According to the betting markets, the odds of a recession

Overnight, have tanked from over 80% to just a fraction under 40%.

It is interesting to see such a development and speaks volumes to how volatile the tech markets are right now.

The V-shaped price action by the Nasdaq index ($COMPQ) perhaps forced the hand of decision makers.

Here we stand, only 6% from all-time highs after a vicious reversal to the upside.

I think it is fair to say that the belief in tech stocks has not corroded and is just resting.

Even though what was agreed was just a 90-day pause, the biggest takeaway is that the Americans aren’t willing to just blow the world order up.

The Chinese won’t just be moved to the side and switched in for Indians like a 6th man coming off the bench.

In fact, this signals that China has a big role to play in the upward trajectory of tech stocks, and that is why the tech index has exploded to the upside this morning.

Some of the tape is mind-boggling.

At the time of this writing, Amazon (AMZN) is up 8% and the Nasdaq is up over 4% in just ONE DAY.

To say this is a victory for tech is an understatement as the world’s two biggest economies unwound for now most of the tariffs they had imposed on each other since April in a tit-for-tat battle that was threatening to stoke U.S. inflation, crash China’s export engine, and upend the global economy.

The U.S. agreed to lower the base level of tariffs on most Chinese goods to 30%, from 145%, while China said it would cut its levies on U.S. products to 10% from 125%.

The U.S. tariff on many Chinese products will be higher than 30%. U.S. duties on steel, aluminum, and autos remain in place, as do some earlier tariffs on certain Chinese goods imposed during President Trump’s first term in office and that of former President Joe Biden.

Washington and Beijing agreed to keep the new tariff levels in place for 90 days, with the goal of working toward a broader deal on trade in further talks.

For China, an unrestrained trade clash with the U.S. would threaten millions of jobs tied to serving U.S. consumers and potentially worsen trade tensions with other countries wary of a surge in Chinese imports. China was also worried about losing access to some U.S. products it still needs, such as Boeing planes, aircraft parts, and certain chips.

In the short-term, I believe we are ready for a short squeeze higher.

The market was taken by surprise by the sudden announcement, and many companies were bracing for another onslaught of negative news.

In the next 60 to 90 days, I can easily see the US dollar popping higher, tech firms reforecasting higher revenue targets, and the Nasdaq coalescing around the positive energy to surge higher.

That’s not to say that everything is hunky and dory, we are literally just one tweet away for the market collapsing and going into a tailspin.

The risk levels have never been higher, and I would urge readers to keep positions small.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-05-12 14:02:312025-05-12 15:31:16The Fight For AI Supremacy

(CHINA AND THE U.S. AGREE TO A TRADE DEAL IN SWITZERLAND)

May 12, 2025

Hello everyone

WEEK AHEAD CALENDAR

MONDAY, MAY 12

8:30 a.m. Australia Consumer Confidence

Previous: -6%

Forecast: 2%

TUESDAY, MAY 13

6:00 a.m. NFIB Small Business survey (April)

8:30 a.m. CPI (April)

WEDNESDAY, MAY 14

9:30 p.m. Australia Unemployment Rate

Previous: 4.1%

Forecast: 4.1%

THURSDAY, MAY 15

8:30 a.m. Initial jobless claims (week ended May 10)

8:30 a.m. Retail sales (April)

8:30 a.m. PPI (April)

8:30 a.m. Empire State mfg index (May)

8:30 a.m. Philadelphia Fed mfg index (May)

9:15 a.m. Industrial production (April)

10:00 a.m. Business inventories (March)

10:00 a.m. NAHB survey (May)

FRIDAY, MAY 16

8:30 a.m. Housing starts (April)

8:30 a.m. Import prices (April)

The U.S. & China meeting in Switzerland: will it deliver?

The news has just come through…

U.S. and China have agreed to slash tariffs for 90 days in a major tariff breakthrough.Reciprocal tariffs will be cut from 125% to 10%.Both the U.S. and China said they will continue discussions on economic and trade policy.What is in doubt is whether the 90-day pause is enough time for the two sides to reach a detailed agreement.But at least we have some movement on negotiation.Dow futures have jumped 1000 points, gold has fallen, and the U.S. dollar has surged.

In other news…

The health of the consumer will be clearly visible this Thursday when we see retail sales data and the producer price index report.We will also see the CPI report which will tell us how the trade conflict has affected inflation.

The S&P 500 has already rallied more than 13% from its April 8 lows, so the market may need a positive surprise on the trade front to take another big jump.

I tend to believe the limited ranges we have been seeing have been in anticipation of some de-escalation out of China, and as such, when the actual news comes out, the market reaction might be rather ho-hum and could even mark a tactical top, regardless of what the news is.

This level in the market could be a good time to re-establish short positions or add to them if you have them already.

They don’t make things like they used to…

White goods, toys, heaters, whatever you can think of – most of these things don’t have a long life.

Some products don’t even outlast the warranty period before they break down and stop working, or need a part replaced, which is not even worth the cost.

Consider the cost of getting someone to your house to replace the part and the cost of the part.It’s often not worth it.

I remember growing up with a Kelvinator refrigerator, which lasted around 30-40 years.Can you imagine anything lasting that long today?

Today, companies make products that are designed to break down, so the consumer must go back and buy another one.

Forty and fifty years ago, we didn’t have the technology we have today, so why, with all the technology we have now, is it so difficult to make quality products?

I’m not saying all products are poorly made, but you must admit that the quality overall is not evident.

It seems companies making money trumps making quality – so disappointing.

