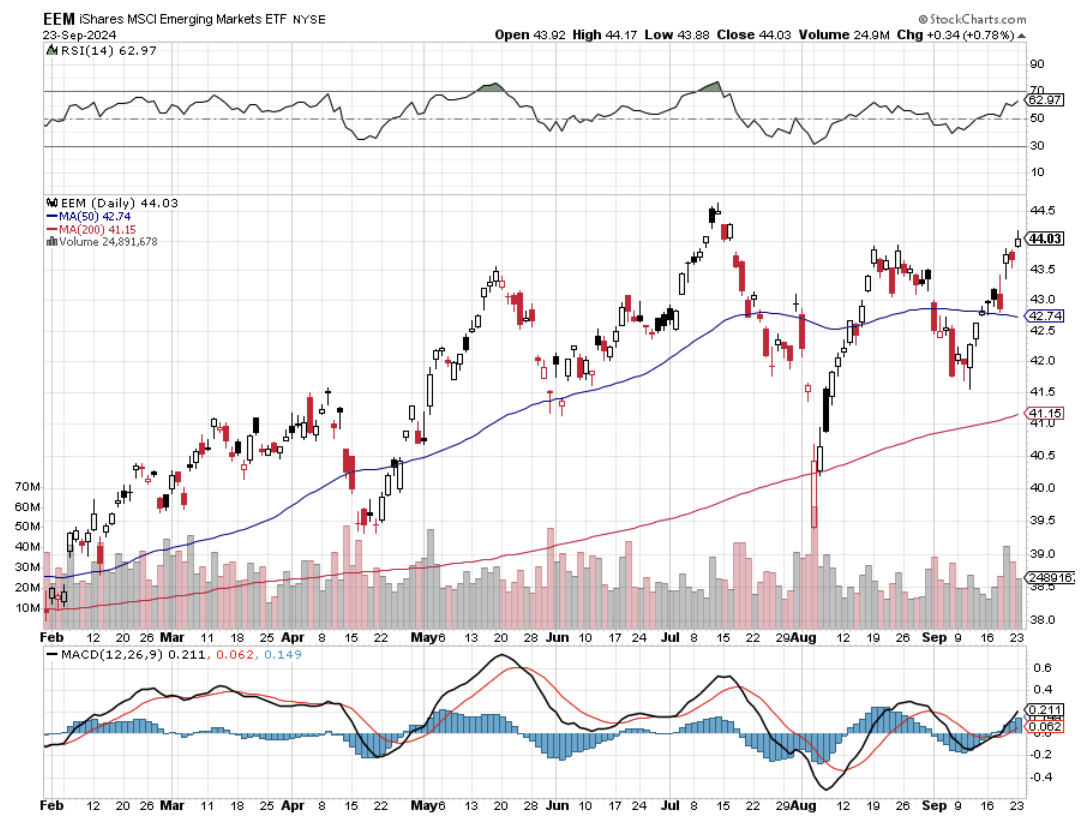

I managed to catch a few comments in the distinct northern English accent of Jim O'Neil, the fabled analyst who invented the “BRIC” term, and who was later kicked upstairs to the chairman's seat at Goldman Sachs International (GS) in London.

Now that the US dollar is in free fall, Jim thinks that it is still the early days for the space, and that these countries have another ten years of high growth ahead of them. As I have been pushing emerging markets all year, this is music to my ears.

By 2030, the combined GDP of these emerging markets, Brazil (EWZ), India (PIN), and China (FXI), will match that of the US. The “BRIC” term is no longer used because the Ukraine War has made Russia the Pariah of international investment.

China alone will reach two-thirds of the American figure for gross domestic product. All that requires is for China to maintain a steady 5% annual growth rate for six more years, the official Beijing forecast, while the US plods along at an arthritic 3.0% rate. China's most recent quarterly growth rate came in at low single digits.

“BRIC” almost became the “RIC” when O'Neil was formulating his strategy two decades ago. Conservative Brazilian businessmen were convinced that the then-newly elected Luiz Ignacio Lula da Silva would wreck the country with his socialist ways.

He ignored them and Brazil became the top-performing market of the G-20 since 2000. An independent central bank that adopted a strategy of inflation targeting was transformative.

This is not to say that you should rush out and load up on emerging markets tomorrow, as they are still being weighed down by weak commodity prices. This will go away.

American big-cap technology stocks are the flavor of the day, and as long as this is the case, emerging markets will continue to blend in with the wallpaper. Still, with growth rates triple or quadruple our own, they will not stay “resting” for long.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/03/China.jpg268339april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-09-24 09:04:462024-09-24 11:19:13The Long View on Emerging Markets

It's been two years since ChatGPT burst onto the scene, and the artificial intelligence world is facing a serious reality check. The skyrocketing energy costs of building and running bigger AI models are putting the brakes on progress.

But before we start sounding the alarm bells, let's take a closer look.

Let's not mince words: large language models are energy hogs. Training OpenAI's GPT-4 model gobbled up enough juice to power 50 American homes for a century.

And as these models bulk up, so do the bills. Today's behemoths cost about $100 million to train. The next generation? We're looking at $1 billion. And the one after that? A cool $10 billion.

And it doesn't stop there. Every time you ask an AI to do something, it's like running up a tab. Summarizing financial reports for all 58,000 public companies worldwide could set you back anywhere from $2,400 to $223,000.

Over time, these "inference" costs can outstrip the initial training expenses. If that's the case, how can generative AI ever become economically viable? This scenario is enough to make any investor uneasy, especially those who've gone all-in on AI.

Just look at Nvidia (NVDA), the chip designer powering most AI models. Its market cap has ballooned by $2.5 trillion in two years.

