Global Market Comments

September 24, 2020

Fiat Lux

Featured Trade:

(ELON’S BATTERY DAY BLOWOUT),

(TSLA), (GM), (F)

Global Market Comments

September 24, 2020

Fiat Lux

Featured Trade:

(ELON’S BATTERY DAY BLOWOUT),

(TSLA), (GM), (F)

I have to admit that I have been buying into Elon Musk’s vision since I first met him more than 20 years ago, back in his PayPal days. He could see how the future would unroll for the next 50 years.

That has delivered the best investment of my lifetime, with my Tesla shares (TSLA) up 151X from my initial $16.50 cost.

Thanks to Elon, my home is now completely grid-independent, with 59 solar panels and three 13.5-watt Tesla Powerwalls. I am only connected to PG&E so I can sell them my excess power at afternoon peak prices. In the mornings, I recharge my batteries. That’s a cool thing to have when your local utility completely shuts off power for six days a year.

So it was with some enthusiasm that I attended Tesla’s annual shareholder meeting and Battery Day.

Elon Musk was there with all his swagger and confidence in front of a giant screen. The audience was limited to those sitting in Teslas to enable social distancing, and when they approved, they honked horns instead of clapping.

It was a noisy event.

The past five years have been hottest on record. Climate change is accelerating, so the time to step up the move to a truly sustainable grid is here. It is nothing less than a matter of survival of the species. As Musk spoke, pictures of San Francisco's recent orange days, when you could see 100 feet, flashed up on the screen. A hundred-fold increase in our efforts is called for.

The good news is that 76% of the new electricity generation built this year will be wind and solar, or 32 GW. In 2010, 46% of electricity was coal-generated. Today it is half. Trump promises to rescue the industry came to nothing.

Even if 100% of new electricity generation comes from alternatives, it would take 25 years to convert the entire national grid. There is not enough time left to accomplish this to avoid environmental catastrophe.

The three legs of the future of power are solar power, solar storage, and electric cars.

Tesla has made a major contribution so far in all of these, with over 1 million electric cars produced, 26 billion electric car miles driven, 5 GWh of stationary batteries installed (I have 40.5 Watts), and 17 terawatt-hours of solar power generated.

The Shanghai Tesla factory went from a pile of dirt to mass production in an amazing 15 months, and that facility will soon be doubled in size.

“Tera is the new giga,” said Elon. A terawatt is 1,000 times more power than a gigawatt.

The world needs 10 terawatt-hours of new battery production a year to transition the global car fleet to all-electric in 15 years. We need 1,600 fold growth in battery efficiencies to convert the entire grid to electric. That means we need 25 terawatt-hours a year for 15 years. That is Tesla’s goal.

Tesla’s present Nevada Gigafactory is producing only 1.5 terawatt-hours a year in batteries. Would need 135 more factories to meet the above demand with current technology.