MARKET UPDATE

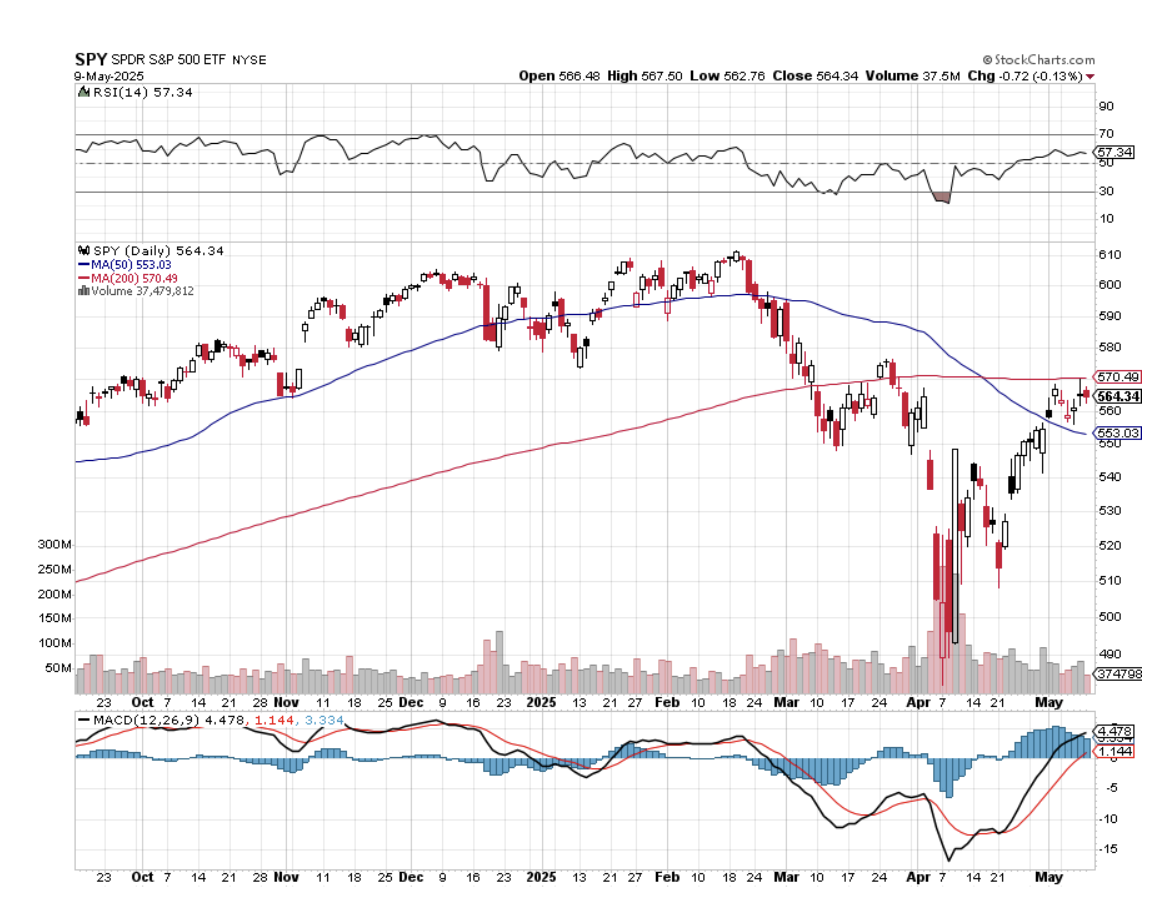

S&P500

The index is up 13% since the April lows at 4835. No confirmation that we have seen a top yet, although upside momentum is slowing and suggests further gains would likely be limited, as the potential of a peak for at least a few weeks/months is rising.So far, we have had a high of S&P 500 5832 in the futures.

Support: 5575/85, 5475/85

Resistance: 5760/85 area/5830

GOLD

Bearish technical data is visible in the gold chart (sell mode on the MACD) & and an overbought pattern. However, we could still see more ranging/consolidation before gold completely rolls over.

Support: $3268/73 & $3197 & $3075

Resistance: $3353 & $3438/43

BITCOIN

We’ve seen Bitcoin move sharply higher – the long-term view remains in focus with a target between $125k and $150k.The market is getting overbought with such a sharp move, so some consolidation might be in front of us before further moves to the upside.

Support: $99.90/$100.4k & $96.0/$96.4k

Resistance: $104.4k

HISTORY CORNER

On May 12

QI CORNER

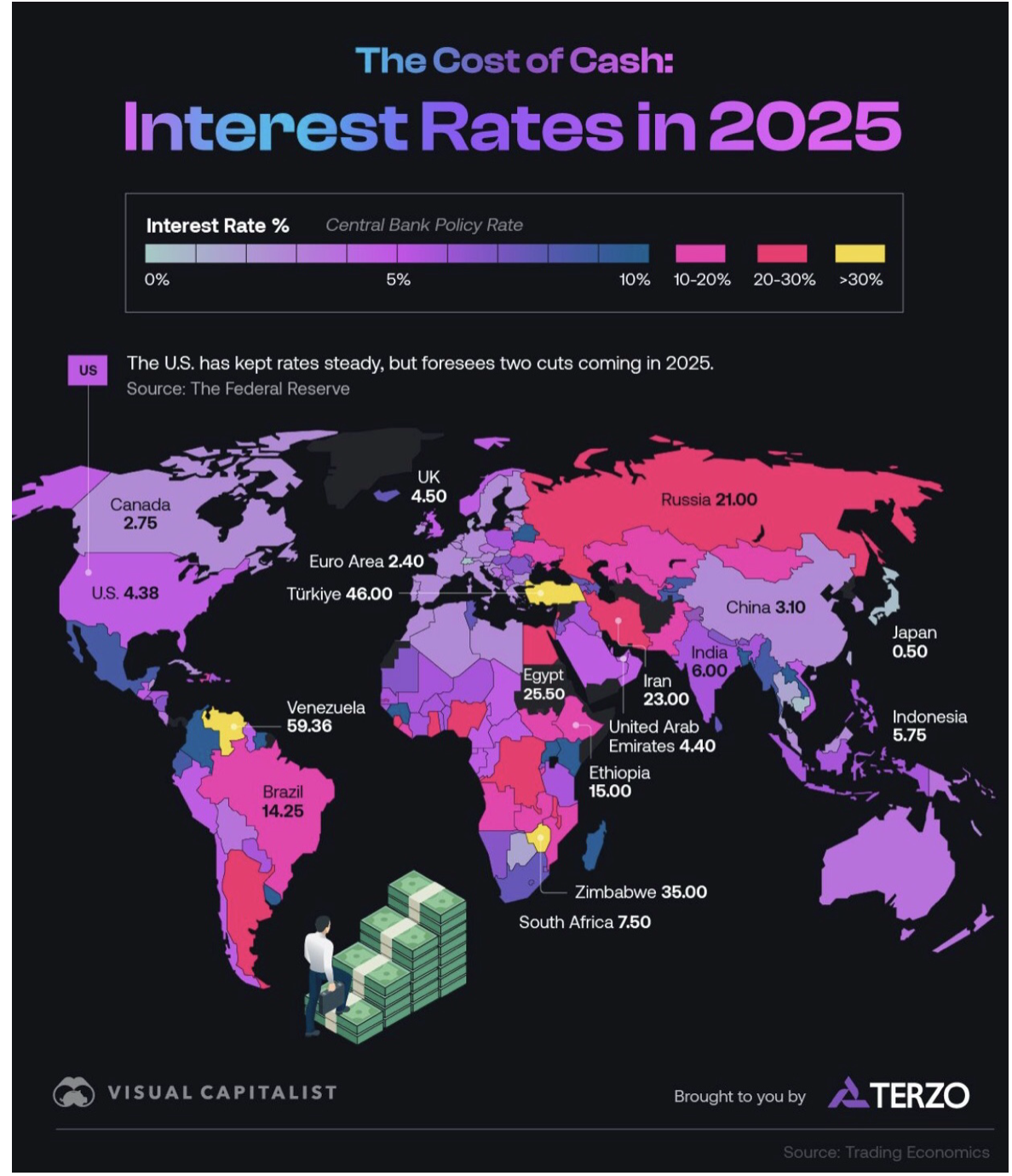

U.S. officials met with Chinese counterparts in Switzerland this past weekend to address the trade war between the world’s two biggest economies.This chart from Spencer Hakimian, founder of Tolou Capital Management, shows why a ratcheting back of rhetoric, at the very least, should be expected.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-05-12 10:10:162025-05-12 10:10:16Trade Alert - (JPM) May 12, 2025 - TAKE PROFITS - SELL

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WAITING FOR THE MISSILES TO HIT)

(GLD), (SPY), (MSTR), (NVDA), (AAPL),

(TSLA), (QQQ), (TLT), (SH), (MCD), (SVXY)

When I was in Ukraine, the air raid sirens used to go off every night exactly at 2:00 AM.

