"It's hard when a $10-$11 trillion economy that affects one third of the global economy is on a learning curve," said my friend, David Tepper, of Appaloosa Management.

"It's hard when a $10-$11 trillion economy that affects one third of the global economy is on a learning curve," said my friend, David Tepper, of Appaloosa Management.

Mad Hedge Technology Letter

February 10, 2023

Fiat Lux

Featured Trade:

(NO LANDING OUTCOME COULD HURT TECH STOCKS)

(NASDAQ)

NO LANDING!

That’s where we are at and that’s what we face as tech stocks need to overcome the “no landing” scenario to see better days in valuation.

There has been much chit-chat about what sort of recession the US economy will face in 2023.

Well, hold your horses there mister.

The smattering of positive labor data means there might not be a recession at all, which translates into neither a soft landing nor a hand landing for the economy.

Why does that matter for tech stocks?

The lack of light or deep recession has absolutely everything to do with inflation. High inflation kills growth stocks!

The logic behind this goes that if there is no recession, US workers will by and large keep their jobs.

From a societal point of view, this is great for Americans who can bank their salaries and spend, spend, spend.

However, this doesn’t work out so great if the stock market needs lower inflation for tech shares to go higher.

Let me just insert here that I am totally aware of all the tech job losses and they have topped around 200,000 so far and it’s a drop in the bucket to overall hiring and firing.

Interestingly enough, tech layoffs haven’t always resulted in the fired getting better jobs.

