When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-02-14 13:08:212025-02-14 13:08:21Trade Alert - (NVDA) February 14, 2025 - TAKE PROFITS - SELL

The market has stalled because of continued uncertainty about everything.

Financials are still leading on deregulation party, but M&A has yet to start.

John says all interest rate plays remain dead in the water, including gold, silver, homebuilders, bonds & REITS.

US dollar remains bid on trade war.

Big technology stalling

Energy sells off on trade wars.

John says financials are the only sure thing this year.

Keep your discipline – don’t look for trades that aren’t there.

THE GLOBAL ECONOMY – CONFUSED

Fed leaves interest rates unchanged at 4.25%, and they might remain there for the rest of 2025.

Nonfarm payroll plunges to 145,000 in January.

The headline unemployment rate came in at 4.0%.

US Job Openings hit 14-month low.

Consumer sentiment falls, according to The University of Michigan.

China counters attacks in trade war.

US Factory Orders fall.

Consumer Inflation Expectations come in soft.

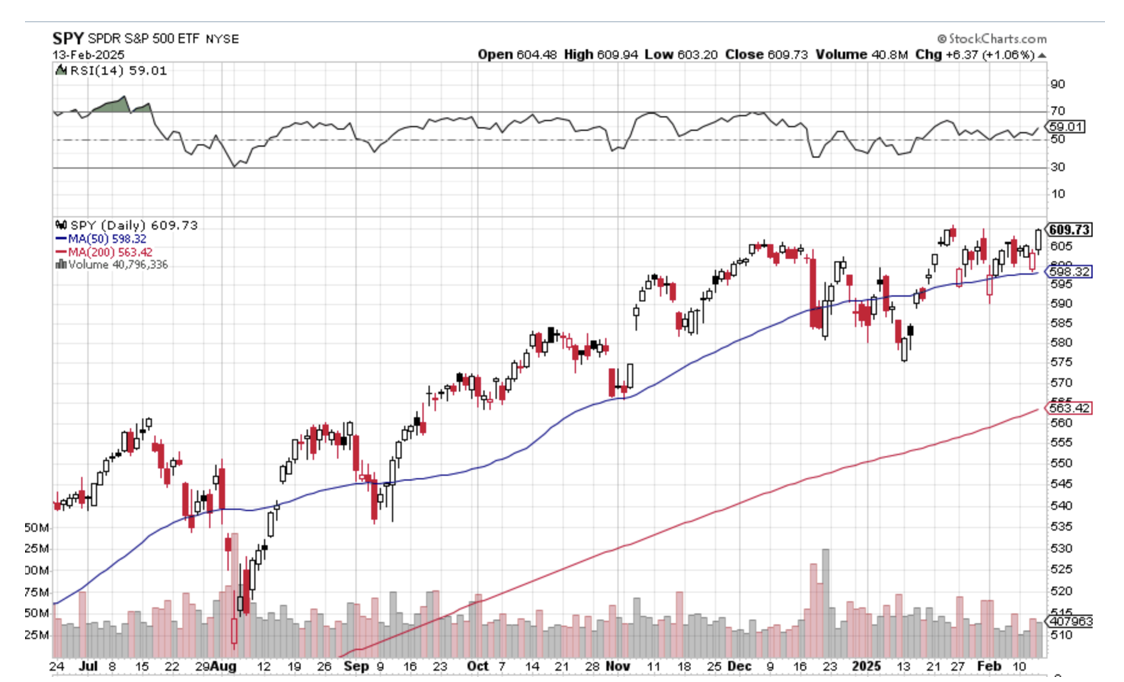

STOCKS – DOWNTREND

Wall Street is souring on Magnificent 7, except for Meta.

Goldman Sachs sees a correction coming in the face of deteriorating global macro conditions, trade wars, and sky-high valuations.

Technology stocks destroyed on news of China’s Deep Seek.

Tariffs to cut US earnings by 5%.

The exemption race is on with many industries pleading for special treatment in the new trade wars.

Palantir soars 25% on the prospect of a surge in government contracts.

Chevron post first loss in four years.