The Russian goal was to deprive the civilian population of sleep and to make their lives miserable. It was also when the country was least able to defend itself.

You knew the missiles were on the way, it was just a question of whether your number was up. You could only hope to make it to the basement before they hit. It was not safe to go back to sleep until you heard the explosions nearby.

It is not a pleasant feeling.

Here we are in the United States in 2025, and there are missiles on the way, but they are economic ones. Ford Motors (F) has already started raising prices so they can spread them out over a longer period of time. Food and produce prices from Mexico will deliver the first price shocks, as they can go bad in a day. The first hint of this might be visible with the release of the Consumer Price Index at 8:30 AM EST on Tuesday, May 13. That’s when we learn if the inflationary surge is hitting now, or if we have to wait until June. But we know for sure it’s coming.

In fact, there is an onslaught of horrific economic data headed our way. Economic growth is slowing dramatically, prices are rising, international trade is grinding to a halt, and consumer confidence is already at all-time lows. We just don’t know yet if it is going to hit us or blow up the neighbors down the street.

The truly alarming thing about these developments is that the data from hell is going to hit just as the stock market is completing one of its most rapid rises in history, up 19.75% in a month. Stocks are now even more expensive than they were in February, with a price earnings multiple of 22X and earnings falling.

Is anyone ready for a February market crash repeat? You may be about to get it.

I have been through many bear markets since I started trading in 1965, a move down in the indexes of 20% or more. They can last 31 months (2002) and decline as much as 56% (2009). In 1987, we had a bear market in a day!

This one is number nine for me. And while no two bear markets are alike, they all share common characteristics. I have seen them caused by oil shocks, hyperinflation, financial engineering, the Dotcom Crash, the Great Financial Crisis, and the Pandemic. This is the first one caused by a trade war.

Spoiler alert! The monster is about to jump out of a closet at you at the end of the movie.

If you’re praying that the new trade deal with the UK is going to rescue your retirement funds, don’t hold your breath. It’s not a treaty; it is simply an agreement to agree sometime in the distant future. It’s not even a letter of intent. It’s nothing but a bunch of hot air.

In 2024, the U.S. actually ran a trade surplus, not a deficit, with the UK. The surplus was $11.9 billion. The U.S. exported $79.9 billion worth of goods to the U.K. and imported $68.1 billion, resulting in a surplus.

Some $10.5 billion of US aircraft were sold to the UK in 2024, followed by $7 billion in machinery and nuclear reactors and $5.6 billion in pharmaceuticals. The deals announced last week were nothing new, just a reaffirmation of existing trade that has been going on for years.

In the meantime, the punitive 10% tariff against UK imports stands. That is nowhere near enough to move the needle for the $27.7 trillion US GDP. And this was the easy one. Why the US needs to negotiate a trade agreement with a country where it is already running a surplus is beyond me.

All of this has prompted me to run the first 100% short model portfolio in the 17-year history of the Mad Hedge Fund Trader. If the market moves sideways or up small, we will make our maximum profit by the June 20 option expiration in 28 trading days (Memorial Day is a Holiday). If the market crashes, which it can do at any time, we make the maximum profit immediately. That should take us to a 2025 year-to-date profit of over 43%.

Heads I win, tails you lose, I like it.

Current Capital at Risk

Risk On

NO POSITIONS 0.00%

Risk Off

(GLD) 5/$275-$285 call spread -10.00%

(GLD) 6/$275-$285 call spread -10.00%

(SPY) 6/$610-$620 call spread -10.00%

(MSTR) 6/$500-$510 put spread -10.00%

(NVDA) 6/$140-$145 put spread -10.00%

(AAPL) 6/$220-$230 put spread -10.00%

(TSLA) 6/$370-$380 put spread -10.00%

(QQQ) 6/$540-$550 put spread -10.00%

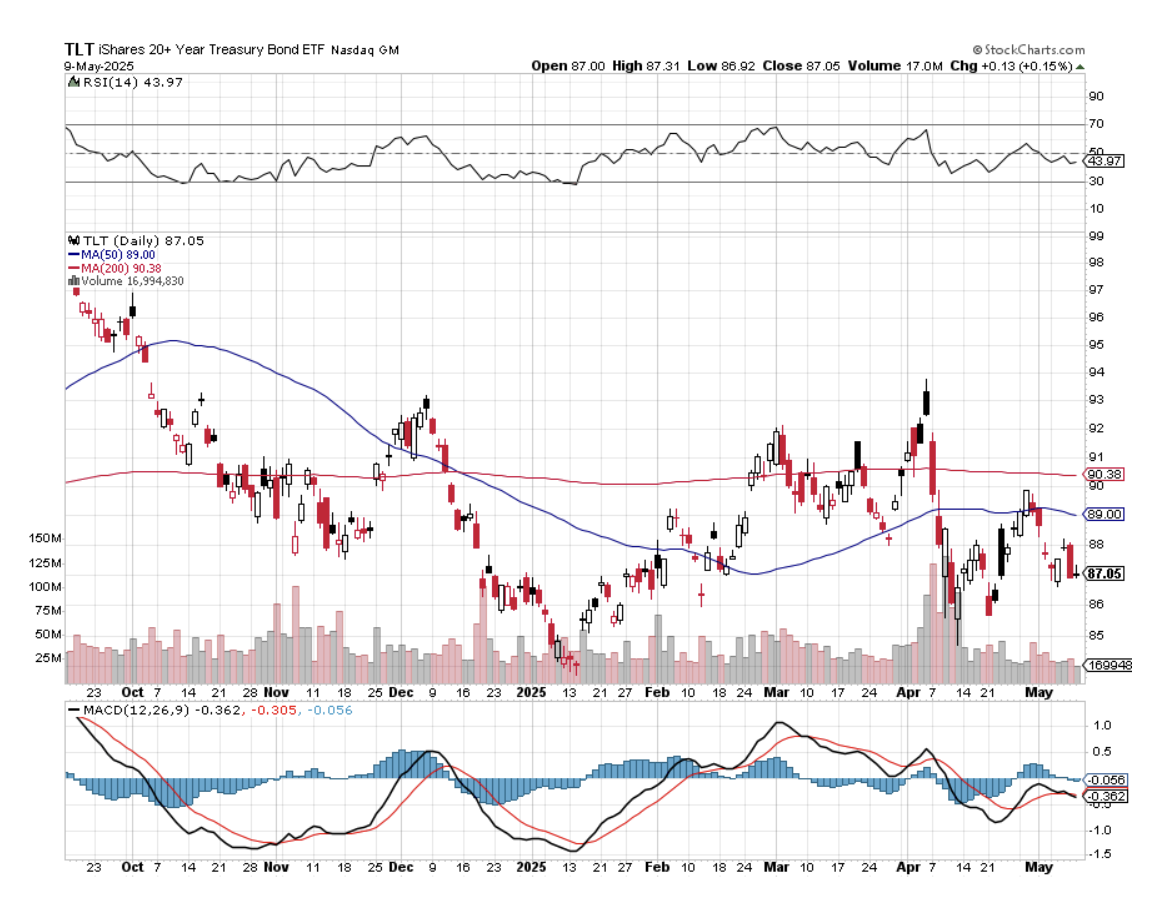

(TLT) 6/$80-$83 call spread -10.00%

(SH) 6/$39-$41 call spread -10.00%

Total Net Position -100.00%

Total Gross Position 100.00%

I love trade wars.

