Your All-Weather Healthcare Fortress

I've stared down bears in Yellowstone, MiGs over Moscow, and market crashes that would make your financial advisor need therapy. But nothing gets my pulse racing like finding a massively mispriced asset hiding in plain sight.

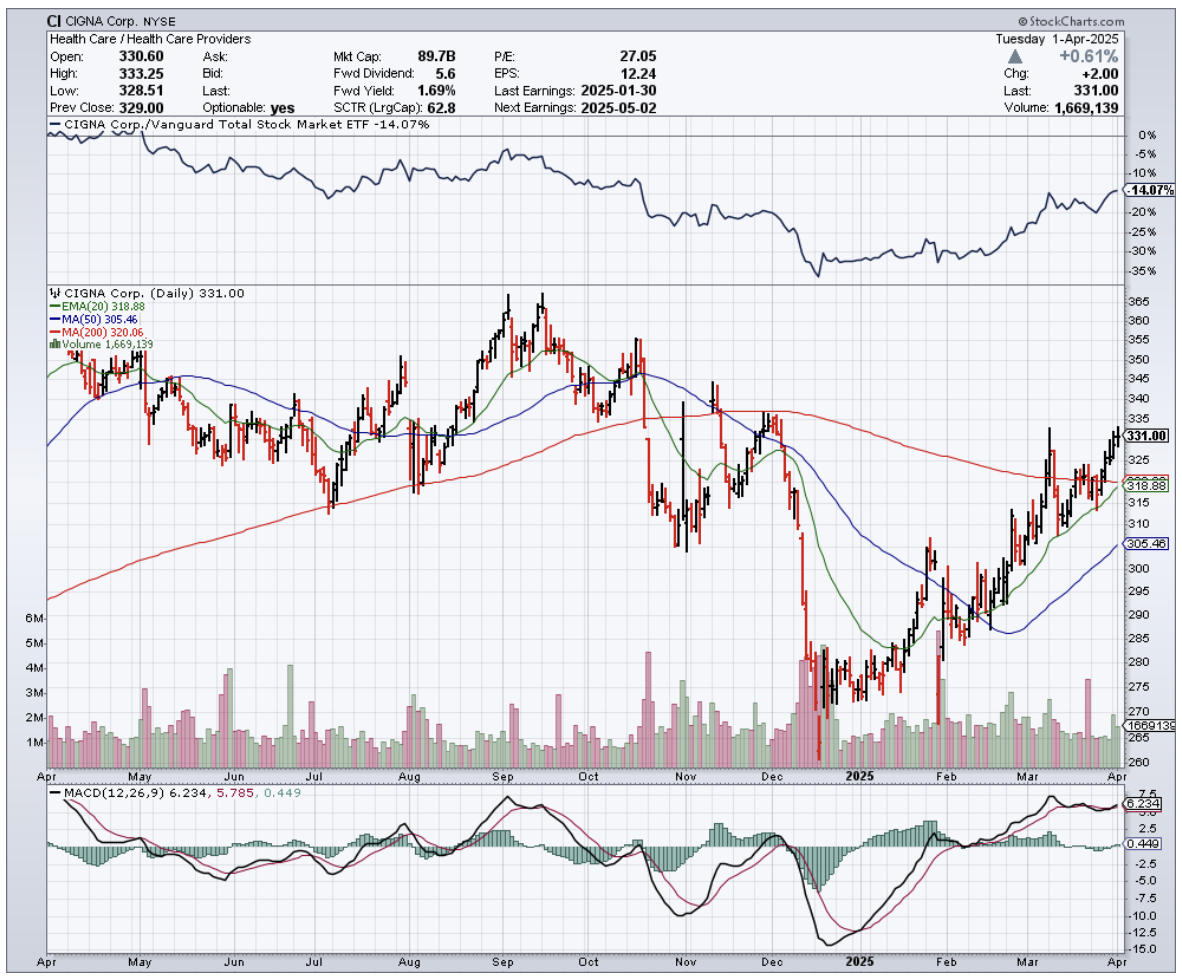

Ladies and gentlemen, I give you Cigna (CI) – the financial equivalent of discovering an abandoned Ferrari with the keys still in the ignition.

Two nights ago, at a private dinner with three healthcare CEOs, I heard something that confirmed what my models have been screaming for months: Cigna isn't just surviving healthcare's perfect storm – it's secretly thriving in it.

At $331 per share, we're looking at a rare beast: a value play with growth-stock upside.

I've spent enough time hanging around hospital C-suites to know when something smells like money.

Healthcare has been absolutely battered these past couple of years – staffing shortages, skyrocketing utilization rates, and the mother of all pandemic hangovers. Yet here's Cigna, delivering 8-9% year-over-year earnings growth.

What really gets my investment juices flowing is watching Cigna’s strategy play out beautifully. In fact, they just closed their Medicare business sale to HCSC in Q1, a move so smart it makes me want to applaud slowly from across the room.

I was having dinner with Medicare Advantage executives last month, and these folks were practically in tears over reimbursement rates. "It's like trying to run a restaurant where customers expect filet mignon but only want to pay for ground beef," one said, nursing his third scotch.

By reducing Medicare exposure, Cigna is saying, "We'd rather control our destiny than beg government bureaucrats for pennies." Companies that pivot away from heavily regulated, margin-compressed businesses typically emerge looking like they've been on a financial fitness program.

Here's the cherry on top – practically all proceeds from the Medicare divestiture are funding stock buybacks.

Cigna already has a track record of reducing share count that would make other CEOs jealous. One of my former students who now runs healthcare equity research at a bulge bracket bank messaged me privately that his team is dramatically underestimating the EPS impact – like forecasting a drizzle when there's a monsoon coming.

As both an insurer and pharmacy benefits manager, Cigna occupies rarefied air. Their ability to steer members toward lower-cost biosimilars isn't just smart business – it's practically printing money.

During my last Mad Hedge Fund Trader conference, I arranged a private tour of Cigna's specialty pharmacy operations for some of our Concierge members, and what I saw confirmed my thesis: their integration of medical and pharmacy data gives them insights that would make McKinsey consultants salivate.

And can we talk about prior authorization? If you've dealt with health insurance, you know it's bureaucratic torture that makes the DMV seem like a day spa. Remarkably, Cigna is reducing these requirements.

A Cigna EVP I've known since our Harvard Business School days told me over golf that their internal data shows customer retention improving by double digits from these changes alone.

Let's get down to the numbers. Like I said earlier, even during healthcare's darkest days, Cigna delivered 8-9% EPS growth. Using that as my bear case and applying a conservative 3% terminal growth rate, we're looking at a fair value of $432.79 per share.

But if they execute on their 10-14% EPS growth strategy, the fair value jumps to $508.40. That's 33-53% upside from current levels – the kind of return profile that usually comes with significantly more risk.

In 40 years of trading everything from Japanese derivatives during the Nikkei bubble to Texas fracking plays, I've learned that when everyone panics about an industry, the smart money quietly pounces on the gems.

Cigna isn't just any healthcare company – it's the one with enough foresight to shed Medicare exposure right before what my Washington contacts warn will be a reimbursement bloodbath.

Mark my words: By this time next year, when I'm recounting this trade over sake in Tokyo, Cigna won't be our little secret anymore – and neither will the 33%+ returns sitting on the table right now.

Well, that's enough financial wisdom for one day. My trading screens are flashing, my yacht captain's texting, and somewhere in the Himalayas, a summit is wondering where I've been.