Venture capitalists have poured nearly $95 billion into AI startups since 2023 kicked off.

And OpenAI? They're reportedly gunning for a $150 billion valuation, which would make them one of the biggest private tech firms on the planet.

But before you start panic-selling, take a breath. We've been here before with other game-changing technologies.

Remember when getting to space seemed impossible? Those innovations now power our everyday lives.

The 1970s oil crisis? It kickstarted energy efficiency and alternative power sources. Fracking made previously untouchable oil and gas reserves accessible, turning America into the world's top oil producer.

We're already witnessing similar creativity in AI.

For example, companies are now developing chips specifically designed for the operations required to run large language models. This specialization allows them to operate more efficiently than general-purpose processors like those from NVIDIA.

Tech giants like Alphabet (GOOGL), Amazon (AMZN), Apple (AAPL), Meta Platforms (META), and Microsoft (MSFT) are all designing their own AI chips.

In fact, more money has flowed into funding AI-chip startups in the first half of this year than in the past three years combined.

At the same time, the industry is rethinking its approach to AI models. The mantra of "bigger is better" is giving way to a focus on smaller, more specialized systems.

OpenAI's newest model, O1, focuses on reasoning rather than text generation. Other developers are streamlining calculations to squeeze more performance out of existing chips. By mixing and matching models for different tasks, they have slashed processing times.

Taking a good look at how AI companies are pivoting these days, it's clear that the old tech playbook is getting tossed out the window.

Remember when we all thought the big incumbents were untouchable? Well, in the world of AI, that idea's about as useful as a screen door on a submarine. Simply put, the game has changed.

While NVIDIA currently sells four-fifths of the world's AI chips, specialized rivals could start eating into its market share. Already, Google's AI processors are the third most used in data centers worldwide.

OpenAI may have kicked off the large language model craze, but as resource constraints bite, rivals like Anthropic, Google, and Meta are catching up fast.

There's still a gap between these heavyweights and second-tier models like France's Mistral, but it's narrowing.

So, if the trend towards smaller, specialized models continues, we might see a galaxy of AI models instead of just a few superstars. Keep an eye out for these up and coming challengers.

I do believe companies heavily involved with gig workers will not experience a boon in the stock price in the near future.

Consumers are tapped out and there is not much more pricing power they can pass on to manufacture higher profits in the short run.

There is a chance the tide will rise with all boats, but I would wait this one out in gig work stocks.

As a cultural phenomenon, the gig economy is here to stay until they get muscled out by technology.

Americans are used to the 24-hour on-demand goods and services offered by gig workers.

The number one expense line item for these tech companies is labor.

They are actively working to try and reduce the burden.

I believe they are holding out until the vaunted robotaxi is green-lighted.

This change will crater labor expense to a pittance with most of the labor costs flowing towards the managers and executives.

It is the holy grail of the tech industry and we are rapidly approaching this inflection point.

These companies have come a long way.

In 2010, the smartphone application offered a new competitor to the taxicab industry by linking a paying passenger with a private driver using his or her own car.

The largest services are still focused on transportation. Uber and Lyft dominate the on-demand ride business.

Massive retailers like Walmart and Amazon joined in with their own on-demand platforms: Spark Driver and Amazon Flex.

Gig workers are recruited with the situation of flexible hours to earn additional income. However, as independent contractors, gig workers are not entitled to traditional employment benefits like health insurance, and they must take on additional occupational risks, equipment costs, and tax burdens.

In a 2024 economic impact report, Flex, a federal lobbying association supported by DoorDash, Grubhub, HopSkipDrive, Instacart, Lyft, Shipt, and Uber, estimated there were about 7.3 million “active drivers and delivery partners on major rideshare and delivery platforms” in 2022.

A 2022 report published by the consultancy McKinsey & Co. surveyed workers and estimated as many as 58 million Americans, or 36 percent of the U.S. workforce, did some gig work that year.

In its Securities and Exchange Commission filings, Uber describes the classification of its drivers as “employees, workers, or quasi-employees” as an “operational risk” to its business. The same document details the various legal and political challenges involved in maintaining independent contractor status.

Uber’s latest quarterly filing, published in August, said that if drivers win the reclassification through legal means or the passage of new laws, the company would incur significant expenses for compensating drivers and would pass its elevated costs onto riders. Uber also argues reclassification would limit its ability to find workers due to a loss of flexibility.

Uber is smart at attempting to root out the labor expenses. If robotaxis are integrated into the business model, the stock would increase by 500%.

In the meanwhile, workers forget ahead hoping to procure more benefits from Uber.

Uber is hell-bent on avoiding the financial toll of paying full-time workers and will indefinitely try to pin the label of independent contractor on its workers.

This existential threat will end up in courtrooms and Uber has good enough lawyers to stall out the lawsuits.

All eyes are on Tesla and Elon Musk to give insight into what the future of gig work and autonomous transportation looks like.

Uber knows it cannot maintain the status quo and something must be done to cut labor costs.

If that does happen, the stock will quadruple in short time.

As for the short-term, buy big dips in Uber stock.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-09-23 14:02:182024-09-23 15:15:24Be Cautious About Stocks Tied To Gig Work

“The best investment you can make is in yourself.” – Said Warren Buffett

https://www.madhedgefundtrader.com/wp-content/uploads/2024/09/warren-buffet.png444312april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-09-23 14:00:392024-09-23 15:15:03September 23, 2024 - Quote of the Day

We’ve got a lot of data points to get through this week.

Consumer confidence in September is expected to have weakened.And that is really expected to be the overall theme in most data – weakness over strength, thereby giving validity to the Fed’s decision to go 50bps last week.