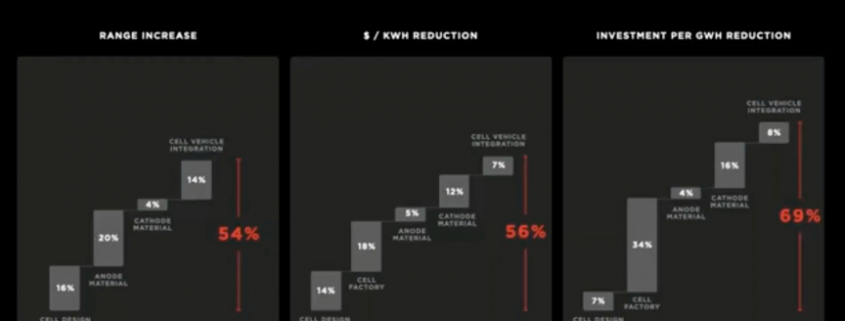

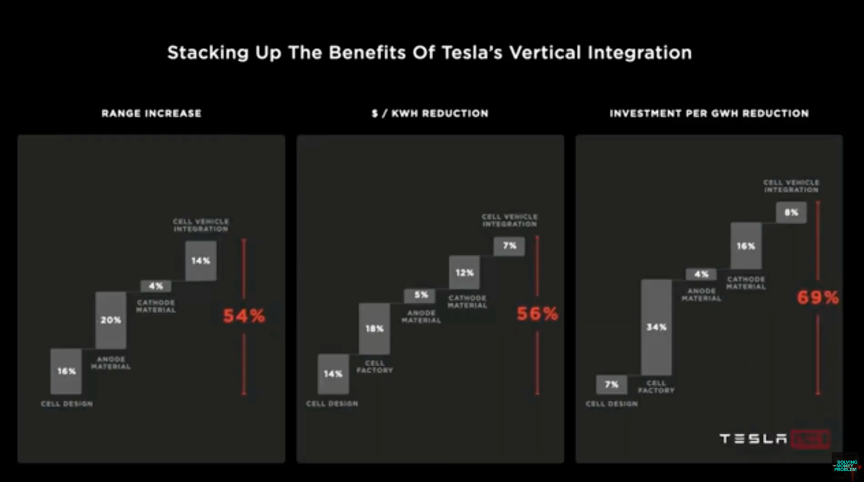

To achieve this, Tesla needs to make cars cheaper. The cost per kilowatt is not improving fast enough.

Tesla’s current plan to cut battery costs by half working by improving every one of the dozens of steps of production.

The newest battery design brings 6X increase in energy density levels, will begin mass production in a year in Fremont. Interestingly, Musk relied on existing paper and mottle mass production as models. The design is too complex to describe here but is brilliant. It’s easier to understand with the graphics found in the YouTube video below.

Down the road, dry electrodes will bring further 10X improvement in power. New machine designs and processes will bring a 7X improvement in output. Tesla’s plan is to achieve a further 75% improvement in the cost of production. The eventual goal is to make Tesla the best manufacturer on earth.

By 2022, Tesla will see a 100 GWh production increase in batteries and 3 terawatt-hours by 2030. That is a 30-fold jump.

Silicon is the most abundant element in the world after oxygen and will be used to replace existing graphite chemistry. Moving from processed silicon to raw silicon will deliver cheaper anodes and an 18% cheaper battery. Cathodes will use nickel-manganese allowing an 80% cost reduction.

Some 100% of batteries are now recycled, will eventually become sole source of raw materials for new batteries. Thus, it will become a super-efficient closed cycle.

Tesla will also reduce car costs by casting the battery as a single piece of the car body. The aircraft industry first accomplished this with fuel tanks during WWII. This alone would eliminate unnecessary 370 parts.

The next upgrade in design and manufacturing will take three years to implement and deliver a 69% reduction in cost creating a “compelling” $25,000 car that is fully autonomous and will not need maintenance.

This chops the lifetime cost of Teslas by half when compared to conventional gasoline-powered engines. If Musk can deliver on this promise, General Motors (GM) and Ford Motors (F) are toast.

Tesla is also developing a new supercar. The Tesla Plaid Model S will have a 520-mile range, go from zero to 60 miles per hour in under two seconds, and offer a positively bestial 1100 horsepower motor. You can order yours at the end of 2021. No price was mentioned, but my guess is somewhere north of $250,000.

I already have the Model X with “ludicrous” mode that catapults from 0 to 60 in 2.9 seconds and just that presents a major whiplash risk.

After the event finished, it was clear that the stock market was not drinking the Kool-Aide, Tesla shares diving 5%. It turned out to be a big “buy the rumor, sell the news” event. When traders hear the words “long-term” they glaze over and run a mile.

We may need to wait for the next cycle of upgrades and product announcements to achieve a true upside breakout.

