When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Biotech and Healthcare Letter

April 15, 2025

Fiat Lux

Featured Trade:

(THE WEIGHT OF EXPECTATIONS)

(LLY), (NVO)

You know that feeling when you've found the perfect restaurant? The food is exquisite, the atmosphere divine, and then you get the bill—and suddenly you're calculating if selling a kidney is a viable financial strategy.

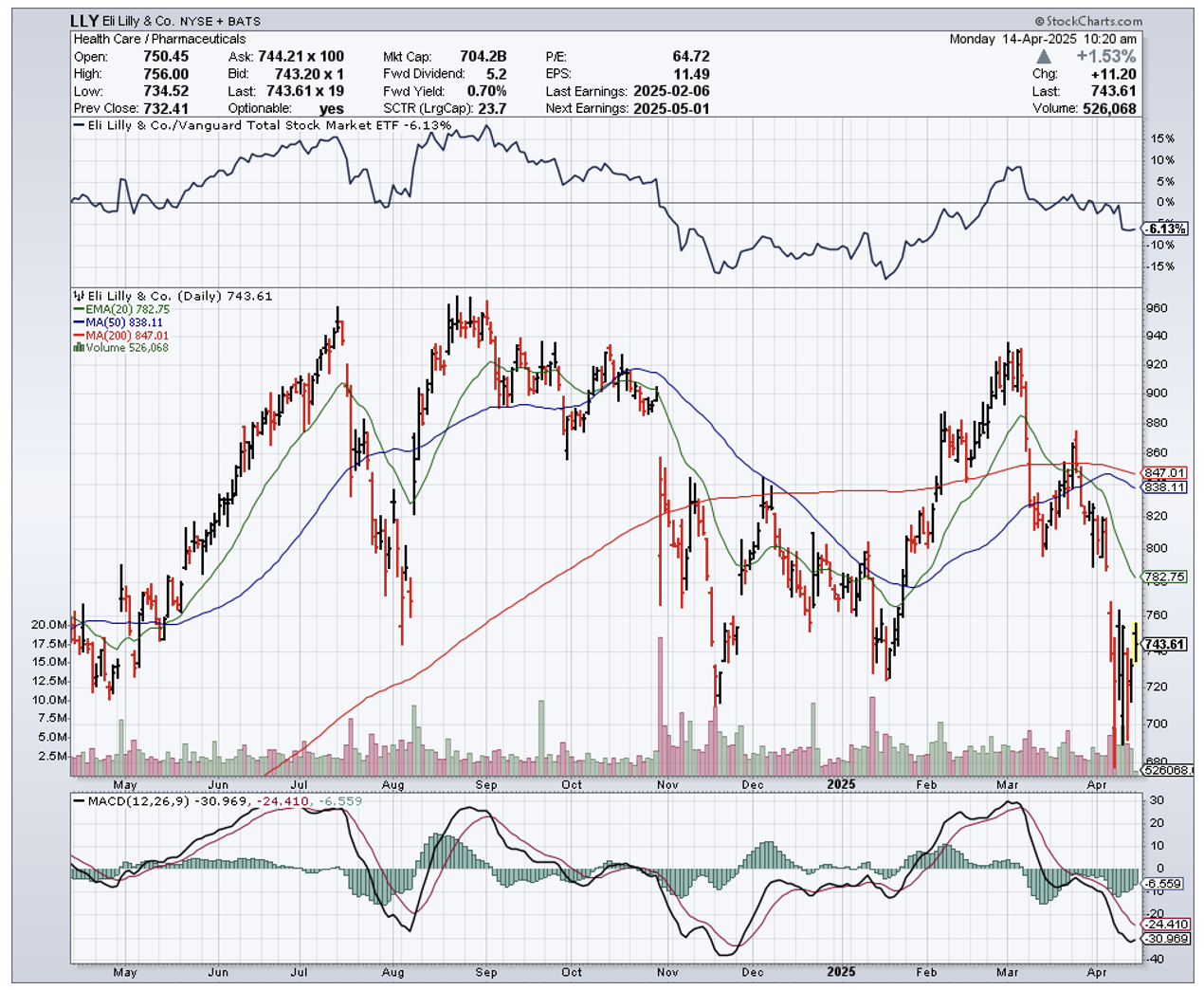

That's essentially my relationship with Eli Lilly (LLY) right now. Phenomenal company, stellar performance, price tag that makes my wallet weep.

I've had a complicated romance with this pharmaceutical juggernaut. Back in my hedge fund days, I learned that timing is everything with pharma stocks. It's like catching the perfect wave off Malibu – ride it too early, you're just splashing in the shallows; too late, and you're eating sand.

