Mad Hedge Technology Letter

December 6, 2021

Fiat Lux

Featured Trade:

(THE HAWKS ARE HERE)

(ROKU), (ZM), (TWLO), (SNAP), (SQ), (MSFT), (CRM), (ADBE)

Mad Hedge Technology Letter

December 6, 2021

Fiat Lux

Featured Trade:

(THE HAWKS ARE HERE)

(ROKU), (ZM), (TWLO), (SNAP), (SQ), (MSFT), (CRM), (ADBE)

Higher inflation is something this tech bull cycle hasn’t dealt with, and it’s starting to rear its ugly head in the form of volatility and spades of it.

The Fed will have to increase interest rates or face runaway inflation that will crash the economy, but increasing interest rates will also make lives harder for tech companies.

As we try to understand the pace of interest hikes, certain tech companies will fare much better in this inflationary environment than others. To deduce the winners from the losers, investors should understand exactly how inflation affects each particular tech company.

Talk has gone from the Fed moving early to raise short-term rates, to the Fed moving even in early spring which in turn is spooking risk markets from cryptocurrencies, the S&P, and the Nasdaq.

Fed Chair Jerome Fed has done a poor job communicating his sudden hawkish tone and the market has had to quickly reprice risk assets because of the surprising nature of the hawkishness.

In the short-term, tech stocks will need some time to digest this new expectation, which I see as quite healthy, but short-term tough to swallow.

Fed Cleveland President Loretta Mester told the media she is “very open” to scaling back the Fed’s asset purchases at a faster pace so it can raise interest rates a couple of times next year if needed so this isn’t just one guy in Powell trying to move the needle.

Clearly, the Fed is moving in unison, and they threaten to become a major force in moving markets which is all we care about.

All that pressure is causing component and labor costs to rise. Companies that don't have enough pricing power to pass those costs on to their customers will likely see their gross and operating margins shrink.

This matters because tech companies offer some of the most generous salaries in the U.S. and substantial increases in pay hurts them the most.

Higher interest rates attract more consumers and businesses to put more money in higher-yield bonds and savings accounts.

There are 3 ways that higher rates are actually a gut punch to tech growth companies.

First, they increase the costs of borrowing incremental capital to expand a business. In more cases than not, tech growth companies rely on borrowed money because their operation is not yet sustainably profitable. That's bad news for high-growth tech companies, which are burning cash with widening losses.

Second, it reduces the long-term estimates for a company's earnings and free cash flow (FCF) growth meaning their underlying stock price is rerated downwards in the anticipation of this new reality.

Loss accruing tech companies commonly suffer an exodus as their underlying shares are repriced to reflect higher costs.

Just this morning we saw Roku (ROKU), Zoom Video Communications (ZM), Snap (SNAP), Twilio (TWLO), Square (SQ) breach 52-week lows.

The breadth of the market has been hollowed and the goalposts have indeed narrowed because of the hawkish tone at the Fed.

Lastly, higher interest rates drive institutional money into fixed income.

They do this largely by taking profits from crypto, tech stocks, or moving their stash on the sidelines then resurfacing the money into “safer” assets that anticipate weakening bond yields at the longer end of the curve.

So I won’t sit here and say sell all and every tech stock, it’s more nuanced than that.

I executed one position in December and that was Microsoft (MSFT) and it got pulled down with the broader market.

More importantly, I didn’t bet the ranch.

Ultimately, we still bask in the ideology that the tech bull market isn’t over yet because it isn’t, but this aggressiveness out of the blue has forced the overall tech market to temporarily rest with growth tech suffering major drawdowns.

In doing that, the ceiling for a Santa Claus rally is somewhat capped to the upside.

The Fed could have waited until January.

Sure, there will still be winners in tech and the odds of these winners are driven firmly behind the biggest and best like Microsoft, Amazon, Google, and Apple.

These are the type of companies that have the pricing power to raise prices and get away with it because consumers will be willing to pay it.

Other potential winners include cloud service giants like Salesforce (CRM) and Adobe (ADBE). These again are top-quality software stocks that can pass up higher enterprise software costs to the firms that can pay for it.

It’s entirely possible that the Fed could end up walking back some of these aggressive stances in the interest-raising process next year.

Don’t fight the Fed and don’t expect tech growth stocks to reverse until we receive more clarity with interest rate policy, if a reverse is triggered, it will play out with Apple, Amazon, Google, and Facebook, and Microsoft leading the way higher.

