Global Market Comments

October 7, 2022

Fiat Lux

Featured Trade:

(OCTOBER 5 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TSLA), (PLTR), (UUP), (ROM), (USO), (ARKK), (ROKU)

Global Market Comments

October 7, 2022

Fiat Lux

Featured Trade:

(OCTOBER 5 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TSLA), (PLTR), (UUP), (ROM), (USO), (ARKK), (ROKU)

Below please find subscribers’ Q&A for the October 5 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: Is the final low in, or could we retest yet again (SPY)?

A: We could retest yet again, but it’s very important to notice that the marginal new lows are very small. The low we had on Friday, the last day of September and Q3, was only 800 points lower than the low we had in June—you had to work 4 months just to get a new low of only 800 points. So I think that's the way it's going to go. If we do get new lows, it’ll be incremental new lows—we’re not crashing to 3,000 or anything like that.

Q: What do you think Tesla (TSLA) will bottom at in the short term?

A: $200 or $210. The Tesla deal is a disaster for Elon Musk. It will amount to a huge diversion of management time; he’s going to be facing regulatory hurdles, and even though he said we’re going ahead for the deal, a lot of people still don’t believe it because the financing for the deal may have vaporized in the massive increase in interest rates that has occurred since February. So, there are still a lot of non-believers in this deal. I’d rather have him making solar panels, electric cars and launching rockets, not getting into the social media morass and taking over a broken company. The shareholders clearly don’t like it either, taking the shares down $30 in two days. By the way, if you look at the charts, you notice that people were front-running the Twitter deal by dumping Tesla stock the day before. So yes, it kind of peed on our Tesla parade for the short term; long term it keeps going up and the bad news is in the price.

Q: How do we get the concierge service?

A: Just contact customer support at support@madhedgefundtrader.com or call (347) 480-1034.

Q: Have you revised Tesla’s (TSLA) price target?

A: No, not the long-term ones, just the short-term ones.

Q: Is it possible that bonds are bottoming here, even if we expect further Fed rate rises?

A: Yes, the Fed only has control of overnight rates, and those are rising. In fact, overnight rates are now higher than 10-year rates, and could go much higher still—that's called inversion of the yield curve. We’re almost certainly getting another 150-basis point rise in overnight rates. 10-year bonds or 20-year bonds could well stay around this level, or maybe just a little bit lower. So yes, the bond short is gone. It worked great for us for 2.5 years, we caught a 43% decline in the TLT, but it’s game over. Time to find other trades, like buying stocks.

Q: Does Elon Musk have to sell more Tesla to buy more Twitter?

A: That is the big question being asked today because he already sold $16 billion worth of stock in Tesla to cover the Twitter purchase this year. With the debt markets having fundamentally changed in the last 6 months, the question is: does he have to raise more equity (i.e. sell more Tesla), or can he bring in other equity investors? Hopefully, if he does have to sell more Tesla, it’s not very much—it’s a $44 billion deal and he’s already put $16 billion into it, so maybe he raises another $6 billion to get up to a 50% control level, which the market can easily handle in a day or two. He’s handled all of his past Tesla share sales fairly easily, and he tends to do these at market tops when demand for the shares is overwhelming. Longer term, the much greater demand for selling Tesla shares will come from the equity raises he will need to do to build another six Tesla factories around the world. That could be anywhere from $400 billion to $800 billion, so that will be the much larger cash call, but those are years off at best.

Q: With so many big techs breaking down, how should we play the (ROM) (ProShares Ultra Technology ETF)?

A: From the long side is how you play it. But you really need these capitulation days, especially if you’re involved in 2X ETFs. There is a spectacular play setting up for the (ROM) because it’ll go from $24 (or whatever the final bottom is) to $100 in the next upcycle, so that is a great leverage play that you really want to get involved in.

Q: If I don’t have time to babysit my portfolio, am I better in LEAPS or physical stocks?

A: Well the LEAPS I’m putting out now have a 2 years 4 months expiration date, so you can literally just buy them and forget about them. On the other hand, if we don’t get an economic recovery in 2 years and 4 months, you’re better off buying stocks outright on 2:1 margin. You make less profit, but if we don’t get a recovery for 3, 4, 5 years, then you have no expiration problem with stocks, as opposed to with LEAPS. Now, there are ways to trade around your LEAPS, like financing the long and by shorting puts and getting in for zero, but that requires smaller positions because you have to maintain the margin for the short put side. So, if you want to play it safe, buy the stocks. You can even handle a lost decade with stocks, especially if their dividend pays. With LEAPS, you need a fairly immediate economic recovery, which we should get, especially if the Fed lowers interest rates next year, which it should.