Mad Hedge Technology Letter

September 23, 2020

Fiat Lux

Featured Trade:

(THE HOT CLOUD IPO OF FALL 2020)

(SNOW), (ZM), (ORCL)

The good news is that investors are thirsting for new cloud IPOs boding well for tech firms like Airbnb who plans to go public later this year.

The long-term health of the U.S. tech sector is on solid footing.

Most recently we had Snowflake (SNOW) who is a cloud provider and has an impressive enterprise business.

The public cloud is the data storage unit which literally everyone stores their operations on that has benefited from a massive wave of digital migration.

Many of the cloud-targeted tech firms of recent years have been 10-baggers and have dominated the overall market's returns.

Typically, these companies trade at high premiums, and rightly so, because of the corresponding growth trajectories and Snowflake is no different.

The stock has doubled after less than half a month as a tradable market-moving instrument.

Even by the standards of the most expensive software companies on the Nasdaq index, Snowflake is not cheap, although it’s a growth monster.

Snowflake was valued at $12.4 billion in February and even has investor Warren Buffett, the Oracle of Omaha, among its investors.

Buffett dove headfirst into tech investments in Apple and even some Indian fintech firms as well.

Snowflake is the largest software IPO on record and the largest since Uber's $8.1 billion IPO in May 2019.

The firm was striving for a valuation of $20 billion. In total, Snowflake has raised $1.4 billion from investors including Sequoia and Iconiq Capital.

Snowflake even makes the high-flying Zoom (ZM) Video Communications look cheap which is hard to do.

Zoom is growing three times faster than Snowflake, but trades at roughly half of Snowflake's price-to-sales ratio.

Zoom is also profitable, whereas Snowflake is a huge loss maker and that is a staple of many tech startups. This is an economic environment that is more conducive to profit drive companies instead of the tech model of promising future growth.

Snowflake is over four times more expensive than cloud company Datadog.

Snowflake's market is thought to be bigger than most other niche software applications, and therefore it may have a longer runway. In the regulatory filing, Snowflake claimed its total addressable market was around $81 billion.

Along with many other growth companies, Snowflake's ultimate margin potential is still hard to fathom and more passengers are starting to arrive in the sector than drivers.

Even worse, Snowflake not only competes with legacy data warehouse companies such as Oracle (ORCL) and Dell but also with products from the cloud infrastructure company it collaborates with.

Since shares have already doubled, I do believe that investors will need to wait for a pullback to put money to work in Snowflake.

The company said it had about 3,100 customers, including 56 clients that contributed about $1 million in a 12-month period.

Even with the pricey valuations, Snowflake is the pre-eminent cloud listing of the second half of 2020 and its enterprise business is sustainable.

If a broader sell-off drags this name down into the $180s, pull the trigger and start wading into this one.

The stock is currently priced as such that it represents flawless execution quarter after quarter for many years, and they would have to live up to lofty expectations to grow into its valuation.

While the management is stellar and is known for its execution, the odds of Snowflake's stock faltering are high because of the high bar.

Keep this one on your hot list because with all the variables waiting to pull down the market, there will be a time when the price is right in Snowflake.

“If someone asks me what cloud computing is, I try not to get bogged down with definitions. I tell them that, simply put, cloud computing is a better way to run your business.” – Said Founder and CEO of Salesforce Marc Benioff

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

September 23, 2020

Fiat Lux

Featured Trade:

(AN INSIDER’S GUIDE TO THE NEXT DECADE OF TECH INVESTMENT),

(AMZN), (AAPL), (NFLX), (AMD), (INTC), (TSLA), (GOOG), (FB)

Last weekend, I had dinner with one of the oldest and best performing technology managers in Silicon Valley. We met at a small out of the way restaurant in Oakland near Jack London Square so no one would recognize us. It was blessed with a very wide sidewalk out front and plenty of patio tables to meet current COVID-19 requirements.

The service was poor and the food indifferent as are most dining experiences these days. I ordered via a QR code menu and paid with a touchless Square swipe.

