The Weight Of Expectations

You know that feeling when you've found the perfect restaurant? The food is exquisite, the atmosphere divine, and then you get the bill—and suddenly you're calculating if selling a kidney is a viable financial strategy.

That's essentially my relationship with Eli Lilly (LLY) right now. Phenomenal company, stellar performance, price tag that makes my wallet weep.

I've had a complicated romance with this pharmaceutical juggernaut. Back in my hedge fund days, I learned that timing is everything with pharma stocks. It's like catching the perfect wave off Malibu – ride it too early, you're just splashing in the shallows; too late, and you're eating sand.

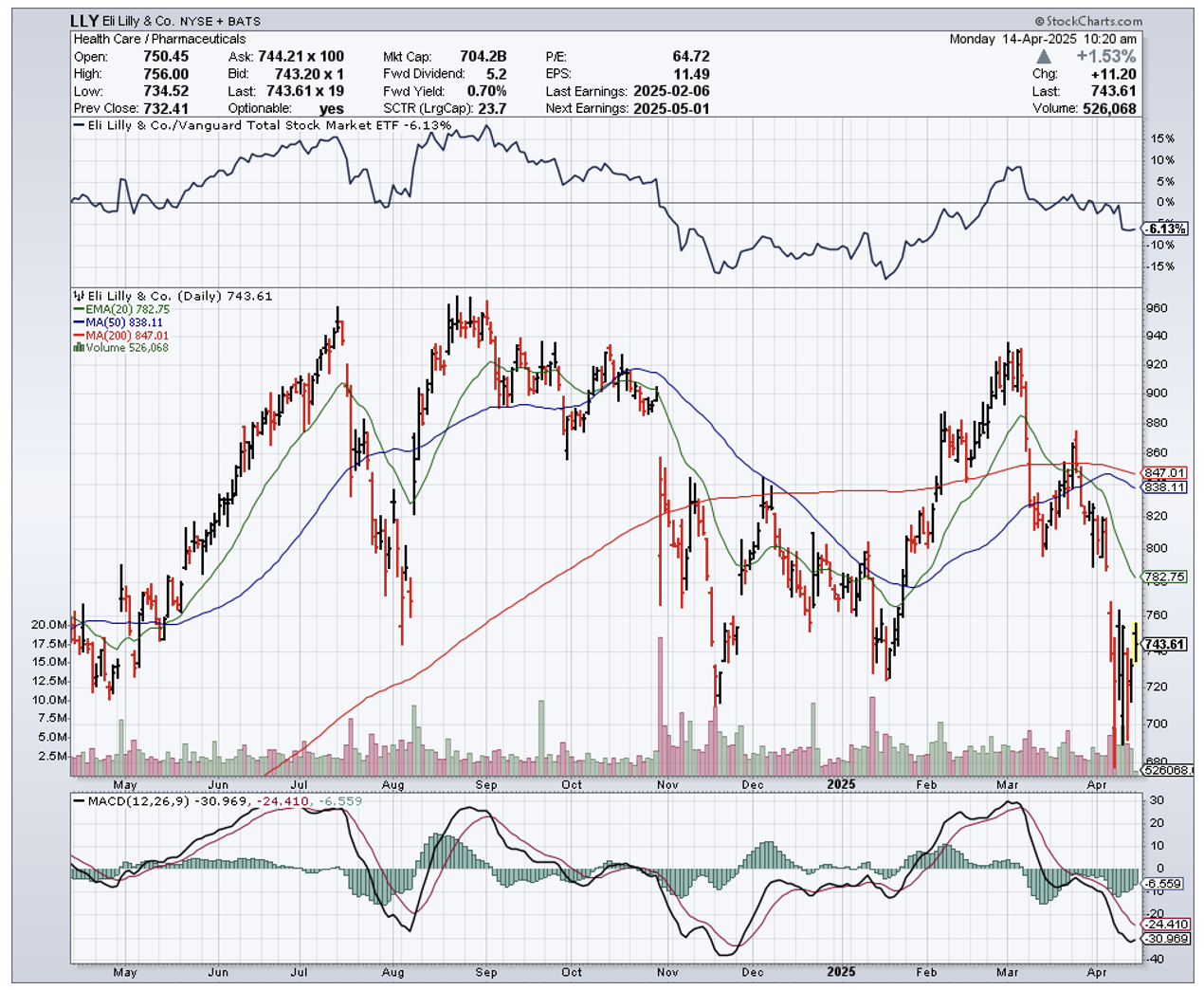

When I first spotted Lilly in June 2023, it was set up beautifully. Shares rocketed 56.2% before I downgraded to a 'hold' last February, while the broader market trudged along with a mere 12.3% gain.