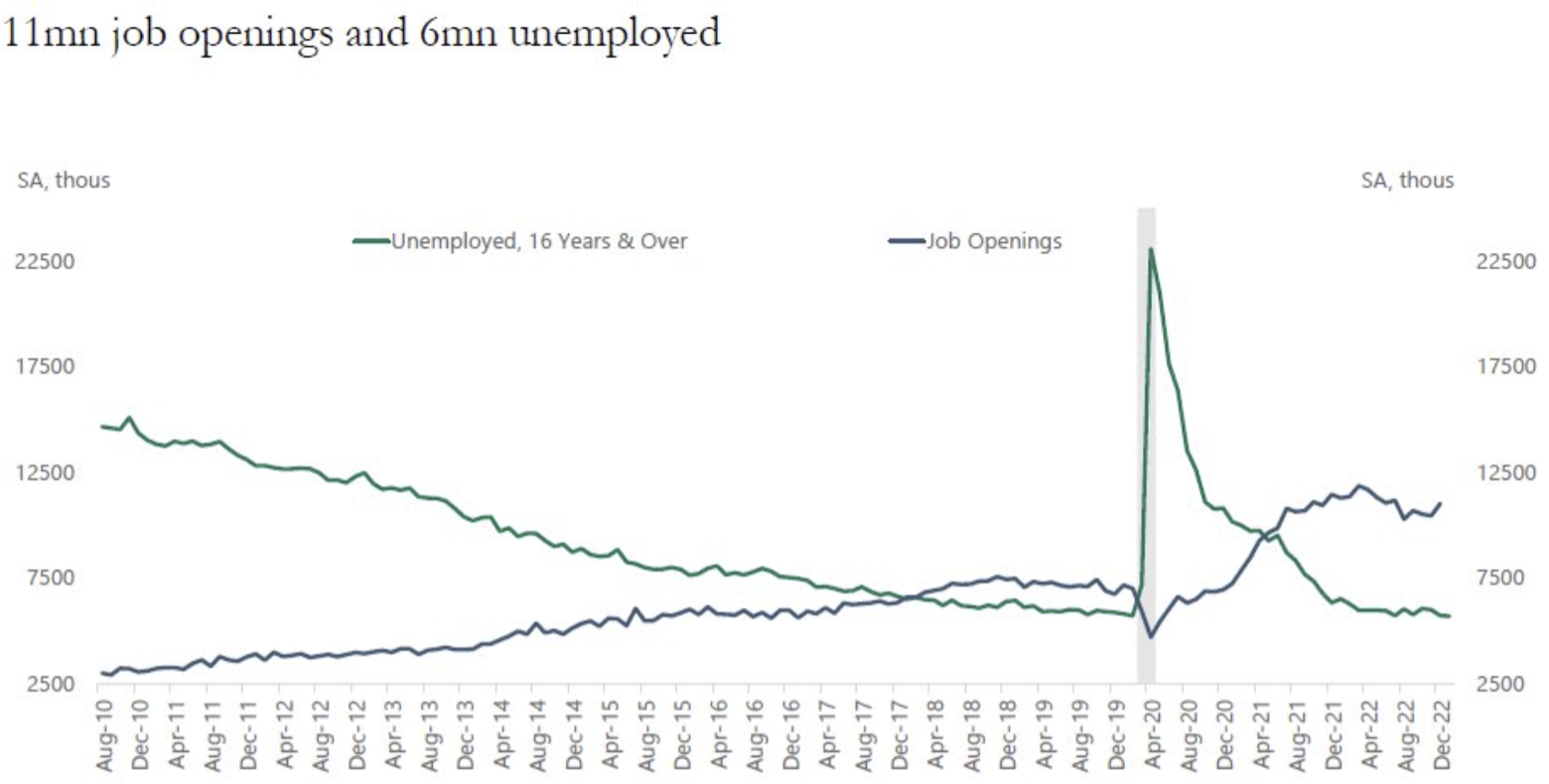

The jobs report shows a massive uptick in hiring particularly for restaurant jobs, retail, and hospitality.

Many of these are also part-time jobs which means the median US job is decreasing in quality and stability.

The result of more hiring for longer is that the US Central Bank might be forced to jack up rates again past the 5% that is priced in.

This is horrible news for the tech sector as the Nasdaq got off to a blistering start in January because of the clear path to lower inflation. This path is starting to close.

Last Friday’s January employment report saw the economy add a much stronger-than-expected 517,000 jobs, while the unemployment rate fell to 3.4%, its lowest level since 1969.

And if the services sector needs to fill hundreds of thousands of jobs, wage gains will threaten to make inflation spike yet again.

The reopening of China’s economy as reverses lockdowns could push commodity prices back to the upside, also contributing to price pressures after several months of slowing inflation readings.

The Fed has always pinpointed strong wage growth and full employment as an impediment to lowering rates.

I have banged on constantly that the Fed hasn’t done enough with lifting rates even though the pace of rate hikes has been historic.

Readers should remember that the amount of stimulus and handouts during the lockdowns were also historic as well.

Demand destruction simply will not occur if real rates are negative and that’s been the case for quite a while I might add.

Now there is a real risk of inflation reaccelerating because the Fed never raised rates high enough for companies to feel pain and fire employees.

This is why tech stocks have been swooning the last few days and the trading environment is still highly complex.

Expect whipsaws for the foreseeable future and if inflation does come back reincarnated, expect a page out of the 2022 playbook with stocks and bonds going decisively lower.

Global Market Comments

February 10, 2023

Fiat Lux

Featured Trade:

(FEBRUARY 8 BIWEEKLY STRATEGY WEBINAR Q&A),

(RCL), (TSLA), (UUP), ($VIX), (BRKB), (TLT), (TBT), (ROM), (CVNA), (SLV), (DIS)

CLICK HERE to download today's position sheet.

NOTE TO SUBSCRIBERS: There will be no strategy letter for

February 13 and 21 as I will be traveling. - JT

Below please find subscribers’ Q&A for the February 8 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: What do you make of the Chinese balloon that crossed the United States last week?

It was the most overhyped, least consequential event in recent memory, and is not a new thing. There is no chance this was an innocent scientific mission as there was no flight plan filed. What’s China’s new frontline weapon? A catapult? A bow and arrow? Are American balloon makers going to demand increased defense spending? Curiously, no mention was ever made of the three Chinese balloons that crossed the US during the previous administration when no action was taken. My guess is that a Chinese Army faction wanted to keep their defense spending rising and torpedoed any rapprochement that was in the works with the US. Another theory was that they wanted to test our response. There is nothing the balloon could have captured that the Chinese didn’t already have from their satellites or even Google Earth for free. The media coverage has been a flood of false information. If the Chinese really can predict global winds at 60,000 feet two weeks in advance, then their math is so far more advanced than our own then we might as well surrender. By the way, during WWII the Japanese sent 20,000 balloons our way in an attempt to set the Western US on fire. Only one exploded, killing a family in Oregon.

Q: I’m getting worried about my long-term LEAPS in (TLT) and (FCX) given the recent market action. Thanks in advance for your help.

