data.

The report was nothing special but good enough to believe that tech will narrowly avoid a recession in 2023.

The balance sheet is so ironclad that Apple even initiated a stock buyback of $90 billion.

Not too shabby.

Granted, there are few that can wield a strong balance sheet in the ways CEO Tim Cook can, but that’s not taking anything away from him.

Apple also told us about the 975 million paying subscribers to their services and that’s 150 million more than one year ago.

The takeaway is that Apple has a highly loyal customer base that continues to drive its dollars into the ecosystem.

Customer retention is incredibly high because they deliver products customers want.

Even their flagship product the iPhone and its revenue was up 2% year over year and beat forecast by $2.5 billion coming in at $51.33 billion when overall revenue decreased year over year.

iPhone revenue is just over half of Apple’s revenue.

A recession data point would be one in which to expect negative growth from iPhone revenue, so low single digits are fine.

The bottom line is that the US economy added 253,000 jobs to the overall job market and the unemployment rate is defying gravity.

US consumers keep spending, spending, and spending more.

Tech has turned into a 7 stock market and generous shareholder returns.

I admit that 2% iPhone revenue growth isn’t eye-popping, but that is where we are at this point in a late economic cycle.

Squeeze the juice out of the iPhone before the next big pivot to the next technology.

Similar can be said about the job market, everyone is trying to make their last buck before this whole thing gets a reset with 0% Fed fund interest rates.

Many even wish that 0% rates were already here.

Tech stocks will grind up as investors will bid up tech stocks, because they believe the Fed will cut sooner than initially thought. We’ll go back to that narrative for better or worse.

Mad Hedge Technology Letter

May 3, 2023

Fiat Lux

Featured Trade:

(ALGORITHMS TAKE OUT ED TECH)

(CHGG), (ZM), (NFT), (CHATGPT)

Chegg (CHGG) is toast.

That is what artificial intelligence has done to their business model and we are in the early innings.

The company said to kiss growth goodbye.

Artificial intelligence is already putting a massive dent in some industries.

Education has changed dramatically in the past generation where more than half of Americans say a 4-year degree is not worth the price of admission anymore.

Now, moving forward, the little value extracted in terms of workable knowledge in the classroom is effectively zilch as generative artificial intelligence will do the job of a million university teachers for free.

There simply is no use case for taking geography studies or getting a basket weaving degree from Wesleyan College.

It doesn’t make sense anymore.

The scary thing is this is just the beginning and other industries are about to get t-boned as well.

Only the nimblest will survive.

Workers need to retrain, network, and preserve and expand skill levels.

Shares of virtual language-learning company Duolingo fell 9% while American depositary receipts tied to shares of London-based Pearson fell 12.5%.

Chegg offers subscription-based academic services that help students with writing and math assignments as well as study materials.

Management said the company didn’t see a significant effect on its business from ChatGPT until March, when the company behind the product, OpenAI, launched GPT-4.

Chegg said the popularity of ChatGPT among students is affecting its customer-growth rate.

The red alarm from Chegg and the subsequent selloff are among the most glaring indications that this isn’t some cute niche thing that can be downplayed or diminished.

AI is coming for most white-collar jobs and workers should be scared if not mortified.

Many of the job losses will occur in big corporations and America has some of the biggest and most profitable.

The tailwind for corporate management is that they don’t need to pay benefits or social payments to AI so big cost savings that will fall down to the bottom line.

Wall Street will be applying this technology to the utmost too.

To say this technology is transformative doesn’t do justice to the word transformative.

This isn’t going to be an all tides lift all boats scenario.

Bloomberg news noted that nearly 40% said that children currently in elementary school will be best off with a job in health care if they want to avoid being displaced by artificial intelligence.

What about tech?

There will be serious winners and losers as this shakes out. It’ll be like a slow-motion car crash for workers while tech firms profit in real-time.

