The Big Winner from Intel's Chip Design Flaw

Buy Intel (INTC) on the dip. That is the only conclusion you can reach after watching the company go through the meat grinder after revelations of its chip design flaws were made public.

After following this company for four decades, that is always the correct kneejerk reaction. Certain industries suffer from inherent idiosyncratic risks unique to them, and this is one of them.

Some 25 years ago, I had dinner with the late Intel CEO Andy Grove (we shared the same doctor), and I asked what was his biggest fear. He answered that the company would spend $1 billion on a new fab, then flipped the switch on opening day, and nothing happed.

Intel has a disaster something like that on its hands today.

Samsung knows this lesson too well from 2016, the makers of the Galaxy S7 smartphone, which took a huge blow when their batteries continually burst into flames in 2016. Apparently, their testers didn't find this flaw until after delivering the first large batch of new phones.

The news went viral and Samsung had a PR disaster of mega proportions, a battery design catastrophe, and quality control crisis on their hands all at the same time. You may recall that every airport had signs at the boarding gate reminding passengers to leave behind their flaming Samsung phones.

In the fickle market of premium smartphones, Samsung was taken out to the woodshed and severely beaten by the Chinese consumer, and their market share in the biggest smart phone market dropped from a robust 18.7% in 2013 to pitiful 2.2% in Q4 2017.

They have never recovered.

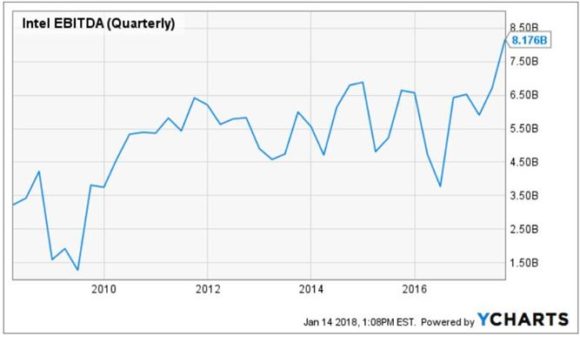

Intel's (INTC) disclosure of the design flaw exposed in their CPU was a terrible start to 2018.

Predictably, Intel shares were hammered.

Hardware companies cannot afford sacrificing whole product cycles. The wasted R&D and the brand damage is lamentable and it will take time to recover, not to mention the multibillion dollar cost.

You can bet that a comprehensive review has been set in motion for the designs in all lucrative hardware products at all companies. Expect a gradual trickle of bad news to come out from other players too.

Intel noted the problem was known for "a few months" but did not fix it immediately. This is awful. Brian Krzanich, CEO of Intel, also suspiciously sold a good chunk of Intel stock during this period. He is already in the SEC's sites.

Hiding architectural problems for months does not exactly breed shareholder trust.

Intel replied, "There have been no examples of the flaw being exploited by hackers". Unawareness does not exactly equate to safety. It's highly possible the future trickle of bad headlines will detail the criminal element that took advantage of this gaping hole.

Will the tech naivety continue unabashed? Will the contagion be worse next time?

Hardware reliability is truly something consumers and companies must ponder about.

Companies have more room to maneuver in the future when negotiating CPU contracts with Intel because of this debacle. That will hurt profit margins.

Technically, the patches will slow certain processors by up to 30% according to Intel officials.

The Intel CPU flaw brings up deeper questions. Is it safe to store important data on the cloud? Can hackers steal entire sets of cloud data and resell it to the highest bidder?

Another option is returning to the good old days when data was kept on external hard drive storage away from the tentacles of professional hackers. By the way, that's what we do here at Mad Hedge Fund Trader, who have never trusted the cloud.

The vast amount of data in 2018 makes this strategy highly inefficient for the biggest firms.

If storage risks flare up, the industry shifts closer to an inflection point and alternative measures will float around about how and where to store data.

Running apps on any platform requires more processing power each passing day as we expand the functionality and integration of smartphone and computing apps into our daily lives.

This higher opportunity cost of operating a slower CPU will be passed onto the user, much to their chagrin, but the problem will subside as the design architecture in new CPU's will be absent design defects.

Companies will also increase overhead. Additional quality control and design specialists to ensure that components produce products as advertised will be added to payroll. This will add higher costs, more stringent development guidelines, further pressuring margins.

The tech industry was the darling of Wall Street for many years and still is in most quarters. But some cracks are starting to form around its core foundations and ethos.

Fortunately, Wall Street still favors the tech sector and the accelerated earnings growth narrative remains intact albeit with a small chink in their armor.

The net net is tech companies will take on more operational risk.

Vulnerability will be a key theme in 2018 and entwined in this game of cat and mouse are cybersecurity firms and rogue hackers.

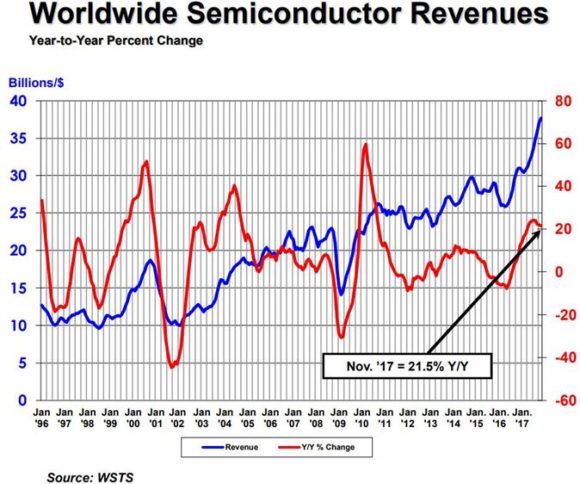

As the total global revenue for semiconductors revs up towards $80 billion, there will be multiple winners as the pie expands. Intel shares look stupidly cheap at 13x forward PE and looks substantially cheaper than AMD which trades at an insane 33x forward PE.

Comparably, the best of breed in this space is NVIDIA (NVDA) which trades at 50x forward earnings and the high multiple is justified as earnings consistently surprises to the upside.

That acrophobic multiple is well deserved, as NVIDIA represents the vanguard of several monster trends in the semiconductor industry and lead in the autonomous driving and AI spaces.

Ultimately, sales of chips could migrate up the industry chain; a natural flight to quality. Intel's slip up highlights Nvidia's top notch quality and the countdown starts again for the next batch of compromised hardware. The losers are the chip companies that are perceived as smaller, lower quality and their sell-offs are dramatic when related names roll over.

As with every other major industry trend, all signs still point to NVIDIA. But I wouldn't mind picking up some (INTC) on this dip either as the CPU market is a duopoly between AMD (AMD) and Intel (INTC).

These days, all problems for equity investors seem to be temporary.