I wanted to glean from my friend the names of the best tech stocks to own for the long term right now, the kind you can pick up and forget about for a decade or more, a “lose behind the radiator” portfolio.

To get this information I had to promise the utmost confidentiality. If I mentioned his name, you would say “oh my gosh!”

Amazon (AMZN) is now his largest holding, the current leader in cloud computing. Only 5% of the world’s workload is on the cloud presently so we are still in the early innings of a hyper-growth phase there.

By the time you price in all the transportation, labor, and warehousing costs, Amazon breaks even with its online retail business at best. The mistake people make is only focusing on this lowest of margin businesses.

It’s everything else that’s so interesting. While its profitability is quite low compared to the other FANG stocks, Amazon has the best growth outlook. For a start, third party products hosted on the Amazon site, most of what Amazon sells, offer hefty 30% margins.

Amazon Web Services (AWS) has grown from a money loser to a huge earner in just four years. It’s a productivity improvement machine for the world’s cloud infrastructure where they pass all cost increases on to the customer who, once in, buys more services.

Apple (AAPL) is his second holding. The company is in transition now justifying a massive increase in earnings multiples, from 9X to 40X. It now trades at 30X. The iPhone has become an indispensable device for people around the world, and it is the services sold through the phone that are key.

The iPhone is really not a communications device but a selling device, be it for apps, storage, music, or third party services. The cream on top is that Apple is at the very beginning of an enormous replacement cycle for its installed base of over one billion phones. Moving from up-front sales to a lifetime subscription model will also give it the boost.

Half of these are more than four years old, positively geriatric in the tech world. More than half of these are outside the US. 5G will add a turbocharger.

Netflix (NFLX) is another favorite. The world is moving to “over the top” content delivery and Netflix is already spending twice as much on content as any other company in this area. This is why the company won an amazing 21 Emmys this year. This will become a much more profitable company as it grows its subscriber base and amortizes its content costs. Their cash flow is growing by leaps and bounds, which they can use to buy back stock or pay a dividend.

Generally speaking, there is no doubt that the pandemic has pulled forward some future technology demand with the stay-at-home trend. But these companies have delivered normal growth in a hard world. Tech growth will accelerate in 2021 and 2022.

5G will enable better Internet coverage for everyone and will increase the competitiveness of the telecom companies. Factory automation will be another big area for 5G, as it is reliable and secure and can be integrated with artificial intelligence.

Transportation will benefit greatly. Connected self-driving cars will be a big deal, improving safety and the quality of life.

My friend is not as worried about government threatened breakups as regulation. There will be more restraints on what these companies can do going forward. Europe, which has no big tech companies if its own, views big American tech companies simply as a source of revenues through fines. Driving companies out of business through cutthroat competition is simply not something Europeans believe in.

Google (GOOG) is probably more subject to antitrust proceedings both in Europe and the US. The founders have both retired to pursue philanthropic activities, so you no longer have the old passion (“don’t be evil”).

Both Google and Facebook (FB) control 70% of the advertising market between them, which is inherently a slow-growing market, expanding at 5% a year at best. (FB)’s growth has slowed dramatically, while it has reversed at (GOOG).

He is a big fan of (AMD), one of his biggest positions, which is undervalued relative to the other chip companies. They out-executed Intel (INTC) over the last five years and should pass it over the next five years.

He has raised value tech stocks from 15% to 30% of his portfolio. Apple used to be one of these. Semiconductor companies today also fall into this category. Samsung with 40% margins in its memory business is a good example. Selling for 10X earnings, it is ridiculously cheap. It is just a matter of time before semiconductors get rerated too.

He was an early owner of Tesla (TSLA) back in the nail-biting days when it was constantly running out of cash. Now they have the opposite problem, using their easy access to cash through new share issues as a weapon to fight off the other EV startups. Tesla is doing to Detroit what Apple did to the cell phone companies, redefining the car.