The Fed’s preferred inflation gauge, the August personal consumption expenditure price index that’s due out Friday is expected to show pricing pressures continuing to pull back from their highs.No doubt, this piece of data may well guide the Fed’s decision on the magnitude of rate cuts come November.

So, back to the rate cut theme, and we saw that the Bank of England maintained its steady course, keeping rates unchanged as August inflation figures failed to show further decline.

On Tuesday, the Reserve Bank of Australia meets.Rates are expected to remain unchanged.This comes amid a strengthening Aussie dollar, with AUD/USD closing at its highest level since January above 0.6800.

If you listen to the media, you will hear all the jibber jabber about the DOW reaching 42,000 for the first time and whether the market can continue to climb.(They are paid to talk, but you are not paid to listen! Take it all with a grain of salt). In other words, receive the information (if you watch/listen to T.V.) with some reservation as all of it may not be entirely credible.

You will also hear the many arguments explaining why the Fed went so big, and what the effects of that will be going forward, and into next year, and what the Fed will do in November and December.

Shut out all that noise.It tends to create confusion, rather than clarity.

The S&P500 is on track to reach the target I gave you many months ago – 5,745.And it will probably rally beyond that target going into year-end.

Next year may be a different story.

We may have many months of sideways movements, and quite possibly an extreme sell-off at some stage.

That sell-off, if it does take place, would create an excellent opportunity to scale into great stocks at cheap prices.

I will keep you up to date with my interpretation of the markets going forward.

But, for now, let’s stick to the present.

MARKET UPDATE

S&P500

Uptrend in progress. The September 6th low of 5403 can be interpreted as a completed corrective Wave ii of 5 and the market can now continue rallying within Wave iii of 5 toward a target of around 6,260.

Advance in progress.Bitcoin completed a complex correction on its August 5th low of $49,577.Now in its Wave 3 advanced toward a target of around $73,830.Support = $62,500/$61,330.

Next targets = $65,000, $68,650/$70,000

CONFLICTS CORNER

AUSTRALIAN CORNER

Housing affordability falls to the worst level on record.

Housing research group Prop Track’s annual Housing Affordability Index reveals the worst conditions for homebuyers on record as continued property price increases and decade-high interest rates remain stubborn.

The analysis found that a median-income household earning $112,000 annually could afford only 14% of all the homes sold last financial year, the smallest share since records began in the 1194-95 financial year.

Just three years ago, the same household could have comfortably purchased 43% of houses or units.

Property prices rose 6.6% nationally over the year to June, the equivalent of a %50,000 increase.The average first-home buyer household now must set aside a fifth of their income for 5.6 years to save a standard 20% deposit for the median home.

PropTrack economist Angus Moore comments that we are on “par with the last period of challenging affordability in 2008 and mortgage repayments today are only a little bit below what they were in the late 1980s and early ‘90s as a share of income.”

Low-income households are effectively locked out of the market, able to buy three in 100 homes.

Yellow Brick Road Home Loans executive chairman Mark Bouris says the reality is many millennials and Gen Zs will not be able to get a mortgage.

Sydney’s median home price is $1.5 million.Tasmania is now close behind.Just six years ago, Tasmania was the most affordable state.Victoria is a close third, with 12% of homes sold last year requiring 25% or less of pre-tax income to meet repayments,

South Australia experienced the most significant decline in affordability over the past year, with 16% of homes available to the state’s average earner.

Western Australia offers the best affordability, with more than a quarter of homes sold last year deemed affordable, followed by Queensland with 15% of properties.

Some relief is on the horizon.Major banks are forecasting rate cuts next year, which has the potential of returning hundreds of dollars into the pockets of mortgage holders each month and boosting new borrower’s limits.

Mr Bouris said it was unfair to lay blame for worsening affordability squarely at the feet of the RBA.He believes the federal government’s lax immigration policies, the state’s reliance on stamp duty revenues, and poor council planning all play a part in Australia’s housing crisis.

WHAT IS…?

