When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

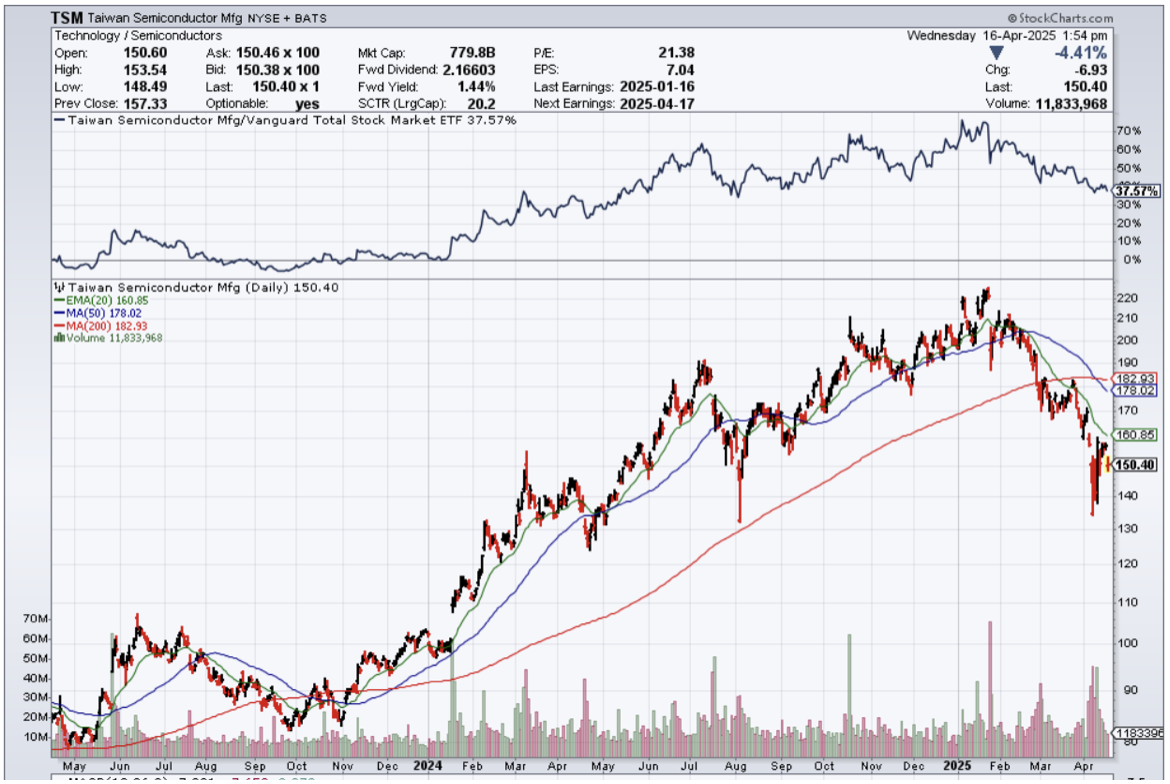

I understand that the U.S. administration wants to bring back American manufacturing, but that will not include Silicon Valley manufacturing.

There is a higher likelihood that if China is a no-go zone, American tech companies will venture out to a low-tariff, cheap labor country to continue their path to profits.

If you look through the numbers, it doesn’t make sense for American tech companies to manufacture goods in America.

The costs are too prohibitive.

Silicon Valley tech firms that are public on the New York markets have a fiduciary responsibility to shareholders to sustain short-term profits.

There is no mandate stating that these American tech companies must be manufactured in any specific sovereign country.

Silicon Valley companies are global, and American jobs lose out because of that.

This is a tough nut to crack because wages in rich Western countries dwarf the nominal amount in more affordable places.

U.S. Commerce Secretary Howard Lutnick said during an interview that the (China tariff) move was temporary.

Instead, he explained, tech products will be tariffed as part of the administration's planned duties on semiconductors, which could be announced later this week.