They shine brilliant spotlights on obscure, usually deeply hidden parts of the global economy, revealing almost impossible-to-find data points. And every single new data point enhances your understanding of the big picture.

My first real trade war was the 1973 Oil Shock. Saudi Arabia had cut off America’s oil supply because of our support for Israel in the Yom Kippur War. Huge lines formed at gas stations, and gasoline prices shot up from 25 cents a gallon to $3.00.

Ever the entrepreneur, I started a side business buying beat-up Volkswagen Beetles, the highest mileage car then available in the United States, driving them to Mexico, and getting them repainted and reupholstered in a day for $50. Then I resold them in LA for double the price.

I remember on my last run, I was in a hurry to catch a physics class, so I left a little early. The US customs office learned about the car and asked me if I had any work done while in Mexico. I answered “No.” As he walked away, I saw that his pants were covered with fresh green paint, which had not yet dried.

I drove away as fast as my green Beetle could go.

In the old days, hedge funds reaped huge trading advantages chasing down obscure data points. When satellite data became available to the public in the 1990s, my fund leased satellite time to track the progress of the US wheat crop.

Several successful trades in the commodities markets followed, until others caught on. You already know that I closely track container ship traffic not only in Los Angeles, but ports around the world. This is easy now through many cheap apps available through Apple’s App Store..

In the 2025 stock market, we have all had to become our own mini hedge fund managers. For a start, more money has been made on the short side than the long side, at least the few who participated in instruments like my many vertical bear put debit spreads in (NVDA), (SPY), (TSLA), (MSTR), and the (TLT). There were also nicely profitable plays in the (SH), the (SDS), and the many volatility plays out there, such as the (SVXY).

It's all been enough to help me achieve a welcome 32% profit this year. Those who took my advice to sit out 2025 and bought 90-day US Treasury bills yielding 4.2% are also profitable this year. Any positive return this year is a great accomplishment.

A whole new cottage industry that has gone viral on the internet, offering up more obscure data points about the economy than we could ever consume. We all know that forward-looking soft sentiment data is the worst ever recorded. Credit card balances held by low-income consumers are at all-time highs. But McDonald’s (MCD) and Taco Bell sales have been falling, while those at Domino's Pizza are rising.

What the heck is that supposed to mean?

Although this may sound arcane and deep in the weeds, the 2 year – 10 year spread recently turned positive and is now at 0.47%. That means the yield on two-year Treasury notes is higher than the yield on ten-year Treasury bonds. This has NEVER happened without a following recession. If you were looking for hard data, this is hard data.

Gold is the only asset class absent from volatility this year. That alone says a lot.

There are more than the usual number of binoculars focusing on the Port of Los Angeles these days (click here for the link). Traffic is now down a stunning 25% on the week. That means a supply chain disaster is imminent.

You learn in the Marine Corps that a 50-cent part can ground a $60 million aircraft. How much extra will you pay to get that 50-cent part to get the plane flying? $1.00, $10? $100? Certainly $1 million for a military aircraft in time of war.

This is the basis for some of the exponential inflation forecasts and supply chain disruptions on the scale last seen during the pandemic. Once started, inflation takes off like a rocket with merchants trying to outraise each other and it can take years to get under control, as we saw with the last pandemic.

By the way, I still wake up at 2:00 AM every morning expecting incoming missiles, even though I have been out of Ukraine for 18 months. It turns out that post-traumatic stress gets worse when you get older. Fortunately, my bedroom is now in the basement.

The Lucky One (it was a dud)