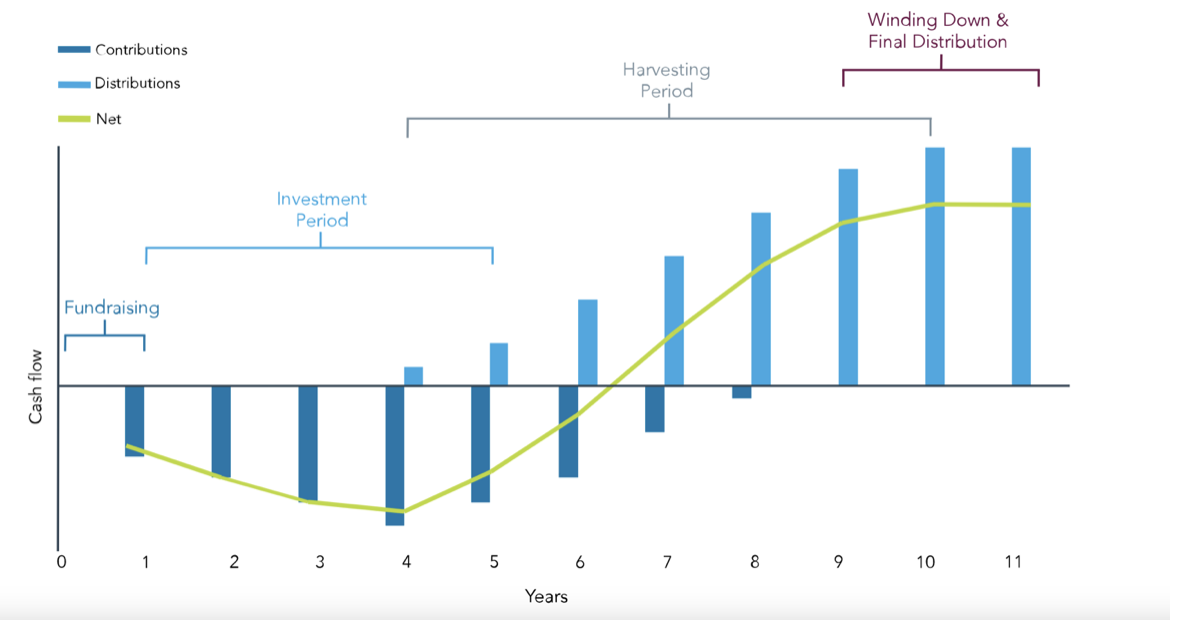

Private equity funds are designed to generate enhanced returns by pooling investors’ capital and investing in private companies to drive business growth, streamline operations, and/or support acquisitions.

Investors provide private equity fund managers with the capital needed to invest in strategically identified companies.Unlike public equity managers, private equity managers actively seek to work with management teams to improve companies with the goal of eventually selling shares at a profit and distributing those profits to investors.In return, fund managers receive a management fee, and a share of the returns generated by the fund, further incentivizing value creation and aligning the interests of fund managers, investors, and company management teams.

4/ Winding down & final distribution – exiting remaining positions.

Sample Life Cycle of a Private Equity Fund

Benefits:

Historically, private equity generates long-term outperformance relative to the public markets.

Private equity provides access to a larger investment circle with more opportunities than the public markets.

Private equity managers aim to create value by taking a long-term view, which can help reduce risk, particularly in uncertain markets.

A private equity allocation can provide enhanced return potential and diversification benefits (i.e. uncorrelated investment exposure in a portfolio).

Risk Considerations:

Private equity funds are considered long-term investments, typically with terms of seven to ten years.

Fees:equity fund managers usually charge an annual management fee of 1-2% of assets under management.They also collect performance fees, which can range from 10-20% of any value appreciation generated by the fund.

Private equity funds may use some form of leverage, which offers the potential for higher returns, cut also increases the downside risk.

Private equity funds may not be as transparent as traditional investments, which are required to provide frequent and full disclosures.

QI CORNER

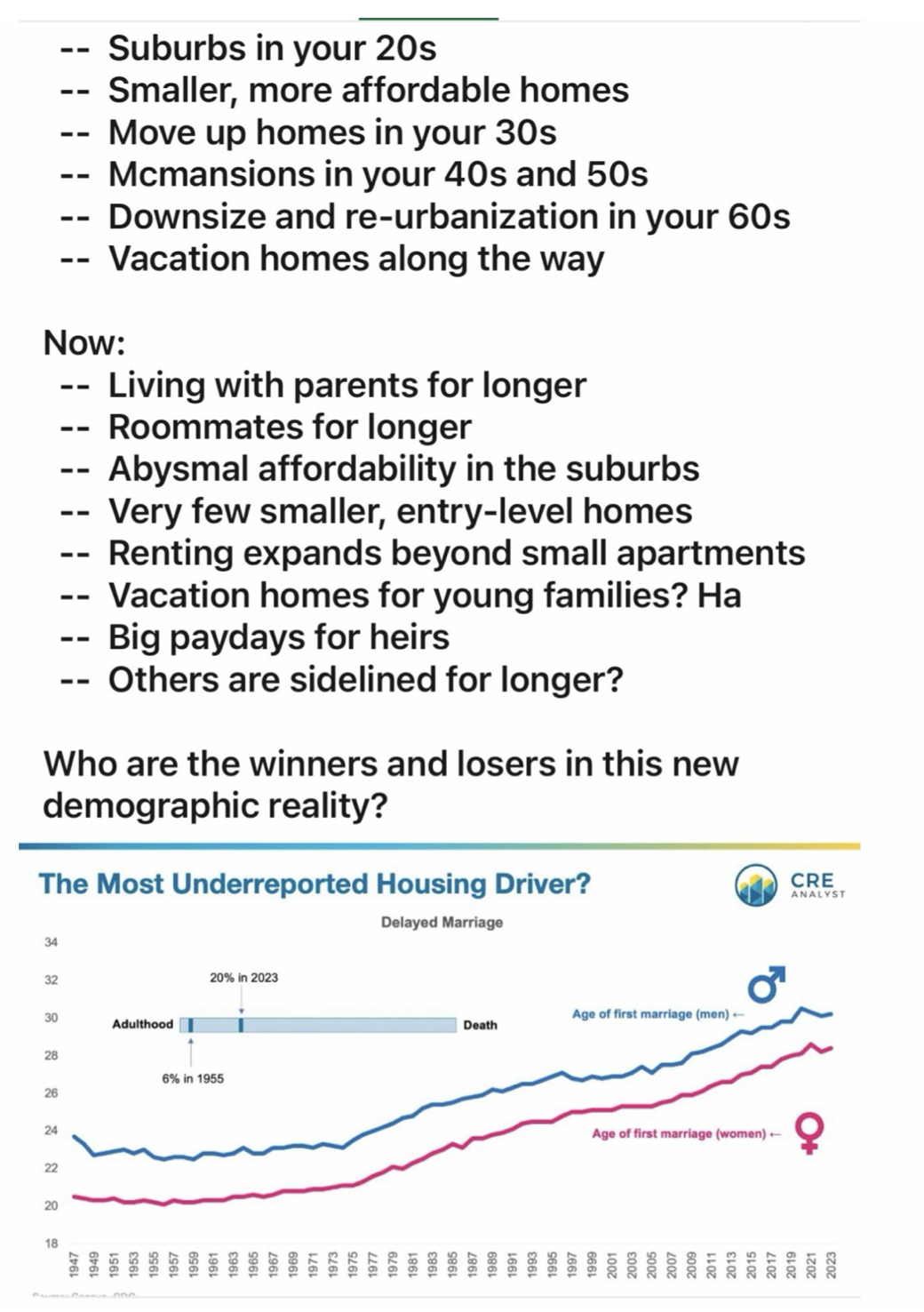

We are witnessing a cultural shift in the average age of marriage and overall marriage rates, couples with the challenges of high entry-level home prices and mortgage interest rates.As a result, many young individuals are opting to rent for more extended periods of their lives.This trend may signal the beginning of a new era where North Americans embrace lifelong renting, akin to many European countries.