Q: What is your view on the US dollar (UUP)?

A: The dollar seems close to peaking right around here. It will peak on the last day that the Fed raises interest rates, which could be on December 14th. In fact, they may not even wait until then. Depending on the inflation rate, they could only do a quarter or a half-point rate rise in December, thus giving the market their signal that way. Or not do it at all, and the sudden selloff that we had in the dollar, and the stabilization of bonds we had last week is telling you that’s on the table as a possibility. So, we saw really important moves for long-term trend considerations in the markets since last week.

Q: Time for Palantir (PLTR)?

A: No, because the CEO doesn’t give a damn about his stock, and the stock reacts accordingly. I gave up on Palantir for that reason.

Q: How do you see the Ukraine/Russia situation developing?

A: It drags on for another year, Russia keeps losing and throwing men into the meat grinder until Putin gets removed, which should happen next year at which point oil prices collapse. That may be why he blew up the Nordstream One pipeline, to tie the hands of a future Russian government.

Q: Is it safe to buy 30-day Treasury bills in November going into the next F1C meeting?

A: Yes, because they essentially have no risk—that’s basically a cash type investment. And if your broker goes bust you can just force them to hand over your Treasury bonds and not get tied up in any three-year bankruptcy proceeding. It’s an asset, not cash.

Q: Will it be time to buy LEAPS on the next market selloff?

A: Absolutely, yes.

Q: Do you believe Putin would use nukes?

A: No I don’t, because the radioactive cloud would fall back on him immediately. There are very few people who are both stock market experts and nuclear weapons experts; I happen to be one of those—probably the only one in the world in fact—because of my time spent with the atomic energy commission at the Nuclear Test Site in Nevada. The problem with bombing your next-door neighbor with nukes is that the nuclear fallout comes right back on you the next day. Most of Russia’s nukes don’t even work, they only have a handful that actually does, and if he does use one, I bet it would be a tiny one just to demonstrate that he has a working nuke—like just a one-megaton one as opposed to Hiroshima which was 20 kilotons. Or he could drop it in the Black Sea or do an above-ground test at their old nuclear test site that wouldn’t kill anyone, just to show that he has working nukes. I don’t think he will, because we would react in kind in twice the size.

Q: Time to buy ARK Innovation ETF (ARKK)?

A: You might start with a small starter position, just to get it into your portfolio so you remember to buy it on the next dip. Cathy Woods’s leverage in this fund is tremendous. You really want to own it at a market bottom, but picking the actual bottom is going to be tough. One way to achieve this is to just go out and buy Tesla—that way you don’t have to pay the management fee—or buy the top 5 holdings in ARK directly, which includes Roku (ROKU) among others. So yes, I’m watching it; I prefer buying things on the way up and missing the first 10% than to catch a falling knife, and boy has this thing been a falling knife this year.

Q: Do you like biotech here?

A: Absolutely; please subscribe to the Mad Hedge Biotech Letter for biotech recommendations plus LEAPS on biotech plays by clicking here.

Q: Energy is still the best sector now?

A: Yes, but for how long? You don’t want to be left standing when the music stops playing, and that is imminent in the oil industry. It will be illegal to sell gasoline cars in California after 2035, and gas makes up half the oil use in the US.

Q: Did you know that oil reserves (USO) are the lowest since 1984?

A: Yes, I think you may have read that in my newsletter, and that’s because of Biden’s efforts to reduce US gasoline prices through a million barrel per day release from the strategic petroleum reserves in Texas and Louisiana. If we are a net energy producer, why do we even have reserves? It’s an out-of-date holdover from the Cold War.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Tokyo 1975

Mad Hedge Biotech and Healthcare Letter

October 6, 2022

Fiat Lux

Featured Trade:

(A SOLID BIOTECH THAT CAN SURVIVE THE CRASH)

(GILD)

In years filled with virtually never-ending market volatility fears, the third quarter of 2022 seems to be one for the books.

We’ve gone through wild currency fluctuation, with the British pound practically free-falling to a record low against the US dollar.