Since then, the stock has performed almost exactly as predicted—just a 0.2% gain compared to the S&P 500's 1.33%. More recently, it's dropped 6.9% since January, looking positively rosy next to the broader market's 12.2% decline.

The company's fourth-quarter results read like a biotech investor's fantasy novel. Revenue soared 44.7% year-over-year to $13.53 billion, driven by its dynamic weight-loss duo.

Mounjaro's sales jumped 60.1% to $3.53 billion, while Zepbound exploded from $175.8 million to a jaw-dropping $1.91 billion.

I've watched patients in clinical trials shed substantial weight on these medications—one of my research contacts dropped 43.4 pounds since starting treatment—and I can tell you these drugs are creating waves not just in waistlines but across the entire healthcare sector.

Other stars in Lilly's portfolio include Verzenio for breast cancer (up to $1.56 billion from $1.15 billion), Jardiance for diabetes (climbing to $1.20 billion), and solid gains from Taltz and Humalog.

Only Trulicity disappointed, watching its revenue tumble from $1.67 billion to $1.25 billion—predictably cannibalized by Lilly's newer weight-loss offerings. It's like watching your reliable sedan gathering dust after buying a Tesla.

With this revenue bonanza, profits naturally skyrocketed. Net income more than doubled to $4.41 billion, adjusted profits surged to $4.81 billion, and operating cash flow swung from negative $311.9 million to positive $2.47 billion.

In my decades of following pharmaceutical stocks from Tokyo to Wall Street, I've rarely seen a quarterly performance this impressive. If Lilly were a student, it would be the annoying one breaking the curve for everyone else.

Looking ahead, management projects 2025 revenue between $58-61 billion (a 32.1% increase at midpoint) and adjusted EPS between $22.50-24.

For the upcoming Q1 report on May 1st, analysts anticipate revenue of $12.77 billion (45.6% higher year-over-year) and EPS of $4.70 (nearly double last year's $2.48).

So with all this financial wizardry, why maintain a 'hold'? One word: valuation.

Even using 2025's projected figures, Lilly trades at eye-watering multiples: forward P/E of 33.3, price-to-cash-flow of 27.6, and EV/EBITDA of 21.2.

For context, pharmaceutical peers trade significantly lower. Novo Nordisk (NVO), perhaps the most comparable given its similar weight-loss market success, trades at a P/E of 19.0, price-to-cash-flow of 15.9, and EV/EBITDA of 14.6.

It's like comparing Manhattan real estate to Cleveland—both might be perfectly fine places to live, but one demands a significant premium.

Don't mistake my caution for bearishness. Lilly's product pipeline is robust, highlighted by Retatrutide, which has shown even more impressive weight-loss results—patients lost an average of 24.2% of their body weight (58 pounds) in clinical trials.

The company is also expanding its manufacturing footprint with four new US sites, creating 3,000 permanent jobs. It's acquiring promising treatments like Scorpion Therapeutics' STX-478 for $2.5 billion upfront.

Meanwhile, shareholders enjoyed $4.7 billion in dividends and $2.5 billion in buybacks last year, with a new $15 billion repurchase program and a 15% dividend increase announced for 2025.

I'd compare Lilly's stock to its own weight-loss drugs: remarkably effective, potentially life-changing, but priced at a level that makes you question whether the benefits justify the cost.

If May's results blast past expectations with raised guidance, I'll happily reconsider. Until then, I'm maintaining my 'hold'—admiring from across the room, but not ready to propose just yet.