Global Market Comments

March 30, 2021

Fiat Lux

Featured Trade:

(HOW THE MAD HEDGE MARKET TIMING ALGORITHM TRIPLED MY PERFORMANCE)

Global Market Comments

March 30, 2021

Fiat Lux

Featured Trade:

(HOW THE MAD HEDGE MARKET TIMING ALGORITHM TRIPLED MY PERFORMANCE)

Mad Hedge Technology Letter

March 29, 2021

Fiat Lux

Featured Trade:

(THE SECULAR TAILWINDS ARE INTACT)

(AMZN), (FB)

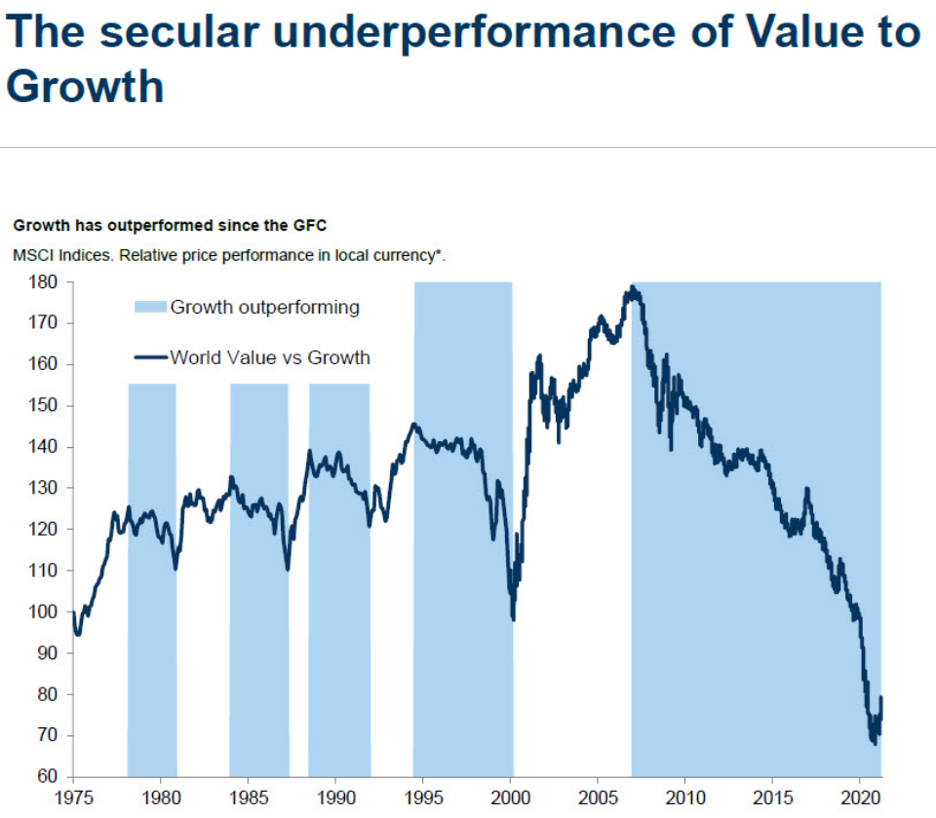

As we zoom out from tech, energy and industrials stocks have muddled through lately relatively well, while growth tech has been lethargic.

I cannot argue that we are in the middle of a rotation away from growth with capital migrating into value stocks.

Issuing low-interest rate corporate debt and spinning around to unload it to the debt market is advantageous because growth projects can be initiated without worrying about a crushing amount of future interest payments.

There is an expectation of three rate hikes by the end of 2023 which the market must absorb.

Then a mid-term expectation that the domestic economy will come roaring back is now penalizing expensive cloud services and digital communications stocks.

So now, here we are at a rock and hard place with growth with the broader market attempting to digest these roadblocks before the Nasdaq turns higher.

Just take a look at the ultimate growth stock Amazon (AMZN) or even Facebook (FB) to see a frustrating sideways consolidation from last September.

As much of this is quite disheartening for the tech investor, the tech sector remains one of the best places to look for companies creating innovative products and services that transcend industries.