The Not So Lucky Ones

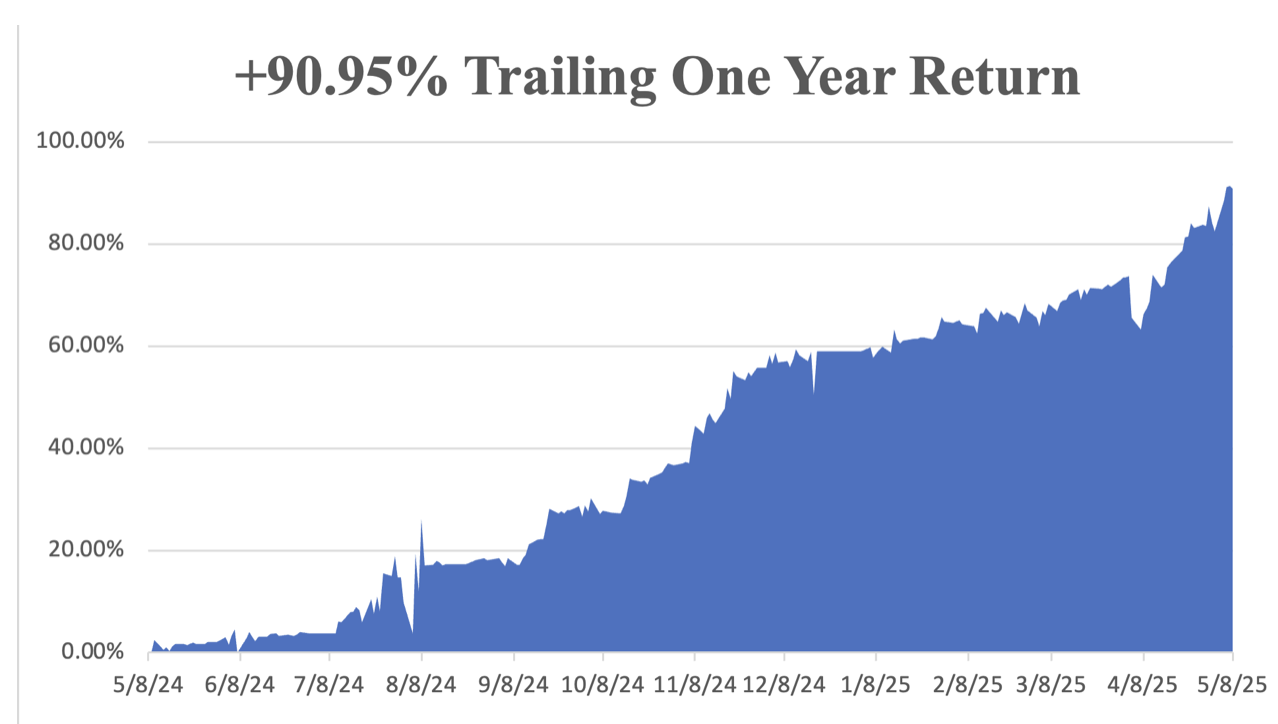

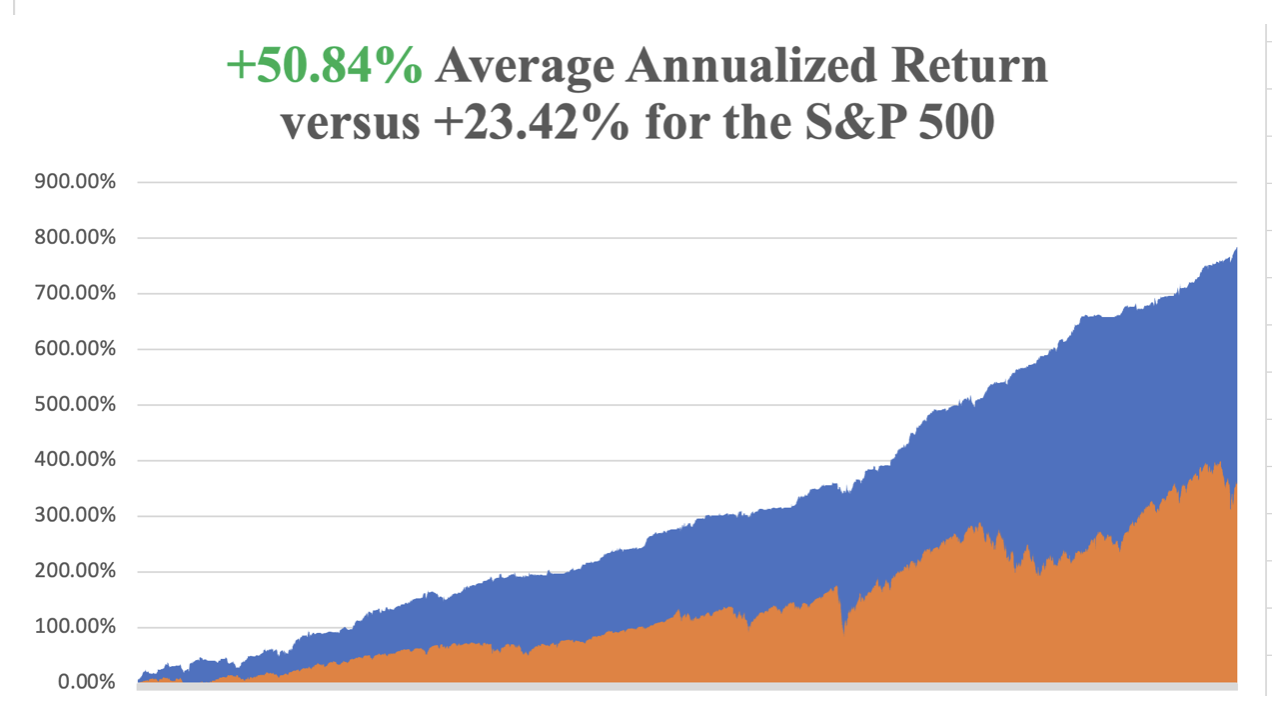

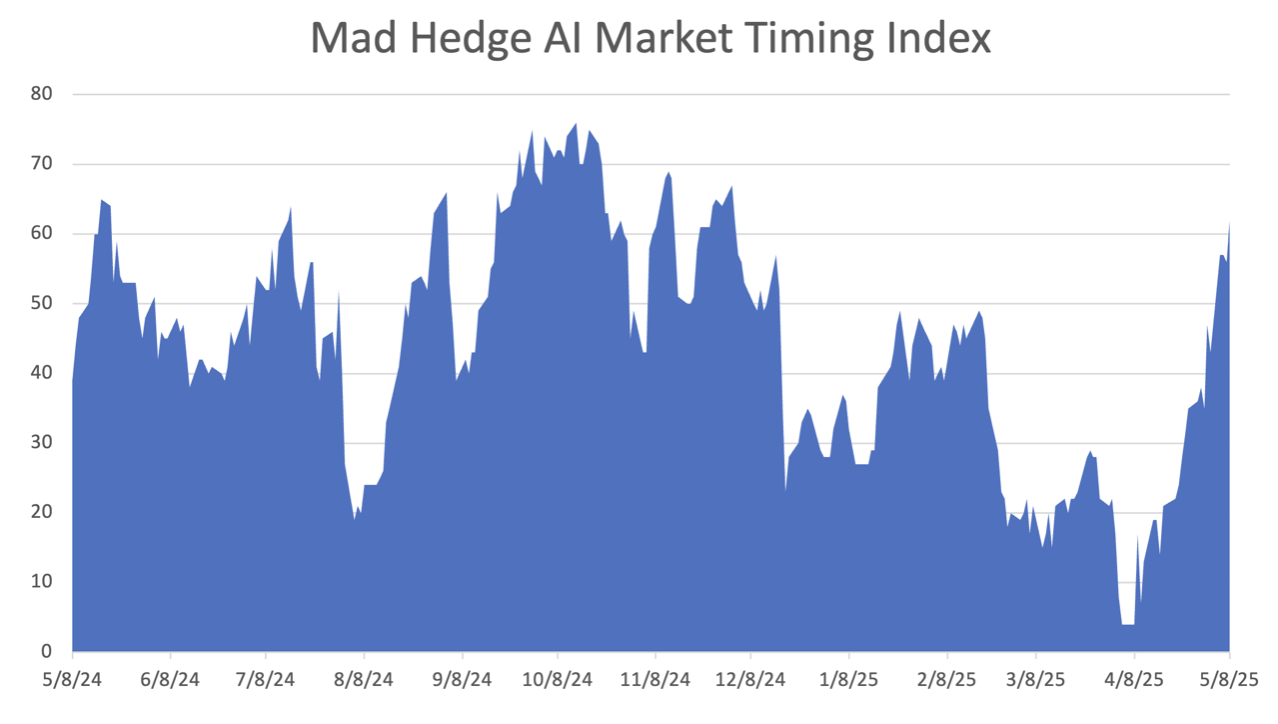

My May performance has reached +3.08%. That takes us to a year-to-date profit of +31.48%so far in 2025. My trailing one-year return stands at a record +90.95%. That takes my average annualized return to +50.84%and my performance since inception to +783.37%, a new all-time high.

It has been another wild week in the market. I took profits in longs in (MSTR) and (NVDA). I stopped out of a short in (SPY) for a small loss. I added a new long in (GLD) and (TLT), new shorts in (QQQ), (AAPL), and (TSLA). After the tremendous run we have just seen, I am moving towards a 100% short portfolio.

