“If you try to do too much, you will not achieve anything.” – Said Confucius

“If you try to do too much, you will not achieve anything.” – Said Confucius

(EUROPEAN COMPANIES ARE CASH-RICH)

May 8, 2024

Hello everyone,

Companies in the Stoxx 600 index have nearly 1.5 trillion euros ($1.6 trillion) in cash on their balance sheets - that’s 25% higher than pre-pandemic levels, according to Goldman Sachs.

The bank further stated that free cash flow yield in Europe is around 6% - more than 1% point above that of the United States. Sectors with the highest yield include autos, commodity producers, and financials. Goldman favors the latter two, given their clearly stated focus on shareholder returns.

Balance sheets are strong. And the bank notes that net debt to EBITDA (earnings before interest, taxes, depreciation, and amortization) is close to an all-time low. Furthermore, Goldman says, “Europe has rarely looked cheaper on an absolute and relative basis.”

Regarding dividends, the bank believes they can continue to grow in Europe given that payout ratios are below the historical average. They expect dividends to grow around 3% in 2024 and 4% in 2025.

Goldman particularly favors stocks in the banking and energy sectors. The MSCI Europe Value index offers a dividend yield of 4.8% - 2.8 times that of the MSCI Europe Growth.

Goldman lists here companies in the Stoxx Europe 600 with the highest, sustainable, 12-month forward dividend yields in each sector.

This is not a recommendation to buy any of these stocks. It is purely for your information to show you what dividend yields are available. Many people are interested in yield, so this is why I’m illustrating these examples.

Bonza removed from Australian skies.

Negotiations have failed between budget airline Bonza and its aircraft lenders. So, the decision has been made to remove the airline’s fleet from Australia.

The airline's financial issues have forced lease agreements on a fleet of Boeing 737-8 planes to be terminated.

Almost 60,000 passengers say they are owed money after many of their bookings were canceled.

The low-cost carrier was less than 12 months old when it canceled all flights across Australia and entered voluntary administration last week.

Wearing Clothing made from Bamboo supports the environment.

Bamboo is the fastest-growing plant in the world. It stores five times more carbon than other hardwood trees. It stores this carbon in its plant and roots, in turn helping to regenerate soil health.

It requires minimal water and little to no pesticides, which protects surrounding habitats and ecological systems from harsh chemicals used to grow crops.

Bamboo viscose, a fibre crafted from bamboo, is very soft. The fabric has natural moisture-wicking properties, meaning it can absorb moisture away from the skin.

Bamboo is biodegradable, making it a more environmentally friendly choice compared to cotton, which often requires more water and chemicals to grow and process.

Brands that use bamboo in their clothing include: Baserange, BAM, Peachaus, Patra, & Lotties Eco.