I view this more as a buy the dip opportunity with the dip being elongated with numerous external events working against tech stocks.

So what are tech’s secular drivers?

According to IDC, investments in digital transformation will nearly double by 2023 to $2.3 trillion, representing more than 50% of total IT spending worldwide.

Deloitte recently released a report revealing that during the next 18 months, they expect to witness global companies embrace the bespoke-for-billions trend by exploring ways to use human-centered design and digital technology to create personalized, digitally enriched interactions at scale.

The study found that digital engagement was essential in 2020, with 96% of business leaders reporting companies who did not digitize customer engagement would experience severe negative repercussions.

These problems include a reduction in competitiveness and an inability to meet customer demands.

The companies who chose to embrace software agility meant empowering their developers to prepare tech firms for the unknown and meeting these customer expectations.

Whether it's a meteor hitting the earth, or anything else that is threatening to disrupt an industry or a business, the companies who do best can change on a dime to suit themselves for conditions in the current marketplace.

The health crisis accelerated transformation overnight.

Healthcare had to accelerate the adoption of telemedicine, and commerce companies accelerated their e-commerce plans.

The funnel that led to the consumer wallet has forever changed and in 2021, we will see further strength and momentum where we left off from last year.

Given the increased importance of digital engagement to the company's success moving forward, nearly all business leaders surveyed, 95%, expect to increase investment in digital tools after the pandemic.

Firms are now hyper-targeting a model revolving around customer engagement platforms that truly serve the end-to-end life cycle of all customer engagement in the enterprise.

Why? Because companies need to understand who their customers are, what products they're looking for, what products they bought, and where customers are interacting with their brand across multiple touchpoints.

Platforms allow the developers of the world to build, to take all of those bits of data that are siloed throughout the company to build a cohesive picture of the customer, build a world-class customer service experience and deliver the right communication over the right channel at the right time.

The endgame is to meaningfully improve every interaction every business has with every customer.

That's incredibly valuable to enterprises because it allows them to create differentiated customer experiences and all of the successful tech companies have participated in this trend.

I think that the infrastructure to build great digital products and great digital experiences spans many categories.

This rich area of opportunity will unlock developer influence and developers' ability in tech companies to build the future of these companies.

Now that every other company and industry needs tech to reach the end-user and to even initiate the selling cycle, tech is entrenched as the long-term winner.

Global business will cease to exist without software and no company will reach full potential without being powered by the best tech tools in the world, period.

And as the digital transformation is suppressed momentarily by external factors out of the control of the tech companies themselves, tech investors wait for signals for when the consolidation is over.

Tech already comprises 40% of the S&P, and by 2030, that number will be close to 75%.

This is still an industry that nobody should bet against in the long term.

“A founder is not a job, it's a role, an attitude.” – Said Founder and CEO of Twitter and Square Jack Dorsey

Global Market Comments

March 29, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WEEK THAT NEVER WAS),

(SPY), (TLT), (TBT), (TSLA), (CSCO), (ORCL), (INTC)

Of course, WWII historians know well the man who never was, the popular name for Operation Mincemeat.

In 1943, British intelligence found a homeless man who died on the streets of London, dressed him up as a Royal Marine Major William Martin, and released his body from a submarine off the coast of Spain, a German ally.

Handcuffed to his wrist was a briefcase with highly detailed plans for the allied invasion of Greece and the Balkans. The Germans shifted ten divisions to defend the region.

When the allies invaded Sicily instead, it came completely out of the blue. The invading American and British forces found the island almost undefended and inadequately manned and supplied by Italian troops. The allies planned for three months to capture Sicily. Instead, they did it in a mere 38 days. Allied losses came in at a tenth of those expected, thanks to Royal Marine Major William Martin.

The analogy here is that last week, we witnessed the market that never was. Stocks went down, then up. Bonds went up, then down. Even Tesla was virtually unchanged. It all ended up as a big fat zero for traders.

What all of this means for us investors is a subject of heated discussion among strategists. Of course, the Cassandras are always out there arguing that this is all proof that markets are peaking and that the mother of all stock market crashes is just ahead of us.