Some 63 of my 70 round trips in 2023, or 90%, were profitable. Some 74 of 94 trades were profitable in 2024, and several of those losses were really break-even. That is a success rate of +78.72%.

Try beating that anywhere.

The Stock Market is Headed for New Lows, even if the China tariffs drop from 145% to only 50%, says hedge fund guru and old friend Paul Tudor Jones. Trump’s rollout of the highest levies on imports in a century shocked the world last month, triggering extreme volatility on Wall Street. You have Trump, who’s locked in on tariffs. You have the Fed, which is locked in on not cutting rates. That’s not good for the stock market. We are the losers.

Fed Leaves Interest Rates Unchanged, at 4.25%-4.50%, supported by a consistently rising inflation rate. Stocks tanked and bonds rallied. In case you were wondering, the Fed ALWAYS prioritizes fighting inflation over unemployment because its mandate is to protect the value of the US dollar. It’s written into the 1913 law creating the Federal Reserve System. Don’t expect ANY rate cuts until year-end.

Apple Tanks on Falling Search Revenues. I bet you don’t get many short recommendations for Apple, but here’s a nice one. The implications for Apple were disastrous when a senior officer testified that artificial intelligence was demolishing their traditional search business. Of course, Alphabet (GOOGL) shares were trashed, down 7%. But Apple took a 5% hit as well because it earns an eye-popping $50 billion a year from its IOS operating system, referring all searches to Google. Apple shares have been trading rather feebly this month. While the S&P 500 rocketed 15%, (AAPL) managed to eak out an unimpressive 20% gain, while shares like Palantir (PLTR) doubled.

Bitcoin Recovers $100,000, for the first time since early February, bolstered by a dial down of the trade war in a sign that perhaps Trump is backing off his trade war. Overbought for now, sell Bitcoin rallies.

Nearly All US Exports are in Free Fall, reaching most ports across the U.S. and nearly all export market products as the trade impact of Trump’s tariffs worsens. Agriculture exports to China have been the hardest hit.

Oil Production has Peaked, thanks to the collapse in prices triggered by recession fears. Saudi Arabia is playing a market share game, and increasing production is another factor. Avoid all energy plays like the plague. We’re headed for $30 a barrel.

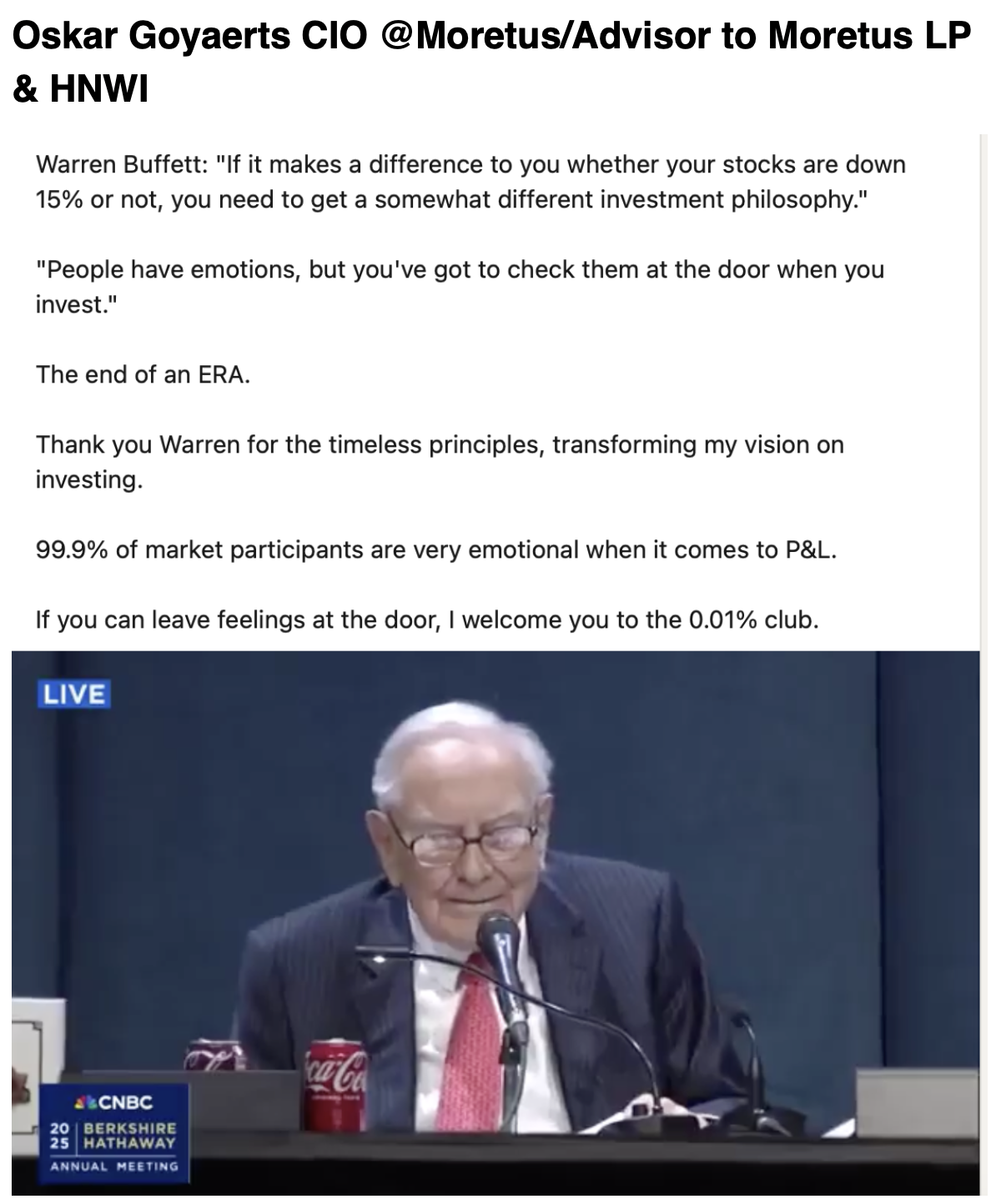

Warren Buffett Retires, handing over day-to-day management of Berkshire Hathaway (BRK/B) to Greg Abel. It’s a personal blow as Warren was one of the first subscribers to Mad Hedge Fund Trader. No one could ever match his investment performance, not even Warren himself, as stocks are so much more expensive now. Even if (BRK/B) shares dropped 99% from today, it would still be the top-performing S&P 500 stock since 1965. Listening to his annual shareholder summit, he’s still all there at age 94. I want to be Warren Buffett when I grow up.

Is Tesla the Next Boeing? By cutting production costs by 17% last year, has Musk also made the cars unsafe? That’s what happened to Boeing (BA), which prioritized raising dividends and share buybacks over quality and safety to the point where its aircraft started falling out of the sky. This year, (TSLA) shares have been matching (BA) downside one for one.

