Global Market Comments

August 7, 2024

Fiat Lux

Featured Trade:

(PLAYING THE SHORT SIDE WITH VERTICAL BEAR PUT DEBIT SPREADS)

(TLT)

Global Market Comments

August 7, 2024

Fiat Lux

Featured Trade:

(PLAYING THE SHORT SIDE WITH VERTICAL BEAR PUT DEBIT SPREADS)

(TLT)

Mad Hedge Biotech and Healthcare Letter

August 6, 2024

Fiat Lux

Featured Trade:

(JUST WHAT THE DOCTOR ORDERED)

(PFE)

Remember when everyone thought Pfizer (PFE) was just a one-hit COVID wonder? Well, it looks like they're proving the naysayers wrong. Let's dive into this medical marvel, shall we?

Pfizer just dropped its Q2 results, and boy, did they deliver a shot in the arm to Wall Street expectations. Revenue hit $13.28 billion, beating estimates by 2.02%.

But the real showstopper? Earnings per share of $0.6, smashing expectations by a whopping 30.19%.

Now, I know what you're assuming: "Isn't Pfizer still riding that COVID wave?"

Well, excluding COVID-19 products, revenue growth was actually a healthy 14% year-over-year. It's like Pfizer's been hitting the gym, bulking up its non-COVID muscles.

Speaking of muscles, let's talk about those margins. The adjusted gross margin pumped up to 79% from 76%. That's a 300 basis point improvement.

But that’s not all. Recently, Pfizer hasn’t only been focused on flexing its financial muscles but also trimming the fat.

Their operating expenses only increased by 5% year-over-year. They're also on track to deliver at least $4 billion in net cost savings by the end of 2024.

Clearly, Pfizer's been pinching pennies harder than a Depression-era grandma.

Now, let's talk about Pfizer's pipeline – the real meat and potatoes here. In 2023 alone, they got FDA approvals for 9 new drugs. That's more approvals than a helicopter parent gives on prom night. And they're not stopping there.

By the end of 2024, they're expecting to launch 20 new products or indications. It's like they're running a drug development assembly line over there.

Notably, Pfizer's oncology segment is quickly growing. Sales hit almost $4 billion in Q2, and with the recent acquisition of Seagen, they're positioning themselves as the oncology powerhouse of the future.

We're talking about a potential market size of over $300 billion by 2030. That's enough zeros to make your head spin faster than a centrifuge.

And let's not forget about their market dominance. Prevnar 20 is ruling the pediatric segment with over 80% market share in the U.S.

But the real dark horse here is their foray into the obesity market. With their GLP-1 agonist in development, they're eyeing a piece of a market that's expected to hit $100 billion by 2030.

Next, let's get down to the nitty-gritty of R&D. Pfizer's been pouring money into research like it's watering a money tree.

They spent a whopping $11.4 billion on R&D in 2023, up 10% from the previous year. That's about 15.7% of their revenue – higher than the industry average of 13.4%.

But despite all this good news, Pfizer's stock is trading at just 11 times projected earnings. In fact, Wall Street analysts are giving modest EPS growth projections.

In my humble opinion, though, a fair valuation for Pfizer should be at least 15 times earnings. And with a dividend yield above 5.5% for the next few years, it's like getting paid to wait for the market to wake up and smell the antibiotics.

Of course, it's not all rainbows and unicorns in Pfizer-land.

They've got some patent expirations coming up that could hit sales harder than a heavyweight boxer. Between 2025 and 2030, they're facing potential losses on products that generated $17 billion in peak sales. That's a pill even Pfizer might have trouble swallowing.

And let's not forget about the elephant in the room – healthcare reform.

With politicians yakking about drug pricing like it's the latest reality TV drama, there's always a risk of regulatory headwinds. But Pfizer's diverse portfolio and global reach give it more shock absorbers than a monster truck.

So, what's the play here? Well, assuming Pfizer keeps managing costs like a coupon-clipping grandma, they could easily beat current forecasts by 10% or more by the end of 2024.

If the market finally recognizes Pfizer's potential and grants it a P/E ratio of 14x, we're looking at a price target of $43.4.

