February 1, 2011 - Thoughts on Egypt

(SPECIAL MIDDLE EAST ISSUE)

Featured Trades: (THOUGHTS ON EGYPT)

1) Thoughts on Egypt. When I first visited Egypt in 1977, they tried to kill me. I was accompanying US Secretary of State Henry Kissinger on an Air Force jet as part of his shuttle diplomacy between Tel Aviv and Cairo. Every Arab terrorist organization had vowed to shoot our plane down. When we hit the runway I looked out the window and saw a dozen armored cars and personnel carriers? chasing us just down the runway;? all on board suddenly got that gut churning feeling. When the plane stopped, they surrounded us, then turned around, pointing their guns outward. They were there to protect us. The sighs of relief were audible. In a lifetime of heart rending landings, this was certainly one of the most interesting ones. Those State Department people are such wimps! Henry was nonplussed, as usual.

When I traveled to Tel Aviv, El Al security made sure my luggage got lost. So the Israeli airline gave me $50 to buy clothes. On that budget, all I could afford were the surplus Israeli army fatigues at the Jerusalem flea market. A week later, my clothes still had not caught up with me when I boarded the plane with Henry. That meant walking the streets of Cairo in my Israeli army clothes. It would be an understatement to say that I attracted attention.

I was besieged with offers to buy my clothes. Egypt had lost four wars against Israel in the previous 30 years, and military souvenirs were definitely in short supply. By the time I left the country, I was stripped bare of all Israeli artifacts, down to my towels from the Tel Aviv Hilton, and boarded the British Airways flight to London wearing a cheap pair of Russian blue jeans. Levi Strauss never had a thing to worry about.

Virtually every research and intelligence organization seemed surprised at the sudden riots in Egypt that dinged the market on Friday. Every one, except this one, that is (click here for 'It's just a matter of time before the food riots resume'). For some time now, I have been warning that high food prices would lead to political instability in emerging markets. If you had to pick one place where this would happen first, it would be Egypt.

The bewitching North African country is a prisoner of a medieval religion that has left its people stranded in the Middle Ages. While its GDP has doubled in the last 60 years, so has its population, to 83 million, meaning there has been no improvement per capital income. Islamic fundamentalism can be traced back to the mid-19th century as an extreme reaction to British colonialism. Egypt responded by? inventing the concept of the sovereign debt default, which is how Britain ended up with the Suez Canal. Later, a young Winston Churchill cut his teeth as a journalist covering a major battle, the first where machine guns were successfully employed, and 10,000 of the faithful were mowed down. During the sixties, Gamel Abdel Nasser's efforts to form an Arab United States failed. As a journalist, I covered Kissinger's negotiations for peace with Nasser's successor, Anwar Sadat, who was? assassinated by his own bodyguard for his efforts shortly afterwards. Hosni Mubarek inherited the throne in 1981, and has been ruling the country with somewhat of an iron fist ever since.

I know that whenever the CIA kidnapped a suspected terrorist, but didn't want to deal with the legal consequences of bringing them home, they happily handed them over to Egypt, where the shadow of Amnesty International is unseen. Today, the advent of cell phones, cable TV, the Internet, Twitter, and even Facebook, enable revolutions to unfold at lightning speed. Cut these off, and everyone pours into the streets. The tourism industry, the big earner for this impoverished country, has been shattered and will take years to recover. The Egyptian stock market gave up $12 billion in stock market capitalization in two days, but who cares.

Events like this tend to have implications far beyond our initial understanding. In 1979, when the Shah of Iran fell to a movement led by an unknown radical mullah named Ayatollah Khomeini, we thought no big deal, it's a local problem. The Shah was no Boy Scout, and corruption in Iran was then endemic. Yet the fall out eventually led to our wars in Afghanistan and Iraq that has cost us trillions of dollars.