“Your margin is my opportunity.” – Said Founder and CEO of Amazon Jeff Bezos

Global Market Comments

December 6, 2021

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT IS ON FOR DECEMBER 7-9) (MARKET OUTLOOK FOR THE WEEK AHEAD, or THE TRIPLE VIRUS ATTACK),

(SPY), (TLT), (BAC), (GS), (JPM), (VIX)

A collection of the 27 best traders and managers in the world, or eight a day, each giving an educational webinar. Back-to-back one-hour presentations are followed by an interactive Q&A. It’s a smorgasbord of trading strategies, so pick the one that is right for you. Covering all stocks, bonds, commodities, foreign exchange, precious metals, and real estate. It’s the best look at 2022’s money-making opportunities you will get anywhere. To view the schedule and speakers, and to register NOW, click here.

Those who were bemoaning the lack of market volatility certainly had their wishes fulfilled last week and then some. Volatility attacked the $30 level remorselessly like a hoard of barbarians. But it didn’t close there.

We actually got three Omicrons last week, the virus kind, the Fed kind, and the jobs variety, with the November Nonfarm Payroll report coming in at a paltry 210,000. Yet, the Headline unemployment rate cratered to a new post-pandemic low, from 4.6% to 4.2%. Go figure.

The Fed’s move amounts to a sudden dramatic lean towards a hawkish stance. The word “transitory” has hopefully been banished from the Fed lexicon for good.

The final flush on Friday no doubt cleansed the market like a colonoscopy, vaporizing any bad positions from yearend reports. That’s why the reopening stocks like hotels, cruise lines, airlines, and casinos were sold down so hard and bounced back with equal vigor.

Last week’s violence cleared the way for the yearend rally to continue, with the final destination a close at the year’s top tic all-time high.

Of course, everyone knows interest rates are rising except the bond market, where prices seemed to magically levitate, keeping interest rates low. Rumors of hedge funds covering shorts to bury losses abound. This is the trade that everyone universally got wrong.

I think the incredible move on Friday was due to hedge funds stampeding to cover money-losing short positions ahead of embarrassing yearend reports.

From here on, trading should get easier as the smarter money departs for Hawaii, the Caribbean, Aspen, or in this case Lake Tahoe, where the pristine waters and ski slopes beckon. Volume and volatility should bleed out from here.

I’m sticking with my long tech, long financials, and short bond strategy until payday, which should be soon.

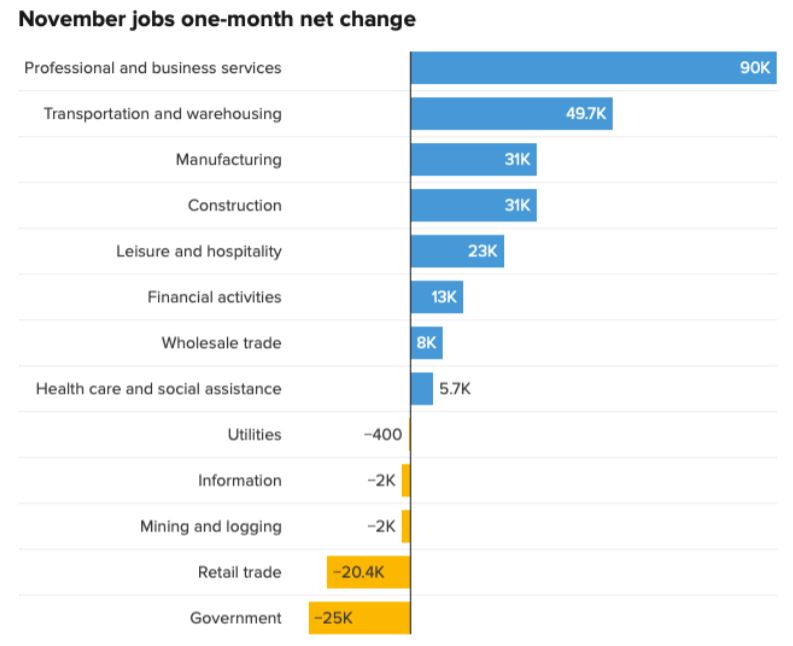

The Nonfarm Payroll Report Disappoints in November, coming in at 210,000. Over 600,000 was expected. The Headline Unemployment Rate fell to 4.2%, a new post pandemic low. There was a lot of confusing and contradictory data this month. Professional & Business Services added 90,000, Couriers & Messengers 26,800, and Leisure & Hospitality 23,000. But total Employment added 1.1 million. Government lost 25,000 jobs.