QI Corner

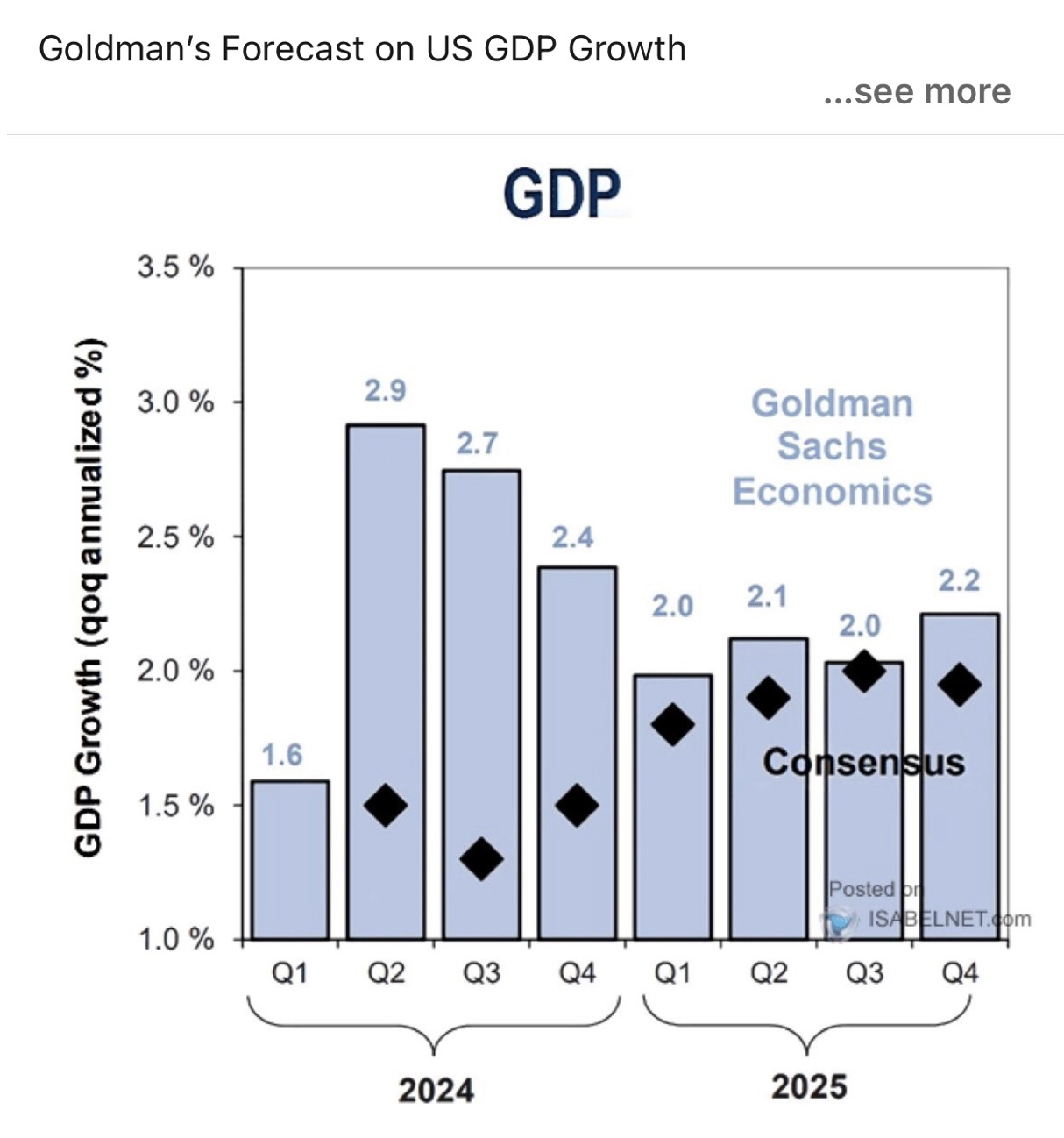

Goldman expresses strong confidence in the robustness of the U.S. economy, projecting a more positive outlook for the growth of U.S. GDP in 2024 and 2025 compared to consensus forecasts.