The evolving dynamics in marriage and housing choices are likely to have intriguing implications for different real estate asset classes investment returns over the next decade.

(Ross W. McBride, Experienced Real Estate Investment Professional)

Global Market Comments

September 23, 2024 Fiat Lux

Featured Trade:

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD or THE DOCTOR JEKYLL AND MR. HYDE MARKET),

(NVDA), (MSFT), (GLD), (NEM), (TSLA). (CCJ), (DHI), (TLT)

I have to tell you that every year I do this, calling the market gets easier and easier. That’s because when you go from year 62 to 63 in the market, you actually learn quite a lot.

What gets more frustrating every year is convincing people to execute my trades because they are increasingly out of consensus, as opposed to conventional wisdom, tradition-shattering, or downright Mad.

Nuclear stocks? Are you out of your mind? Haven’t you heard of Three Mile Island?

So, the Fed went with 50.

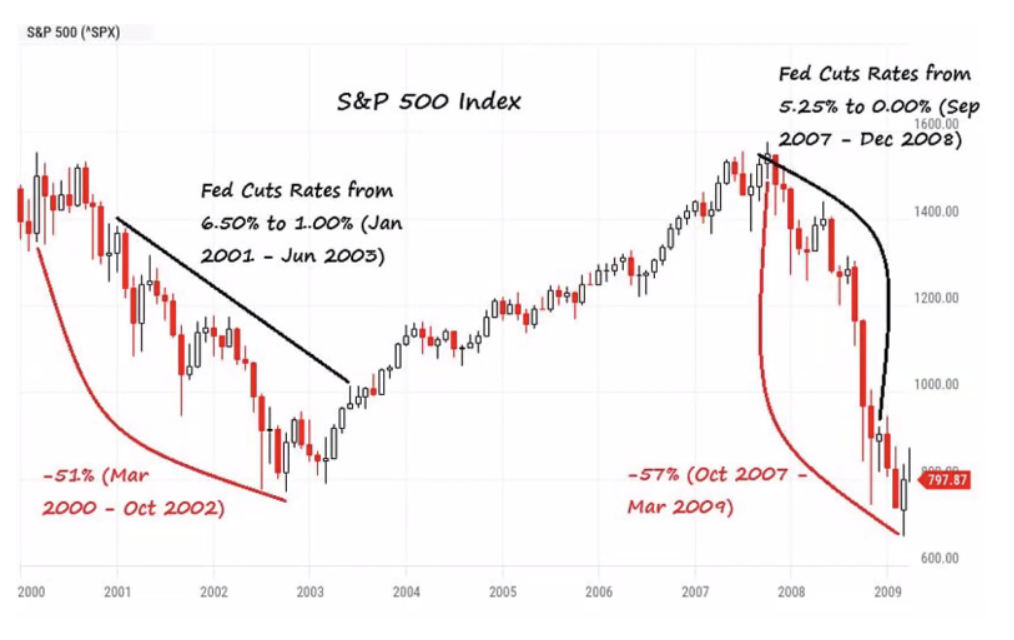

Initially, the stock reaction was “Oh my gosh, the free lunch is bigger than we thought!” By the close, this morphed to “Oh my gosh, the economy must be worse than we thought!” This opens the way to another possible 50 basis point rate cut in November, which happens to be the day after the presidential election. It only took 5 seconds for most investors to realize that they had way too much cash.

By acting so aggressively and out of character, Fed governor Jay Powell is admitting that he blundered, blew it, dropped the ball, and scored an own goal all at once by not lowering interest rates in July.

By doing his best impression of a deer frozen in the headlights in H1, all Powell got us were six more weeks of job losses, taking the headline Unemployment Rate up to 4.2%.

Don’t get too complacent though. Look at the chart below and you will see that when the Fed began an aggressive round of interest rate cuts in 2007, the market launched into a major crash of 57%.

Dow 42,000.

It may seem commonplace and ordinary for mere mortals to see this number. But for those of us who remember when it was only 600 back in 1982 (and predicted to immediately plunge to 300 by the late Joe Granville), we are now in the realm of science fiction.

However, in Q3 this year, the character of the bull market suddenly changed, from a Dr. Jekyll to a Mr. Hyde. The Magnificent Seven has shrunk to the Pitiful Seven, with long boring sideways-range trades. In the meantime, growth and interest rate-sensitive value stocks that I have been pounding the table about for six months have begun trading like red-hot must-own biotech IPOs.

The choice is very simple. Do I buy a stock that has a single-digit price-earnings multiple that is flying like a bat out of hell, or do I choose an incredibly expensive tech stock with a PE multiple of 27X or worse that is stagnating?

I know what I’m going to do with my money, which reached new all-time highs almost every day this month. I’ll go with the former all day long.

Don’t get me wrong. The Mag Seven aren’t going to stay out of favor for very long. It’s like holding a basketball underwater that keeps inflating. Their earnings are still growing at an explosive rate. Personally, I think Nvidia (NVDA) will hit $160 a share by early 2025.