It's not just about timing. Companies would also need the workers to build devices.

While there's a degree of automation possible and while many of the components needed are made in the US, there's still a need for tens of thousands of trained electronics assemblers willing to work long, arduous hours in highly repetitive tasks.

Companies including Nvidia (NVDA), TSMC (TSM), Apple (AAPL), and others have announced increased investments in the US to win over Trump and avoid tariffs.

Nvidia said it will produce $500 billion in AI infrastructure in the US over the next four years through partners including Foxconn (601138.SS), TSMC, and Wistron (3231.TW).

And while that doesn't take away from the fact that the companies are pouring money into the US, it doesn't exactly support the idea that they're moving vast amounts of their manufacturing capabilities to America.

Even if companies brought their manufacturing bases to the US, they'd still have to deal with importing certain parts from abroad.

It's not just Apple that's contending with manufacturing headwinds; everything from laptop makers to display producers would face the same problems if they were to move to the US.

According to some estimates, prices on devices could double, resulting in demand destruction as consumers seek out less expensive options or hold onto their existing smartphones and computers for longer periods.

While it's unlikely manufacturing is coming back to the US, there's still plenty of uncertainty about how tech companies and consumers navigate the next four years of tariff shocks.

The biggest winners appear to be Vietnam or India, and much of the American tech manufacturing has their sights set on these places to reduce costs.

In short, this won’t destroy American tech and their shares will outperform in the long run, but in the short-term, it hurts, because it puts doubt into where they will produce their gizmos and gadgets.

At the very least, this gets American tech out of China, and I believe the federal government would be happy if businesses migrated to a more neutral country, even if they don’t come back home.

Either way, after this all blows over, there will be a great buying opportunity in American tech companies, which will all be trading at a discount.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-04-16 14:02:252025-04-16 15:02:37American Tech Able To Outflank

The global economic landscape is being reshaped as we speak.There are now heightened concerns about economic growth, currency stability, and financial retaliation.We need to consider China’s potential response via US Treasury yields and other retaliatory measures.

On April 2, 2025, President Trump signed Executive Order 14257, imposing a 34% tariff on Chinese imports, pushing total levies above 70% for some goods.China retaliation on April 4 with a matching 34% tariff on US imports, plus rare earth export curbs.This is reminiscent of the 2018 trade war.

The US aims to boost manufacturing and cut reliance on China, whose share of US imports fell from 21% in 2018 to 14% in 2023.Yet, higher tariffs will likely raise consumer prices for electronics and machinery.The US-China Business Council estimates that revoking China’s trade status could cost 744,000 jobs. With a $36.2 trillion national debt, the US faces refinancing challenges in 2025 as Treasury yields rise, a vulnerability China could exploit.

The US faces a delicate moment in its fiscal policy.With national debt exceeding $36.2 trillion, the Treasury is set to refinance substantial portions in 2025 amid rising yields.The 10-year Treasury yield has surged recently, reflecting market unease over tariffs and inflation expectations.If China leverages its $1.11 trillion in US Treasury holdings, it could exacerbate this pressure.

China’s economy, slowed by post-COVID recovery and property debt, faces a tariff hit.The Economist Intelligence Unit predicts as 20% US tariff increase could cut GDP growth by 0.6 points through 2027, with a 60% tariff costing 2.5 points.Exports to the US (2.9% of GDP in 2023) remain key.China plans a 6.9 trillion-yuan stimulus and rate cuts to hit a 5% growth target, but success is uncertain amid trade disruptions.

The yuan has weakened to its lowest since September 2023, with the People’s Bank of China (PBOC) seemingly willing to let it go lower.A weaker yuan could offset tariffs by cheapening exports, potentially sliding to 7.7 to 7.8 if tensions rise.However, this risks capital outflows and higher import costs, as well as global ripple effects from a broader monetary breakdown.

Alongside the changed economic environments, China holds several strategic tools for retaliation against the US.

