Global Market Comments

April 20, 2021

Fiat Lux

Featured Trade:

(WATCH OUT FOR THE COMING COPPER SHOCK)

(FCX), ($COPPER)

Global Market Comments

April 20, 2021

Fiat Lux

Featured Trade:

(WATCH OUT FOR THE COMING COPPER SHOCK)

(FCX), ($COPPER)

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Technology Letter

April 19, 2021

Fiat Lux

Featured Trade:

(AN ECOMMERCE / EGAMING BEHEMOTH TO LOOK AT)

(SEA)

Do you want to invest in the 3rd most downloaded app in the shopping category globally for 2020?

Well, you can.

And that’s not all this company does, there is more.

This tech company is also part of a wider portfolio that includes Esport assets.

Sea Limited (SEA) is listed on the Nasdaq stock exchange under the ticker symbol SEA.

SEA, previously known as Garina, is headquartered in Singapore and serves the South East Asian and Latin American markets.

In both the fourth quarter and for the full year, Shopee, SEAs ecommerce division, was ranked the No. 1 in the shopping category across Southeast Asia and Taiwan by average monthly active users, total time spent in-app on Android, and the downloads based on App Annie.

Initially, SEA was a communication platform for video gamers, before distributing games made by Tencent for the Southeast Asian audience.

The company then went on to produce its own in-house game, Free Fire, which became an international phenomenon on the company's first try out of the gate.

Free Fire was once again the top-ranked mobile-only video game and the top-ranked battle royale video game on YouTube in terms of views.

It was also the third-ranked game overall on YouTube by view count. Free Fire-related content recorded over 72 billion view count across YouTube globally over the course of the year.

The game was also named the Esports Mobile Game of the Year at the Esports Award 2020.

They have the in-game titles to accumulate the eyeballs in its ecommerce division.

SEA's ambition went well beyond video games, and the company then launched Shopee in 2015, along with SeaMoney, its digital financial-services arm around the same time.

Shopee has been a winner, overtaking early e-commerce players in the region just as Southeast Asians began to adopt e-commerce at a larger scale.

The pandemic then hit just as Shopee was overtaking its rivals, leading to meteoric growth last year.

It continued to invest in its fintech ambitions by buying Jakarta-based bank Bank BKE. Acquiring a bank signals SEAs ambition to become a swiss army knife of financial services beyond mere e-commerce payments.

Second, Sea Limited has also entered Latin America in a dramatic fashion.

After starting with a small e-commerce presence in Brazil in 2019, Shopee just launched its app in Mexico in February.

The launch signaled that SEA is targeting Latin America for the next phase of incremental growth, where e-commerce is underpenetrated, and where it can cross-market effectively with the many Free Fire players in the region.

Moreover, Latin America has an even bigger population than Southeast Asia, with 2019 GDP of $5.2 trillion, versus Southeast Asia's $3.6 trillion.

The recent performance is quite breathtaking, to say the least with total revenue increasing 102% year on year to $1.6 billion in the fourth quarter, and 101% year on year to $4.4 billion for the full year of 2020.

This was mainly driven by rapid rate growth in SEAs e-commerce business as they continue to grow tools to better serve users' needs, as well as the growth of the digital entertainment business, especially self-developed game Free Fire.

The proof is in the numbers.

To sustain the momentum in Esports, in the fourth quarter, Phoenix Labs, SEAs triple-A gaming studio based in Vancouver, is adding new offices in Montreal and Los Angeles, alongside its existing - existing bases in Vancouver and Seattle.

Shopee reported 1 billion gross orders, up 135% year on year, and a gross market value (GMV) of $11.9 billion, an increase of 113% year on year resulting in quarterly revenue growing 178% year on year to $842.2 million.

Shopee continued to rank first in Indonesia by average monthly active users, total time spent in-app on Android, and the downloads in the shopping category in the fourth quarter and the for the full year of 2020.

For the full year of 2021, SEA currently expects bookings for digital entertainment to be between $4.3 billion and $4.5 billion, representing 38% year-on-year growth.

Sea Limited also expects that revenue for e-commerce could be between $4.5 billion and $4.7 billion, representing 112% and year-on-year growth as a mid-point of the guidance.

A tech company that grows revenue from $4.38 billion to a projected $9 billion by end of 2021 has caught my eye but there are some major caveats.