U.S. business activity slowed to a nine-month low.

BONDS – RALLYING

Foreign investors continue to soak up US debt, seeking higher interest.

Americans own 55% of the outstanding $36 trillion in US debt, while foreign investors own 24%, and the federal reserve 13%.

The market is giving up on any interest rate cuts this year, as the prospect of rising inflation from trade wars weighs on the market.

All fixed-income plays have gone dead.

Higher rates for longer don’t fit in here anywhere.

Possible target for (TLT) = $82

FOREIGN CURRENCIES – TRADE WAR BOOST

Trade wars are pushing up the US dollar, making American exports more expensive.

High import duties will shrink US imports dramatically and impoverish our foreign customers, creating dollar strength.

Ten-year US Treasuries have risen from 4.40% to 4.50%.

The mere fact that rates have stalled has allowed currencies to rally.

Higher for longer interest rates mean higher for longer US dollar.

Avoid (FXA), (FXE), (FXB), (FXC), and (FXY).

ENERGY & COMMODITIES

US global economic disruption sink oil prices.

Oil & Gas dealmaking hits $105 billion in 2024.

Government to stop minting new pennies.

Nuclear plays like (VST) and (CCJ) rebound sharply.

The EIA said it expects Brent Crude oil prices to fall 8% to average $74 a barrel in 2025 and then fall further to $66 in 2026.

PRECIOUS METALS – BID AGAIN

Government may revalue gold holdings from the current 1932 price of $42 an ounce to $2936.

It is just a bookkeeping move, but it has put the yellow metal back in the spotlight.

As of January 2025, the United States government owned 133.45 tons of gold worth $39.9 billion at current market prices.This makes the US the country with the largest gold reserves in the world.

Gold has become the only way the average Chinese can save as they can no longer speculate in real estate or copper, and the population doesn’t trust the Chinese Yuan, so there is support lower down.

Central banks in emerging market countries are continuing to buy gold.

REAL ESTATE – STAY AWAY

Homebuyer Mortgage demand is collapsing, with the 30-year fixed at a buzzkill 7.0%.

Demand is 35% lower YOY, with housing demand at a 30-year low.

Homes are sitting on the market much longer.Avoid all real estate plays.

US Home Sales hit a 30-year low in 2024, the second year in a row of weak sales.

High costs related to homeownership sapped sales again.

The average rate for a 30-year fixed mortgage has hovered between 6% and 8% since late 2022.

Avoid real estate plays.

TRADE SHEET

Stocks – buy the next big dip, sell rallies.

Bonds – sell rallies

Commodities – stand aside.

Currencies – stand aside.

Precious metals – buy dips.

Energy – buy nuclear dips.

Volatility – sell over $30.

Real estate – stand aside.

NEXT STRATEGY WEBINAR

12:00 EST Wednesday, February 26, 2025, from Incline Village, NV.

Below, please find subscribers’ Q&A for the February 12 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