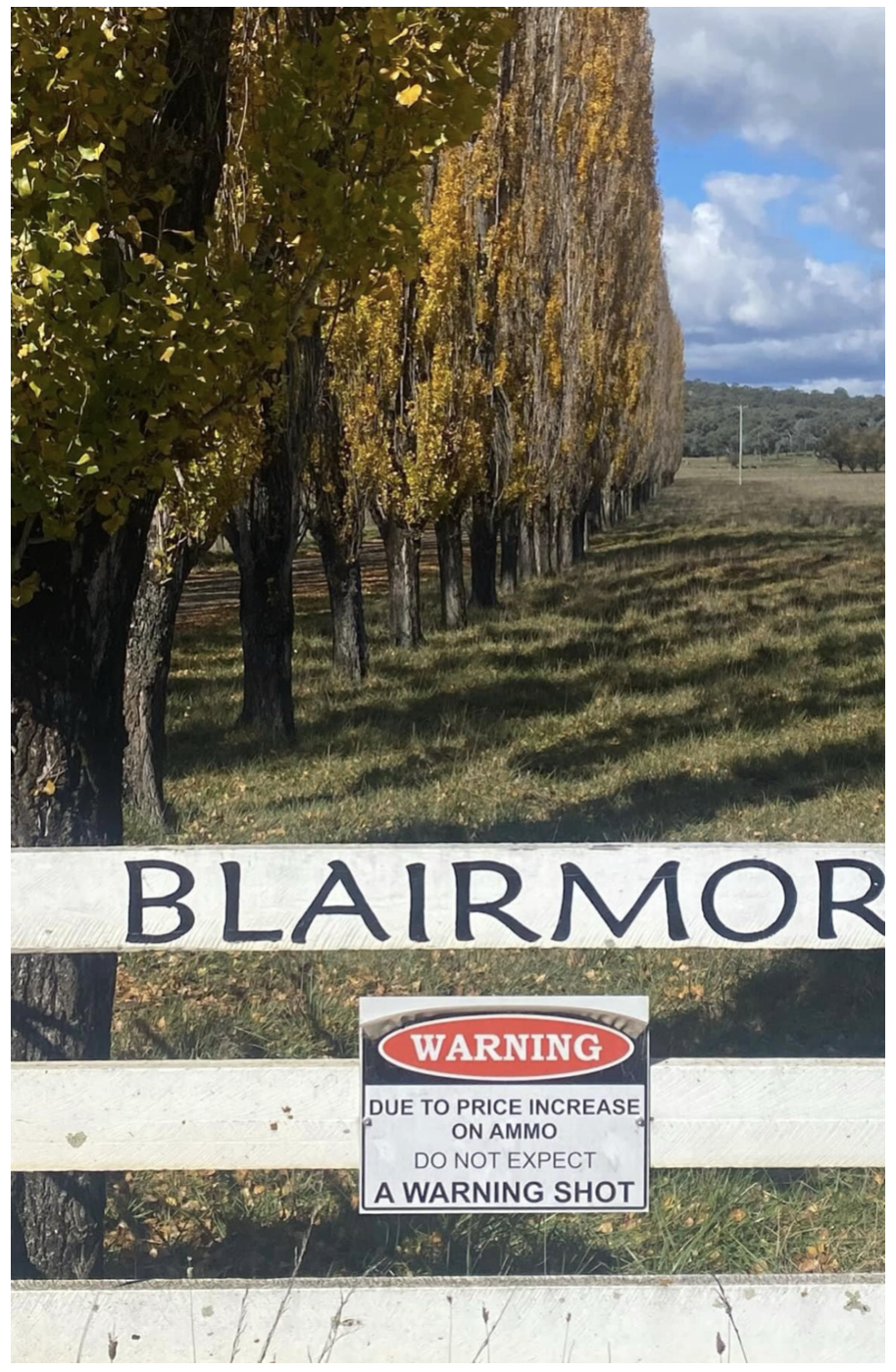

A sign on the gate of a Glen Innes property in New South Wales. It seems Australians take their privacy quite seriously.

Cheers,

Jacquie

Global Market Comments

May 8, 2024

Fiat Lux

Featured Trade:

(TAKING A LOOK AT HOME DEPOT)

(HD)

I have been out shopping the neighborhood for good non-tech plays and I found another one.

You are going to think that I am completely MAD by thinking about this trade right now. But I’ve gotten used to that by now.

If you had to pick one sector of the 100 or so that Standard & Poor’s tracks, that is universally hated by all traders and investors, it would have to be the retailers.

Widely viewed as headed for the dustbin of history, many retailers are not going to make it to Christmas, let alone stay in business through 2025.

Do any value screen of all listed stocks, and about half of all the bargain stocks are found in the retail industry.

These are the buggy whip manufacturers of 1901 before they got run over by the auto industry.

Of course, you can blame Amazon, which is rapidly taking over all sales of everything in the US. They have about a 50% market share of all online sales. No wonder the government is going after them with an antitrust case.

This is thanks to their cutting-edge technology and massive economies of scale.

Amazon is probably the number one job destroyer in the US today, with some 5 million retail jobs on the chopping block over the next five years.

However, there is one safe haven that so far seems immune from Amazon’s appetite and that would be Home Depot (HD).

I am using the recent 18% sell-off in the shares to look at (HD), which is occurring, not because of anything Home Depot did, but because of higher interest rates for longer.

Longer term, I think Home Depot will continue to appreciate, as the housing and remodel boom will take off like a rocket once interest rates DO fall. That could be in four months….or sooner.

Then we will have a home remodeling boom that has years to run, and possibly decades. The more expensive homes get, the more inclined owners are to fix up their existing digs. They go to Home Depot to do that.