That's a 42% upside from the recent closing price – more juice than you'd get from a whole orchard of oranges.

So, here's the bottom line: Pfizer's current stock price is criminally undervalued. With its robust pipeline, improving margins, and commitment to dividends, I'm suggesting you buy this stock faster than you can say "take two and call me in the morning."

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

August 6, 2024

Fiat Lux

Featured Trade:

(HOW TO EXECUTE A MAD HEDGE TRADE ALERT)

Nvidia, the world leader in graphics processing units (GPUs), has hit a significant roadblock in its highly anticipated Blackwell B200 chip launch. A design flaw, discovered late in the production process, has forced the company to delay the release of these powerful chips, expected to be a game-changer in the artificial intelligence (AI) landscape. This unexpected delay could have ripple effects throughout the tech industry, particularly for companies heavily invested in AI development and those relying on Nvidia's hardware to power their AI initiatives.

The Blackwell B200: A Promise of AI Power

The Blackwell architecture, Nvidia's next-generation GPU design, was poised to revolutionize AI computing. The B200, the flagship chip in this series, promised to deliver unprecedented performance and efficiency for AI workloads, such as training large language models and powering complex AI applications. The chip's advanced features, including a massive increase in processing power, improved memory bandwidth, and enhanced energy efficiency, made it a highly sought-after component for data centers and AI researchers worldwide.

Nvidia's partners, including tech giants like Microsoft, Meta, and Google, had eagerly awaited the B200's arrival, hoping to leverage its capabilities to accelerate their AI projects and gain a competitive edge in the rapidly evolving AI landscape. The chip's delay, therefore, has come as a major disappointment, leaving these companies scrambling to adjust their plans and potentially delaying their own AI initiatives.

The Design Flaw: A Late Discovery

The design flaw, reportedly discovered by Nvidia's manufacturing partner Taiwan Semiconductor Manufacturing Company (TSMC), affects the processor die connecting two Blackwell GPUs on a single board. This critical component, responsible for communication and data transfer between the GPUs, was found to have a defect that could impact the chip's performance and reliability.

The late discovery of this flaw, unusually late in the production process, has raised concerns about Nvidia's quality control and testing procedures. The company typically conducts rigorous testing throughout the chip development cycle to identify and address any potential issues before mass production. However, in this case, the flaw managed to slip through the cracks, resulting in a costly and embarrassing delay.

Consequences of the Delay

The delay of the B200 chip is expected to have significant ramifications for Nvidia and the broader tech industry. For Nvidia, the delay could impact its financial performance, as the company had projected strong sales of the B200 to its major partners. The setback could also tarnish Nvidia's reputation as a reliable provider of cutting-edge AI hardware, potentially opening the door for competitors like AMD to gain market share.

For Nvidia's partners, the delay could disrupt their AI development timelines and force them to reconsider their hardware choices. Some companies may opt to wait for the B200 to become available, while others may explore alternative solutions from other vendors. This could create opportunities for AMD and other GPU manufacturers to capitalize on Nvidia's misstep and attract new customers.

The delay could also slow down the pace of AI innovation, as researchers and developers who were counting on the B200's capabilities may have to scale back their ambitions or delay their projects. This could have a ripple effect on various industries that are increasingly relying on AI to drive growth and efficiency, such as healthcare, finance, and transportation.

Nvidia's Response

Nvidia has acknowledged the design flaw and is working to rectify the issue. The company has stated that it is revising the chip's design and will conduct further testing with TSMC before resuming mass production. Nvidia has also assured its partners that it is committed to delivering the B200 as soon as possible, but the revised timeline now extends into 2025.

Looking Ahead

The delay of the Blackwell B200 chip is a significant setback for Nvidia, but it is not necessarily a fatal blow. The company has a strong track record of innovation and has overcome challenges in the past. However, the incident serves as a reminder that even industry leaders are not immune to mistakes and that the development of complex technology like GPUs is fraught with risks.

As Nvidia works to address the design flaw and resume production of the B200, the AI community will be watching closely. The chip's success or failure could have a major impact on the trajectory of AI development and the competitive landscape in the GPU market.