The first major eyesore is the gigantic losses.

Granted, net losses are only half as bad as Uber, but they have a track record of badly missing earnings projections as well.

This would lead me to suggest that the company is not being managed properly if they consistently forecast earnings that are unattainable.

I am quite discouraged by the lack of future profitability rhetoric by management in their earnings call.

Next, they are targeting markets of Latin America and South East Asia that aren’t as lucrative as the North American markets.

Granted, North America is cornered by local incumbents, but that doesn’t change the fact that consumer purchasing power in Mexico, Brazil, and Indonesia is low.

Being a foreign company, regulatory risks are now the order of the day as well.

In the past 365 days, the underlying stock has risen around 500% validating the trajectory of this tech group as a real ecommerce and digital gaming force.

The stock year to date is only up 20% suggesting the pace of appreciation is plateauing and even though annual revenue is projected to double in 2021, I do believe there will be consolidation before the next leg up.

Cut it up any way you want, in a market that pays a premium for big loss-making tech firms, the over 100% in projected revenue growth in 2021 delivers exactly what the tech market desires.

But like other growth stocks ROKU, the ride up will be exhilarating and rocky because unpredictable earnings results are part and parcel of high beta tech stock’s inner workings.

Readers looking for global exposure in a volatile tech name taking advantage of the emerging ecommerce story, take a look at Sea Limited on a meaningful pullback.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

April 19, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LIE BACK AND THINK OF ENGLAND)

(JPM), (BAC), (AAPL), (FXI), (TLT), (VIX), (TSLA)

If you have to ask what this classic phrase from Britain’s colonial past means, you are too young to know.

The stock market equivalent is that there is nothing to do. Just sit back and relax, watching the value of your stocks go up every day. Let the greatest monetary and fiscal stimulus work its inevitable magic.

When I said last week that stocks might go up every day in April, I wasn’t kidding. NASDAQ (QQQ) has gone up every day this month except one. The S&P 500 has seen only two down days when it was virtually unchanged.

And the best may be yet to come.

The mere prospect of a $2.3 infrastructure trillion budget is enough to keep stocks powering upward for the foreseeable future. Biden may have to negotiate the total down to get it through congress and that may be the cause of the next correction…in about three months.

What really had the phones buzzing on Thursday was the bizarre move in the bond market. After seeing spectacularly positive data, the Weekly Jobless Claims plunging by 200,000 and Retail Sales coming in at a prolific 9.8%, bonds should have crashed.

Instead, the (TLT) jumped by $2.60. That took interest rate and inflation fears packing and sent the indexes soaring to all-time highs once again.

It’s proof yet again that inflation is the boogie man that will never show. Despite the incredible strength of the economy, any time anyone tries to raise prices, another company comes along with a better product or service at half the price. Such is the relentless tide of technology.

In the meantime, Goldilocks has moved in, unpacked her bags, gotten comfortable, and has settled in for the duration. I have been so aggressive in trading the market for the last six months it is wearing me out.

So, I took a rare Saturday off, weeding the garden, setting up a new computer, and generally fixing things that I haven’t had time to attend to since last year. I lived almost normally….for a day.

One of the best Earnings Seasons in history started last week, with 25% growth expected at 81% beating forecasts. JP Morgan (JPM) and Bank of America (BAC) kicks off on Wednesday, with the big kahuna, Apple (AAPL) reporting on April 28. Expect stocks to rally until then. It may give us the first hint of the massive stimulus on the economy to come. Q2 and Q3 will be the monster quarters.

Equity Funds pick up a half trillion dollars in five months, more than they attracted over the last 12 years. It’s all rocket fuel for the ongoing market melt-up. With the Volatility Index (VIX) at a one-year low at $17, the best may be yet to come. Equity investors are the most bullish in years.

Tesla is upgraded to $1,071 per share by research firm Canaccord Genuity. The company is transitioning from low-volume high-priced cars to high-volume low-priced cars, as seen in the 47% leaps in sales during Q1. The stationary battery business is booming, thanks to a new generation of technology. Tesla is developing an Apple-type brand value in the energy market, which is worth a big premium, which competitors can’t match. Tesla has brought a machine gun to a knife fight. Global chip shortages are a risk. The stock jumped $25 on the news.

