Global Market Comments

December 6, 2023

Fiat Lux

Featured Trade:

(THE MAD HEDGE DICTIONARY OF TRADING SLANG),

(TESTIMONIAL)

Global Market Comments

December 6, 2023

Fiat Lux

Featured Trade:

(THE MAD HEDGE DICTIONARY OF TRADING SLANG),

(TESTIMONIAL)

Mad Hedge Biotech and Healthcare Letter

December 5, 2023

Fiat Lux

Featured Trade:

(A UNION IN THE MAKING?)

(HUM), (CI), (CVS), (AET), (UNH)

The healthcare market was recently abuzz with the news of a potential mega-merger that sent shares of Humana (HUM) and The Cigna Group (CI) into a nosedive - 5.5% and 8.1% respectively. This news, centered around a transaction combining stocks and cash, could significantly reshape the healthcare landscape.

But let's not get ahead of ourselves. After all, in the world of healthcare mergers, certainty is as elusive as a mirage.

Still, if you’re feeling a sense of déjà vu, it’s because this isn’t the first time Humana and Cigna have danced around the idea of a merger.

Recall 2015 when Humana flirted with the idea of a merger with Cigna but ended up cozying up to Aetna (AET) – a union that never saw the light of day, thanks to the US courts.

A similar fate befell an attempted merger in 2017, when Elevance Health (ELV), then known as Anthem, tried to acquire Cigna for $48 billion, only to be blocked by the courts.

Since these previous attempts, both Humana and Cigna have significantly grown.

Prior to this market shake-up, Humana boasted a market capitalization of $62.87 billion, with Cigna commanding a higher ground at $83.77 billion.

But as history shows, regulatory skepticism often casts a long shadow over such ambitious plans, with fears of increased costs for the American public. This skepticism has extended to smaller deals, such as UnitedHealth Group's (UNH), which faced hurdles in their acquisition attempts.

Yet, the potential merger between these healthcare giants teases the possibility of substantial cost savings.

When giants unite, the promise of cost savings looms large. Redundancies in corporate functions like HR, investor relations, and executive positions offer low-hanging fruits for cost-cutting.

But the real cherry on top is the potential for operational synergies – cross-selling opportunities and leveraging infrastructure for efficient service delivery.

Humana's stronghold lies in its Insurance unit and CenterWell, with the latter, including pharmacy, provider services, and home solutions, contributing 16.3% of last year's revenue.

In contrast, Cigna wades into deeper waters, with its substantial revenue streams from pharmacy benefits and home delivery pharmacy businesses.

Now, let’s look at the companies in terms of revenue. A side-by-side of Humana and Cigna's revenues offers an intriguing picture.

Humana's Medicare Advantage revenues soared from $59.47 billion in 2020 to $72.89 billion in 2022.

Cigna, however, has only inched forward in this space. Humana's evident dominance in Medicare Advantage, with a market share of about 18%, contrasts sharply with Cigna's modest 2%.

Despite these differences, a merger isn't outside the realm of possibility.

For example, CVS (CVS) managed to successfully acquire Aetna for $69 billion back in 2018, with the two companies eventually turning into CVS Health.

While that merger proved that big deals could happen, the odds for Humana-Cigna are not exactly in Vegas betting territory.

Speculations about Cigna offloading its Medicare Advantage operations could make this merger more palatable to regulators, but it's far from a sure bet.

Another question to think about amidst these talks is why the market reacted like someone yelled “fire” in a crowded theater.

Well, it all boils down to the fear of overpayment.

Cigna, being larger, could potentially swallow Humana. But Humana, with its stronger financial health and market positioning, is seen as the more desirable entity.

The valuation metrics – price to earnings, price to adjusted operating cash flow, and EV to EBITDA – further complicate this perception, as Humana commands a premium.

With a potential merger announcement might be on the horizon, investors should approach this with a blend of skepticism and intrigue. The market is jittery, perceiving a possible merger as potentially detrimental to shareholder value.