Mad Hedge Technology Letter

August 5, 2024

Fiat Lux

Featured Trade:

(A GREAT OPPORTUNITY FOR TECH INVESTORS)

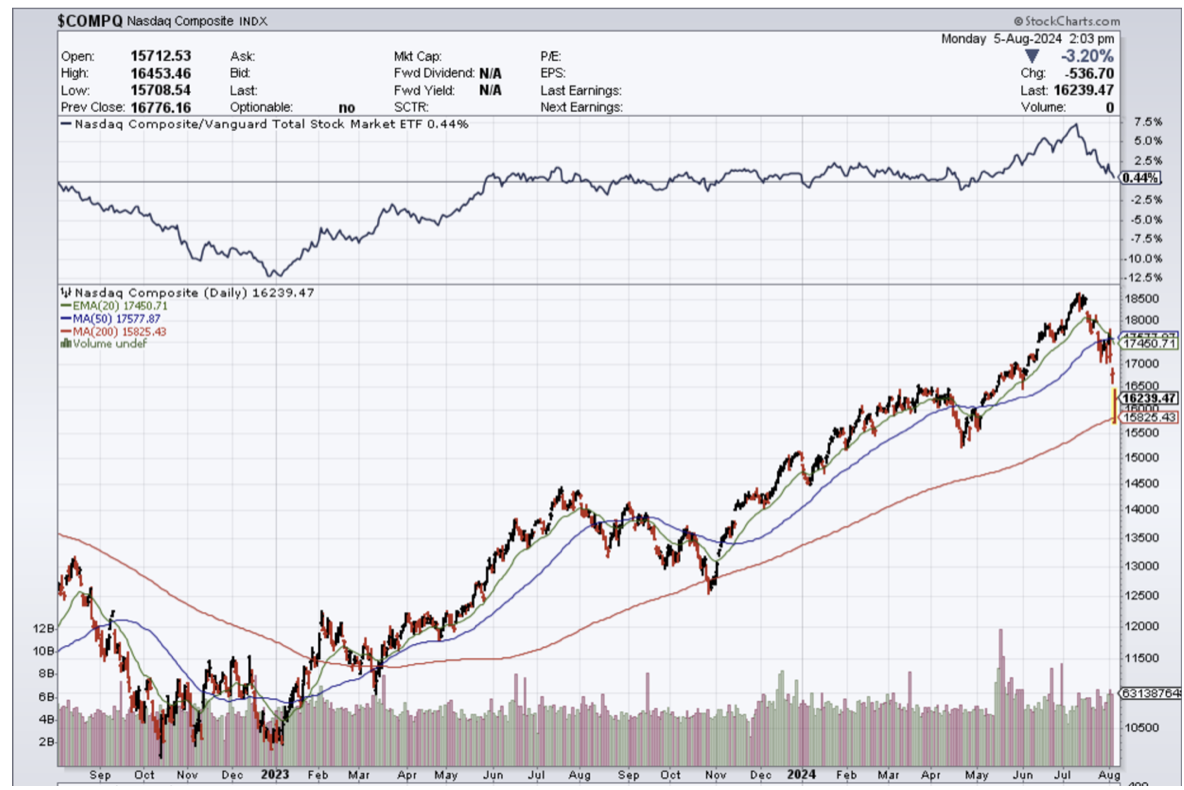

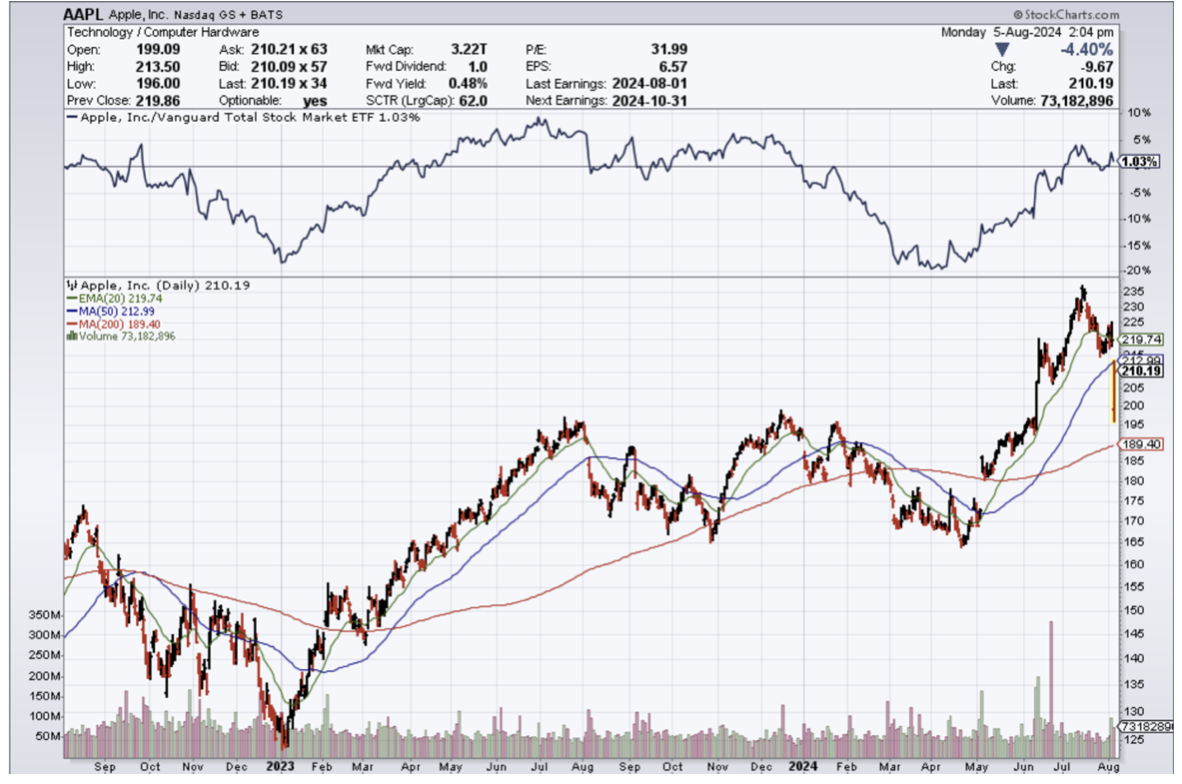

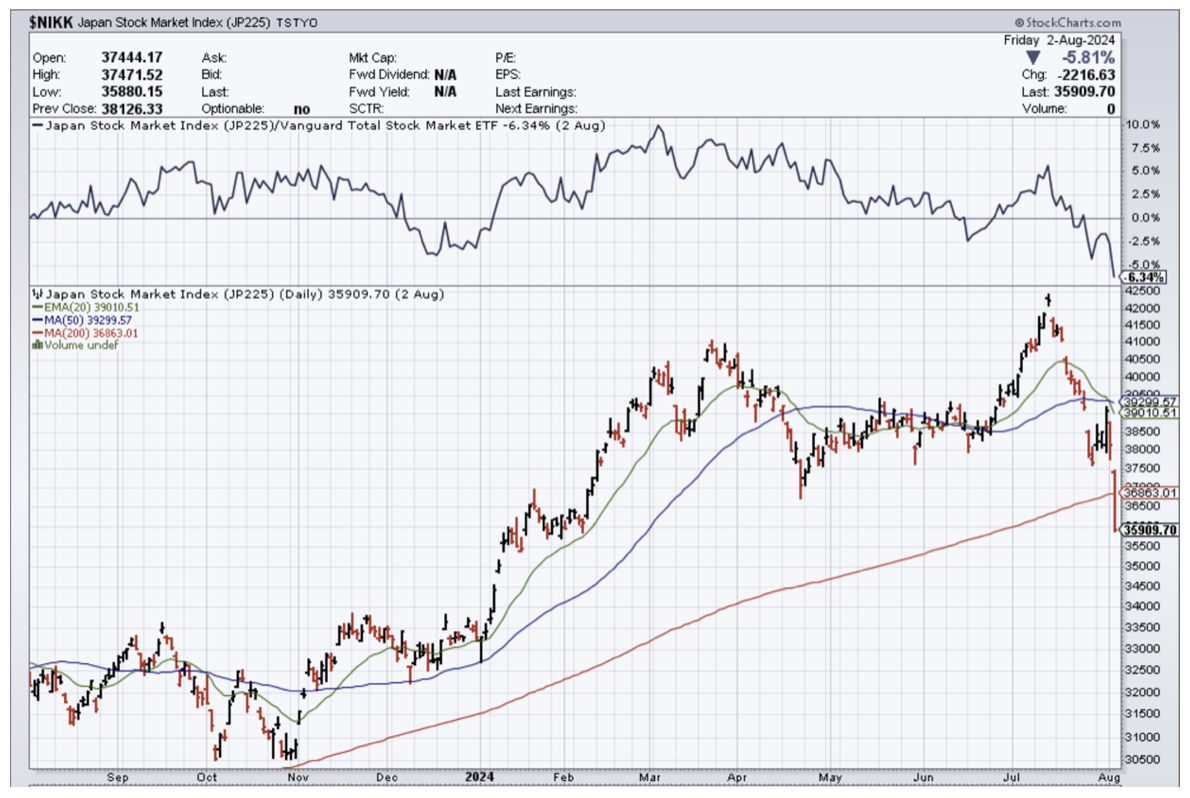

($COMPQ), (AAPL), ($NIKK)

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

We avoided the big one.

That’s a common utterance in Japan when the Japanese believe they avoided devastation when it comes to earthquakes.

The same goes for US tech stocks today.

Sure, raising interest rates when the Japanese economy is contracting is something a schoolboy wouldn’t do, but that is what took place and U.S. tech stocks ($COMPQ) are dealing with the devastating aftermath.

Japan is in a rock and a hard place in terms of monetary policy - orders were sent through to Bank of Japan governor Kazuo Ueda to protect the yen at all costs.

It was a totally political move.

Then the Japanese yen exploded higher after Ueda raised rates a measly 25 basis points, but by mistake crashed the U.S. tech sector and the Japanese stock market ($NIKK) which is down around 25% in the past month.

All this talk about the economy going into recession is too early.

