Meta (META) cutting staff in its virtual reality and augmented reality divisions means uncertainty about future products originating from these places.

The juice has not been worth the squeeze.

I think everyone remembers when Founder Mark Zuckerberg had those goofy metaverse commercials depicting him as an avatar when he debuted the company name change from Facebook to Meta.

Well, the metaverse project isn’t working, which is why he’s firing staff from those projects.

The metaverse division has underdelivered and overpromised.

This lethal cocktail of failure is finally forcing management to cut off the fat from its body.

VR and AR are now losing billions of dollars per year, and as the business environment turns more pragmatic, these experimental projects are thrown out for good.

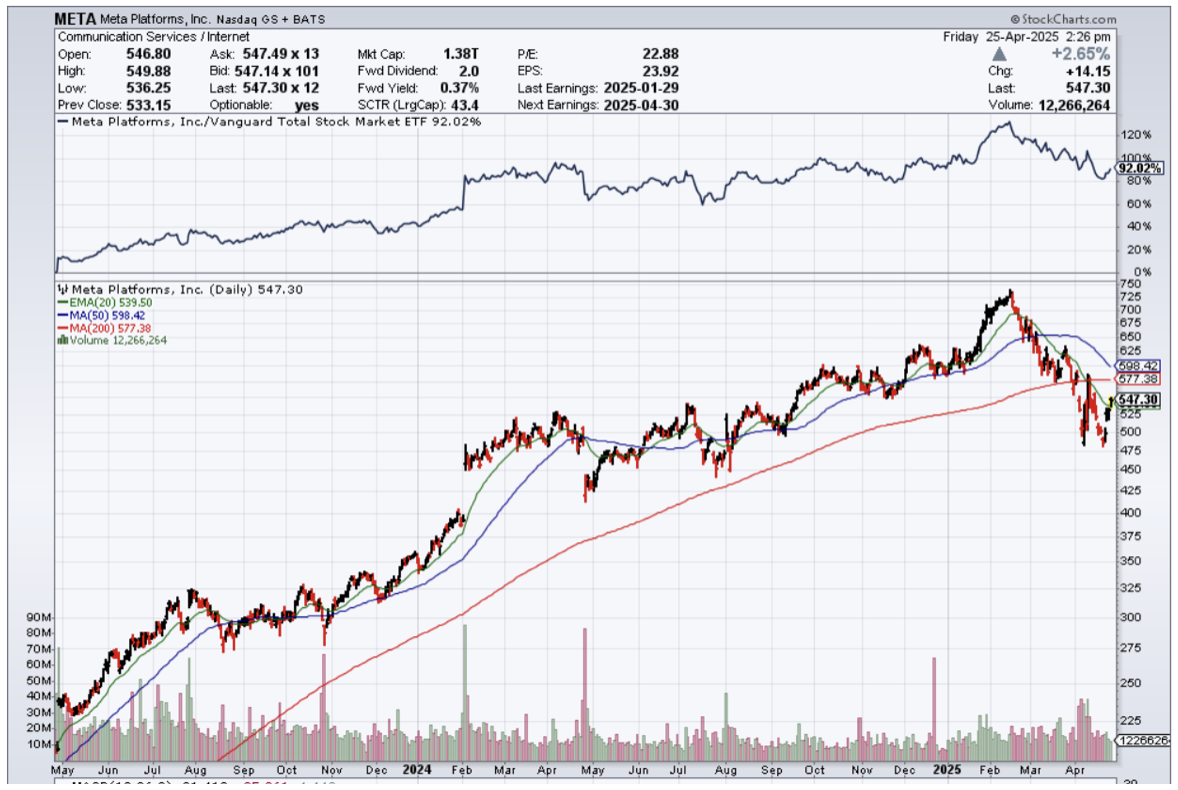

META said its Reality Labs unit recorded an operating loss of $4.97 billion while generating $1.1 billion in sales.

A nice quarterly performance of minus 3 billion dollars has forced management to make some tough decisions.

Now, the AR and VR divisions will be gutted.

Reality Labs is Meta’s unit that makes the Quest family of virtual-reality headsets and Ray-Ban Meta Smart Glasses.

Meta CEO Mark Zuckerberg kick-started his company’s VR endeavors in 2014 when it acquired the startup Oculus for $2 billion. Since then, Zuckerberg has characterized VR and AR as central to his plans to develop the futuristic digital world known as the metaverse, which he has said represents the next major computing platform.