I take a different tack.

I think we are well into a long-overdue “time” correction whereby stocks go sideways for weeks or months before resuming their heroic assault on new highs. The timing will be dictated by the frantic reversal of the bond market at a ten-year Treasury yield of 2.00%.

Investors will rotate from the newly expensive recovery plays like banks into the newly cheap, such as technology stocks. Notice the sudden recent interest in legacy companies like Oracle (ORCL), Intel (INTC), and Cisco Systems (CSCO), which completely missed the great 2020 tech rally.

All of this sets up perfectly for the barbell portfolio which I have been advocating all year.

If there is a selloff, it will be by things that normal people don’t own. Those include SPACS, anything the Reddit crowd chases, stay-at-home stocks, and very high-priced tech stocks with no earnings.

Much focus has been placed on the Taiwanese-owned Ever Given stuck in the Suez Canal. As a Middle Eastern war correspondent for many years, I spent endless hours debating with my compatriots over what closure of the canal would mean.

What hasn’t been mentioned was that the accident was not caused by a Chinese captain, but Egyptian pilot ships are required to take on to raise revenues, and bribes, for the impoverished country. This all happened in the middle of a sandstorm where visibility is near zero.

I can tell you right now that they won’t get the Ever Given off there until they start to unload containers and lift off some weight so the 200,000-ton ship can rise of its own accord. Good luck with that in the middle of the Sinai Desert. Why not just sell all the contents on Amazon and have them deliver it for free as part of their prime membership?

This is a debacle that will last weeks, if not months, and will cost $9 billion a day in international trade until it’s over. In the meantime, commercial shippers have asked for protection from pirates from the US Navy as they navigate the unfamiliar water around the tip of Africa.

The Mad Hedge Summit Videos are Up, from the March 9,10, and 11 confab. Listen to 27 speakers opine on the best strategies, tactics, and instruments to use in these volatile markets. The product discounts offered last week are still valid. Start, stop, and pause the videos at your leisure. Best of all, access to the videos is FREE. Access them all by clicking here, click on CURRENT SUMMIT REPLAYS in the upper right-hand corner, and then choose the speaker of your choice.

Weekly Jobless Claims dive by 100,000, to 684,000, a one-year low. The decline was led by Illinois and Ohio. Labor shortages are popping up around the country in skilled areas, but bars and restaurants are still lagging severely.

Huge Office Cuts are coming, with execs planning a permanent 20% cut. Better to give the money to shareholders. Downtowns across the country will change beyond all recognition. How do you turn an office into an apartment?

CP Rail buys Kansas City Southern, for $25 billion, further concentrating the north American rail industry. It’s a steal because an economy entering a decade-long boom moves lots of stuff. It’s also a great North/South international trade play, which is recovering strongly with the exit of our last president. I used to ride box cars on the old Canadian Pacific back in the sixties (you can’t hitch hike where there are no cars), and occasionally the engineers would let me drive. It suddenly makes Norfolk South (NSC) and Union Pacific (UNP) look very tempting.

Another Tesla $3,000 Target was issued by Ark’s Cathie Wood, an early investor. Cathie’s Ark Innovation Fund ETF was up 180% last year largely on the strength of a massive Tesla (TSLA) holding. Her bear case is a low of $1,500 by 2025, nearly triple the current price. She has only one more triple to go to get to my own $10,000 forecast.

Biden has $3 Trillion More to Spend on top of the just passed $1.9 trillion rescue package. It's all rocket fuel for the stock market, not so much for bonds. The money will be spent on a mix of old-line freeway and bridge repair along with new spending on decarbonizing the power grid and social measures. It will be financed by tax hikes on those earning over $400,000. Remember, Roosevelt hiked the maximum tax rate to 90% on the wealthy, where it stayed for 30 years, and Biden is old enough to remember.

Daily Air Travelers top 1.5 Million, for the first time in a year. The pandemic low was 200,000 a day. It’s an indication of how anxious Americans have become to travel, and how strong the imminent economic boom will be.