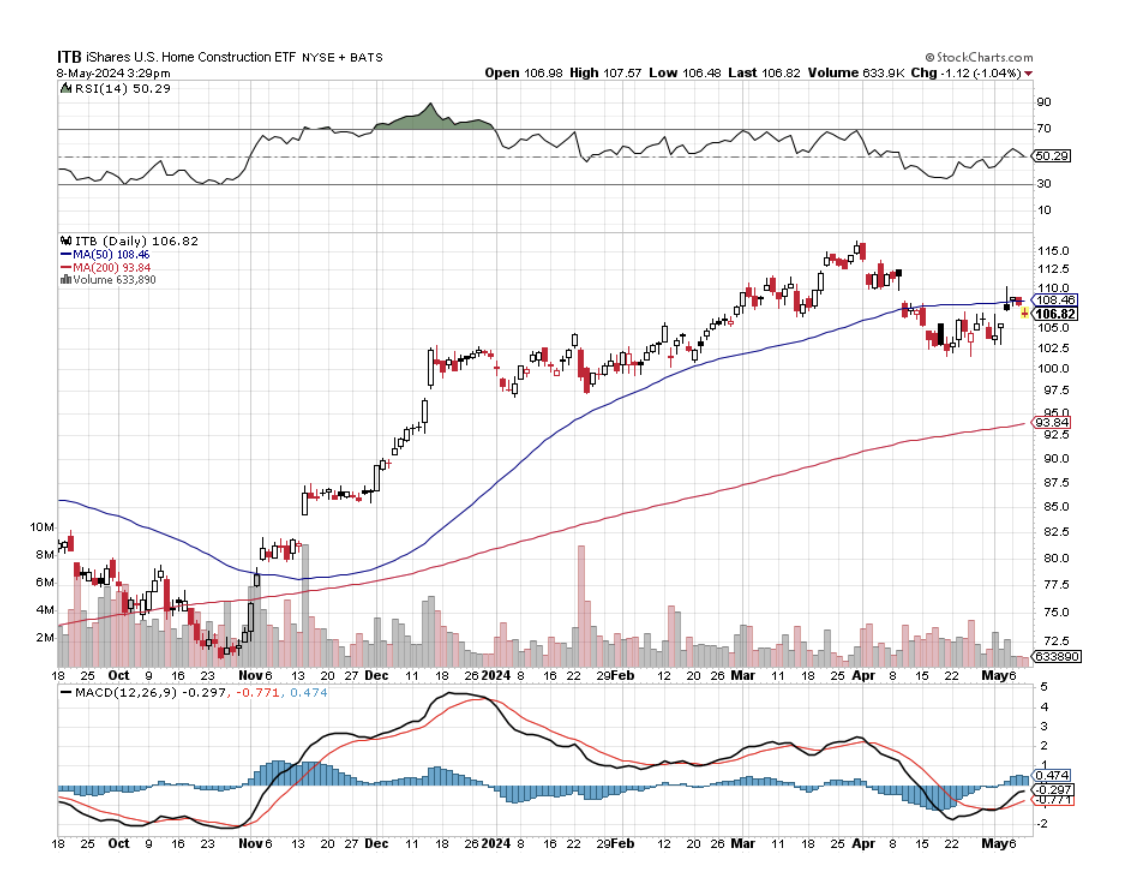

If you want to make a safer play, buy the iShares US Home Construction ETF (ITB) on this dip, which gives you broader exposure to the real estate recovery and has a much more solid bottom.

Baskets of shares always have lower volatility than single stocks, but lower returns as well.

We just have to give the market a chance to have a few more heart attacks before the current correction ends.

Home Depot is in a tiny retail niche that has so far avoided the Amazon onslaught. There are many reasons for this.

When you need a particular screw, lighting fixture, or unique plumbing part, calling Amazon will get you absolutely nowhere.

You need (HD)’s sympathetic, knowledgeable customer service people, usually retired contractors themselves, to point you in the right direction and assist with a few helpful suggestions.

They’ve done this for me a million times.

Home remodeling and repair is also an industry where a premium is paid for making parts available NOW! A burst pipe won’t wait for an Amazon priority delivery, nor will a leaky roof or broken sprinkler head.

A lot of independent contractors are now not even able to plan supplies weeks or months in advance. They buy what they see.

The home repair and remodel boom will continue, as it is the working man’s solution to high home prices, especially on the coasts, as the profusion of home repair YouTube videos testify. You can fix ANYTHING on YouTube.

While Home Depot recently reported annual revenues of $34.79 billion, up 2.92%. Operating income was reported at $4.8 billion, up 12.82%. Net income came in at an impressive $2.8 billion, up 16.69% YOY. Yet, you get a low 22.7 times price-earnings multiple typical of retailers.

They should do much better in the spring Q2 reporting season. We will know for sure when the company reports on Q2.

This gives us a great discount entry point for a super long-term company, which doesn’t care what the US dollar is doing, which will soon be falling.

“Most of the ETF’s today are your dad’s Oldsmobile,” said Lee Kranefuss of Source Advisors, about the outdated irrelevance for most equity indexes.

Mad Hedge Biotech and Healthcare Letter

May 7, 2024

Fiat Lux

Featured Trade:

(PACKING A HEAVIER PUNCH)

(AMGN), (NVO), (LLY), (REGN)

Amgen (AMGN) is having a moment. Early results for their injectable drug MariTide sound pretty darn promising.