Reality Labs has piled up an operating loss of more than $60 billion since 2020.

The losses cannot just be swept under the carpet.

Meta last week said it would invest between $60 billion and $65 billion in 2025 capital expenditures to expand its computing infrastructure related to artificial intelligence.

Even this AI infrastructure build-out is questionable at this point, as other big tech firms pull back from this type of investment.

Meta released its latest VR headset, the $299 Quest 3S, during its September Connect event and pitched the device as a way for people to watch movies, play games, and work out in VR.

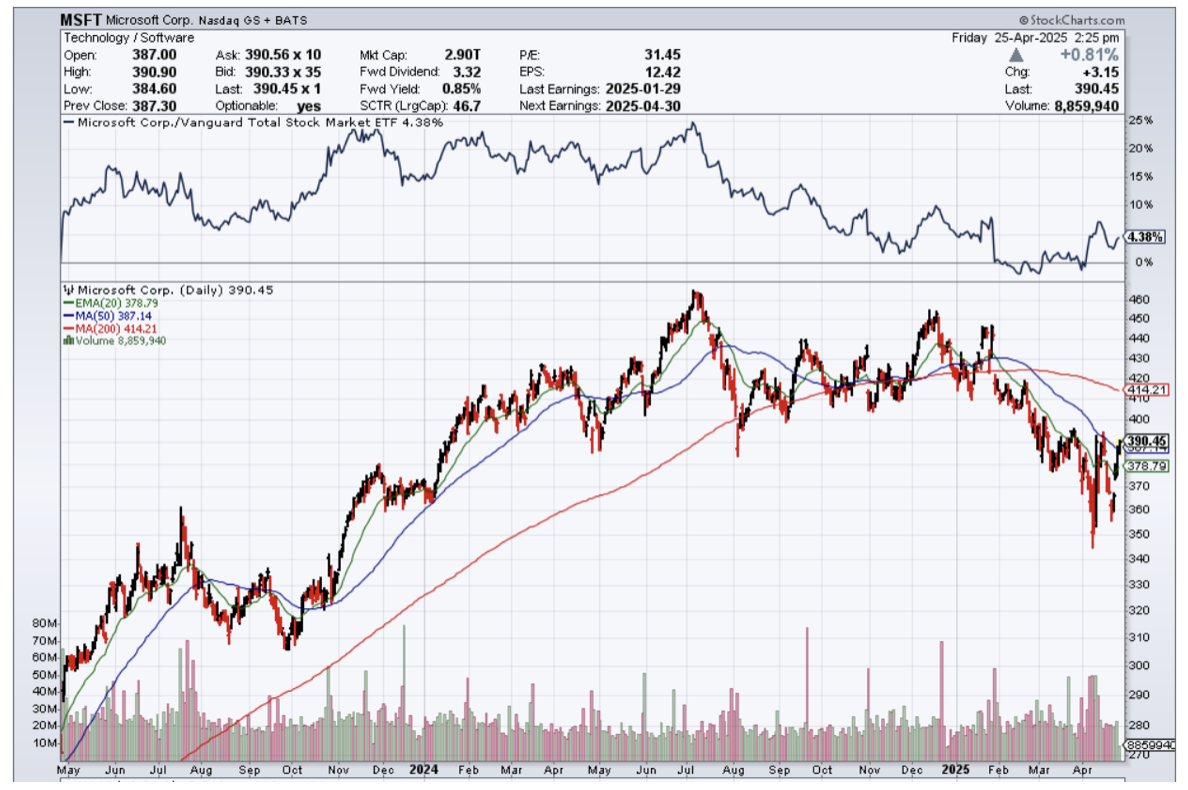

Microsoft (MSFT) has lost at least $5 billion on HoloLens since the launch of the first model in 2016.

The Microsoft HoloLens is a mixed reality headset that allows users to overlay digital information onto the real world, creating a blended experience of physical and digital environments.

Microsoft’s withdrawal from the market for augmented and virtual reality hardware leaves competitors such as Apple and Meta with a less crowded field on which to compete.

Apple (AAPL) is another company that has bet on AR and VR.

In short, VR and AR have been money pits that suck up investment dollars, but deliver nothing in terms of profit.

Whether it is Meta, Apple, or Microsoft, they have all struck out at this technology and will need to embrace the reality that consumers don’t want Google-type technology on their face to interact with a screen.

AR and VR divisions should be buried in the graveyard of attempted technology that people aren’t interested in.

Back to the drawing board…