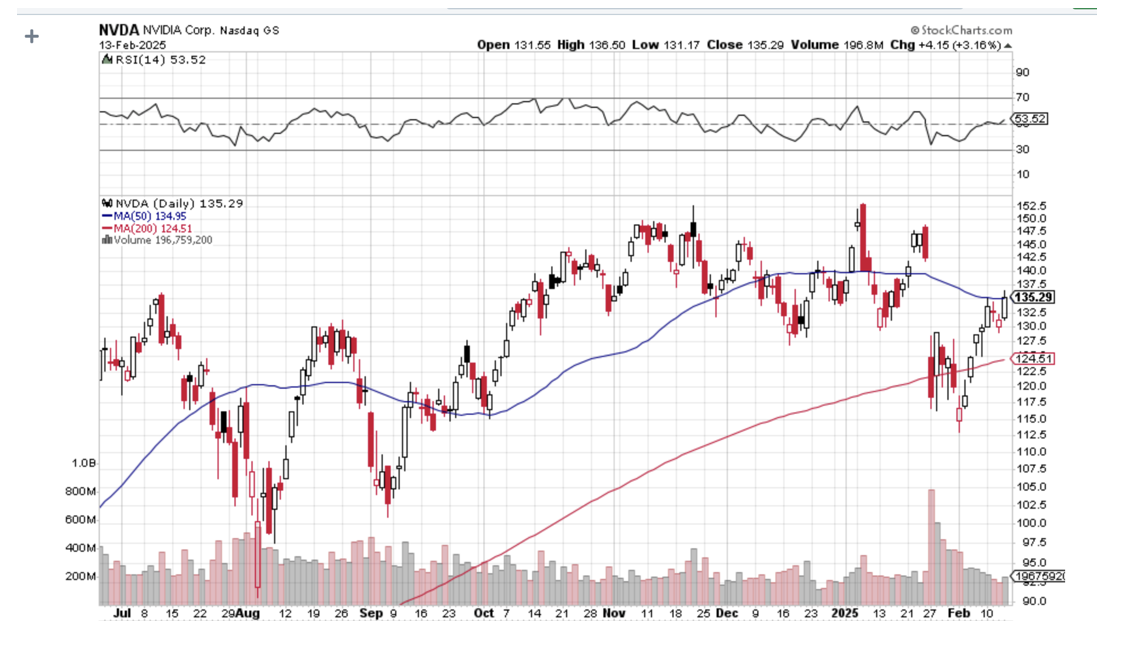

Q: Can Nvidia (NVDA) go to $200 in the next three years?

A: I would imagine probably, yes. They still have a fabulous business—enormous orders and record profits. But it's not going to happen in the next six months. You need to get us out of the current stock market malaise before anything moves dramatically one way or the other, except for META, which is at an all-time high. Their basic business is still great, and the threat posed by DeepSeek is wildly overblown.

Q: Why is McDonald's (MCD) seeing declining sales?

A: Partly, it's because they have been cutting prices. So, of course, that automatically feeds into declining sales. Also, I think the weight loss drugs Mounjaro or Ozempic are having an impact. People just don't go in and eat three Big Macs for lunch anymore. They may not need any Big Macs at all. And forget about the fries and the super-size high fructose corn syrup drink. When these drugs first came out, it was speculated that fast food companies would be the number one victim of these drugs, and that is turning out to be true. Some 15.5 million people in the United States suddenly aren't hungry anymore; they just take one bite of a meal and then push their food around the plate with their fork. That’s better than taking amphetamines, which people like Judy Garland used to take to lose weight. I think that will affect not only McDonald's, but all fast-food companies which I avoid like the plague anyway because my doctor says I shouldn't eat that food.

Q: Should I buy First Solar (FSLR) based on the revised higher sales outlook?

A: I don't want to touch alternative energy anything right now. I think the government will eliminate all subsidies for all alternative energy—be it solar, windmills, hydrogen, nuclear, whatever—and turn us back into an all-oil and coal economy. That is the announced goal of the new administration. So that eliminates the subsidies for sure. It certainly will be a blow to the earnings of all solar-type companies. If you are going to do an energy form, I would do nuclear, which benefits from deregulation, if that ever happens.

Q: Do price caps fix supply problems? Because Europe is thinking about capping energy prices in the short term.

A: Price caps never work, nor does any other attempt to artificially control prices, because all it does is dry up supply. If you cap the prices, and therefore the profits that energy companies can make, they'll quit. They'll abandon the energy business, or they'll pare it down, or they won't expand. One way or the other, you reduce the return on capital. Capital is like water; it will go where it gets the highest return, and price caps certainly are not part of that formula. But what do I know? I only drilled for natural gas for six years.

Q: What's your top AI choice?

A: Well, I would say it's Nvidia (NVDA) still, and the big AI users which include Meta (META), Google (GOOG), and Amazon (AMZN). Nothing has changed here.

Q: Is there any chance that Ford Motors (F) will be bought out anytime soon or never?