Jeff Bezos to Sell $4.7 Billion of Amazon Stock by May 2026. Time to free up some spending money. Jeff sold $13.4 billion worth of shares in 2024. Some of the money will go to finance his Blue Origin rocket hobby. Bezos still owns 9.56% of the $2 trillion company.

My Ten-Year View – A Reassessment

We have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties, is now looking at multiple gale-force headwinds. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. My Dow 240,000 target has been pushed back to 2035.

On Monday, May 12, at 8:30 AM EST, the WASDE Report is announced, the World Agriculture Supply and Demand Estimate.

On Tuesday, May 13, at 7:30 AM, the Consumer Price Index, a key inflation read, isreleased.

On Wednesday, May 14, at 9:30 AM, EIA Oil Stocks are disclosed. No move is expected in the face of a rising inflation rate. A press conference follows at 1:30.

On Thursday, May 15, at 8:30 AM, the Weekly Jobless Claims are disclosed. We also get the Producer Price Index and Retail Sales.

On Friday, May 16, at 7:30 AM, we get Housing Starts and Building Permits. At 1:00 PM, the Baker Hughes Rig Count is published. As for me, one of the many benefits of being married to a British Airways senior stewardess is that you get to visit some pretty obscure parts of the world. In the 1970s, that meant going first class for free with an open bar, and sometimes in the cockpit jump seat.

To extend out 1977 honeymoon, Kyoko agreed to an extra round trip for BA from Hong Kong to Colombo in Sri Lanka. That left me on my own for a week in the former British crown colony of Ceylon.

I rented an antiquated left-hand drive stick shift Vauxhall and drove around the island nation counterclockwise. I only drove during the day in army convoys to avoid terrorist attacks from the Tamil Tigers. The scenery included endless verdant tea fields, pristine beaches, and wild elephants and monkeys.

My eventual destination was the 1,500-year-old Sigiriya Rock Fort in the middle of the island, which stood 600 feet above the surrounding jungle. I was nearly at the top when I thought I found a shortcut. I jumped over a wall and suddenly found myself up to my armpits in fresh bat shit.

That cut my visit short, and I headed for a nearby river to wash off. But the smell stayed with me for weeks.

Before Kyoko took off for Hong Kong in her Vickers Viscount, she asked me if she should bring anything back. I heard that McDonald’s has just opened a stand there, so I asked her to bring back two Big Macs.

She dutifully showed up in the hotel restaurant the following week with the telltale paper back in hand. I gave them to the waiter and asked him to heat them up. He returned shortly with the burgers on plates surrounded by some elaborate garnish. It was a real work of art.

Suddenly, every hand in the restaurant shot up. They all wanted to order the same this, even though the nearest stand was 2,494 miles away.

We continued our round-the-world honeymoon to a beach vacation in the Seychelles, where we just missed a coup d’état, a safari in Kenya, apartheid South Africa, London, San Francisco, and finally back to Tokyo. It was the honeymoon of a lifetime.

Kyoko passed away in 2020 from breast cancer at the age of 50, well before her time.

Sigiriya Rock Fort

Kyoko

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader|

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-05-12 09:02:382025-05-12 11:54:20The Market Outlook for the Week Ahead, or Waiting for the Missiles to Hit

“My job is to find 10 problems for every three that exist,” said Jeffrey Gundlach of DoubleLine Capital.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-05-12 09:00:382025-05-12 11:54:10May 12, 2025 - Quote of the Day

You know what's more complicated than explaining blockchain to your grandmother? Keeping up with OpenAI's corporate structure.

Just when I thought I had a handle on their business model (scribbled on the back of a cocktail napkin during a particularly illuminating earnings call), Sam Altman and his crew decided to reshuffle the deck.

OpenAI just pulled off what I'm calling the "nonprofit boomerang" – tossing aside plans to become fully for-profit and instead embracing a hybrid structure where their nonprofit entity remains in charge. At $300 billion valuation, that's one expensive boomerang!

This new hybrid structure creates a fascinating tension. It’s pretty much like trying to drive a Ferrari while simultaneously pledging to use it primarily for charity work.

For those of us with skin in the AI game (and if you're reading this, I assume you're not still investing exclusively in rotary phone manufacturers), this forces a fundamental question: are we betting on companies that can quickly maximize quarterly returns, or those positioned for sustainable leadership in what might be humanity's most transformative technology since fire? (Okay, maybe the wheel too, but you get my point.)

Let's talk about the elephant (or should I say, window?) in the room: Microsoft (MSFT).

With billions invested in OpenAI, Redmond execs must be having interesting conversations about how this governance shift affects their investment.

Back in 2019, I actually relocated my portfolio to give Microsoft a heftier allocation precisely because of their OpenAI partnership – a decision that paid handsome dividends as their stock climbed.

The market's relatively muted reaction to OpenAI's latest twist suggests investors are taking a "wait and see" approach, which in investor-speak means "panicking quietly while maintaining a neutral facial expression."

My take? Microsoft's diverse portfolio provides insulation from OpenAI governance surprises, while still giving them prime access to cutting-edge AI.

They're essentially wearing a safety harness while rock climbing alongside a partner who might suddenly decide halfway up the cliff that they're now spiritually opposed to carabiners.

This governance seesaw creates ripple effects across the entire AI ecosystem so profound that even my normally tech-oblivious neighbor asked me about it between complaints about my unmowed lawn.

And last week at a dinner party, I watched several tech VCs nearly come to blows over OpenAI's structure.

"It's brilliant camouflage," one argued between bites of overpriced sushi. "They get to look responsible while still chasing unicorn valuations."

Another countered that the structure genuinely changes incentives, potentially slowing development but creating more sustainable long-term value than a well-diversified retirement portfolio.

Both perspectives directly influence where smart money flows in the AI sector – and where my own investment dollars are headed next quarter.

The timeline question becomes more critical for your investment approach than deciding when to leave for the airport (hint: earlier than you think).

Short-term players looking 1-2 years out should focus on companies monetizing existing AI capabilities – those turning the current generation of models into revenue streams faster than politicians turn scandals into fundraising opportunities.

For long-haul investors with 5+ year horizons, OpenAI's move suggests prioritizing companies with both substantial R&D investments and ethical frameworks for deployment more robust than my New Year's resolutions.

The days of "move fast and break things" may be yielding to "move thoughtfully and build lasting value" – at least in this corner of the tech universe, which frankly is refreshing in an era where most things are designed to last about as long as unrefrigerated seafood.

OpenAI's conversion to a public benefit corporation rather than remaining an LLC adds another fascinating wrinkle.

I recently shared an elevator with a corporate governance expert who called benefit corporations "the mullets of business structures – profit in the front, social responsibility in the back." But watching a $300 billion company embrace this model suggests we're witnessing a genuine shift.

For our portfolio, this means evaluating not just quarterly performance but the alignment between profit motives and ethical considerations.

My investment approach has evolved accordingly. I've built an AI portfolio resembling a well-balanced meal rather than just loading up on sugar.