The US Treasury yields rose to their peak since April 2011, while the S&P 500 is going into its third-consecutive quarter marked with losses for the first time since we experienced the 2008 financial crisis.

On top of these, the Federal Reserve disclosed that rates would climb even higher than expected as the previous month’s inflation data came in scorching.

The situation across the globe isn’t exactly showing any indications of improvement. Sanctions on Russia are becoming more severe following the Kremlin’s decision to annex certain areas of Ukraine formally. Meanwhile, emerging markets look to be down in the dumps as well.

Amid the market turmoil, some stocks managed to weather the storm and still hold the potential to deliver good results.

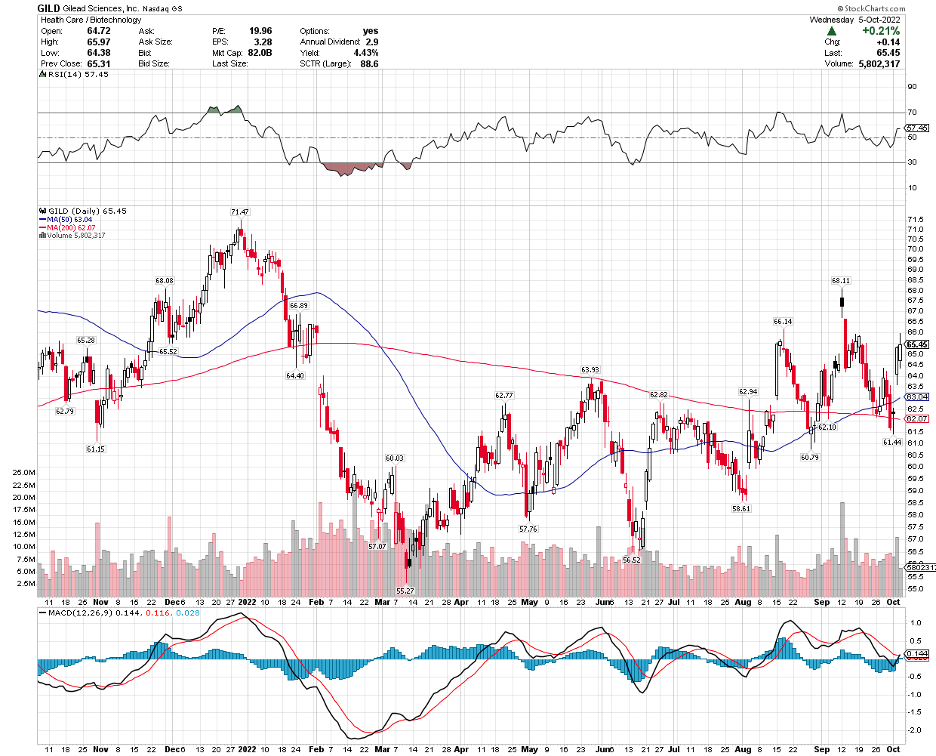

One of them is Gilead Sciences (GILD).

Gilead rose to fame when it launched an effective treatment for HCV, which came after its excellently timed (or lucky) acquisition of Pharmasset for $11 billion. This created a massive boost to the company’s business, with shares peaking at more than $100 per share in 2015.

With HCV finally having a solution, the boom did not last. Obviously, sales from the drug were not recurring since the patients were already getting cured.

At that time, Gilead bolstered its pipeline with a flourishing HIV business. However, the company’s revenues and earnings eventually became flat.

In the meantime, Gilead went after more expensive deals, including a $21 billion acquisition of Immunomedics to gain access to Trodelvy, a $12 billion contract with Kite Pharma to get their hands on Yescarta, and multi-billion deals involving Forty-Seven and Galapagos. Unfortunately, none of them delivered the same pay-off as the Pharmasset deal.

However, Gilead has been gaining traction recently.

Wall Street has been desperately looking for businesses that could help investors regain their losses, and it looks like Gilead is part of the very short list of companies that made the cut.

While it hasn’t exactly done anything groundbreaking as of late, the company’s consistency and foreseeable growth are boosting its attractiveness to investors.

Right now, Gilead’s HIV franchise is singlehandedly supporting the entire market cap of the stock. That’s impressive and promising, considering the company also has a burgeoning oncology sector.

For context, Gilead’s oncology franchise is estimated to hit roughly $5 billion in sales by 2030.