A: My view of all of the legacy car companies, including Stellantis, which is the old Chrysler, Ford (F), and General Motors (GM), is that they are basically giant mountains of scrap metal and only have a scrap metal value, which is about 5 cents on the dollar. That's what they fell to in the 2008 financial crisis, and all of them except for Ford went bankrupt. So I am not a big fan of the legacy auto industry now. And now, they have a trade war. They happen to be one of the biggest victims of trade wars because to stay competitive with Tesla, they moved a lot of their production to Canada and Mexico, and now those plans are going up in flames. So it seems like they're damned if they do and they're damned if they don't. I'm happy driving my Tesla, but I'm wondering if my next car is a BYD. Prices are so low, it might even be worth paying 100% duty just to get a cheaper car that has better self-driving capability. But the future is unknown, to say the least.

Q: Is the next big rotation out of Silicon Valley and into Chinese tech stocks?

A: Over the long term, that may happen, but with the current administration and China (the number one target in restraint of trade and trade wars), I don't want to touch anything Chinese. There are too many better things to do in the U.S. Imagine you buy a Chinese stock, and then the administration announces a total cutoff of trade with China the next day. Not good. Chinese stocks are incredibly cheap. Most of the big ones are now single-digit multiples compared to multiples in the 20s, 30s, and 40s for our stocks. But they come with a very high political risk, and that has been true for several years now. There are better fish to fry than in China. I'd rather buy Europe than China right now if you really do want to go international. But I have no idea why they're going up unless they're discounting an end to the Ukraine War.

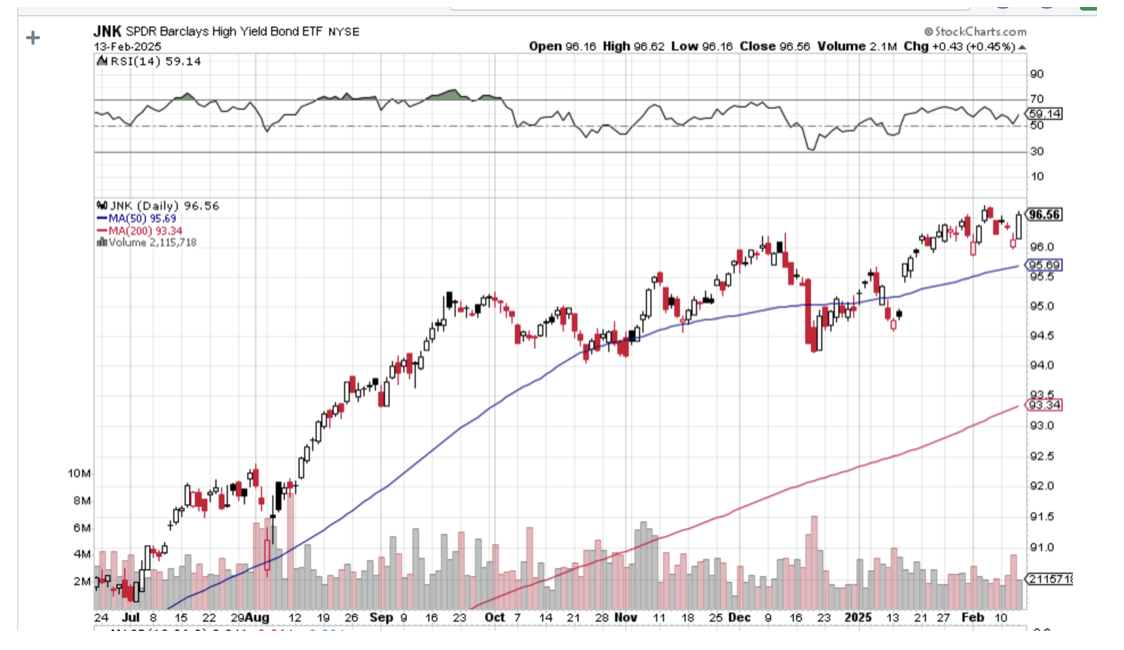

Q: Are junk bonds (JNK) and (HYG) a good play?

A: I would say yes. Their default risk has always been over-exaggerated thanks to their unfortunate name. They're yielding 6.54% and change, but it's a very slow mover. If we do get any improvement, any economy without inflation junk will go to $100. It's currently around $96. And you know, yield is a nice thing to have these days since the capital gain side seems to have dried up and turned into dust on almost any asset class.