A: The (TLT)'s should be OK by expiration because they hit max profit even in an unchanged bond market. But Republican radicals who want a government shutdown at any price are definitely going to rattle your cage. That’s why I currently have no short-term position in bonds and am waiting for a bigger pullback to maybe $101 before I get back in. As for Freeport McMoRan (FCX) you can take profits any time. The stock doubled after we recommended the LEAPS in October. Longer term, I think (FCX) goes to $100 because of a coming global copper shortage.

Q: Should I buy Royal Caribbean (RCL) because we’re looking at a record-breaking cruise season coming up this year?

A: The time to buy Royal Caribbean was actually last June; it was one of the first outperformers in the market, completely skipped the October meltdown, and is practically doubled off the low. So great idea, just 8 months too late. And that actually is the case with a lot of stocks now—they've had such enormous runs over a short time, that you’re taking a lot of risks to get involved here.

Q: Do you think Silicon Valley should force all workers back into the office? Wouldn't that enhance creativity?

A: It does enhance creativity but at the cost of productivity. People are much more productive when they work at home, don’t have to spend 2 hours commuting, and can build their job around their lifestyle. They work at home cheaper too. So, it’s a trade-off, do you want creativity or do you want productivity? Well, the productive people should stay at home, the creative people should go to the office—it’s a company by company, product by product decision.

Q: You say you never touch 2x and 3x ETFs?

A: The only exception to that is the ProShares UltraShort 20+ Year Treasury ETF (TBT) which we traded for 2.5 years while the bonds were making a straight line move down, or the ProShares Ultra Technology ETF (ROM) which tends to have straight up move like this year. And the only time you could do a 2x is if you think the move in the underlying is going to be so enormous it covers up all the costs of dealing in these ETFs, then it’s worth doing. 3xs I never ever touch them because those reset at the end of the day and are really designed to be intraday hedging instruments, which we’re not interested in.

Q: Are you still bearish on the US dollar (UUP)?

A: Absolutely, we’ve had almost a straight line move down ever since October, and we’re getting a temporary break on that while interest rates stay higher for longer. The next dive in interest rates, the dollar collapses once again.

Q: When you buy back into bonds, where in the curve will you be buying?

A: In bull markets, you always want to buy the longest maturity available. Back in the 1970s, I used to buy WWI infinite British Treasury bonds because they had 100-year maturities, and therefore, in any bull market, have the largest gains. In the US, the 30-year instruments are pretty illiquid, so I focus on the 10-year, which is the iShares 20 Plus Year Treasury Bond ETF (TLT).

Q: What could be the next entry point for Tesla (TSLA) LEAPS?

A: I’m afraid that we have left LEAPS land for Tesla, I mean $100, $110, $120, $130—that’s all LEAP territory. Up here? Not unless you want to do a very low return LEAP like a $150/$160. I don’t see Tesla going below $150. Too many people trying to get into the stock, and Elon Musk is a master at delivering short squeezes, which he has done a perfect job of this year.

Q: What do you think about Real Estate Investment Trusts (REITS)?

A: I love REITS. They are a falling interest rate play. Highly exposed to interest rates, highly leveraged, and you get some great performance—and we’ve already had some since October. I think the bear market in real estate ends this year and we get a new bull in housing that starts next year because we still have a chronic structural shortage of housing. We’re missing about 10 million houses that we need—in that situation, prices go up. In fact, there are still bidding wars going on in the prime residential (mostly rural) parts of the country.

Q: Wouldn’t you want to buy at-the-money calls, not spreads in a low Volatility Index ($VIX) market on a 4-6 month view, because of cheaper pricing?

A: Yes you do, but not on top of a record move to the upside. If we can get a pullback in the markets of a1 /3-1/2 of their recent moves, and the ($VIX) is still low, then that makes all the sense in the world, to buy at the money calls with ($VIX) of $17. The only problem is if we give up half the recent gains, you’re not going to have a ($VIX) at $17 anymore, it’ll be more like $27 if we get a pullback like that and options will be expensive again. It’s amazing how cheap upside exposure gets at market tops—that’s what the ($VIX) market is telling you. In other words, it’s a sucker’s bet. You can’t have your cake and eat it too.

Q: What do you think about Alphabet (GOOGL)?

A: It’s overbought like the rest of the stocks in the sector. But the charts are looking very attractive, with an upside breakout of the 200-day. Long-term, they have a killer business model, but they also have antitrust problems. Again, everything is way too overbought for me to get involved on a short-term basis.