If there is one common factor in all financial markets today, it is the vast underestimation of the potential of AI and the impact on stock prices, which keeps surreptitiously sneaking into our lives every day.

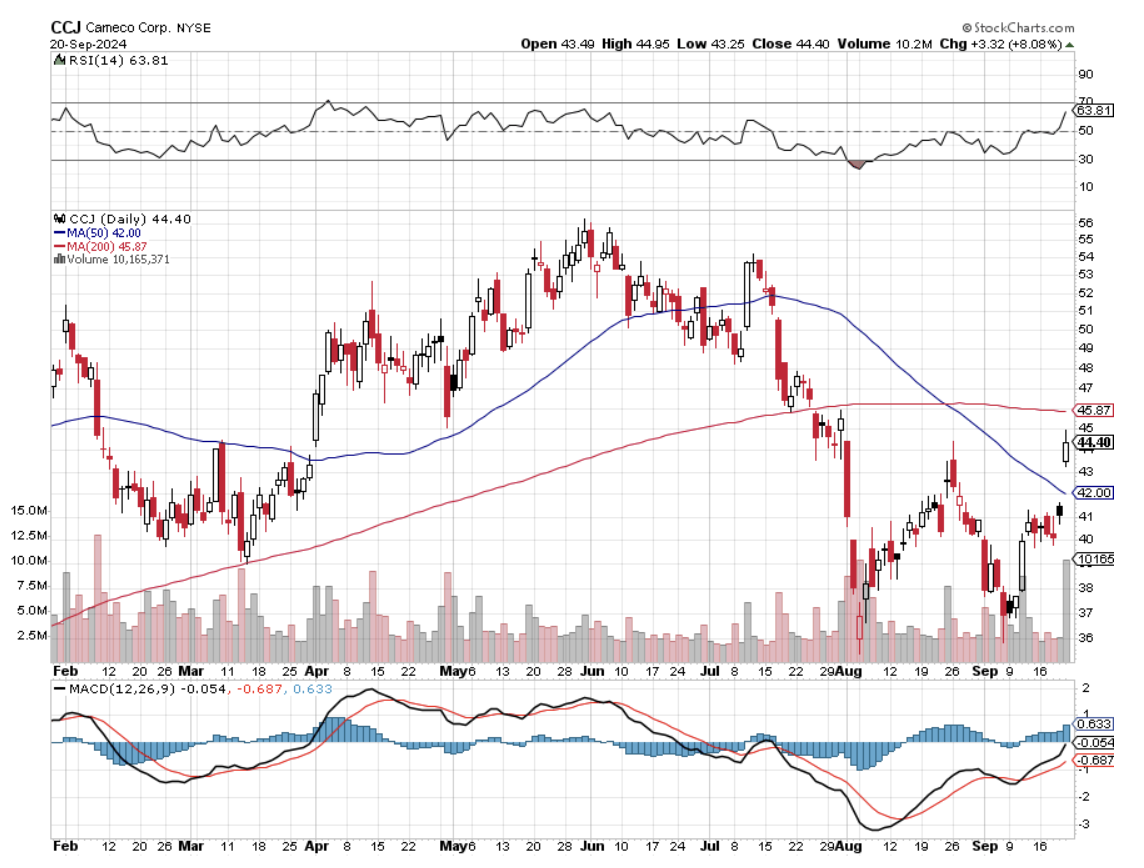

My Cameco (CCJ) trade alert came through in a week, immediately tacking on 10%. I have to tell you that reading my email, there is a lot of demand for positions that rise by 15% in a week. But that is better than the two-week wait for the Concierge clients who bought the 2026 $40-$42 LEAPS for only 75 cents. The consolation is that they will make a lot more money, potentially some 167% by expiration. The big money is always made with long-term trades.

I can honestly say that I put 54 years of work into this trade, dating back to when I started my work at the Atomic Energy Commission Nuclear Test Site in Nevada. While advanced nuclear power plant design and fuels (low enriched uranium oxide with an M5TM zirconium-based cladding) have been around for a long time, the industry had the kiss of death on it thanks to Three Mile Island (watch the movie China Syndrome), Chornobyl, and Fukushima.

It was going to take someone bold with deep pockets to restart this industry. Then out of the blue Microsoft (MSFT) announced the reopening of Three Mile Island, the site of the worst nuclear accident in US history in 1979.

Constellation Energy announced Friday that its Unit 1 reactor, which closed five years ago, is expected to be revived in 2028, dependent on Nuclear Regulatory Commission approval. Microsoft will purchase the carbon-free energy produced from it to power its data centers to support artificial intelligence.

Twelve U.S. nuclear power reactors have permanently closed since 2012, with the most recent being Indian Point 3 on April 30, 2021. Another seven U.S. reactor retirements have been announced through 2025, with a total generating capacity of 7,109 MW (equal to roughly 7% of U.S. nuclear capacity).

I have a feeling that all of these will get reopened, which cost about $4 billion each to build and can be bought now for pennies on the dollar. In the meantime, the world’s largest uranium supplier, Kazakhstan, is cutting supplies. Buy all nuclear plays in dips.

I have to tell you that this was one of those weeks that by making 6.74% it makes all the barbarically early mornings and exhausting late nights worth it. While all my friends are working on their golf swings or improving their bowling scores, I am scoring the Internet search for the next original investment theme. Every customer I have spoken to lately is having a great year.