Q: How can I decide when to sell the stocks that we bought on your recommendations?

A: Well, our trade alerts always have a buy recommendation and a sell recommendation or an expiration date. If you bought the stocks and kept it,just read Global Trading Dispatch for an updated market view. Watch our Mad Hedge Market Timing Index. When we get up into the 70s and 80s, that is definitely sell territory. It's hard for individuals to have an economic view going out to the rest of the year, but even the people who are economists have no idea what's going to happen right now. As I said, uncertainty is at an 8-year high, and that is being reflected in the market. So nothing beats cash, especially when you can earn 4.2% on 90-day US treasury bills. No one ever got fired for taking a profit.

Q: Can Intel (INTC) make a comeback this year?

A: No. I'm sorry, but they won’t. They had a horrible manager. They dumped him after a couple of disastrous years. I knew he was a horrible manager. I fought off all the pressure to buy Intel. So far, that's working. I mean, the stock has been terrible, so it is very cheap, but there is no guarantee that they will ever recover and, in fact, may get taken over by somebody else. So—too many better things to do. I'd rather be buying more Nvidia right now at these prices than sticking my neck out and praying for a miracle at Intel.

Q: A couple of years ago, I bought a bunch of Palantir (PLTR) on your recommendation for the next 10 bagger. I now have a 10 bagger. What should I do?

A: You know, we did recommend Palantir about 10 years ago, and it did nothing for the longest time. And then last year, it just took off like a rocket—I think it's up 400% last year. Price-earnings multiples are insanely high now. So what I would do is sell half your position. That way, the remaining half is all profit. You're playing with the house's money, and you're reducing your risk in a high-risk environment. Sell half, keep the other half. If it looks like it's starting to roll over and die, then you sell your remaining half.

Q: What's your favorite currency this year, and what should we do about it?

A: My favorite currency is the US dollar. If we're not going to get any interest rate cuts this year, the dollar will remain the highest-yielding currency in the world, and then everybody wants to buy it. It's really that simple. It’s all about interest rate differentials. Everybody else in the world has low interest rates, so stick with the dollar and don't touch the foreign currencies yet.

Q: Inflation expectations have exploded higher in view of today's number. Do you expect it to get worse?

A: If the trade war continues, it will absolutely get worse. 25% price increases are inflationary—period. End of story. A price increase is the definition of inflation, and right now, we are increasing the number of countries subject to high punitive tariffs, not decreasing them. You can expect markets to worry about that. And even if they put a temporary hold on these, people are raising prices now. They are not waiting for the actual tariff to hit; they are front-running that right now. So if you don't believe me, go to the grocery store where prices are through the roof. I actually went to a grocery store the other day, and I couldn't believe what things cost.

Q: I'd like to hedge my Nvidia (NVDA) position with a covered call. Which one should I do?

A: Well, it's not actually a hedge. What a covered call does is reduce your cost price and increase income. Right now, we have NVDA at $135. If you shorted something like the February $145 calls, you might get a dollar for that. That reduces your average price by a dollar. If you shorted the March $145 calls, that'll bring in probably $5, reduce your costs by $5, or bring in an extra $5 in income. And if you keep doing this every month and Nvidia stays stuck in a range, you can end up taking $10, $20, or even $30 in premium income over the next six months. And I have a feeling that will be the winning strategy for the first half of this year, using rallies to sell covered calls. You really could get your average cost down quite a lot; that way, if we have a massive sell-off, a lot of that loss will already be covered. If we get a massive rally, your stock just gets called away, and you buy it back on the next dip. The only negative here is the tax consequences of taking capital gains on the call-aways.

Q: You mentioned that the US has a demographic problem coming up; how will that affect the market in the short term?