When I first spotted Lilly in June 2023, it was set up beautifully. Shares rocketed 56.2% before I downgraded to a 'hold' last February, while the broader market trudged along with a mere 12.3% gain.

Since then, the stock has performed almost exactly as predicted—just a 0.2% gain compared to the S&P 500's 1.33%. More recently, it's dropped 6.9% since January, looking positively rosy next to the broader market's 12.2% decline.

The company's fourth-quarter results read like a biotech investor's fantasy novel. Revenue soared 44.7% year-over-year to $13.53 billion, driven by its dynamic weight-loss duo.

Mounjaro's sales jumped 60.1% to $3.53 billion, while Zepbound exploded from $175.8 million to a jaw-dropping $1.91 billion.

I've watched patients in clinical trials shed substantial weight on these medications—one of my research contacts dropped 43.4 pounds since starting treatment—and I can tell you these drugs are creating waves not just in waistlines but across the entire healthcare sector.

Other stars in Lilly's portfolio include Verzenio for breast cancer (up to $1.56 billion from $1.15 billion), Jardiance for diabetes (climbing to $1.20 billion), and solid gains from Taltz and Humalog.

Only Trulicity disappointed, watching its revenue tumble from $1.67 billion to $1.25 billion—predictably cannibalized by Lilly's newer weight-loss offerings. It's like watching your reliable sedan gathering dust after buying a Tesla.

With this revenue bonanza, profits naturally skyrocketed. Net income more than doubled to $4.41 billion, adjusted profits surged to $4.81 billion, and operating cash flow swung from negative $311.9 million to positive $2.47 billion.

In my decades of following pharmaceutical stocks from Tokyo to Wall Street, I've rarely seen a quarterly performance this impressive. If Lilly were a student, it would be the annoying one breaking the curve for everyone else.

Looking ahead, management projects 2025 revenue between $58-61 billion (a 32.1% increase at midpoint) and adjusted EPS between $22.50-24.

For the upcoming Q1 report on May 1st, analysts anticipate revenue of $12.77 billion (45.6% higher year-over-year) and EPS of $4.70 (nearly double last year's $2.48).

So with all this financial wizardry, why maintain a 'hold'? One word: valuation.

Even using 2025's projected figures, Lilly trades at eye-watering multiples: forward P/E of 33.3, price-to-cash-flow of 27.6, and EV/EBITDA of 21.2.

For context, pharmaceutical peers trade significantly lower. Novo Nordisk (NVO), perhaps the most comparable given its similar weight-loss market success, trades at a P/E of 19.0, price-to-cash-flow of 15.9, and EV/EBITDA of 14.6.

It's like comparing Manhattan real estate to Cleveland—both might be perfectly fine places to live, but one demands a significant premium.

Don't mistake my caution for bearishness. Lilly's product pipeline is robust, highlighted by Retatrutide, which has shown even more impressive weight-loss results—patients lost an average of 24.2% of their body weight (58 pounds) in clinical trials.

The company is also expanding its manufacturing footprint with four new US sites, creating 3,000 permanent jobs. It's acquiring promising treatments like Scorpion Therapeutics' STX-478 for $2.5 billion upfront.

Meanwhile, shareholders enjoyed $4.7 billion in dividends and $2.5 billion in buybacks last year, with a new $15 billion repurchase program and a 15% dividend increase announced for 2025.

I'd compare Lilly's stock to its own weight-loss drugs: remarkably effective, potentially life-changing, but priced at a level that makes you question whether the benefits justify the cost.

If May's results blast past expectations with raised guidance, I'll happily reconsider. Until then, I'm maintaining my 'hold'—admiring from across the room, but not ready to propose just yet.

Global Market Comments

April 15, 2025

Fiat Lux

Featured Trade:

(HOW TO HANDLE THE THURSDAY, APRIL 17 OPTIONS EXPIRATION)

Followers of the Mad Hedge Fund Trader alert service have the good fortune to own FIVE in-the-money options positions that expire on Thursday, April 17, and I just want to explain to the newbies how to best maximize their profits.

These involve the:

Risk On

(COST) 4/$840-$850 call spread 10.00%

(TSLA) 4/$160/$170 put spread 10.00%

(NFLX) 4/$800-$810 call spread 10.00%

(NVDA) 4/$70-$75 call spread 10.00%

Risk Off

(MSTR) 4/$340-$350 put spread -10.00%

Provided that we don’t have a monster move in the market in three trading days, these positions should expire at their maximum profit points.

So far, so good.

I’ll take the example of the (NVDA) 4/$70-$75 call spread.