However, should the merger succeed against the odds, the combined prowess of Humana and Cigna could spell a profitable future for investors. Knowing that the healthcare sector is never short of surprises, this potential merger, should it come to pass, could be one for the history books.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

December 5, 2023

Fiat Lux

Featured Trade:

(The Mad Hedge December traders & Investors Summit is ON!)

(HOW TO SPOT A MARKET TOP),

(A COW BASED ECONOMICS LESSON)

The Fed has stopped raising interest rates, inflation is falling, and tech stocks are on fire! What should you do about it? Attend the Mad Hedge Traders & Investors Summit from December 5-7. Learn from 18 of the best professionals in the market with decades of experience and the track records to prove it. Every strategy and asset class will be covered, including stocks, bonds, foreign exchange, precious metals, commodities, energy, and real estate. Get the tools to build an outstanding performance for your own portfolio. Best of all, by signing up, you will automatically have a chance to win up to $100,000 in prizes. Usually, access to an exclusive conference like this costs thousands of dollars. You can attend for free!

Listening to this webinar will change your life! To register, please click here.

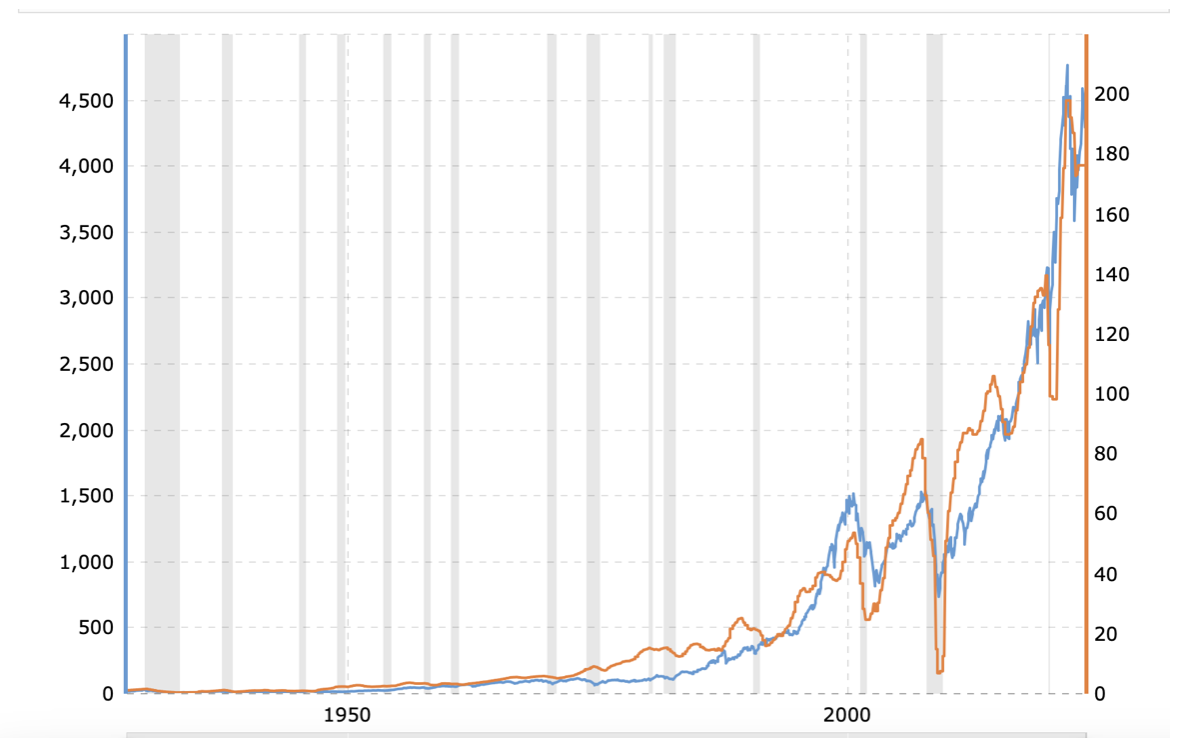

After the sharpest move up in stock prices, you have to ask the question of whether the market is topping?