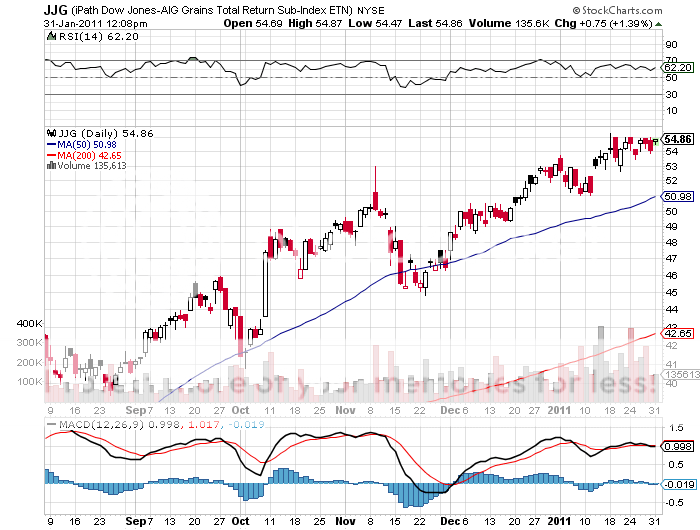

Of course, the final question has to be how all of this affects you and I and the financial markets. The positive impact on food prices has to be obvious. But as long as the world is in 'RISK OFF' mode, we aren't going to see dramatic moves in my favorite ETF in the area, the (JJG). The selloff in stocks was going to happen anyway, so don't pin the correction on the Middle East. Egypt was just the match to a market pyre that had been drenched with gasoline.

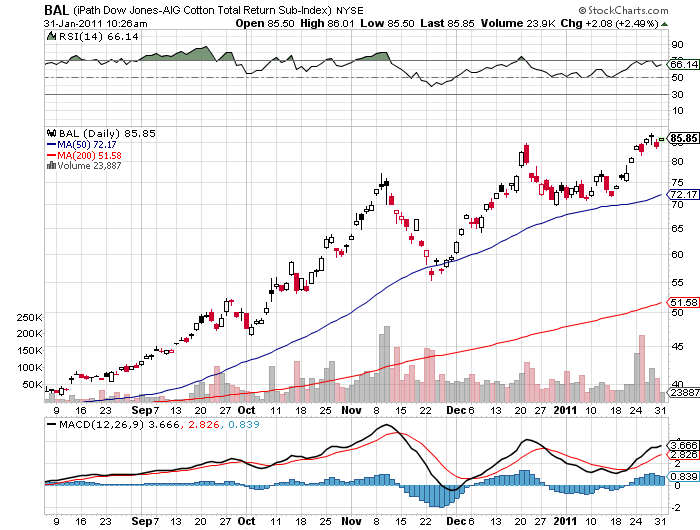

Today, Egypt is far and away the world's largest importer of wheat. It is also a major supplier of food to the rest of Africa, as it always has been. At first sight of the troubles, surrounding countries rushed to increase stockpiles to head off shortages, and are a major force driving prices higher. Egypt is also a leading supplier of cotton to the world market, and there is no other commodity less able to handle a supply cut off right now. Its price has already doubled in the past four months.

-

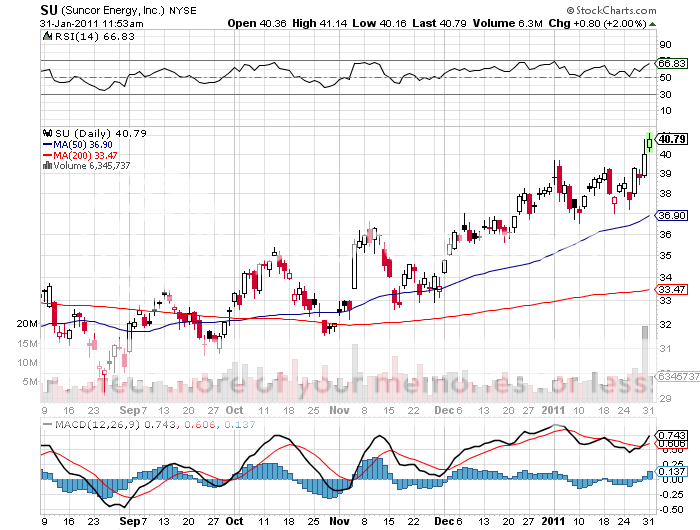

There has been much talk about the oil situation. While Egypt produces 600,000 barrels a day, that is a drop in the bucket in today's 84 million barrel/day global production. That is barely enough to meet domestic needs. A cut off of the Suez Canal would be problematic, but only for the short term. This explains why there has been a huge run up in Brent crude, to a record $9 a barrel premium over West Texas intermediate. But that is Europe's problem, not ours. All of America's crude from the Middle East comes around Cape Horn because the tankers are so large. If anything, this places a greater premium on Canadian tar sands producers like Suncor (SU), which are already rapidly replacing imports from other unstable sources.

The net net of all of this is a lot of short term angst, but little long term impact. This is great for volatility owners (VIX), (VXX), but of little consequence to the rest of us.