A: It doesn't affect the market in the short term. Demographics are a long-term game. You have to think in terms of a generation being the round lot, which is about 20 years. Suffice it to say, when demographics go against you, like they did in Japan for 30 years, markets are horrible. Demographics are going against China now, and you're getting horrible markets. Demographics are good now in the US because we have millennials just entering their peak spending years, and that's when economies boom, and that should continue up to 2030. That is how to play demographics, and we keep updated here, although the government has suddenly ceased making available all demographic data to the public—I don't know why, but it's going to make the science of demographics much more difficult to follow without the government data. I don't know why they did that. I don't know what they hope to gain by clouding the demographic picture. Maybe it has to do with the allocation of congressional seats to the states or something like that.

Q: Do you have information on how to place a LEAPS order?

A: Just go to www.madhedgefundtrader.com, go to the search box, put in LEAPS in all caps, and you will find an encyclopedia of information on how to do LEAPS or Long Term Equity Anticipation Securities.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Back in 1989, when I was setting up one of the first international hedge funds, I learned a timeless lesson about pharmaceutical stocks: the market doesn't care what you think it should care about—it cares about whatever it wants to care about.

That was on full display last week, as I watched Amgen (AMGN) dance its post-earnings tango and rally despite the FDA putting a mysterious hold on its obesity drug trials.

The stock’s move was exactly what its technical patterns suggested.

After managing hedge fund money for decades, I’ve seen literally millions of chart setups, and AMGN’s current formation is one of those rare “textbook” moments that make veteran traders sit up a little straighter in their ergonomic chairs.

The numbers paint a fascinating picture. Amgen isn’t just any biotech; it’s one of the dwindling few in the Dow 30 that still yield north of 3%. In this market, that’s about as rare as finding a bargain at Sotheby’s.

Better yet, it carries a dividend safety rating of A—something I’ve come to value above all else after living through multiple market crashes.

In my experience, dividend safety is the bedrock on which everything else is built, so seeing that in a company is like stumbling upon a bomb shelter with a view.

Digging deeper, the company just delivered a revenue beat that would make any analyst grin, but the real hook for me is the pattern of earnings revisions.

They’re trending up more than down, fueling a kind of momentum that reminds me of the early days of Genentech’s meteoric rise back in the 1980s.

Of course, there’s an elephant in the room: valuation.

With a D- grade in that department, Amgen’s price tag is about as stretched as my old climbing rope from Mount Everest. But modern markets aren’t your grandfather’s markets anymore.

The days of pure buy-and-hold being a guaranteed winning strategy have gone the way of paper trading tickets, replaced by algorithms and new trading paradigms.

This is why I like to employ what I call the "Triple-Lock Position" strategy.

Essentially, you buy the stock, buy a put for protection, and sell a call to offset that cost - three distinct moves that work together to lock in your risk parameters.

With Amgen hovering around $300, one round lot sets you back roughly $30,000. That price tag is a good reminder that position sizing matters more than ever.

From my hedge fund experience, steady cash flow and consistent profits often trump the promise of explosive growth, especially when storm clouds gather.

In volatile markets, companies that can reliably generate cash tend to outlast the flashier high-flyers.

Then there’s the technical angle. After analyzing enough charts to wallpaper the old Swiss Bank Corp building, I can say these trend lines have been as reliable as a Swiss watch.

Yes, we see the occasional short-term break, but it’s akin to a compass briefly pointing south before swinging back to true north.

For those who track this stuff closely, AMGN appears to be offering one of those rare situations where technical strength aligns with fundamental quality.

So what’s the play? I see Amgen as a “buy the dip” opportunity, but I suggest doing it with a twist. Instead of simply loading up on shares the old-fashioned way, consider collaring your position or using call options to define your risk.

Markets these days reward flexibility, and adapting your strategy to the current environment is crucial—something I learned during the Asian financial crisis, when clinging to outdated rules was a surefire path to disappointment.

All of this brings us back to that FDA hold on AMG 513. The market’s collective shrug reminds me of an old trading floor saying: “The market will decide what to worry about, not us.”

In biotech, as in most sectors, the reaction to news often reveals more than the news itself. Watching how investors brush off certain announcements can be more informative than pouring over the finer details.

Keep a close eye on those trend lines, because they’ve served as a pretty good compass so far. AMGN is showing the kind of setup where technical signals and strong fundamentals converge, and that rarely goes unnoticed for long.