Consumer Price Index comes in muted at 0.6% in April and 2.6% YOY. The market had been fearing worse, sparking another leg up in technology stocks. Much of the gain was from a jump in gasoline prices, which are now falling. Food prices are also rising.

JP Morgan pops on upside earnings surprise, with Q1 profits soaring from $2.9 billion a year ago to an eye-popping $14.5 billion. Revenues were up 14% to $33.1 billion. Loan demand is weakening because so many people are getting government money for free. Credit card debts are being paid down.

Retail Sales explode in March, up a staggering 9.8%. New spending at bars and restaurants was a major factor, and we haven’t even started yet! Stocks soar to new highs, and the bond market takes off like a scalded chimp, taking ten-year US Treasury yields below 1.57%. It confirms my thesis that when we see actual real numbers of an unprecedented recovery, we get another new leg in the bull market.

Weekly Jobless Claims collapse to 576,000, the lowest of 2021. That's down a massive 193,000 jobs from the previous week. Herd immunity is here! Keep getting those shots!

China’s (FXI) GDP grew by a staggering record of 18.3% in Q1 at an annualized rate YOY. Strong industrial production and exports were the leaders. It presages a similar explosive growth rate for the US in Q2. We won’t know until the end of July. Having your largest customers breaking growth records is great for your business too. Buy everything on dips.

Hedge funds nailed the Bond Crash, selling short some $100 billion in paper since January. It will be more than enough to cover their losses in equity shorts.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 7.17% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

It was a very busy week for trade alerts, with five positions expiring at their maximum profit points in (TSLA) and the (TLT). It’s been so long since I’ve had a loss, I forgot what they looked like.

I used a puzzling $2.60 spike in the (TLT) to add to my already substantial short position in bonds (TLT) with a distant May expiration. Ten-year US Treasury yields fell all the way to 1.51%.

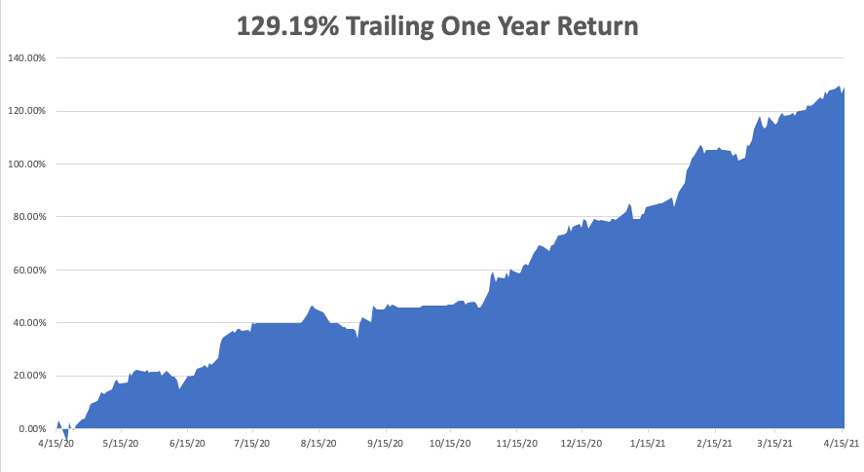

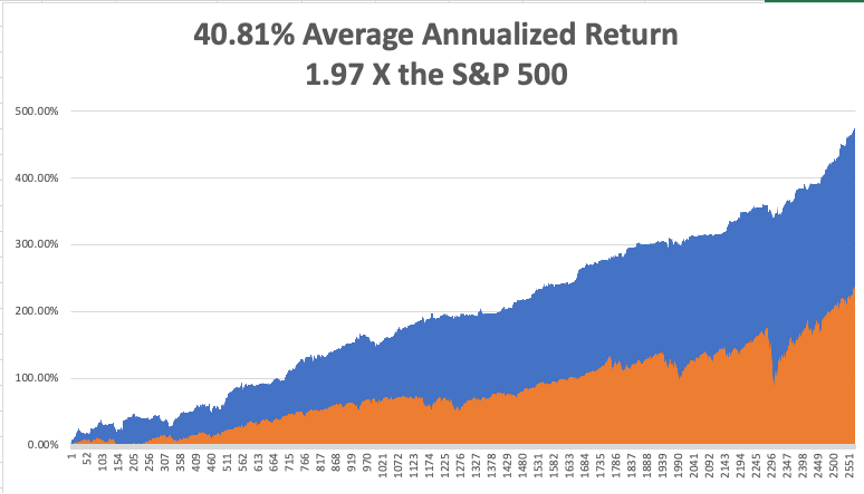

My 2021 year-to-date performance soared to 51.26%. The Dow Average is up 12.9% so far in 2021.