Intel to build two chip fabs for $20 billion in Arizona to address the current severe shortage. US construction is a positive as it helps reduce reliance on foreign supplies. Too bad it will still leave them five years behind (AMD), but it’s a major move in the right direction. It deals with everything investors wanted to hear and moves them solidly into the 10nm architecture market. Buy (INTC) on dips.

New Home Sales Dive, off 18.2% in February, now that the free money train has left the station. Weather was blamed as a factor, with giant snowstorms slamming much of the country. Shortage of supply is another big issue. Some big builders are basically out of inventory and are reduced to selling floor plans with extended completion dates.

US Dollar (UUP) hits a four-month high, with a major assist from rising US bond interest rates. Expect the rally to continue until ten-year yields hit 2.00%, then sell the daylights out of it. With the US money supply growing at a near exponential 30% annual rate, there’s no way the dollar strength can continue. When you increase the supply, you decrease the value, simple supply and demand. My first pick is to buy the Aussie (FXA) a call option on a global synchronized economic recovery.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000, here we come!

It’s amazing how well patience can help your performance. My Mad Hedge Global Trading Dispatch profit reached a super-hot 18.61% so far in March on the heels of a spectacular 13.28% profit in February.

It was a go-nowhere week in the market, so I limited myself to a single trade all week, a double short in the bond market (TLT) on top of a welcome $5 rally. The position turned immediately profitable.

I still have a deep in-the-money call spread Tesla (TSLA) that is profitable and expires in 14 trading days. That leaves me with 70% cash and a barrel full of dry powder.

This is my fifth double-digit month in a row. My 2021 year-to-date performance soared to 42.10%. The Dow Average is up 9.9% so far in 2021.

That brings my 11-year total return to 464.65%, some 2.08 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 41.30%.

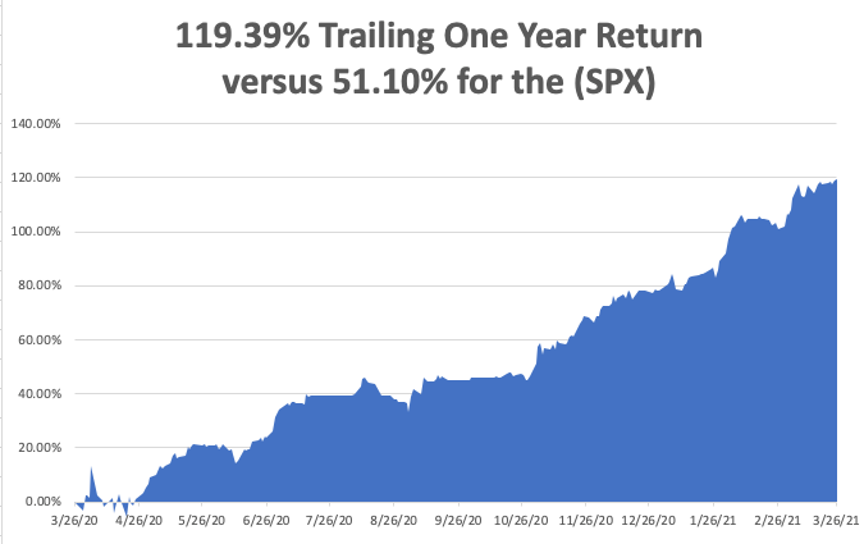

My trailing one-year return exploded to positively eye-popping 119.39%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Corona virus cases at 30.2 million and deaths topping 550,000, which you can find here.

Thankfully, death rates have slowed dramatically, but Obituaries are still the largest sector in the newspaper. At this point, some 47% of the US population has achieved immunity through vaccination or catching the disease. Herd immunity is near.

The coming week is a big one for jobs data.

On Monday, March 29, at 9:00 AM, the Dallas Fed Manufacturing Index for March is released.

On Tuesday, March 30, at 9:00 AM, the S&P Case Shiller National Home Price Index for January is published.

On Wednesday, March 31 at 8:15 AM, the ADP Challenger Private Employment Report for March is out. Pending Home Sales for February are indicated at 9:00 AM.