How Real is Omicron? On Friday, the market viewed it as a delta variant 2.0. I don’t think so. If anything, it shows how effective the global early response system has become to new variants. South Africa caught omicron with only a handful of cases and the borders started closing immediately. There is no indication that Omicron can’t be stopped by vaccination. It will only kill the anti-vaxers. It means we’re safer, not more at risk, and the economic recovery and the bull market should continue.

Oil Plunges Down 13% in a Day, breaking $70, as fears of a new variant-caused recession run rampant. It was a “sell everything” selloff.

Biden Says No Travel Restrictions or Lockdowns, in response to the new Covid Omicron variant. Therefore, no negative response for the stock market. It was worth a 350-point rally yesterday.

Pending Home Sales Soar by 7.5% in October. The Midwest showed the strongest sales, reflecting a mass migration to cheaper homes from the coasts.

ADP Comes in Red Hot at 534,000. Services dominated and Leisure & Hospitality picked up a massive 136,000. Large companies led the hiring binge. It augers well for the Friday Nonfarm Payroll Report.

More Taper Sooner was the bottom line on Powell’s comments last week. The Fed governor said in testimony in front of the Senate Banking Committee that inflation is no longer “transitory”, implying that hotter inflation numbers are to come. Yikes! Finally, a nod to reality! Stocks tanked 600 points on the comment. Bonds should crash but strangely are holding up. Watch this space. The news could give us a tradable bottom for all asset classes.

ISM Manufacturing Improves, from 60.8 to 61.1 in November. It’s more proof that the economy is expanding.

Weekly Jobless Claims Still Hot at 222,000, and continuing claims fell below 2 million, a new post-pandemic low. No recession here.

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With the pandemic-driven meltdown on Friday, my December month-to-date performance plunged to -4.58%. My 2021 year-to-date performance took a haircut to 72.18%. The Dow Average is up 13.00% so far in 2021.

I used the collapse in interest rates to add a 20% position in financial stocks, Goldman Sachs (GS), and Bank of America (BAC). I got hammered with my existing short in bonds, with the ten-year yield plunging to an eye-popping 1.37%.

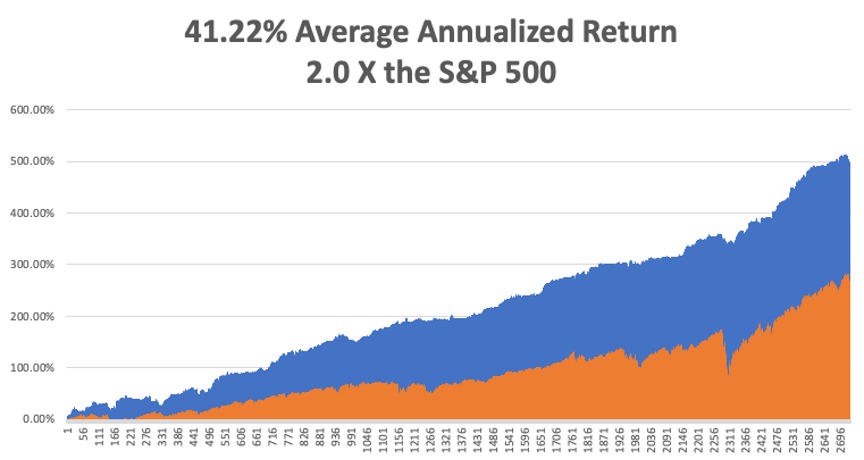

That brings my 12-year total return to 494.73%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 41.22% easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 49 million and rising quickly and deaths topping 788,000, which you can find here.

The coming week will be all about the inflation numbers.

On Monday, December 6, nothing of note takes place as we move into the yearend slowdown.

On Tuesday, December 7 at 5:30 AM EST, the US Balance of Trade is released for October. We will remember Pearl Harbor Day when the US Navy lost 3,000 men.

On Wednesday, December 8 at 5:15 AM, the JOLTS Job Openings for October are published.

On Thursday, December 9 at 8:30 AM, the Weekly Jobless Claims are disclosed.

On Friday, December 10 at 5:30 AM EST the US Inflation Rate for November is printed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, occasionally I tell close friends that I hitchhiked across the Sahara Desert alone when I was 16 and am met with looks that are amazed, befuddled, and disbelieving, but I actually did it in the summer of 1968.