Your profit can be calculated as follows:

Profit: $5.00 expiration value - $4.50 cost = $0.50 net profit

(25 contracts X 100 contracts per option X $0.50 profit per option)

= $1,250 or 11.11% in 9 trading days.

Many of you have already emailed me asking what to do with these winning positions.

The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck, and pat yourself on the back for a job well done.

You don’t have to do anything.

Your broker (are they still called that?) will automatically use your long position to cover your short position, canceling out the total holdings.

The entire profit will be credited to your account on Monday morning, April 21, and the margin freed up.

Some firms charge you a modest $10 or $15 fee for performing this service.

If you don’t see the cash show up in your account on Monday, get on the blower immediately and find it.

Although the expiration process is now supposed to be fully automated, occasionally, machines do make mistakes. Better to sort out any confusion before losses ensue.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. You can probably unload those pennies below their maximum expiration value.

Keep in mind that the liquidity in the options market understandably disappears and the spreads substantially widen when a security has only hours or minutes until expiration on Thursday. So, if you plan to exit, do so well before the final expiration at the Thursday market close.

This is known in the trade as the “expiration risk.”

One way or the other, I’m sure you’ll do OK, as long as I am looking over your shoulder, as I will always. Think of me as your trading guardian angel.

I am going to hang back and wait for good entry points before jumping back in. It’s all about keeping that “Buy low, sell high” thing going.

I’m looking to cherry-pick my new positions going into the next quarter's end.

Take your winnings and go out and buy yourself a well-earned dinner.

Well done, and on to the next trade.

You Can’t Do Enough Research

(NVDA), (MSFT), (GOOG),(AMZN)

You know what's crazy? A company that burns $5 billion a year in computing costs getting valued at $300 billion.

Yet here we are. OpenAI just closed a monster funding round, raising up to $40 billion from investors including SoftBank Group at a staggering $300 billion valuation. That's nearly double what the company was valued at just six months ago.

I've seen this movie before, both as a hedge fund manager and while dodging Russian artillery in Ukraine. Euphoria rarely ends well, whether in markets or on battlefields.

The company behind ChatGPT has become the darling of the investment world despite the fact that it won't be profitable until 2029, according to Sam Altman's own projections. 2029! That's four years and several AI generations from now.

This is a company that expects to generate $13 billion in revenue this year, which sounds impressive until you realize they'll likely spend more than that on computing costs alone. In fact, in 2024, OpenAI reported revenue of around $4 billion while racking up $5 billion in computing costs just to train and run their models.

When I was running hedge funds in the 1990s, we had a technical term for businesses like this: money pits.

Let's dive deeper into these numbers. Over 90% of OpenAI's 500 million users worldwide pay absolutely nothing to use the service. In 2025, the company projects that just under 5% of users might pay the $20-a-month charge to access their more advanced AI models. That would generate about $5.5 billion. Another 0.3% might opt for ChatGPT Pro, contributing another $3.6 billion.

The trouble is that a whopping 70% of OpenAI's revenue comes with expenses that may keep rising faster than the top line. According to reporting from The Information, by the end of the decade, OpenAI will still probably spend 60% to 80% of its annual revenue just to train or run its models.

Meanwhile, competition is heating up. OpenAI's market share of enterprise large language models (LLMs) has already fallen to 34% in 2024 from 50% a year ago, according to Menlo Ventures data. Companies like Anthropic, Meta, Google, and Mistral AI are eating into their lead.

And there's another problem: intense pricing competition. As companies like Mistral AI and Anthropic offer competitive alternatives, OpenAI's ability to charge premium prices for its API services is under pressure.

During my decades reporting from Asia, I witnessed countless companies with "revolutionary technology" that eventually became commoditized faster than anyone expected. When I covered the Japanese semiconductor industry in the 1970s, companies that once had seemingly unassailable leads saw their margins evaporate within years.

So why are investors like SoftBank's Masayoshi Son so eager to pour billions into this cash-burning machine? The answer lies in the potential of achieving artificial general intelligence (AGI) – AI systems that can perform any intellectual task that a human can. If OpenAI succeeds in developing AGI, the economic rewards could be incalculable.

In a fascinating twist, OpenAI just made its first cybersecurity investment, putting money into a startup called Cosmic. This signals a strategic expansion beyond its core AI development work. Smart move, considering that as AI becomes more ubiquitous, securing it becomes increasingly critical.

Additionally, there are rumors that OpenAI may release an open-source model, which would be a significant shift in strategy. This could be a play to expand their ecosystem and solidify their position as the standard-bearer in AI development.

For investors trying to play the AI revolution, the question becomes: is it better to invest directly in pure AI plays like OpenAI (if and when it goes public), or in the companies that actually make money from the AI boom today?