That brings my 11-year total return to 473.81%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 40.81%, the highest in the industry.

My trailing one-year return exploded to positively eye-popping 129.19%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives. Every time I think these numbers can’t be topped, they increase by another 10% during the following two weeks.

We need to keep an eye on the number of US Corona virus cases at 31.6 million and deaths topping 567,000, which you can find here.

The coming week will be dull on the data front.

On Monday, April 19 at 11:00 AM, earnings for (IBM), Coka-Cola (KO), and United Airlines (UAL) are released.

On Tuesday, April 20, at 4:30 PM, API Crude Stocks are published. We also get earnings for Johnson & John (JNJ) and Netflix (NFLX).

On Wednesday, April 21 at 1:00 PM, there is a big 20-year US Treasury bond auction. Chipotle (CMG) and Verizon (VZ) earnings are out.

On Thursday, April 22 at 8:30 AM, the Weekly Jobless Claims are printed. At 10:00 AM Existing Home Sales for March are announced. Snap (SNAP) and Intel (INTC) announce earnings.

On Friday, April 23 at 10:00 AM, we get the New Home Sales for March. American Express (AXP) and Honeywell (HON) release earnings. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, someone commented that I walk kind of funny the other day, and the memories flooded back.

In 1975, The Economist magazine in London heard rumors that a large part of the population was getting slaughtered in Cambodia. We expected this to happen after the fall of Vietnam, but not in the Land of the Khmers. So my editor, Peter Martin, sent me to check it out.

Hooking up with a right-wing guerrilla group financed by the CIA was the easy part. Humping 100 miles in 100-degree heat wasn’t.

We eventually came to a large village that was completely deserted. Then my guide said, “Over here.” He took me to a nearby cave containing the bodies of over 1,000 women, children, and old men that had been there for months.

I’ll never forget that smell.

With the evidence and plenty of pictures in hand, we started the trek back. Suddenly, there was a large explosion and the man 20 yards in front of me disappeared. He had stepped on a land mine. Then the machine-gun fire opened up. It was an ambush.

I picked up an M-16 to return fire, but it was bent, bloody, and unusable. I picked up a second rifle and fired until it was empty. Then everything suddenly went black.

I woke up days chained to a palm tree, covered in shrapnel wounds, a prisoner of the Khmer Rouge. Maggots infested my wounds, but I remembered from my Tropical Diseases class at UCLA that I should leave them alone because they only ate dead flesh and would prevent gang green. That class saved my life. Good thing I got an “A”.

I was given a bowl of rice a day to eat, which I had to gum because it was full of small pebbles and might break my teeth. Farmers loaded their crops with these so the greater weight could increase their income. I spent my time pulling shrapnel out of my legs with a crude pair of plyers.

Two weeks later, the American who set up the trip for me showed up with cases of claymore mines, rifles, ammunition, and antibiotics. My chains we cut and I began the long walk back to Thailand.

It’s nice to learn your true value.

Back in Bangkok, I saw a doctor who attended to the 50 caliber bullet that grazed my right hip. It was too old to sew up so he decided to clean it instead. “This won’t hurt a bit,” he said as he poured in hydrogen peroxide and scrubbed it with a stiff plastic brush.

It was the greatest pain of my life. Tears rolled down my face.

But you know what? The Economist got their story and the world found out about the Great Cambodian Genocide, where 3 million died. There is a museum in Phnom Penh devoted to it today.

So, if you want to know why I walk funny, be prepared for a long story. I still set off metal detectors.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

April 16, 2021

Fiat Lux

Featured Trade:

(SHOULD I BUY COINBASE TODAY?)

(COIN), (CRM), (ADBE), (PYPL), (SQ)

For all the cryptocurrency haters in the world, it’s getting harder to take that stand.

I’ll tell you why.