I had spent two months hitchhiking from a hospital in Sweden all the way to my ancestral roots in Monreale, Sicily, the home of my Italian grandfather. My next goal was to visit my Uncle Charles, who was stationed at the Torreon Air Force base outside of Madrid, Spain.

I looked at my Michelin map of the Mediterranean and quickly realized that it would be much quicker to cut across North Africa than hitching all the way back up the length of Italy, cutting across the Cote d’Azur, where no one ever picked up hitchhikers, then all the way down to Madrid, where the people were too poor to own cars.

So one fine morning found me taking deck passage on a ferry from Palermo to Tunis. From here on, my memory is hazy and I remember only a few flashbacks.

Ever the historian, even at age 16, I made straight for the Carthaginian ruins where the Romans allegedly salted the earth to prevent any recovery of a country they had just wasted. Some 2,000 years later, it worked as there was nothing left but an endless sea of scattered rocks.

At night, I laid out my sleeping bag to catch some shut-eye. But at 2:00 AM, someone tried to bash my head in with a rock. I scared them off but haven’t had a decent night of sleep since.

The next day, I made for the spectacular Roman ruins at Leptus Magna on the Libyan coast. But Muamar Khadafi pulled off a coup d’état earlier and closed the border to all Americans. My visa obtained in Rome from King Idris was useless.

I used to opportunity to hitchhike over Kasserine Pass into Algeria, where my uncle served under General Patton in WWII. US forces suffered an ignominious defeat until General Patton took over the army 1n 1943. Some 25 years later, the scenery was still littered with blown-up tanks, destroyed trucks, and crashed Messerschmitt’s.

Approaching the coastal road, I started jumping trains headed west. While officially the Algerian Civil War ended in 1962, in fact, it was still going on in 1968. We passed derailed trains and smashed bridges. The cattle were starving. There was no food anywhere.

At night, Arab families invited me to stay over in their mud brick homes as I always traveled with a big American Flag on my pack. Their hospitality was endless, and they shared what little food they had.

As a train pulled into Algiers, a conductor caught me without a ticket. So, the railway police arrested me and on arrival took me to the central Algiers prison, not a very nice place. After the police left, the head of the prison took me to a back door, opened it, smiled, and said “si vou plais”. That was all the French I ever needed to know. I quickly disappeared into the Algiers souk.

As we approached the Moroccan border, I saw trains of camels 1,000 animals long, rhythmically swaying back and forth with their cargoes of spices from central Africa. These don’t exist anymore, replaced by modern trucks.

Out in the middle of nowhere, bullets started flying through the passenger cars splintering wood. I poked my Kodak Instamatic out the window in between volleys of shots and snapped a few pictures.

The train juddered to a halt and robbers boarded. They shook down the passengers, seizing whatever silver jewelry and bolts of cloth they could find.

When they came to me, they just laughed and moved on. As a ragged backpacker I had nothing of interest for them.

The train ended up in Marrakesh on the edge of the Sahara and the final destination of the camel trains. It was like visiting the Arabian nights. The main Jemaa el-Fna square was amazing, with masses of crafts for sale, magicians, snake charmers, and men breathing fire.

Next stop was Tangiers, site of the oldest foreign American embassy, which is now open to tourists. For 50 cents a night, you could sleep on a rooftop under the stars and pass the pipe with fellow travelers which contained something called hashish.

One more ferry ride and I was at the British naval base at the Rock of Gibraltar and then on a train for Madrid. I made it to the Torreon base main gate where a very surprised master sergeant picked up half-starved, rail-thin, filthy nephew and took me home. Later, Uncle Charles said I slept for three days straight. Since I had lice, Charles shaved my head when I was asleep. I fit right in with the other airmen.

I woke up with a fever, so Charles took me to the base clinic. They never figured out what I had. Maybe it was exhaustion, maybe it was prolonged starvation. Perhaps it was something African. Possibly, it was all one long dream.

Afterwards, my uncle took for to the base commissary where I enjoyed my first cheeseburger, French fries, and chocolate shake in many months. It was the best meal of my life and the only cure I really needed.