But it’s not all roses and sunshine at Amgen. The company also dropped the curtain on AMG786, an experimental oral weight-loss pill that just wasn't cutting it.

It’s tough in the pharmaceutical arena, especially since this whole weight-loss drug market is a gold rush right now. Eli Lilly (LLY) and Novo Nordisk (NVO) are cleaning up, and even Pfizer (PFE), despite their hiccup, isn't going to roll over that quickly.

Now, back to MariTide. Calling it a "multi-blockbuster" sounds flashy, but investors want to see if it can crack the hold those big two already have. Amgen's got a decent track record though, so I wouldn't write them off just yet.

The early scoop on MariTide is pretty tantalizing. The last round of Phase 2 trials showed that three monthly shots could significantly trim the waistline, with the heftier doses keeping the pounds off for up to four months post-treatment.

Actually, MariTide’s core strength is that it’s just once-a-month jab — an easier regimen compared to the weekly routine required by current front-runners like semaglutide and tirzepatide.

Speaking of the competition, Novo Nordisk’s semaglutide and Eli Lilly’s tirzepatide have been seeing users pack the pounds back on pretty quickly after stopping treatment.

That’s not ideal, and it’s exactly the kind of opening Amgen is looking to capitalize on with MariTide.

Now, let’s broaden our scope. It's a bit of a misnomer to just call it an “obesity pipeline” because, let me tell you, this technology is dipping its toes into much more than just shedding pounds.

Those GLP-1 agonists like semaglutide and the double-duty “double G” agonists like tirzepatide? They’re not just one-trick ponies.

Aside from battling the bulge, they’re making waves in treating diabetes, slicing through cardiovascular risks, and even exploring new frontiers like osteoarthritis and sleep apnea.

Heck, they’re even peeking into Alzheimer’s prevention — Novo Nordisk is already revving up for a phase 3 trial.

Despite these lucrative offshoots though, obesity remains the arena’s juggernaut.

Novo Nordisk’s latest data, as bleak as it might seem for global health, paints a picture of a market vast enough to entice anyone. Think about it—out of 813 million people wrestling with obesity, only one million are currently on these incretin drugs.

And with projections pointing to numbers ballooning to 1.2 billion by 2030, well, the potential market is jaw-dropping.

If Amgen’s MariTide hits the mark, we could be talking about a whopping $20 billion in annual sales from just this one contender in about 7-8 years, spanning obesity and a few neighboring conditions.

That’s even if they face a dogfight over pricing and if the average price per patient hangs below what the big guns like Novo Nordisk and Eli Lilly are currently pulling.

Now, think about this — current estimates peg Amgen’s growth from $33 billion this year to a modest $35.1 billion by 2033. My take? That’s wildly conservative.

If you ask me, Amgen's obesity pipeline alone, even with just modest success, could blast those numbers out of the water.

But let's not kid ourselves – MariTide alone won't make Amgen king of the obesity market. To truly capitalize on the segment’s potential, Amgen might need to consider teaming up with those emerging stars working on preserving lean body mass, or even big players like Regeneron (REGN).

They could take a couple of routes here. One slick move could be scooping up some smaller biotech firms or cozying up to bigger fish through partnerships or in-licensing deals to beef up their treatment options.

Alternatively, Amgen could play it cool and simply pair MariTide with their own upcoming products once they hit the market. Sure, this might keep things simple, but it kind of feels like leaving money on the table, isn’t it?

Admittedly, it’s still early days when it comes to these weight loss treatments. One thing's for sure: the next few years will be a wild ride for obesity drugs. After all, it’s clear that the GLP-1 craze is doing for pharma what AI hype is doing for tech stocks. It’s like a rising tide lifting all boats.

Looking ahead, the big winners in the next 18 months are looking to be Novo Nordisk and Eli Lilly. These guys are leading the pack, while others might just not make it to the finish line, ending up as flops in the stock market drama.

Yet, through all this, Amgen stands out as a dark horse.

Even if the obesity pipeline doesn't turn out to be their golden ticket, Amgen's strategic positioning could still deliver solid long-term value.

But, and here’s the kicker, if MariTide and its potential combo treatments hit their stride as hoped, Amgen could sprint ahead in this fast-paced market race — not just in obesity but in those juicy, adjacent niches too. This could spark some serious value creation that current forecasts haven't even begun to factor in.

So, while the market’s getting its gears grinding, Amgen might just surprise us all. I say keep this stock on your watchlist.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more