Meanwhile, Gilead has another HIV blockbuster making waves in Lenacapavir. Earlier in 2022, the company managed to expand the covered distribution channels of this HIV treatment and gained marketing authorization in the EU.

Given the current performance of its HIV franchise and the promise of expansion for Lenacapavir, this particular segment can be conservatively estimated to report at least single-digit growth through the early 2030s.

Overall, Gilead has been recording solid results for this year. In the first quarter, sales climbed 3% to $6.6 billion, partly thanks to its Veklury sales and the gaining momentum of its cell therapy business.

While growth was not as impressive, the 10% earnings yield, stability, and, of course, 5% dividend yield make Gilead a compelling choice. Admittedly, we’ve witnessed how interest rates climb higher, which results in additional competition for the 5% dividend yield, but the company appears to be holding up nicely in this aspect.

Gilead’s apparent independence from its COVID-centered product shows a highly encouraging trend. In August, Gilead shared its second quarter report showing revenues rising 1% to $6.3 billion. The “positive” note is that Veklury, a COVID-19 treatment, fell 46% while other products jumped 7% to contribute $5.7 billion.

Riding this momentum, Gilead shared another bolt-on deal worth $405 million to acquire MiroBio, a biotechnology company based in the UK. MiroBio develops treatments that aim to restore immune balance.

In summary, Gilead remains a solid bet in these trying times. It has established programs, which are expected to rake in higher earnings in the years to come, and an ability to execute great deals to bolster its pipeline—all while keeping its debts and costs well under control. I suggest you buy the dip.

Mad Hedge Bitcoin Letter

October 6, 2022

Fiat Lux

Featured Trade:

(MAX OUT CRYPTO)

(BTC), (MAXI)

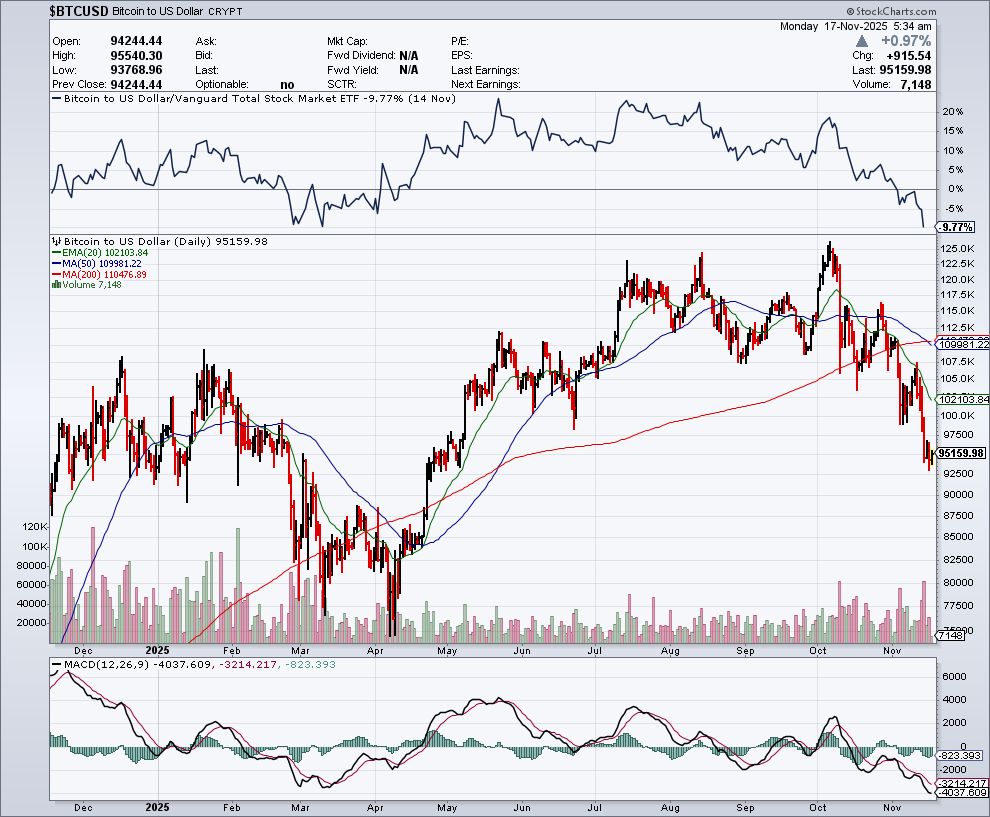

One of the big knocks on the digital gold or crypto is that it doesn’t generate some type of annuity-like payment.