Q: What price would you get in at for Berkshire Hathaway (BRK/B)?

A: It’s not selling off, it’s flatlining. So even a small dip like we had yesterday would be a decent place to get into. Long term we’re looking for $400/share for this by the end of this year.

Q: Will strong wage growth lead the Fed to raise interest rates higher?

A: Well they’ve already said essentially they’re going to do 2 more quarter point rises. Beyond that, the Fed itself doesn’t know. When you have interest rates at 10-20 year highs, and 3.4% unemployment. No one has ever seen that before, there is no playbook for what’s happening now—either in the economy or in the stock market. So everyone’s standing around, scratching their heads, trying to figure out what to do, and waiting for more data to come out to give direction. And I’m in the same position really.

Q: Will the US Treasury bond get down to a 2.0% yield by the end of the year?

A: I think it's a possibility but expect a lot of volatility and fears around prospects of a government shutdown this summer and a debt default. Part of the Republican party seems intent on forcing that, and that is not good for bond longs. You get through that, you could have an absolutely ballistic move up in the (TLT), to $120 or even $130.

Q: Would you consider a LEAPS on housing stocks?

A: LEAPS are things you do at multi-year market bottoms, not after 50% moves; and the housing stocks have actually been moving since June; so that was a June story. Buy low, sell high—it’s my revolutionary new concept; most people do the opposite.

Q: Should I invest in Disney (DIS) on a buy it on a Bob Iger turnaround?

A: Yes, but only on a dip; we’ve already had a massive move. If we don’t get a recession, that is fantastic for Disney’s park business.

Q: What is your target for Silver (SLV)?

A: $50/oz. We’re at $20 now. Silver is becoming the new industrial metal, far outstripping any jewelry demand that you used to have; and that’s because of EVs and solar. Who knew that we’re at 10 million homes with solar panels in California now? That is just an enormous number that’s happened mostly in the last five years.

Q: When you look at Natural Gas, would you consider LEAPS?

A: Yes, but I haven’t run the numbers yet. The price has gotten so low, down 80% in eight months that you buy it even if you hate it.

Q: Should I pay attention to demographics when I invest? What is the most important one right now?

A: Demographics are very important, because children born today become customers in 20 years, and companies will start adapting their policies for those customers now in terms of capital investments and so on. It also affects stock markets now. Also, you always want to invest in the country that had the fastest growing population, which used to be China but isn’t anymore. By the way, the reason the US economy has outperformed Europe by 1% a year in GDP growth for the last 70 years is because we allow immigrants, and they don’t. All parties used to be in favor of immigration while now only one is. Why, I don’t understand.

Q: What about a LEAP on Silver (SLV)?

A: That is a possible candidate because we have had a move, but it’s only been about 20%. It’s not like 50% or 100% like we’ve seen with Tesla (TSLA). There are a few asset classes that are still in LEAPS territory—I think Silver would be one of them, and certainly natural gas (UNG). If I were to do a LEAPS, I’d go out 2 years and do something like a $25-$27; the old high is $50. You should get about a 5x leverage on that kind of LEAPS.

Q: Would you buy LEAPS puts on Carvana (CVNA)?

A: Absolutely not. Again, another great one-year-ago idea, not a now idea. Buy Put LEAPS at extreme market tops, not now. Carvana had dropped 95% in the last year.

Q: Is seasonality an important consideration in your trading strategy?

A: Absolutely yes. If you buy stocks in November and do the sell-in-May strategy, your average annual return is something like 20% a year. If you buy stocks in May and sell them in December, the 70-year return on that is zero. I love having the tailwind of seasonality; I can’t remember seeing it when it didn’t work. It’s an important consideration, and we’re right in the middle of the “BUY” season and the market is agreeing with me.

Q: You should do a LEAPS letter.

A: I already do in fact do a LEAPS letter, and it’s called the Mad Hedge Concierge Service where we have a whole website dedicated to just LEAPS. Some ten out of 12 made money last year, and some went up 10X. Contact customer support at support@madhedgefundtrader.com if you’re interested. Concierge members are very happy with their LEAPS coverage.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

At 29 Palms in my M1 Abrams Tank in 2000

“If I had asked what the customers wanted, they would have told me faster horses,” said Henry Ford.