Coinbase (COIN) was the first major crypto business to go public in the U.S. when it began trading at $381 Wednesday morning on the Nasdaq and its IPO symbolizes the acceptance of an alternative digital asset class in technology.

Prior to this watershed moment, the only way to play crypto was through second derivatives plays like PayPal (PYPL) and Square (SQ) who have been handsomely rewarded through higher share prices.

Now, we get the biggest U.S. cryptocurrency exchange trading publicly that will allow exposure to mainstream stock-market investors.

The event has also been tabbed as a catalyst that might drive the adoption of incremental digital assets.

At the very least, this lays down a marker for further crypto-related companies eyeing the Nasdaq after Coinbase’s blowout success.

This also shows that the cryptocurrency infrastructure is developing rapidly and its budding credibility is something that needs to be acknowledged.

The Coinbase IPO was also the catalyst in sending bitcoin prices to almost $65,000.

No doubt that the appreciating asset has been the most attractive use case for the incremental investor and cryptocurrency buyer.

Many early investors who got into bitcoin at 20 cents are now billionaires many times over.

After such stunning success, it’s hard to believe that any fintech or cryptocurrency start-up would ever consider doing their IPO anywhere else but New York.

New York has the liquidity, the US dollar, and the capacity to receive such type of growth companies in bulk.

This is not only an emphatic victory for digital assets, but also for the US tech sector and a stamp of validation for the Nasdaq market.

Ironically enough, even during this trade war, Chinese tech companies are clamoring to go public in New York and not mainland China for the above reasons.

Here are a few other highly positive data points to digest that were talking points in their S-1 filing.

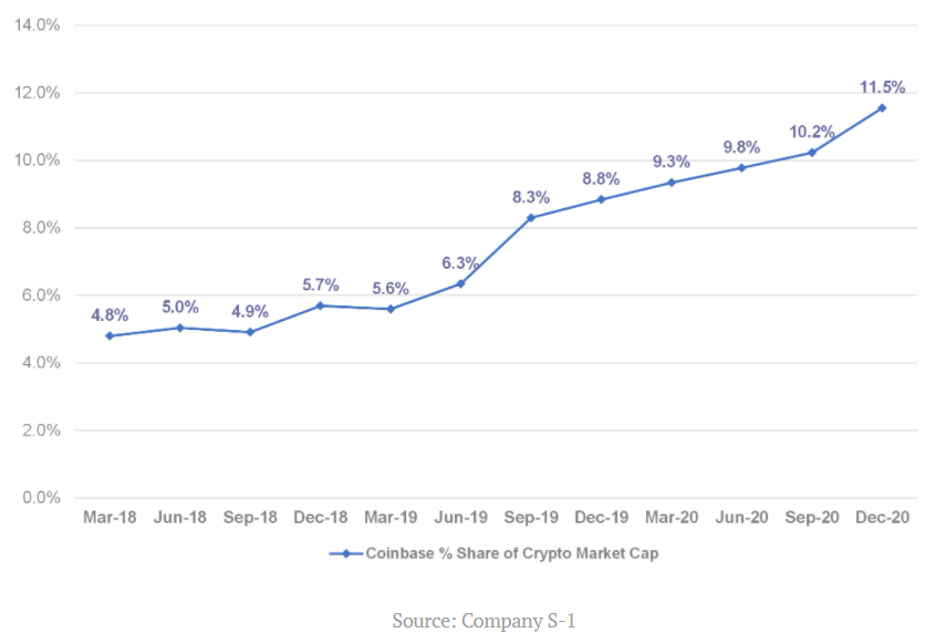

The overall market capitalization of crypto assets grew from less than $500 million to $782 billion between December 31, 2012, and December 31, 2020, representing a CAGR (compound annual growth rate) of over 150%.

Over the same period, Coinbase retail users grew from less than 13,000 to 43 million, a 175% CAGR.

I believe the total market cap of crypto is now around $2 trillion in April 2021.

And more recently, Coinbase has experienced significant growth in the number of institutions on their platform, increasing from over 1,000 as of December 31, 2017, to 7,000 as of December 31, 2020.