Just remember, in the modern market, it’s not only about what you buy; it’s about how you buy it. The once-reliable buy-and-hold mindset is no more current than my old Financial Times columns from the 1970s.

Now, if you’ll excuse me, I need to check on my option positions. The market waits for no one—not even old hedge fund traders with stories to tell.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-02-13 12:00:292025-02-13 11:54:40Triple - Locked And Loaded

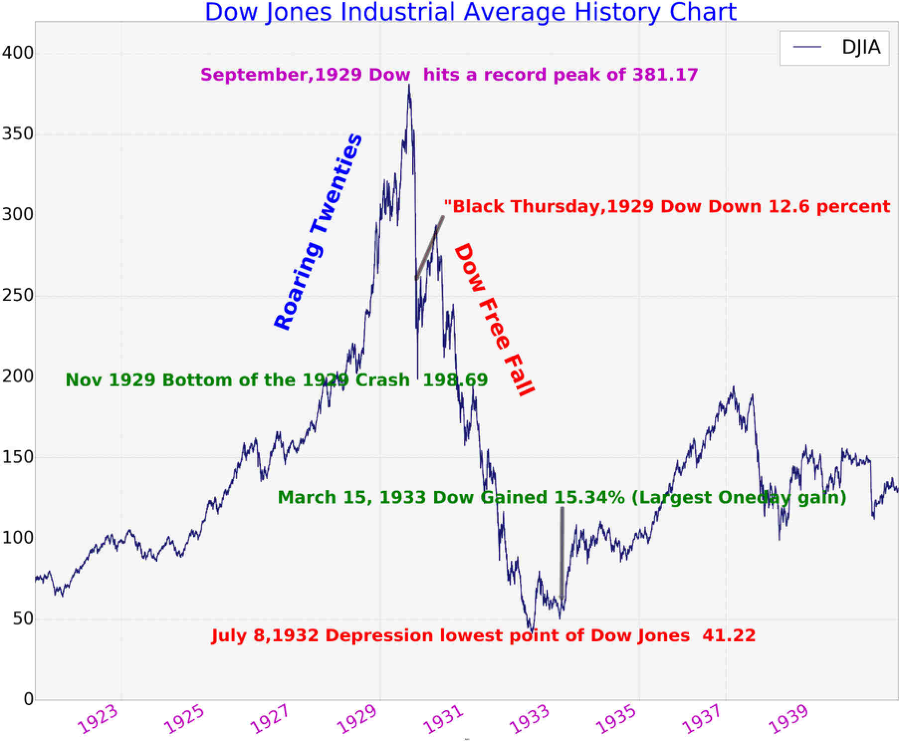

When I first arrived on Wall Street during the early 1980s, some of the old veterans who worked through the 1929 stock market crash were just retiring and passed their stories on to me before they left.

One was my old friend, Sir John Templeton, founder of the Templeton funds, who often hosted me for dinner at his antebellum-style mansion at Lyford Cay in the Bahamas. John told me he was really excited when hired in ‘29 to handle the surge of brokerage business. After that, things got really boring for a decade.

The volatility we are experiencing now has many similarities to that epic event. In some ways, it's far worse. The 1929 downturn was spread over 34 months.

We all know about the Roaring Twenties, with flappers, bathtub gin, and a soaring stock market. Then, individuals could buy on ten to one margin. The high-flying tech stocks of the day, like RCA Radio, General Motors (GM), and Ford (F), soared. From 1921 to 1929, the Dow Average rocketed six-fold. The working class was sucked in.

Industry followed suit, taking the sign of rising stocks as proof of an economic boom. They massively boosted production in all sectors. That meant they went into the Great Depression loaded to the gills with inventory.

The Dow Average peaked on September 3, 1929, at 381. A slow burn of profit-taking ensued. Suddenly, a cascading waterfall of SELL orders hugely accelerated on “Black Monday” when the Dow plunged by 13%. It was followed by “Black Tuesday” when stocks lost another 13%.

Margin calls triggered a run on the banks as investors tried to withdraw cash to cover rampant cash calls. This spawned a financial crisis where eventually 4,000 banks went under.