China holds $1.11 trillion in US Treasuries and could sell or halt purchases to spike yields, raising US borrowing costs as $6 trillion in debt matures in 2025-2026.This is China’s primary trade war weapon.

It dominates the global rare earth supply chain – critical to military and high-tech industries – supplying roughly 72 per cent of US rare earth imports, by some estimates.

On March 4, China placed 15 American entities on its export control list, followed by another 12 on April 9.Many were US defence contractors or high-tech firms reliant on rare earth elements for their products.

Export restrictions on rare earths could further pressure US tech and defence sectors, though escalation risks backlash.

China also retains the ability to target key US agricultural export sectors such as poultry and soybeans – industries heavily dependent on Chinese demand and concentrated in Republican-leaning states.China accounts for about half of US soybean exports and nearly 10 per cent of American poultry exports.On March 4, Beijing revoked import approvals for three major US soybean exporters.

And on the tech side, many US companies – such as Apple and Tesla – remain deeply tied to Chinese manufacturing.Tariffs threaten to shrink their profit margins significantly, something Beijing believes can be used as a source of leverage against the Trump administration.Already, Beijing is reportedly planning to strike back through regulatory pressure on US companies operating in China.

Let’s not forget the position that Elon Musk holds.As we understand it, he is a senior Trump insider who has clashed with US trade adviser Peter Navarro against tariffs.Furthermore, we know he has major business interests in China.These facts could be a strong wedge that Beijing could exploit to divide the Trump administration.

As I pointed out last week in my Post on Friday (WHO’S IN CONTROL – TRUMP OR XI?) the changing dynamics could significantly reshape the geopolitical landscape of East Asia, bringing together countries to take advantage of a strategic opportunity to displace American hegemony.

Southeast Asian countries could see a strengthened alliance and an “all-round cooperation”, which offers an opportunity to directly erode US sway in the Indo-Pacific.

A promising strategic opportunity is building in Europe too, with the European Union contemplating strengthening its own previously strained trade ties with China.Both sides have jointly condemned US trade protectionism and advocated for free and open trade. EU and Chinese officials are holding talks over existing trade barriers and considering a full-fledged summit in China in July.

China is watching the US dollar.It sees in Trump’s tariff policy a potential weakening of the international standing of the US dollar.Widespread tariffs imposed on multiple countries have shaken investor confidence in the US economy, contributing to a decline in the dollar’s value.

Traditionally, the dollar and US Treasury bonds have been viewed as haven assets, but recent market turmoil has cast doubt on that status.At the same time, steep tariffs have raised concerns about the health of the US economy and the sustainability of its debt, undermining trust in both the dollar and US Treasurys.

The tariff standoff between the US and China is more than a trade dispute, it may well reveal a world at a historic inflection point, where economic strategies and asset choices will define the next decade.For the US, higher costs and refinancing woes loom; for China, growth hangs in the balance, with yuan depreciation a risky but viable counter.

China’s potential to sway US Treasury yields adds a financial warfare dimension – a weapon that should not be taken lightly.It has the tools to inflict meaningful damage on US interests.Perhaps, more significantly, we need to understand that Trump’s all-out trade war is providing China with a rare and unprecedented strategic opportunity that could forever change the economic landscape.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2025/04/China-retaliates.png9241118april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-04-16 09:00:482025-04-16 13:42:11April 16, 2025 - Quote of the Day

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-04-15 13:12:572025-04-15 13:12:57Trade Alert - (NFLX) April 17, 2025 - EXPIRATION AT MAX PROFIT

You know that feeling when you've found the perfect restaurant? The food is exquisite, the atmosphere divine, and then you get the bill—and suddenly you're calculating if selling a kidney is a viable financial strategy.