The smartest money might be in NVIDIA (NVDA), which supplies the crucial GPUs that power AI development. Despite trading at seemingly high multiples, NVIDIA continues to see explosive growth in data center revenue as AI development accelerates. Even with competition from AMD and Intel, NVIDIA maintains a commanding lead in AI chip technology.

Microsoft (MSFT) provides another interesting angle, given its deep partnership with OpenAI. The company has exclusive rights to commercialize OpenAI's technology and has already integrated ChatGPT capabilities across its product line, from Bing to Office 365.

For those looking at pure AI plays beyond the giants, Anthropic (backed by Google (GOOG) and Amazon (AMZN)) and Mistral AI represent interesting alternatives to OpenAI, though they remain private for now.

Is AI revolutionary? Absolutely. Are most AI companies going to make money anytime soon? Don't bet your retirement on it. For OpenAI to hit Altman's projected $125 billion revenue target by 2029, they need to grow 10-fold while dramatically shifting from money-losing free users to enterprise clients that actually pay the bills.

That's a tall order, even for a company with seemingly unlimited access to capital. I've witnessed too many "guaranteed successes" implode over my five decades in the markets. After covering countless bubbles from Tokyo to Silicon Valley, I've learned that eventually, cash flow matters. Always.

If I were allocating capital today, I'd be putting my money on companies with proven ability to convert AI hype into actual profits. Let others chase the AGI dream while you count real returns.

At this late stage in my life, I've learned that what seems inevitable rarely is, and what looks impossible often becomes routine within years. Will OpenAI justify its $300 billion valuation? Perhaps. But at these prices, investors are paying for perfection when the company hasn't even figured out a sustainable business model.

That's not investing – that's speculation.

And if there's one thing my bullet wound from Ukraine taught me, it's that life's too short for bad bets.

Mad Hedge Technology Letter

April 14, 2025

Fiat Lux

Featured Trade:

(BIG TECH ANXIOUS FOR CLARITY)

(MSFT), (AAPL), ($COMPQ)

At this pace, nobody knows what the government policies will look like, and if this doesn’t change, the uncertainty will bleed into lower tech stocks ($COMPQ).

Tech has had a hard short-term run, and the unstable backdrop will lead to investors pausing on big tech stock purchases.

Tech businesses are also reigning in their investment spend, waiting to see what happens.

Microsoft (MSFT) has already made announcements on pausing its AI database build out and that has really chilled momentum in the wider AI trade.

If this electronics exemption announced Friday night is true, it represents an important temporary win for Apple (AAPL) and other China-dependent technology giants.

News reports that producing the iPhone in America could cause the price of a new iPhone to double send shockwaves throughout the investment community.

The federal government might have to pull back their aggressive policies when factoring in surging yield in interest rates and a short-term collapse of the dollar.

The president said these products are simply moving to a different tariff "bucket," telling reporters that a separate rate for semiconductor tariffs will be announced over this week.

Trump added that his goal is to "uncomplicate" things by moving production to the US but that companies will have a say.

Either way, the fact remains that Trump has offered at least a temporary boost to companies with close links to China, and investors are responding by sending stocks of directly impacted companies like Apple and Dell (DELL) higher this morning.

These technology companies' goods are still subject to 20% blanket tariffs on China over fentanyl and likely face legacy sector-specific tariffs from Trump 1.0 and the Biden era, but they are now able to sidestep the lion's share of the 145% rate that is now in place for other goods.

The move is also a significant walk back of Trump's overall tariff plans, with electronics representing the top exports from China to the US.

This weekend's move means the overall effective tariff rate on US imports is now 22% — down from 27% just last week.

The smaller the tech company is, the bigger they are impacted with this whipsawing strategy of threatening all your trading partners.

Larger companies certainly have more options than small businesses to dodge the tariffs due to their worldwide networks and political relationships.

Apple, as one example, also gained attention in recent days for reportedly chartering cargo flights to move as many as 1.5 million iPhones to the United States from India quickly to get ahead of tariffs there.

Tech shares are pricing in nothing positive emerging in the short-term.

Management doesn’t want to get burned by moving in one direction, only to see a product get wiped out due to high costs.

It is hard to change the issue of how the U.S. relocated the supply chain to cheaper foreign countries.

The consensus of higher prices comes after Americans have been dealing with uncontrollable inflation since 2020.

The extra price increase preceding Trump’s tariff crusade has consumers in a hole.

Even compared to 2024, I don’t see where the incremental dollar comes into the tech sector when margins are being squeezed in real time.

At best, we could experience a bear market or choppy sideways price action to reflect a tougher environment for doing tech businesses, whether it is streaming, software, hardware of EVs.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more