By November, the Dow had fallen by 48% to 198. JP Morgan stepped in to stabilize the market, prompting a short-term rally. It was to no avail, with many retail investors seeing this as their last chance to sell. The market continued its slide, eventually hitting bottom at 41, or down an astonishing 89% from the top by July 8, 1932. The market then moved sideways in a wide 150-point range until the outbreak of WWII. It didn’t recover its 1929 peak until 1959.

A few years ago, I had lunch with the former governor of the Federal Reserve (click here), who did his PhD dissertation on the causes of the Great Depression. The big mistake the Fed made then was to raise interest rates to damp down stock speculation. They ended up destroying the economy, inadvertently making the depression far deeper and longer.

The world has learned a lot about central banking since those dark days. For a start, the theory of Keynesianism has been adopted whereby governments borrow and spend during economic downturns and run balanced budgets or surpluses during good times.

The modern Fed won’t be making the same mistake twice. During the last bear market, the Fed almost immediately took interest rates down to zero. Our central bank has also responded with monetary stimulus that is a large multiple of what we saw in 2008-09, essentially buying everything that was out there in fixed-income land.

My grandfather never participated in the stock boom of the 1920’s. He never found a broker he could trust. When the market crashed, he had to finish his basement in Brooklyn, New York, so that several relatives who had lost their homes could move in. We lost many equity investors for good in the 2008-09 crash. No doubt we will lose many more in this cycle.

What did Grandpa do with his money? He poured it all into real estate, including the land on which the Bellagio Hotel was eventually built, which he picked up for $500 an acre. His estate sold it in the 1970’s for $10 million.

Grandpa never bought a stock during his entire life.

Grandpa on Right

https://www.madhedgefundtrader.com/wp-content/uploads/2020/03/dow-jones-1929.png741899Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2025-02-13 09:04:132025-02-20 12:38:44Revisiting the Great Depression

While in New York waiting to board Cunard’s Queen Mary 2 to sail for Southampton, England, a few years ago, I decided to check out the Bay Ridge address near the Verrazano Bridge where my father grew up. I took a limo over to Brooklyn and knocked on the front door.

I told the owner about my family history with the property, but I could see from the expression on his face that he didn’t believe a single word. Then I told him about the relatives moving into the basement during the Great Depression.

He immediately let me in and gave me a tour of the house. He told me that he had just purchased the home and had extensively refurbished it. When they tore out the walls in the basement, he discovered that the insulation was composed of crumpled-up newspapers from the 1930s, so he knew I was telling the truth.

I told him that grandpa would be glad that the house was still in Italian hands. Could I enquire what he had paid for the house that sold in 1923 for $3,000? He said he bought it as a broken-down fixer upper for a mere $775,000. After he put $500,000 into the property, it is now worth $2 million.

I’ll recite one story that took place at this address which has been passed down through the generations. By the end of 1945, the family had not seen my father for nearly four years, who was off fighting in the Pacific with the Marine Corps.

Then a telegram arrived informing the family of the date of my father’s return after a five-day train ride from Los Angeles. As only two daughters remained at home, he warned everyone not to cry.

Then the doorbell rang and there was Dad, 40 pounds lighter with a yellowish tinge to his skin from malaria but smiling. My grandfather burst into tears and wouldn’t stop bawling for an hour.

As I passed under the Verrazano Bridge on the Queen Mary II later that day, I contemplated how much smarter grandpa became the older I got.

I hope the same is true with my kids.

Queen Mary II Passing Under the Verrazano Bridge

https://www.madhedgefundtrader.com/wp-content/uploads/2012/08/queenmary.jpg300400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2025-02-13 09:02:502025-02-20 12:38:45Exploring my New York Roots

“Lower yields, for longer, and lingering. I don’t think we’re going to get to an end for some period of time. The money that has been pumped into the system is going to keep equities high,” said Mark Grant, managing director of Hilltop Securities.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/08/Wall-street-quote-of-the-day-e1535492480774.jpg197350MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2025-02-13 09:00:372025-02-13 09:48:01February 13, 2025 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.