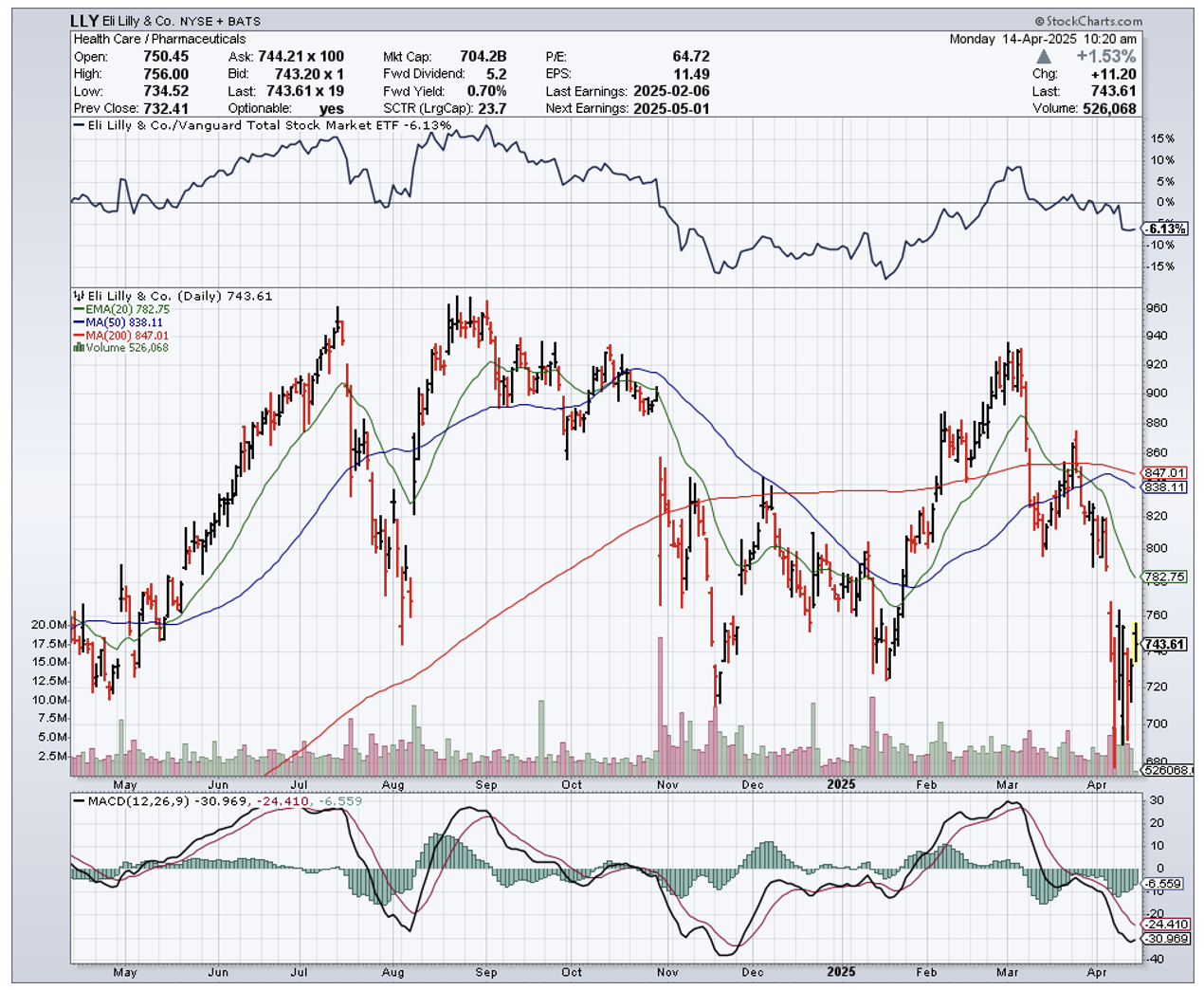

That's essentially my relationship with Eli Lilly (LLY) right now. Phenomenal company, stellar performance, price tag that makes my wallet weep.