Technology stocks will hollow out similar to how we see the behemoths pull ahead lately muscling out smaller companies with their solid balance sheets.

This has essentially become a 7-stock tech sector.

Tech companies will absolutely be chomping at the bit to fire computer engineers whom many command in excess of $150,000 in pre-tax gross salary.

Of course, the lower-level computer engineers will be thrown by the wayside first then slowly the terminations will reach higher up the value chain.

If a computer engineer wants to survive in the future, they will need to dive into generative artificial intelligence themselves which will easily offer the highest salaries in technology.

AI is now the new bitcoin and the best talent will flood that space. It’s easy to see how starting salaries with start with a 3 and end with 5 more numbers.

As for tech investors, this shows that getting into these little micro tech stocks is more and more treacherous as the landscape has dictated a hard future ahead.

That is why I tripled up on a bearish position in Zoom technologies (ZM). All big tech companies have some sort of version of video conferencing tech and it is easy to replicate. Stay with the strongest during this bank crisis.

Mad Hedge Technology Letter

May 1, 2023

Fiat Lux

Featured Trade:

(GRINDING HIGHER)

(META)

It’s clear that the cost of gaining each incremental load of revenue is a lot harder than it used to be for Meta (META) platforms.

This is why expenses have exploded out of control, but I wouldn’t say that it’s time to take profits because they benefit from the “too big to fail” mantra just like other systemically important stocks.

I don’t believe they will rekindle sales growth of yore because there isn’t anything on the horizon that strikes me as something that would be a game changer.

The metaverse which they are sinking a fortune into has turned into a black hole of capital.

CEO Mark Zuckerberg himself couldn’t explain on the conference call when there would be tangible results that would deliver help to the bottom line.

That means open-ended funding to R&D and that is not what you want to hear from shareholders.

The pay-as-you-go elements to this don’t bode well, because they still don’t understand how they can monetize AI.

The silver lining here is that Meta is still quite profitable.

The top line of $28.6 billion was up 3% year over year.

It was the first year-over-year revenue growth Meta has been able to muster since the first quarter of last year. Per-share earnings of $2.20 also topped the consensus of $2.02.

Sales guidance for the quarter currently underway was also better than expected, with the company forecasting a top line of somewhere between $29.5 billion and $32 billion.

Q1's net income of $5.7 billion is 24% less than the bottom line from the first quarter of 2022 showing that even though they make a lot of money, profitability is slowing.

While Meta did sequentially add 60 million daily users to its services last quarter, most of that growth came from the Asia-Pacific market or the "rest of the world" - not Europe, Canada, or the U.S.

Those two markets experience the lowest ARPU (average revenue per user) figures among all the ones Meta serves.

And in both of those cases, ARPU figures have been essentially stagnant since the second quarter of last year.

It’s increasingly worrisome that the growth part of META is low quality.

Zuckerberg knows that it’s a fight to the bottom with his existing business which is why he is hell-bent on making the metaverse work.

Don’t forget that META shares fell from $360 per share last year and many investors can describe the recent price action as a reversion to the mean.

Expect higher costs to eat into META’s bottom line, but not so damaging that it will kill the business model.

The gains are there to be had, but don’t expect any high growth to come from META – those days are essentially over.

META will most likely grind higher and I do believe investors should buy the dip when available.

When the trend isn’t broken, then don’t fight against it.

Don’t forget they will benefit from another tailwind of end of 2023 rate cuts.

Tech business models aren’t as good as they used to be, but that doesn’t mean these stocks won’t go up.

A tepid META receiving investor love also shows how bad things are at the bottom of the barrel from SPACS to lockdown darlings.

Small growth stocks have little to no chance to compete moving forward so investors should only focus on “too big to fail” tech stocks in a world of higher rates.

Mad Hedge Technology Letter

April 28, 2023

Fiat Lux

Featured Trade:

(BUY AMAZON ON THE DIP)

(AMZN), (AAPL)