That’s right, it doesn’t.

It’s not like a rental property that pumps out dollars every month.

That honestly turns off a lot of people.

I get it.

Getting those Benjamins to fill pockets for investors is a comforting feeling.

Instead, crypto holders are rewarded by the appreciation of the asset itself.

Speculative investors must wait for the price of crypto to elevate and sometimes it doesn’t so investors can’t cash out.

For the first time in the history of crypto products, the ETF Simplify Bitcoin Strategy PLUS Income ETF (MAXI) is designed to solve that challenge.

It combines investments in the bellwether coin crypto bitcoin with derivative-based income-producing products.

The Simplify Bitcoin Strategy PLUS Income ETF (MAXI US) is listed on Nasdaq with an expense ratio of about 1.00%.

The fund’s options sleeve is actively managed and consists of opportunistically selling short-dated put or call spreads on the most liquid global equity indices.

The management of MAXI described the portion of income-generating opportunities as “padding.”

However, that doesn’t adequately describe the large risk of what they are actually doing.

They are talking about this ETF as if the “income” is almost guaranteed.

But the risk here is that selling option calls and puts can be extremely loss-making and they fail to disclose that to investors.

This type of Frankenstein investment is definitely an interesting spin on crypto products by combining a derivative portion to the speculative crypto part.

There are many moving parts to this and due diligence is necessary.

In addition to the high risk, the management fee is a big turn-off.

The fee is to basically fund the operation, but it’s no guarantee that the derivative portion of the portfolio will be successful.

They claim they will generate income by writing short-dated option spreads on the “most liquid global equity indices,” yet as of 2025 the portfolio is still dominated by exposure to the iShares Bitcoin Trust (IBIT), along with a small sleeve of listed call options and index-based spreads.

The opaqueness doesn’t sit well with me and it shouldn’t with you.

The prospectus explains that the “options overlay strategy will invest up to 20% of fund’s assets,” which remains true in current filings.

Therefore, it could either be 0 or 20% of the ETF capital exposed to complete losses because the traders bet on the wrong short-dated strategy.

Essentially, investors have no idea what they are investing in.

What if there are no “income generating” profits and they are all losses?

Surely, they must be refunded to the customers, but I highly doubt it.

Adding speculation on top of speculation usually ends up badly and that is exactly what personifies MAXI.

Buy it for the asset appreciation or avoid it, but then might as well just buy Bitcoin itself.

This ETF needs to be avoided at all costs.

“Creativity is just connecting things.” – Said Co-Founder of Apple Steve Jobs

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Hello everyone,

First, let’s welcome Sabelo Mthembu and Mia Lily to the group.

This post will be a summary of John’s most recent webinar – on October 5th.

Titled: Betting the Ranch

John is up +70.18% YTD in 2022

He is up 9.72% in September.

An annualized return of 45.36% for 14 years.

80.09% trailing one-year return.

He has made 9.12% in 9 trading days.

I would argue that you could count on one hand people that can do this consistently over many years.

We are now 9 months into a 12–15-month bear market.

Q4 could be the best entry point for stocks in a decade. It will be the time to look at those LEAPS.

Concierge clients will soon have a dedicated website for all their LEAPS.

Inflation is plunging but it may not show up until the October 13 number.

VIX pops to $34.00

The major trading rally launched with the onset of Q4 may be discounting the end of interest rates in as early as two months.

U.S.$ is close to peaking with bond bottoming at a 4.00% yield.

Tesla's deal to buy Twitter is a disaster for Musk – there are a lot of non-believers that the deal will even take place.

The Fed raises rates by .75 basis points – the statement suggested rates will be higher for longer.

Consumer sentiment hits a record low according to the University of Michigan. It is worse than the pandemic low and the 2009 Great Recession.

The VIX hits $34.00 on Tuesday. Perfect time for John to put out trade alerts.

The bond short is gone. The rich uncle has given everything away.

The risks of NOT being invested are rising.

Stocks for your list:

PANW – great LEAP candidate

ROM – great entry point.

VISA – great entry point

BRKB – great LEAP

As are many others…

TLT has lost 43% in 21/2 years.

Real estate is in freefall. Case Shiller – falls 18.7% to 16.1% in June.

That’s all for now.

Do take care.

Cheers,

Jacque

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more