On Thursday, April 1 at 8:30 AM, the Weekly Jobless Claims are published.

On Friday, April 2 at 8:30 AM we get the Nonfarm Payroll Report for March. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, tax time is coming up and let me tell you, I have absolutely the best IRS story of all time.

It comes from my late, dear friend, Al Pinder, who I sat next to for ten years at the Foreign Correspondents of Japan in Tokyo, pounding away on antiquated Royal typewriters until our shoulders were as stiff as boards. Al then was the shipping correspondent for the New York Journal of Commerce newspaper.

Al was a colorful character, to say the least.

In the run up to WWII, Al took an extended vacation in Japan where he toured and photographed the country’s beaches, looking for the best landing sites for the US military in case war broke out.

To sneak the top-secret pictures out of the country, he bought a large steamer trunk and placed them a false bottom. Then he went to Tokyo’s red-light district in Yoshiwara, bought a dubious sex toy, an inflatable life-sized Japanese doll, and placed it on top.

When the trunk was searched, the customs officials found the doll, had a good laugh and passed him on. Al’s photos were the basis of Operation Olympic, the 1945 US invasion of Japan, made unnecessary by the dropping of the atomic bomb.

When the war broke out, Pinder parachuted into western China, where he acted as the liaison with Mao Zedong’s guerilla forces in Hunan province. In 1944, Al received a coded message from headquarters ordering him to intercept a top-secret airdrop from a DC3 in the middle of the night.

Knowing he would be mercilessly tortured by the Japanese if caught, he set up three signal fires in a triangle in a remote part of the desert and managed to find the parachute. Dodging enemy patrols all the way, he returned to his hideout in a mountain cave and opened the package.

In it was a letter from the IRS asking why he had not filed a tax return for the past three years.

I told this story at Al’s wake a few years ago and everyone had a good laugh. Al went on to run CIA operations in Japan during the fifties and sixties. When he passed away, there was a frantic search for a safe deposit box by American intelligence officials containing records of all CIA payoffs to Japan’s leading conservative party.

When the box was finally found, there was an enormous sigh of relief at the embassy. I still miss Al.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

March 26, 2021

Fiat Lux

Featured Trade:

(AVOID THIS KOREAN ECOMMERCE COMPANY)

(CPNG), (AMZN), (GRUB), (UBER), (JD), (SHOP), (MELI)

I might characterize Coupang (CPNG) as something akin to China’s JD.com.

It's an e-commerce company that has fulfillment solutions, not dissimilar to Amazon (AMZN) Fulfillment. They also have storefronts that they provide for businesses, which isn't dissimilar to say, a Shopify (SHOP).

Even combining aspects of Amazon and Shopify are there but they don’t have the powerful AWS cloud business.

Similar to JD.com (JD), which is a Chinese e-commerce platform, Coupang has differentiated itself by owning its entire logistics and delivery system.

What is different about Coupang versus the other players in Korean e-commerce is that they own their own inventory for the most part.

That means that they have inventory sitting on their balance sheets.

They have responsibility for pushing that through. But it also means, since they directly negotiate with the manufacturers of these items, they're able, for the most part, to get lower prices.

Total Korean e-commerce spend was $128 billion in 2019, which is expected to grow to $206 billion by 2024, implying a CAGR of approximately 10%.

This is where Coupang has a chance but in a rising interest rate environment and with competition on the New York exchanges from Amazon (AMZN), Shopify (SHOP), even MercadoLibre (MELI), I don’t believe Coupang is more attractive than these 3 in its current form as it relates to American investors pouring money into their stock.

Is it an advantage if 70% of Koreans live within seven miles of the Coupang logistic centers?

Certainly, there is that train of thought.

The massive investments into fulfillment centers mean they can surpass the delivery speed of many of its competitors because South Korea is essentially one capital city with millions upon millions hovering on top of each other like many other parts of Asia.

The problem I can have with this scenario is that margins could suffer because a busy Korean lifestyle doesn't lend itself to things like in-store shopping as readily as it does in the United States, and it could manifest itself with Koreans tapping into higher frequency in which they buy online which will push up total spend, but margins will decrease because you are buying stuff that won’t move the needle higher because you've paid for the service.