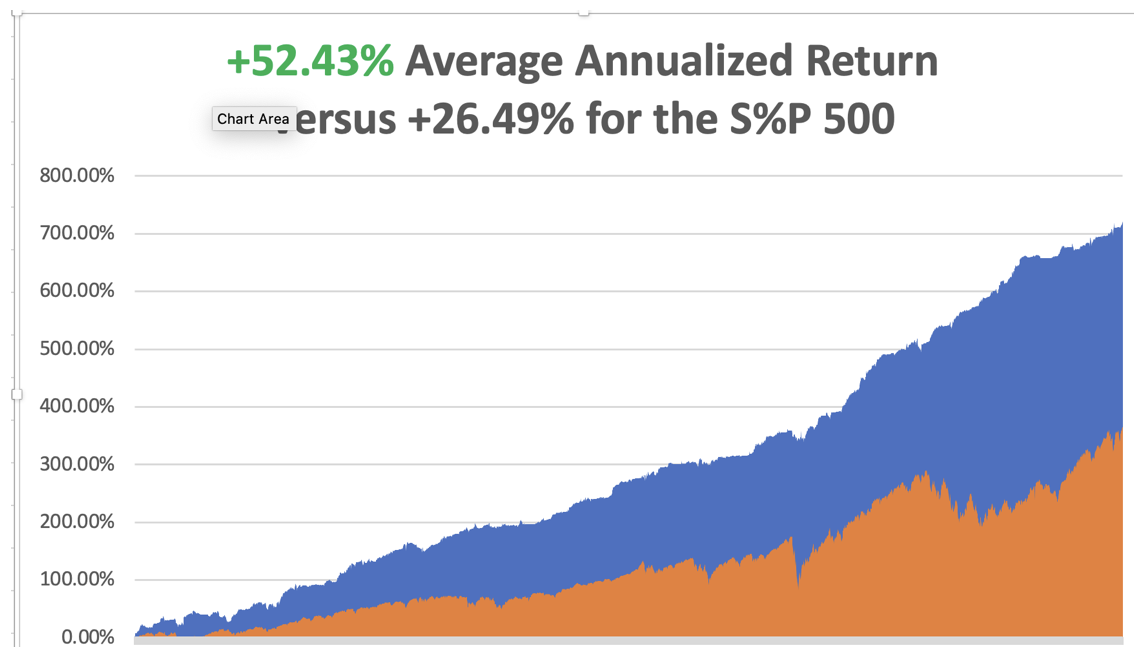

So far in September, we are up by a spectacular +9.67%. My 2024 year-to-date performance is at +44.36%.The S&P 500 (SPY) is up +19.08%so far in 2024. My trailing one-year return reached +63.00%. That brings my 16-year total return to +720.99%.My average annualized return has recovered to +52.43%.

I front-ran the Fed move by adding positions in interest rate sensitives like (GLD), (NEM), and (TSLA). I added (CCJ) based on the arguments above. Once the Fed showed its hand, I added another interest rate sensitives with (DHI). I also added a short in (TLT).

My logic on (TLT) was very simple. I think it is safe to say that we won’t have any downside surprises in interest rates until the next Fed meeting on November 6. We don’t even get a Nonfarm Payroll Report until October 4.

In any case, the bond market has already fully priced in half of the 250 basis points worth of interest rate cuts now discounted by the June Fed futures markets. We have just witnessed a massive $20 rally off the (TLT) bottom. Upside surprises in prices from here should be nil.

If you couldn’t get into (TLT), you are not alone. As soon as the big hedge funds saw my trade alerts, they started hammering not only the options market but the underlying bond market as well with several large $100 million sales. That pushed the trade to near max profit almost immediately and made my trade alert impossible to execute.

At The Economist, they used to say that imitation is the sincerest form of flattery.

Some 63 of my 75 round trips, or 90%, were profitable in 2023. Some 57 of 75 trades have been profitable so far in 2024, and several of those losses were break-even. That is a success rate of +76%.

Try beating that anywhere.

FedEx Gets Crushed 10%, on disappointing earnings and guidance. Cost control is a big issue. Right now, investors are presented with the Dow Industrials at all-time highs and Transports barely positive for the year. Transports are up just 2.7% year to date, and a 13% drop in FedEx shares early Friday will likely drag it into the red for 2024. Buy (FDX) on dips, a great economic recovery play.

Existing Home Sales Drop 4.2%, in August to a seasonally adjusted annualized rate of 3.86 million units, according to the National Association of Realtors. There were 1.35 million units for sale at the end of August. That’s up 0.7% from July and up 22.7% year over year. median price of an existing home sold in August was $416,700, up 3.1% from August 2023, a new all-time high. Real estate should pick up once lower interest rates feed through.

Weekly Jobless Claims Hit 4 Month Low at 219,000. This flies in the face of yesterday’s 50 basis point rate cut by the Fed yesterday based on a weakening jobs market.

Alaska Airlines Takeover of Hawaiian Gets Approval, in a rare case of agreement from the government. The Feds have opposed the most concentration of industry. I think without the deal Hawaiian would have gone under. Expect prices to go and services to decline. Avoid the airlines.

Berkshire Hathaway Cash Approaches $300 Billion. Berkshire ended the second quarter with cash and equivalents (mostly Treasury bills) of $277 billion, up from $168 billion at year-end 2023, mostly due to heavy sales of Apple (AAPL). It highlights how much money is sitting on the sidelines waiting to come in on the next dip. It's also an indication that in the 75 years of Warren Buffet’s investing experience, stocks are expensive.

The Entire Energy Sector is About to Double, once the Chinese economy starts to recover. A recovering US economy powered by lower interest rates will also help. Everything from oil futures to master limited partnerships and stocks are on sale with the highest dividends in the market. It’s almost the only place Warren Buffet is buying.