I have a laundry list of items to check off before I draw that harsh conclusion:

1) Retail buyers enter the stock market on a large scale. So far, they are missing in action. Nobody believes in this rally.

2) S&P 500 profits historically peak at 50% above the old high. In the last cycle, they got to $200 a share. So we still have room to soar to $300/share, some 50% above today’s probable $200/share.

3) The yield curve is always inverted at a market top (short term interest rates are higher than long term ones.) In actual fact, this relationship is about to reverse. Interest rates are about to de-invert.

4) Stocks are always more expensive than bonds on a relative basis at bubble tops. Currently, both stocks and bonds are historically cheap.

5) Even if the Fed does raise 25 basis points one more time, the next big trend is down, probably 200-300 basis points.

Add all of this up together, and not only are stocks not topping, they have just launched on a years-long bull market.

The party is only just getting started.

I just thought you’d like to know.

S&P 500 Earnings per Share

The party is only just getting started

“Data is worth more than gold,” said Elon Musk, founder of PayPal, Space X, Tesla, Solar City, The Boring Company, Neuralink, and owner of “X”, the former Twitter.

Mad Hedge Technology Letter

December 4, 2023

Fiat Lux

Featured Trade:

(SPOTIFY SHOWS US THE WAY)

(SPOT)

The music streaming service Spotify (SPOT) is living in the future and by that I mean they are cutting 17% of staff.

Silicon Valley will be a lot leaner in the future and this is just one of many firms that will shed to become more efficient.

The announcement was made today and is making shockwaves through the industry.

Many ponder what might be the catalyst to the next move up in the tech sector.

Well, look no further than Spotify which is delivering the playbook to squeeze out higher earnings at a time when tech earnings are exposed to potential downgrades.

It’s no joke that tech salaries are exorbitant and gutting the froth is the next stage of Silicon Valley.

Elon Musk delivered us a preview when he dumped 80% of Twitter’s staff realizing that most of his staff didn’t meaningfully contribute or justify what they earned.

Spotify is next to take a magnifying glass to its balance sheet as it hopes to appease shareholders as we head into a 2024 interest rate-cutting year.

It’s my guess that CEO Daniel Ek wants to get his show to benefit from that slingshot effect next year for Spotify shares.

In an email sent out to staff, Ek said that Spotify was taking “substantial action to rightsize our costs,” adding that the company took on too many employees over the years 2020 and 2021 when the capital was cheap and tech companies could invest significant sums into team expansion.

The latest round of cuts equates to roughly 1,500 jobs.

It comes after Spotify reported a 65 million euros ($70.7 million) profit in the third quarter, citing lower spending on marketing and personnel.

Spotify raised the prices of its subscription plans earlier this year and has been expanding into podcasts and audiobooks.

Spotify cut 6% of its workforce, or about 600 employees, at the start of the year. Spotify then laid off 2% of staff, equivalent to roughly 200 roles, in June.

This isn’t the first time they have shed staff and won’t be the last.

Europe has barreled straight into an economic recession and the macroeconomic backdrop has given a great reason for Ek to downsize.

With the way generative AI is going, I don’t believe any further staff cuts will be followed by a hiring bump, because AI will get the job done instead of humans.

Around 2021, we blasted through peak tech hiring and we will never see not only that type of volume hiring, but gone are the days of sweet salaries.

It’s a lot cheaper to plug in software and tech firms will continue to downsize even though economic growth waves come and go.

No economic growth wave in the future will prompt a massive uptick in fresh faces.

AI and its advancement of will effectively mean that Spotify will be run by a few people running servers, infrastructure, and algorithms.

Eventually, the entire tech sector will be run by a handful of people and software underpinning their investments and Ek of Spotify will be included in one of the handful in this exclusive group.

Buy SPOT on the dip.