I can easily see someone just buying one item for delivery in the morning and doing that seven days per week.

Now I need a set of tweezers, I'm going to order that. Tomorrow, I need cotton pads, I’m going to order that.

Over time, operating margin will get butchered with a business like this.

And what do you know? I’m right, they have been losing billions upon billions the past few years with no end in sight.

How long will the external investors subsidize their losses?

At a broader level, mobile phone penetration is already at 96% of Koreans and 40% of Koreans order groceries online, so it’s hard for me to digest where the addressable market can expand from here because they have already collected so much of the available harvest.

This IPO does feel a little bit like an ex-growth dump on the retail investor and that’s not saying shares can’t appreciate at all, but investors believing this is the next Amazon are sorely mistaken.

They are not Amazon, not even close, and they are also confined to one small market where the population has peaked and will start decreasing in numbers.

The population is only 15% of the U.S. and incomes in the U.S. are vastly higher, so how does Coupang become an Amazon without the AWS business?

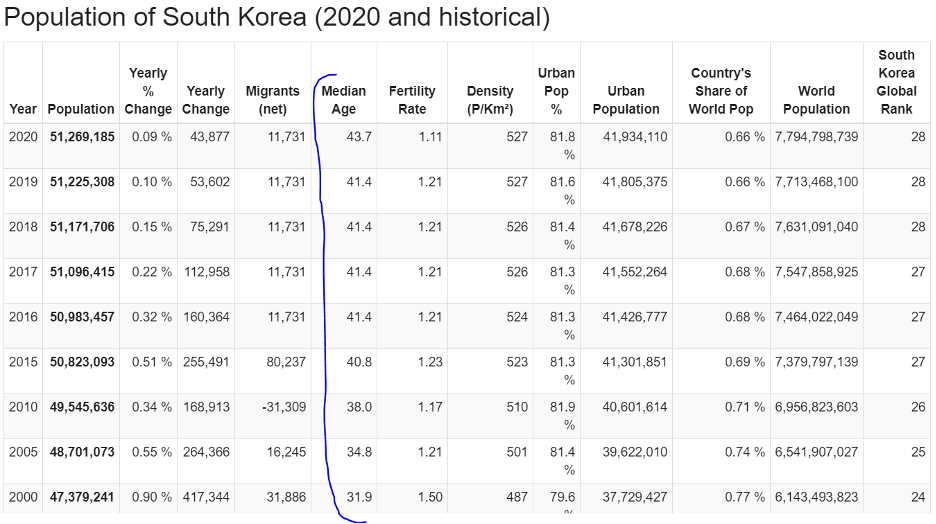

Just as disturbing, the median age in Korea has ballooned from 31.9 in 2000 to 43.7 in 2020 and this cohort doesn’t strike me as the group in the glory years of family formation, peak spend, or technological know-how.