I've had a complicated romance with this pharmaceutical juggernaut. Back in my hedge fund days, I learned that timing is everything with pharma stocks. It's like catching the perfect wave off Malibu – ride it too early, you're just splashing in the shallows; too late, and you're eating sand.

When I first spotted Lilly in June 2023, it was set up beautifully. Shares rocketed 56.2% before I downgraded to a 'hold' last February, while the broader market trudged along with a mere 12.3% gain.

Since then, the stock has performed almost exactly as predicted—just a 0.2% gain compared to the S&P 500's 1.33%. More recently, it's dropped 6.9% since January, looking positively rosy next to the broader market's 12.2% decline.

The company's fourth-quarter results read like a biotech investor's fantasy novel. Revenue soared 44.7% year-over-year to $13.53 billion, driven by its dynamic weight-loss duo.

Mounjaro's sales jumped 60.1% to $3.53 billion, while Zepbound exploded from $175.8 million to a jaw-dropping $1.91 billion.

I've watched patients in clinical trials shed substantial weight on these medications—one of my research contacts dropped 43.4 pounds since starting treatment—and I can tell you these drugs are creating waves not just in waistlines but across the entire healthcare sector.

Other stars in Lilly's portfolio include Verzenio for breast cancer (up to $1.56 billion from $1.15 billion), Jardiance for diabetes (climbing to $1.20 billion), and solid gains from Taltz and Humalog.

Only Trulicity disappointed, watching its revenue tumble from $1.67 billion to $1.25 billion—predictably cannibalized by Lilly's newer weight-loss offerings. It's like watching your reliable sedan gathering dust after buying a Tesla.

With this revenue bonanza, profits naturally skyrocketed. Net income more than doubled to $4.41 billion, adjusted profits surged to $4.81 billion, and operating cash flow swung from negative $311.9 million to positive $2.47 billion.

In my decades of following pharmaceutical stocks from Tokyo to Wall Street, I've rarely seen a quarterly performance this impressive. If Lilly were a student, it would be the annoying one breaking the curve for everyone else.

Looking ahead, management projects 2025 revenue between $58-61 billion (a 32.1% increase at midpoint) and adjusted EPS between $22.50-24.

For the upcoming Q1 report on May 1st, analysts anticipate revenue of $12.77 billion (45.6% higher year-over-year) and EPS of $4.70 (nearly double last year's $2.48).

So with all this financial wizardry, why maintain a 'hold'? One word: valuation.

Even using 2025's projected figures, Lilly trades at eye-watering multiples: forward P/E of 33.3, price-to-cash-flow of 27.6, and EV/EBITDA of 21.2.

For context, pharmaceutical peers trade significantly lower. Novo Nordisk (NVO), perhaps the most comparable given its similar weight-loss market success, trades at a P/E of 19.0, price-to-cash-flow of 15.9, and EV/EBITDA of 14.6.

It's like comparing Manhattan real estate to Cleveland—both might be perfectly fine places to live, but one demands a significant premium.

Don't mistake my caution for bearishness. Lilly's product pipeline is robust, highlighted by Retatrutide, which has shown even more impressive weight-loss results—patients lost an average of 24.2% of their body weight (58 pounds) in clinical trials.

The company is also expanding its manufacturing footprint with four new US sites, creating 3,000 permanent jobs. It's acquiring promising treatments like Scorpion Therapeutics' STX-478 for $2.5 billion upfront.

Meanwhile, shareholders enjoyed $4.7 billion in dividends and $2.5 billion in buybacks last year, with a new $15 billion repurchase program and a 15% dividend increase announced for 2025.

I'd compare Lilly's stock to its own weight-loss drugs: remarkably effective, potentially life-changing, but priced at a level that makes you question whether the benefits justify the cost.

If May's results blast past expectations with raised guidance, I'll happily reconsider. Until then, I'm maintaining my 'hold'—admiring from across the room, but not ready to propose just yet.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-04-15 12:00:042025-04-15 12:07:38The Weight Of Expectations

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.