I have pictures of all this which are sitting in a box somewhere in my basement. The Michelin map sits in a giant case of old, used maps that I have been collecting for 60 years.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Mediterranean in 1968

Mad Hedge Technology Letter

December 3, 2021

Fiat Lux

Featured Trade:

(THE ULTIMATE TECH SUPPLY CHAIN SHOCK)

(TSLA), (CMOC), (AAPL), (DRC)

China is monopolizing the raw materials industry in Africa at such a fast pace that it might be a thorn in the side of American EV makers like Tesla and other US tech companies soon.

Tesla (TSLA) has decided to veer its business interests and kowtow to China and is really doubling down there with a Shanghai Gigafactory which now produces more cars than its plant in California.

Under the hood, most of the material is Chinese-made, and the minerals that power the batteries are largely refined and mined by Chinese companies.

As the world adopts EVs, companies are desperate to secure and strengthen their positions in the battery supply chain, from mineral extraction and processing to battery and EV manufacturing.

Vertical integration is more fashionable than ever, where one company controls a number of steps along the supply chain to guarantee supply.

This is not surprising since the supply chain breakdown has forced many companies to stop production for lack of parts.

This battery arms race is being won by China.

China is the world’s biggest market for EVs with global sales of 1.3m vehicles in 2020, more than 40% of sales worldwide.

Chinese battery-maker CATL has cornered about 35% of the world’s EV battery market.

Chinese refineries supplied 85% of the world’s battery-ready cobalt last year; a mineral that helps the stability of lithium-ion batteries.

Democratic Republic of the Congo (DRC) is where most of the cobalt is found, where almost 70% of the mining sector is dominated by Chinese companies.

Meander around DRC’s southern copper and cobalt mining belt, and it looks as if you are in China.

In August, China Molybdenum Company (CMOC), a giant Chinese mining firm, announced an investment of $2.5bn to triple copper and cobalt production at its Tenke Fungurume Mine, already one of the largest in DRC.

That followed its purchase of a 95% stake in nearby Kisanfu copper and cobalt mine for $550m.

Fellow Chinese corporate giant, Huayou Cobalt has a stake in at least three copper-cobalt mines in DRC and dominates at every step of the cobalt supply chain, from mines to refineries to battery precursor and cathode production.

Some car and battery manufacturers are beginning to reduce the amount of cobalt in their batteries to de-risk themselves from China.

Nickel-rich batteries could be a solution, but the same Chinese companies that dominate cobalt mining in DRC, Huayou Cobalt and CMOC, are also cornering nickel extraction and processing in Indonesia, which has the world’s largest nickel reserves at 72m tons.

This means China is now the largest global market producer of nickel, far surpassing the efforts of Europe and the US.

In Europe too, companies are beginning to gain on China’s lead. By the end of the decade, the continent is expected to have 28 factories producing lithium-ion cells, with production capacity due to increase by 1440% from 2020 levels.

That growth is being driven by companies such as Britishvolt in Northumberland and Sweden’s Northvolt, as well as Asian firms expanding production into Europe.

European investment in mining and the production of battery and cathode materials is not keeping pace.

China is creating the equivalent of one battery Gigafactory a week compared with one every four months in the US.

A new global lithium-ion economy is being developed, and the United States lagging Europe and China means they will need to pay a premium for the raw materials in the future.

It’s almost as if the U.S. is going through a round 2 of outsourcing their rust belt manufacturing, but this time it’s Internet 3.0 manufacturing.

The U.S. has fallen asleep at the wheel and allowed China to coax itself into relevancy by undercutting global competitors, the same is happening in the raw material industry that is fundamental to the survival of the United States tech and EV prowess.

The quickness and potency of a mercantilist one-party state can be felt here as many broader issues are bogged down in the U.S. in Congress and get stuck there in perpetuity.

When allowed to flourish, US capitalism is the most mesmerizing force in global economics, but it is also prone to stumbling over itself.

Policymakers need to reroute their energies to the raw material precious metal sector to make pricing competitive for the American consumers, or the share prices of US tech companies will be hurt.

Like the supply bottlenecks caused pain for many American companies, companies like Apple (AAPL) or Dell might not be able to build smartphones and laptops without the right raw materials.

Tesla might not be able to build a car anymore without bowing down to the Chinese forces.

Don’t be surprised in a few years if tech companies need to halt production due to China not selling certain parts to certain countries, this could be the next battleground between the United States and China.

“Inadvertent creation of a micro black hole, or some as-yet-unknown technology could spell the end of us.” – Said Founder and CEO of Tesla Elon Musk

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more