The protein comes from established tech giants with significant AI investments – your Microsofts and Alphabets (GOOGL).

The complex carbs are specialized AI implementers actually generating revenue today, like Salesforce (CRM) and Nvidia (NVDA).

The vegetables (yes, eat your vegetables) are emerging innovators with strong ethical frameworks like C3.ai (AI), which has built responsible principles into its foundation, or LivePerson (LPSN) with its ethical approach to customer service AI.

And for dessert? A small slice of speculative moonshots like BigBear.ai (BBAI) or SoundHound AI (SOUN) because sometimes revolutionary returns come from unexpected places.

Last month, this philosophy led me to trim a position in a high-flying but ethically questionable AI startup that had tripled my initial investment.

Was walking away from potential gains painful? Like giving up the last slice of pizza.

But in the AI sector, today's ethical shortcuts often become tomorrow's regulatory nightmares or reputational disasters – a lesson I learned the hard way after an ill-advised investment in a facial recognition company that shall remain nameless (though their legal team certainly knows my name).

We are getting to the part of the cycle where tech could potentially be cannibalizing each other.

The fact is that the overall pie is not growing fast enough, and competition is.

Search is a massive market, and participants are all vying for ad dollars.

Once what was thought of as a duopoly is no longer that and Facebook and Google will need to fight that much harder to command the growth rates they were accustomed to.

The US consumer is gradually becoming weaker and allocating a bigger part of their budget to essentials.

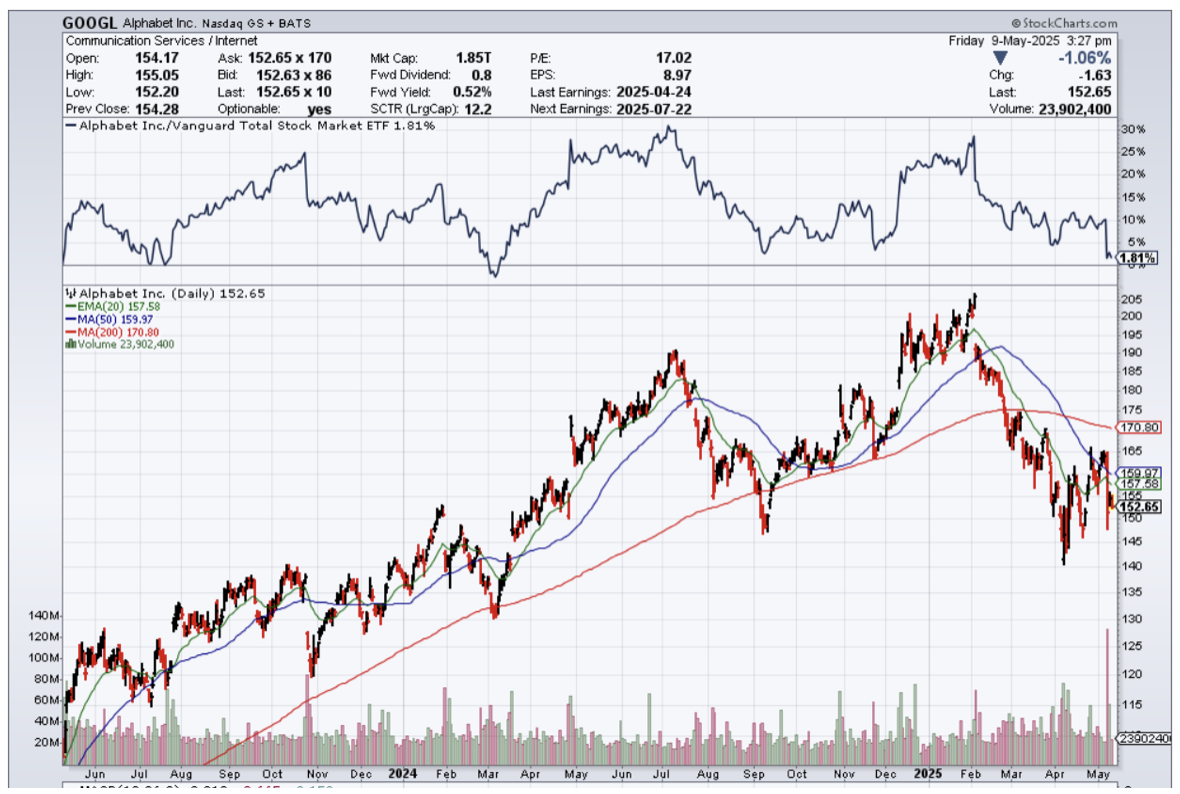

An Apple testimony by one of its executives has now revealed that search operations on Google via Apple's Safari browser decreased for the first time in April 2025, attributing this decline to users increasingly opting for AI-powered tools instead of traditional search engines.

Google’s parent stock Alphabet, was crushed in trading.

This time of development is really damaging for Google, and it puts doubt on their ability to negotiate higher ad rates moving forward.

The executive blamed AI platforms like OpenAI, Perplexity, and Anthropic as alternatives that are becoming more appealing to consumers, signaling a future where AI could play a central role in search functionalities on Apple devices.

The implications of Cue's testimony are profound, especially considering that Apple reportedly receives over $20 billion annually from Google to maintain its status as the default search engine on iPhones and iPads. This lucrative arrangement lies at the heart of the antitrust case brought by the U.S. Department of Justice against Google, raising questions about the competitive landscape of the search engine market.

The market believes that AI will disrupt Google's dominance in search. The decline in stock prices reflects investor anxiety about whether AI could significantly erode Google's market share, which currently stands at approximately 90% of the global search engine market, including a commanding 94% on mobile devices and 79% on desktops.

As the landscape of search technology evolves, the competition between traditional search engines like Google and emerging AI platforms will likely intensify.

As the antitrust case against Google unfolds, the stakes are high not only for the company but also for the broader tech ecosystem. The outcome could have lasting implications for how search engines operate and how consumers access information in the digital age.

Technology is barreling straight into a hairy situation in which the winner will take all in the AI race.

There won’t be enough profits to share around, and the company with the best product will win with consumers.

Search is just one place where AI is being fought.

I do believe we will see the fall of big tech companies, and the ones who are one-trick ponies will run the risk of becoming irrelevant quickly.

Is it fair?

No, but the market will tell us how good each tech companies does AI.

This is bad news for both Apple and Google, and it is not news that these two are lagging far behind in the AI arms race.

However, I do believe this is a good short-term buy-the-dip moment for Google for a trade.

With us moving deeper into 2025, investors are chomping at the bit to hear the commentary about AI developments.

There will be some big disappointments, are those companies unable to recover will be a sell the rallies type of stock.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-05-09 14:02:442025-05-09 16:06:53The Fight For AI Supremacy

“Any product that needs a manual to work is broken.” – Said CEO of Twitter Elon Musk

https://www.madhedgefundtrader.com/wp-content/uploads/2024/02/elon-musk.png370308Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2025-05-09 14:00:112025-05-09 16:06:33May 9, 2025 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.