It is also highly positive for US tech stocks that this crash was provoked in Japan and has nothing to do with structural issues to the US economy or tech sector.

I do agree that the US economy is slowing and hiring is getting worse, but the economy is still growing, unlike Japan.

Therefore, this is a swift overreaction from another policy error from the Japanese establishment. The Bank of Japan is also out of bullets on the monetary side of things. One and done.

Japan could be the worst-run country in the world which is why most foreigners want to briefly visit to eat sushi and leave.

The Japanese will soon eclipse the 300% debt per GDP threshold – a practice of pile-driving a country completely into the ground while demoralizing the local youth and their fragile future hopes.

So I’ll get to the meat and bones of it.

This will be a big dip to buy into and the hard landing narrative should be delayed by a few months because data is still too good to ignore.

The major tech companies have been priced for perfection for quite some time now. But doubts over AI, which incurs high costs today for uncertain returns in the future, have crept in and started to unnerve investors.

Chipmaker Intel plans to cut a huge chunk of its global workforce while pocketing $8 billion from the federal government. The transformation into lean staffing continues in Silicon Valley and won’t stop.

Now what?

The tech stock freakout does make it much easier for the Fed to push through a half-point rate hike rather than a quarter-point rate cut in September, which really puts a floor under tech stocks. I could argue that this would inject rocket fuel into a possible winter rally.

I highly doubt that tech stocks will suffer real panic before the US election because imagine a boatload of democratic voters who are the ones mostly owning tech stocks going to the polls grumpy, frustrated, and confused as to why their 401k has been flushed down the toilet.

This is most likely the biggest dip in the best of tech that we will get before the US election. Embrace and execute.

Warren Buffett unloading half of his Apple (AAPL) position almost suggested that he knew something before the rest of us, but I do believe that he will regret selling out so early. He is deep in the know in Japan and stateside.

He will need to buy tech back at a higher price, but he can afford it. Most of the rest of us must execute like a miracle depended upon it and that’s why I am here to guide you through the fog of war.

Buy the dip in tech shares.