Mad Hedge Biotech and Healthcare Letter

February 9, 2023

Fiat Lux

Featured Trade:

(AN EMERGING KING OF BIOSIMILARS)

(AMGN), (ABBV), (JNJ), (BAYG), (AZN), (REGN)

Patience is one of the key attributes that long-term investors need to cultivate, but practicing it is challenging. Stock markets are entirely unpredictable, and their ups and downs tend to rattle even the most experienced investors.

However, it’s essential to keep a calm mind and to be confident that the businesses you invest in have the fortitude to overcome even the most challenging economic or market downturn.

The biotechnology industry is an excellent place to search for stocks that can overcome market turmoils and succeed in the long run because the treatments they develop are so crucial to the lives of their clients.

Amgen (AMGN) is a biotech that would make an excellent long-term investment.

This business, which has been a leader in the biotech sector since the 1980s, is among the largest in the world.

Amgen is also a member of the renowned Dow 30 companies, with a focus on oncology, biosimilars, and inflammatory diseases. In the past 10 years, it has established a strong track record and solid revenue growth trajectory.

The company recently released its fourth-quarter results, and they looked a tad flat on the surface. The report disclosed a total revenue growth of only 2%, which could have been caused by the pressures linked to pricing and competition around the company’s top-selling cholesterol-lowering treatment Repatha, migraine drug Aimovig, and immunology medications Otezla and Enbrel.

Still, Amgen continues to be a solid profit-making business, holding an A+ grade in terms of profitability. It sustains considerable pricing power on its treatments under exclusive patents and from its up-and-coming portfolio of biosimilar candidates.

Amgen has maintained a BBB+ rated balance sheet. It also pays a respectable dividend yield of 3.5%, with a well-protected payout ratio of 44%.

The company has also recorded consecutive growth in this aspect for 11 years. Looking at these figures, Amgen has scored primarily As in terms of consistency, growth, dividend, and yield.

Notably, the company’s foray into the biosimilar landscape would make long-term investors of the company quite happy soon.

Its long-awaited biosimilar version of the No. 1 selling drug worldwide, AbbVie’s (ABBV) Humira, has recently been launched to market.

Amgen’s version, called Amgevita, is the leading biosimilar in this market to date. It already has a five-month lead over the next competitor, arming it with a lot of time to establish a more competitive standing.

Beyond this candidate, Amgen has at least six more biosimilars that it plans to launch in the US and across the globe from 2023 until the end of 2030. This timeline would give the company excellent visibility in the long run.

Another potential biosimilar blockbuster is ABP 654, which is a biosimilar of Johnson & Johnson’s (JNJ) top-selling immunology treatment Stelara.

Amgen also has biosimilar versions of Bayer's (BAYG) and Regeneron’s (REGN) eye disorder drug Eylea and AstraZeneca’s (AZN) rare kidney disease treatment Soliris.

Basically, biosimilars are knock-offs for biologic drugs. They cost less because the manufacturers do not spend less in the research, trials, and approval stages. The processes are also shorter and less risky.

Biosimilars provide a way for patients and the whole healthcare system to save billions of dollars, signaling a bright future for this segment. They offer more affordable options to patients, which is an excellent response to the rising prices of medicines.

This means biosimilar development is far less speculative than creating a new drug, as manufacturers only need to replicate the already established results and success of the existing “original” drug.

Moreover, biosimilars bring with them a degree of pricing power. Unlike traditional treatments, no two biosimilars are allowed to carry the same biologic profile and should still undergo a stringent FDA assessment prior to gaining approval.

Overall, Amgen is a good option for long-term investors on the lookout for a quality biotech to add to their portfolios. Thanks to its burgeoning portfolio of potentially top-selling biosimilars, it has long-term solid revenue growth catalysts. These factors make Amgen a compelling buy on the drop.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

February 9, 2023

Fiat Lux

Featured Trade:

(THE BULL CASE FOR BANKS),

(JPM), (BAC), (C), (WFC), (GS), (MS)

CLICK HERE to download today's position sheet.

Urgent Trader Warning: The Mad Hedge Market Timing Index moved to a one-year high yesterday and is in “STRONG SELL” territory. Any long stock positions you have for the short-term should be hedged. For more details, please visit my Refresher Course at Short Selling School by clicking here.

Caveat Emptor!