Its stock is overvalued now but will become much more profitable than people realize. They also are starting to extract services revenues from their cars, like Apple has. Tesla will grow revenues 30%-50% a year for the next two or three years. They should sell several million of the new small SUV Model Y. Most other companies bringing EVs will fall on their faces.

EVs are a big factor in climate change, even in China, the world’s biggest polluter. In Europe, they are legislating gasoline cars out of existence. If you can make money building cars in Fremont, CA, you can make a fortune building them in China.

Tech valuations are high, there is no doubt about it. But interest rates are much lower by comparison. The Fed is forcing people to buy stocks, enabling these companies to evolve even faster.

When rates rise in a year or so, tech stocks may have to come down. They have a lot more things going for them than against them. The customers keep coming back for more.

Needless to say, the above stocks should make up your shortlist for LEAPS to buy at the coming market bottom.

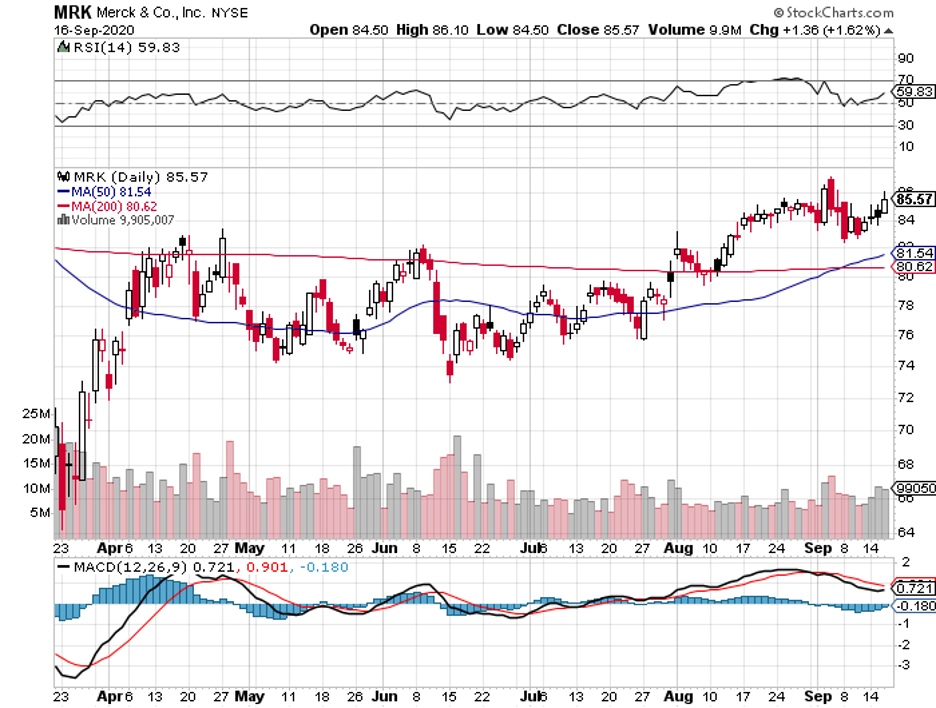

Mad Hedge Biotech & Healthcare Letter

September 22, 2020

Fiat Lux

Featured Trade:

(WHY MERCK IS UNDER-APPRECIATED IN THE COVID-19 RACE)

(MRK), (PFE), (MRNA), (RHHBY), (REGN), (BMY), (GILD)

The excitement over the COVID-19 vaccine candidates has boosted the shares of the most widely reported companies like Pfizer (PFE) and Moderna (MRNA). Meanwhile, other developers have not received the same love from investors.

However, it looks like another COVID-19 vaccine player will be joining Pfizer and Moderna under the spotlight: Merck (MRK).

Merck recently announced that it is now ready to test its vaccine on humans. The trials will be conducted in Germany, and the company has been scouring government databases for viable volunteers.

Unlike Pfizer and Moderna, which are utilizing a novel technology that will need two vaccine doses to be fully effective, Merck is working on two different COVID-19 vaccine candidates designed to work with only a single dose.