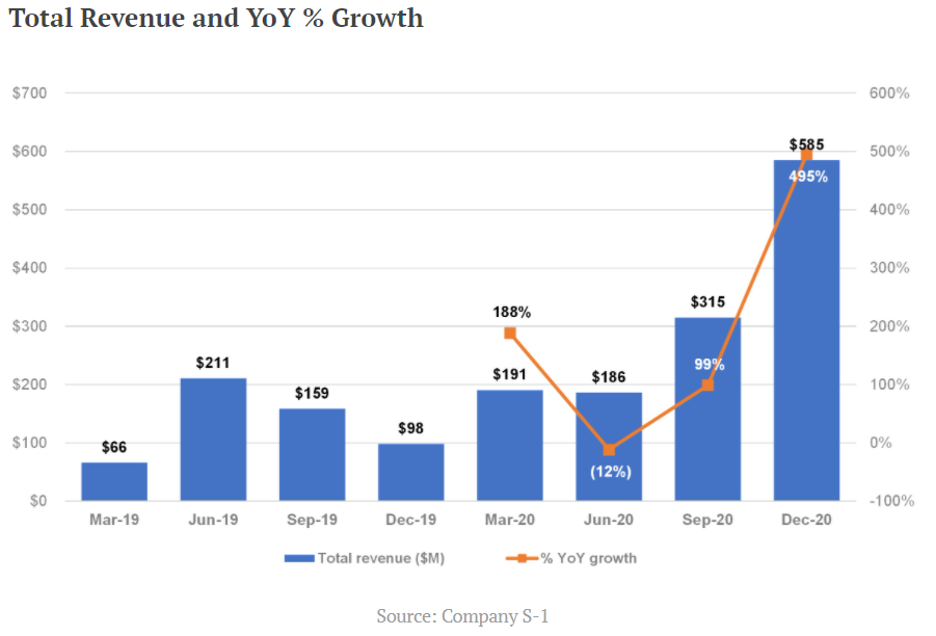

Bitcoin reported a nine-fold increase in Q1 revenue, to $1.8B, up from $190.6M the previous year.

Just like Google and Facebook benefit from a duopoly, Coinbase will benefit from being the only pure cryptocurrency option on the Nasdaq and that will put a floor under shares in the short-term.

The growth metrics of the company are also robust via a helping hand by the increasingly expensive price of bitcoin.

No doubt that this company’s prospects are tied to the hip with the prices of cryptocurrencies.

If the price of bitcoin retraces to $30,000, which it could because of the high volatility of it, expect Coinbase shares to dive with it.

This for all intents and purposes is a bet on the health and price trajectory of bitcoin for better or worse until other crypto-based choices are introduced which would give more layers and complexity to this sub-sector.

Bitcoin calls out Binance which they state as a competitor and Kraken is another exchange that is large and vying for the same capital.

I believe these two companies have a chance to go public and that is when you will really see the institutions jump on this crypto bandwagon.

More options and a foundational investment base will also promote stability in this new technology sub-sector.

Should you buy Coinbase today?

No.

I understand Coinbase’s growth metrics are off the charts with revenue growing 900%, but it’s not worth $100 billion market cap on just $1.8 billion of quarterly sales.

Investors would need solid tailwinds such as bitcoin passing $100,000 in 2021 for this company to be worth $100 billion and I just don’t see it.

Then also understand the cybersecurity and possible regulations are two risks that could blow up the business model at any moment which would take down the premium in the stock.

Yes, the meteoric rise of crypto at the start of 2021 has turned heads, but as the economy reopens, I do believe money will rotate from crypto back into traditional technology that is underpinned by cash cow businesses.

Highly profitable companies that aren’t FANGs are also set to deliver share appreciation to shareholders such as Salesforce (CRM) or a company like Adobe (ADBE) who earn profits of $5.27 billion on $13 billion of annual revenue.

I acknowledge that Coinbase’s IPO was the perfect time to go public.

They are taking advantage of easy money and low rates while the acceptance of this alternative asset class has never been higher.

However, I don’t see any more incremental growth in the short term and the stock is more than fully priced today.

The risk-reward is not favorable to pile into this stock now unless you have a bullish 50-year view on crypto and can’t wait.

This stock will go through volatility because of the inherent dynamics they are tied to and I would seriously look at buying Coinbase only on a massive sell-off.

Don’t go chasing unicorns.

At the end of the day, this is a real company with real revenue growth of 900% year-over-year. Slice it up anyway, and these numbers are numbers that attract investors, but the stock is too expensive right here.