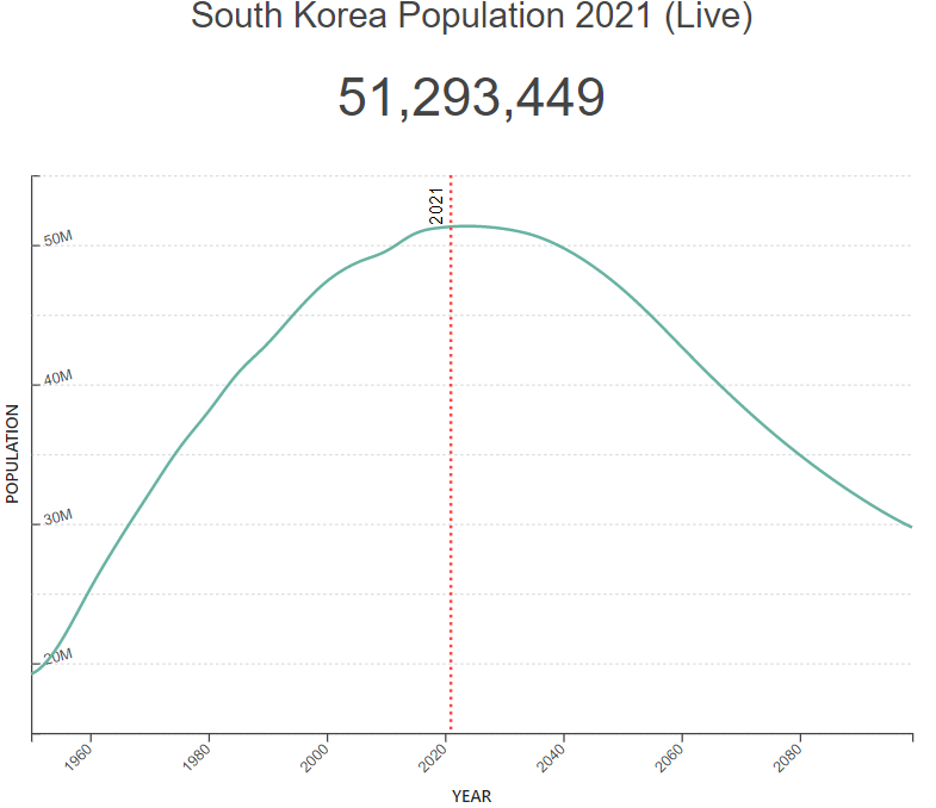

As the Korean population starts to decline in 2025 and the median age creeps up from 43.7 to 50, then aside from adult diapers, where does the incremental growth come from in Korea?

I just don’t see it.

Personal incomes are going to rise at an annualized rate of about 3% every year and I believe much of the total spend will be fought out attempting to woo the big buyers which offer a point of attack for competition that should come around in the next 2 to 3 years.

They also have Coupang Eats, not dissimilar to Grubhub (GRUB) or Uber (UBER) Eats. They have grocery delivery, and even an integrated payment processor. All of these things that took Amazon much longer to build out, admittedly, were a little before their time there, Coupang has already integrated that into the platform.

For this, I give them credit, but they are still nothing like Amazon in terms of potency and scale.

In 2019, active customers rose 34% and that’s what a prototypical growth company should do.

It’s not shocking.

Then an analyst would think that with covid and all that public chaos pinning consumers at home, surely, Coupang would grow active customers by 50% of even 60% in 2020, right?

But active customers only grew 18% in 2020, and they provided zero insight about why active customer growth slowed nearly in half year-over-year, and that for me shows, Coupang is severely limited by what Korea can offer in terms of growth and total spend.

If readers want to get into the Korean economy then I would advise to wait on other Korean homegrown entrepreneur-led startups with IPOs in the pipeline by Krafton Inc., the creator of hit game PUBG, and the country’s biggest mobile-only bank Kakao Bank. Unlike Coupang, those firms are profitable.

Ultimately, total e-commerce spend for all Internet buyers in Korea is expected to grow from approximately $2,600 in 2019 to approximately $4,300 in 2024 on a per buyer basis and Coupang will take advantage of that but I don’t foresee the 30% annual rise in underlying shares that others do.

I can definitely visualize a grind up with periodical substantial selloffs because of missed targets and disappointing forecasts.

That’s not the type of price action I want to see.

The signs point to Coupang maturing immediately and the executive management creating a special clause to allow them to dump shares right after the IPO illustrates that this tech company will stall out moving forward.

Normally, management must wait 6 months after going public before the lock-up period ends.

Highly unusual and can you believe it? They even gave stock shares to their courier drivers at the IPO, making me pause, then come to the conclusion that I rather invest in a tech company returning incremental value to the shareholders and not the manual labor that is paid by an hourly wage. How bizarre!

Avoid Coupang like the plague.

“If you're gonna make connections which are innovative... you have to not have the same bag of experiences as everyone else does.” – Said Co-Founder of Apple Steve Jobs

Global Market Comments

March 26, 2021

Fiat Lux

Featured Trade:

(PLAYING THE SHORT SIDE WITH VERTICAL BEAR PUT SPREADS)

(TLT)