This could offer Merck a clear advantage over its competitors.

Also, one of Merck’s candidates could be taken in oral form. This is another significant advantage since it would make the vaccine easier and more convenient to administer.

Merck’s vaccine candidates contain a destabilized version of the same virus that causes measles. This virus is then used to deliver the coronavirus’ spike protein to the patient’s immune system, which would trigger an immune response.

The goal is not only to create a vaccine that would offer protection using a single dose, but also utilizing an existing and reliable technology that can be readily scaled up for mass production.

Since we need to immunize roughly 7 billion across the globe, Merck’s plan to manufacture a single-dose vaccine would be more convenient instead of using multiple doses.

Overall, the COVID-19 vaccine market could reach $50 billion in revenue by 2030.

Apart from its vaccine candidate, Merck is also looking into an antiviral treatment for COVID-19 patients

If successful, this product would be competing against Gilead Sciences’ (GILD) Remdesivir. Just like one of its vaccines, Merck is also developing a treatment in oral form instead of a hospital infusion.

Merck’s Remdesivir alternative can reduce the severity of the COVID-19 by interrupting the virus’s capacity to replicate.

Unlike Gilead’s drug, which can only be used in severe cases, Merck’s candidate can be prescribed immediately after a patient is diagnosed with the disease.

This COVID-19 cure is set to begin its Phase 3 trial this September, with Merck is confident that it can manufacture millions of doses before 2020 ends.

Experts dubbed this drug as an “underappreciated COVID-19 treatment,” which is estimated to reach blockbuster status.

Aside from not getting enough credit for its COVID-19 efforts, Merck is also not receiving enough attention for its pipeline.

So far, the company holds the leading drug that boosts the immune system to fight off cancer: Keytruda. It also has one of the leading vaccine franchises in the world.

Keytruda can easily generate $14.5 billion in sales in 2020 alone, which represents a 30% jump from its 2019 performance. More importantly, the drug can reach $22 billion by 2025.

However, investors are worried over Merck’s dependence on the drug, which comprises 30% of its revenue. In fact, Wall Street keeps zeroing in on the 2028 patent expiration of Keytruda.

At the moment, Keytruda faces competitors like Roche Holding (RHHBY), Regeneron Pharmaceuticals (REGN), and Bristol Myers Squibb (BMY).

However, Merck is not the type to put all its eggs in a single basket.

The company is developing new products that can generate an additional $13 billion to $18 billion in sales annually.

Among these treatments is another potential immuno-oncology antibody, which has been sent to clinical trials this year. Merck also has a long-term HIV treatment queued for clinical studies.

One exciting drug candidate is ARQ531, which is a potential cancer therapy. This projected blockbuster was part of Merck’s $2.7 billion acquisition of ArQule in January.

Other than this acquisition, Merck also obtained the rights to several cancer treatments, which are hailed to be more effective than the conventional chemotherapy, thanks to its acquisitions of Astex Pharmaceuticals and Taiho Pharmaceuticals.

In terms of its vaccine franchise, this arm of the business is projected to generate $9 billion in annual sales in 2021, with the revenue steadily rising to $100 billion in the next several years.

In particular, Merck is looking into developing further its cervical cancer vaccine Gardasil. So far, this vaccine is estimated to generate roughly $3.9 billion in sales in 2020 and reach $5.5 in 2023.

The focus on boosting its vaccine franchise is a strategic move considering that vaccines are generally a durable business and are typically immune from any generic competition.

Although it is not one of the leading vaccine developers in the COVID-19 race, Merck has positioned itself as the leader in the cancer drug development sector and its distribution over at least the next decade.

I believe that Merck’s prudent business, strategic acquisitions, and exciting pipeline will gradually push the stock to the top.

In summary, I think that Merck is a good stock to buy. For those searching for a strong biopharmaceutical play at a reasonable price, this company should be on your shortlist.