Amazon Puts AI to Work, using it to plan new delivery routes which saves time and millions of gallons of gasoline. It’s a simple application with vast results. It all goes straight to the bottom line. AI is spreading throughout the economy far faster than most people realize. Buy (AMZN) on dips.

Foreign Direct Investment into China Collapses, down 31.5% in the first eight months of 2024 the Chinese Commerce Ministry said on Saturday. This could be a drag on the recovery of global commodity prices.

US Import Prices are in Free Fall, showing the biggest drop in eight months in August, driven by a broad decline in the costs of goods.

Ebbing price pressures give the Federal Reserve ample room to focus on the labor market which has slowed considerably from last year's robust job growth. Expectations of lower interest rates as well as slowing inflation results are making people feel better about the outlook for the economy.

Foreign Investors Pour $31 Billion into Emerging Markets in August. Fixed income funds ex-China accounted for $27.8 billion of inflows, with $1.4 billion funneled to Chinese debt, the data show. The net inflow to stocks stood at $1.7 billion despite a $1.5 billion outflow from Chinese equities. It’s all about falling US interest rates and a US dollar that is expected to be weak for years.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 23 at 8:30 AM EST, the S&P Global Flash PMI is out On Tuesday, September 24 at 6:00 AM, the S&P Case Shiller National Home Price Index is released.

On Wednesday, September 25 at 7:30 AM, New Home Sales are printed.

On Thursday, September 26 at 8:30 AM EST, the Weekly Jobless Claims are announced. We also get the final read on Q2 GDP.

On Friday, September 27 at 8:30 AM, we learn the Fed’s favorite inflation indicator, the Core PCE Price Index. At 2:00 PM EST, the 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when the Cold War ended in 1992, the United States judiciously stepped in and bought the collapsing Soviet Union’s entire uranium and plutonium supply.

For good measure, my client George Soros provided a $50 million grant to hire every Soviet nuclear engineer. The fear then was that starving scientists would go to work for Libya, North Korea, or Pakistan, which all had active nuclear programs. They ended up here instead.

That provided the fuel to run all US nuclear power plants and warships for 20 years. That fuel has now run out and chances of a resupply from Russia are zero. The Department of Defense attempted to reopen our last plutonium factory in Amarillo, Texas, a legacy of the Johnson administration.

But the facilities were deemed too old and out of date, and it is cheaper to build a new factory from scratch anyway. What better place to do so than Los Alamos, which has the greatest concentration of nuclear expertise in the world?

Los Alamos is a funny sort of place. It sits at 7,320 feet on a mesa on the edge of an ancient volcano so if things go wrong, they won’t blow up the rest of the state. The homes are mid-century modern built when defense budgets were essentially unlimited. As a prime target in a nuclear war, there are said to be miles of secret underground tunnels hacked out of solid rock.

You need to bring a Geiger counter to garage sales because sometimes interesting items are work castaways. A friend almost bought a cool coffee table which turned out to be part of an old cyclotron. And for a town designing the instruments to bring on the possible end of the world, it seems to have an abnormal number of churches. They’re everywhere.

I have hundreds of stories from the old nuclear days passed down from those who worked for J. Robert Oppenheimer and General Leslie Groves, who ran the Manhattan Project in the early 1940s. They were young mathematicians, physicists, and engineers at the time, in their 20’s and 30’s, who later became my university professors. The A-bomb was the most important event of their lives.

Unfortunately, I couldn’t relay this precious unwritten history to anyone without a security clearance. So, it stayed buried with me for a half century, until now.

Some 1,200 engineers will be hired for the first phase of the new plutonium plant, which I got a chance to see. That will create challenges for a town of 13,000 where existing housing shortages already force interns and graduate students to live in tents. It gets cold at night and dropped to 13 degrees F when I was there.

I was allowed to visit the Trinity site at the White Sands Missile Test Range, the first visitor to do so in many years. This is where the first atomic bomb was exploded on July 16, 1945. The 20-kiloton explosion set off burglar alarms for 200 miles and was double to ten times the expected yield.

Enormous targets hundreds of yards away were thrown about like toys (they are still there). Half the scientists thought the bomb might ignite the atmosphere and destroy the world but they went ahead anyway because so much money had been spent, 3% of US GDP for four years. Of the original 100-foot tower, only a tiny stump of concrete is left (picture below).

With the other visitors, there was a carnival atmosphere as people worked so hard to get there. My Army escort never left me out of their sight. Some 78 years after the explosion, the background radiation was ten times normal, so I couldn’t stay more than an hour.

Needless to say, that makes uranium plays like Cameco (CCJ), NextGen Energy (NXE), Uranium Energy (UEC), and Energy Fuels (UUUU) great long-term plays, as prices will almost certainly rise and all of which look cheap. US government demand for uranium and yellow cake, its commercial byproduct, is going to be huge. Uranium is also being touted as a carbon-free energy source needed to replace oil.

At Ground Zero in 1945

What’s Left of a Trinity Target 200 Yards Out

Playing With My Geiger Counter

Atomic Bomb No.3 Which was Never Used in Tokyo

What’s Left from the Original Test

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/03/ground-zero.png758584april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-09-23 09:02:102024-09-23 10:37:24The Market Outlook for the Week Ahead, or the Dr. Jekyll to a Mr. Hyde

“All over the world, money managers are waiting for the signal that the Fed is going to end tightening. I think everyone is on a hair trigger,” said oracle of Omaha, Warren Buffett.

https://www.madhedgefundtrader.com/wp-content/uploads/2024/09/cowboy.png364476april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-09-23 09:00:312024-09-23 10:37:04September 23, 2024 - Quote of the Day

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.